|

시장보고서

상품코드

2043916

소 결핵 진단 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Bovine Tuberculosis Diagnosis - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

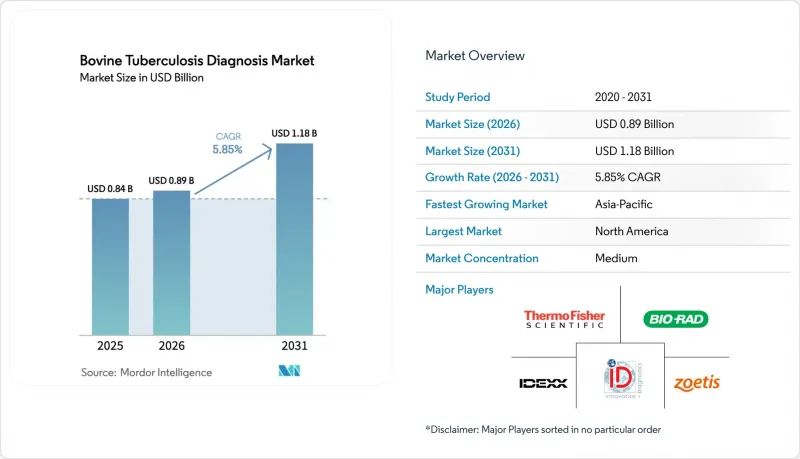

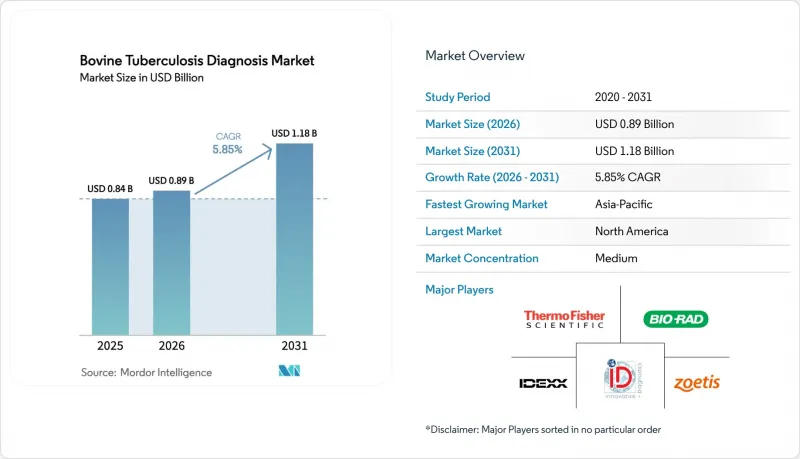

소 결핵 진단 시장 규모는 2025년에 8억 4,000만 달러로 평가되었습니다. 2026년 8억 9,000만 달러에서 2031년까지 11억 8,000만 달러에 이를 것으로 예측되며, 2026-2031년에 걸쳐 CAGR 5.85%를 나타낼 전망입니다.

젖소와 육우 사육두수 증가, 식품안전 규제 강화, 인수공통전염병에 대한 인식이 높아짐에 따라 검사 건수는 꾸준히 증가하는 추세입니다. 수출 지향적 낙농장의 의무적 모니터링, 보상형 도태 프로그램, 분자 검사에 대한 정부 자금 지원은 기본적인 수요를 촉진하고 있습니다. 분자진단 플랫폼, 특히 PCR 및 신흥 CRISPR 검사는 투베르쿨린 피부 반응 검사보다 더 일찍 감염을 감지할 수 있기 때문에 지속적으로 인기를 얻고 있습니다. 동시에 현장 배치가 가능한 AI 탑재 리더, 탄소배출권과 연계된 '결핵 없는' 라벨, 통합된 야생동물 모니터링은 새로운 경쟁 영역을 개척하고 있습니다.

세계의 소 결핵 진단 시장 동향과 인사이트

인수공통전염병으로서의 결핵 확산과 검사 및 살처분 프로그램

생우유를 통한 인수공통전염병의 전파가 공중보건에 경종을 울리고 있는 가운데 각국 정부는 모니터링 체계를 강화하고 있습니다. 남아시아에서는 특정 지역에서 M. orygis가 M. bovis를 능가하고 있어 소 이외의 동물에 대한 검사 확대가 요구되고 있습니다. 보상이 수반되는 살처분 조치로 인해 동물은 선별검사와 확진 검사를 모두 받게 되므로 검사 접점이 두 배로 늘어납니다. 2024년 한 해에만 영국은 수백만 파운드의 보상금을 지불했으며, 이는 강제 검사의 범위가 얼마나 확대되었는지를 잘 보여줍니다.

전 세계 소 사육두수 증가와 동물성 단백질 수요 증가

중국, 인도, 브라질, 멕시코의 급격한 가축군 확대로 인해 일상적인 모니터링에 대한 부담이 증가하고 있습니다. 미국 농무부(USDA)의 데이터에 따르면, 소 사육두수가 증가하는 미국 각 주에서 검사 건수가 증가하고 있으며, 이는 규모 확대와 진단 처리 능력의 상관관계를 뒷받침하고 있습니다. 생산자들은 진단 검사를 소의 도태를 막기 위한 보험료로 인식하고 있습니다. 생산자들은 예방적 진단을 단순한 규제상의 의무뿐만 아니라, 특히 결핵 미검출이 전두수 도태로 이어질 수 있는 경제적 리스크를 고려할 때 매우 중요한 리스크 관리 전략으로 인식하고 있습니다.

신흥 쇠고기 생산 지역의 제한된 수의학 인프라

동아프리카의 연구는 검사 능력, 인력 양성, 콜드체인 물류의 격차를 강조하고 있으며, 이 모든 것이 분자진단의 보급을 저해하고 있습니다. 검사 시설에서 멀리 떨어진 소규모 농업 종사자들은 피부 반응 검사에 의존할 수밖에 없고, 그 결과 초기 단계의 감염을 간과할 수밖에 없습니다. 검사의 질과 빈도의 지역적 격차는 복잡한 진단 절차에 대해 잘 알고 훈련된 수의사가 부족하기 때문입니다. 이러한 인력 부족은 특히 신흥 시장에서 소 사육두수의 대부분을 차지하는 소규모 농가의 경영에 큰 영향을 미치고 있습니다.

부문 분석

기존 피부반응 검사와 인터페론 감마 검사는 저렴한 가격과 규제 친화성으로 인해 2025년 소 결핵 진단 시장 점유율의 40.92%를 차지했습니다. 그러나 생산자들이 조기 발견을 우선시함에 따라 분자진단법은 CAGR 6.69%로 기존 검사법을 능가하는 성장세를 보이고 있습니다. CRISPR 분석은 현재 약 80분 만에 펨토몰 수준의 민감도를 구현하여 농장에서의 워크플로우와 실용성 간극을 좁히고 있습니다. PCR은 확립된 표준작업절차(SOP)가 있기 때문에 여전히 분자진단 시장 점유율을 지배하고 있지만, 차세대 시퀀싱과 CRISPR은 확진 검사 부문에서 틈새 시장을 개척하고 있습니다. 전통적인 접근법은 여전히 필수적인 선별 검사 도구이지만 무증상 환자를 감지할 수 없습니다는 단점이 있기 때문에 분자진단의 추진력이 지속되고 있습니다.

AI를 활용한 이미지 스코어링과 항원 기반 검사를 결합한 하이브리드 알고리즘에 대한 수요가 증가하고 있습니다. 이러한 플랫폼은 합리적인 가격을 유지하면서 정확도를 높이고, 실험실 인프라를 전면적으로 개편하지 않고도 단계적으로 업그레이드할 수 있는 중간 규모의 생산자에게 매력적인 타협안이 될 수 있습니다.

우유 품질과 수출에 대한 접근이 엄격하게 규제되는 젖소군은 2025년 소 결핵 진단 시장 규모의 68.18%를 차지했습니다. 집중적인 관리가 이뤄지는 목장에서는 검사 빈도가 높기 때문에 진단은 리스크 관리에 필수적인 요소로 자리 잡았습니다. 버팔로와 들소 떼는 CAGR 6.66%로 확대되고 있으며, 특히 인도와 미국에서는 자연보호와 상업적 목축이 겹치고 있습니다. 바이슨의 경구용 백신에 대한 조사는 야생동물과 가축의 접촉 지점에 대한 경각심이 높아졌음을 보여줍니다.

육용 소의 검사 빈도는 일반적으로 낮지만, 이동 전과 수출 관련 규제로 인해 검사 수요가 주기적으로 급증합니다. 사슴, 엘크, 오소리 등 야생 동물의 보균자 개체군에 대한 모니터링에 대한 자금 지원이 증가하면서 비침습적 샘플링 도구에 대한 틈새 수요가 생겨나고 있습니다.

지역별 분석

2025년에는 북미가 37.34%의 점유율로 1위를 차지했습니다. 이는 미국 농무부(USDA)의 100년 이상의 역사를 가진 근절 프로그램에 의해 뒷받침되고 있으며, 매년 수백만 마리의 소를 대상으로 검사를 실시하여 검사 대상 소 100만 마리당 약 7건의 사례가 확인되고 있습니다. 정부의 비용 보조로 PCR 검사에 대한 가격적인 우려가 해소되어 기술의 빠른 보급이 촉진되고 있습니다. 캐나다에서는 주별 구역제도에 따라 2024년부터 결핵 비발생 지역의 동물에 대한 검사가 폐지되었습니다. 이는 동적 위험 평가가 어떻게 지역 수요를 재구성하는지를 보여줍니다.

아시아태평양은 CAGR 6.48%로 가장 빠르게 성장하는 지역입니다. 중국의 확대되는 상업용 낙농장과 인도의 광범위한 소규모 농업인 네트워크는 모두 질병 관리를 강화하고 있지만, 인프라 격차는 여전히 남아 있습니다. 국제수역사무국(OIE)의 기준 조화에 따른 노력으로 국경 간 기준이 합리화되어 진단기기 공급업체가 지역 규모로 사업을 확장하기 쉬워지고 있습니다.

유럽에서는 엄격한 동물 위생 지침에 힘입어 견조한 수요가 유지되고 있습니다. 영국의 2024년 오소리 조사에서 일부 카운티에서 최대 14.5%의 감염률이 확인되어 야생동물 모니터링 예산이 유지되고 있습니다. EU의 지속가능성 정책은 비침습적 검사 및 저탄소 축산 라벨을 권장하고 있으며, 환경 DNA 키트 및 탄소 관련 인증 진단에 대한 관심을 높이고 있습니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The Bovine Tuberculosis Diagnosis Market size is projected to be USD 0.84 billion in 2025, USD 0.89 billion in 2026, and reach USD 1.18 billion by 2031, growing at a CAGR of 5.85% from 2026 to 2031.

Expanding dairy and beef herds, stricter food-safety rules, and rising zoonotic-disease awareness keep testing volumes on a steady upward path. Mandatory surveillance in export-oriented dairies, compensation-backed culling programs, and government funding for molecular assays reinforce baseline demand. Molecular platforms-particularly PCR and emerging CRISPR assays-continue to gain favor because they detect infection earlier than the tuberculin skin test. At the same time, field-deployable AI-enabled readers, carbon-credit-linked "TB-free" labels, and integrated wildlife monitoring open new competitive frontiers.

Global Bovine Tuberculosis Diagnosis Market Trends and Insights

Increasing Prevalence of Zoonotic TB & Test-and-Slaughter Programs

Governments intensify surveillance as zoonotic transmission from unpasteurized milk raises public-health alarms. In South Asia, M. orygis now eclipses M. bovis in certain pockets, prompting expanded testing beyond cattle. Compensation-backed culling doubles testing touchpoints because animals undergo both screening and confirmatory assays. The United Kingdom alone paid millions in indemnities during 2024, underscoring how large the compulsory-testing pool has become.

Growing Global Cattle Population & Rising Demand for Animal-Sourced Protein

Rapid herd expansion in China, India, Brazil, and Mexico boosts routine surveillance loads. USDA data show that testing volumes are climbing in U.S. states with herd growth, echoing the link between demographic scale and diagnostic throughput. Producers increasingly view diagnostics as an insurance premium against whole-herd depopulation. Producers increasingly view preventive diagnostics not just as a regulatory obligation, but as a crucial risk management strategy, especially given the economic stakes of undetected tuberculosis leading to the potential depopulation of entire herds.

Limited Veterinary Infrastructure in Emerging Beef-Producing Belts

East-African studies highlight gaps in lab capacity, workforce training, and cold-chain logistics, all of which blunt molecular expansion. Smallholders far from laboratories default to skin tests, leaving early infections unchecked. Geographic disparities in testing quality and frequency arise from a shortage of trained veterinary personnel adept at complex diagnostic procedures. This shortfall notably impacts smallholder operations, which account for substantial portions of cattle populations in emerging markets.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory Routine Screening in Export-Oriented Dairies

- Government Reimbursement for Advanced Molecular Tests

- High Cost & Cold-Chain Dependence of PCR Kits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Traditional skin and interferon-gamma assays held 40.92% of the Bovine tuberculosis diagnosis market share in 2025 thanks to low price and regulatory familiarity. Yet molecular methods are tracking a 6.69% CAGR, outpacing legacy tests as producers prioritize earlier detection. CRISPR assays now deliver femtomolar sensitivity in roughly 80 minutes, narrowing the practicality gap with on-farm workflows. PCR still dominates molecular share because of well-established SOPs, while next-generation sequencing and CRISPR are carving niches in confirmatory testing. Traditional approaches remain essential screening tools, but their inability to flag subclinical cases sustains molecular momentum.

Demand for hybrid algorithms that pair AI-enhanced image scoring with antigen-based tests is climbing. These platforms augment accuracy while preserving affordability, an attractive compromise for mid-scale producers seeking incremental upgrades without overhauling lab infrastructure.

Dairy herds, tightly regulated for milk quality and export access, generated 68.18% of the Bovine tuberculosis diagnosis market size in 2025. Intensively managed operations test more often, making diagnostics integral to risk management. Buffalo and bison herds are expanding at a 6.66% CAGR, notably in India and the United States where conservation and commercial ranching overlap. Oral vaccine research in bison underscores the heightened vigilance around wildlife-livestock interfaces.

Beef cattle generally test less frequently, but pre-movement and export rules create periodic surges. Wildlife reservoirs-deer, elk, badgers-are attracting funding for surveillance, opening niche demand for non-invasive sampling tools.

The Bovine Tuberculosis Diagnosis Market Report is Segmented by Test Type (Serological Tests [ELISA Kits and More] and More), Animal Type (Dairy Cattle and More), Sample Type (Blood and More), End-User (Veterinary Reference Laboratories and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 37.34% share in 2025, anchored by USDA's century-old eradication program that screens millions annually, generating roughly 7 cases per million cattle inspected. Government reimbursement removes price objections to PCR, encouraging rapid technology turnover. Canada's province-based zoning eliminated tests for animals from tuberculosis-free regions in 2024, illustrating how dynamic risk assessments reshape local demand.

Asia-Pacific is the fastest-growing region at a 6.48% CAGR. China's expanding commercial dairies and India's large smallholder network are both tightening disease controls, though infrastructure gaps linger. Harmonization work by the World Organisation for Animal Health is streamlining cross-border standards, making it easier for diagnostic suppliers to scale regionally.

Europe, backed by stringent animal-health directives, sustains robust demand. The UK's 2024 badger survey found prevalence rates up to 14.5% in some counties, keeping wildlife surveillance budgets intact. EU sustainability policies favor non-invasive testing and low-carbon livestock labels, fueling interest in environmental DNA kits and carbon-linked certification diagnostics.

- Abbott Laboratories

- AsureQuality

- bioMerieux

- Bionote

- Bio-Rad Laboratories

- Creative Diagnostics

- Enfer Group

- Hangzhou Frenovo Biotech Co., Ltd.

- IDEXX

- Innovative Diagnostics SAS (IDvet)

- Neogen

- QIAGEN

- Randox Food Diagnostics

- Sansure Biotech

- Thermo Fisher Scientific

- Zoetis

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing prevalence of zoonotic TB & test-and-slaughter programs

- 4.2.2 Growing global cattle population & rising demand for animal-sourced protein

- 4.2.3 Mandatory routine screening in export-oriented dairies

- 4.2.4 Government reimbursement for advanced molecular tests

- 4.2.5 AI-enabled image-based field diagnostics gaining VC funding

- 4.2.6 Carbon-credit linked "low-methane, TB-free" certification premiums

- 4.3 Market Restraints

- 4.3.1 Limited veterinary infrastructure in emerging beef-producing belts

- 4.3.2 High cost & cold-chain dependence of PCR kits

- 4.3.3 Farmer resistance to mandatory culling despite compensation

- 4.3.4 Strain diversity causing false negatives in wildlife reservoirs

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Test Type

- 5.1.1 Serological Tests

- 5.1.1.1 ELISA Kits

- 5.1.1.2 Agglutination / Lateral-flow

- 5.1.2 Molecular Diagnostic Tests

- 5.1.2.1 PCR

- 5.1.2.2 NGS & CRISPR-based Assays

- 5.1.3 Traditional Tests

- 5.1.3.1 Tuberculin Skin Test

- 5.1.3.2 Gamma-Interferon Assay

- 5.1.1 Serological Tests

- 5.2 By Animal Type

- 5.2.1 Dairy Cattle

- 5.2.2 Beef Cattle

- 5.2.3 Buffalo & Bison

- 5.3 By Sample Type

- 5.3.1 Blood

- 5.3.2 Milk

- 5.3.3 Tissue / Lesion

- 5.3.4 Fecal & Environmental Swab

- 5.4 By End-User

- 5.4.1 Veterinary Reference Laboratories

- 5.4.2 On-farm / Point-of-care Settings

- 5.4.3 Government Agencies & Animal Health Departments

- 5.4.4 Academic & Research Institutes

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Competitive Benchmarking

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Abbott Laboratories

- 6.4.2 AsureQuality

- 6.4.3 BioMerieux SA

- 6.4.4 Bionote

- 6.4.5 Bio-Rad Laboratories

- 6.4.6 Creative Diagnostics

- 6.4.7 Enfer Group

- 6.4.8 Hangzhou Frenovo Biotech Co., Ltd.

- 6.4.9 IDEXX Laboratories

- 6.4.10 Innovative Diagnostics SAS (IDvet)

- 6.4.11 Neogen Corporation

- 6.4.12 Qiagen N.V.

- 6.4.13 Randox Food Diagnostics

- 6.4.14 Sansure Biotech

- 6.4.15 Thermo Fisher Scientific Inc

- 6.4.16 Zoetis Inc

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment