|

시장보고서

상품코드

2043931

식물 추출물 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Plant Extracts - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

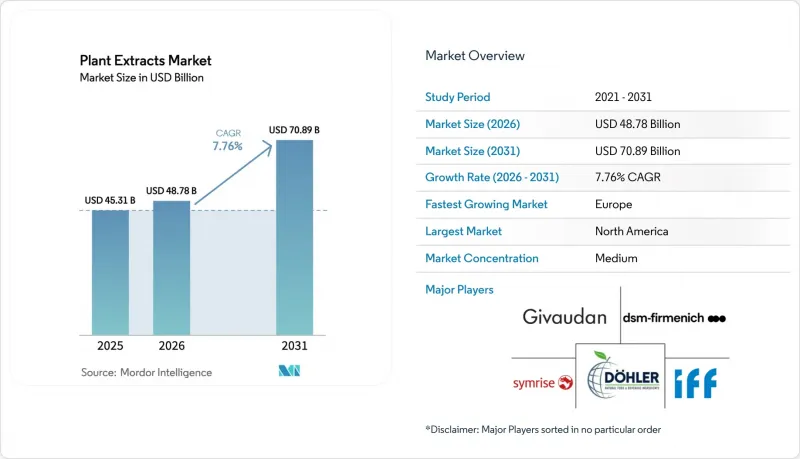

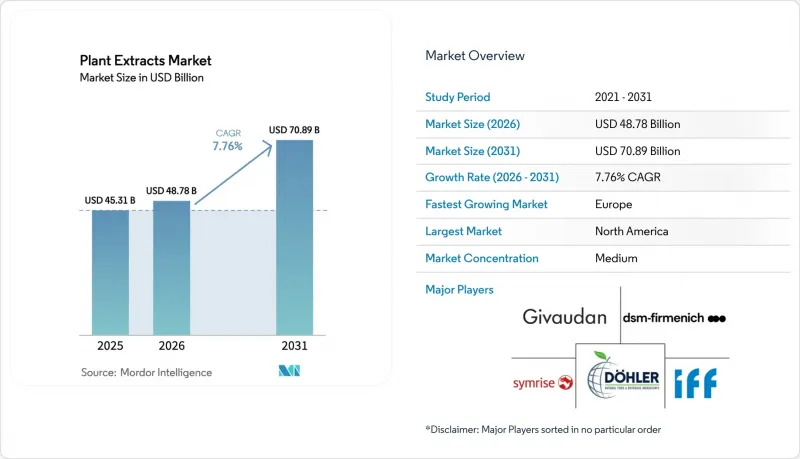

식물 추출물 시장 규모는 2025년에 453억 1,000만 달러로 평가되었습니다. 2026년 487억 8,000만 달러에서 2031년까지 708억 9,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 7.76%를 나타낼 전망입니다.

이러한 확대는 클린 라벨로의 제품 재구성, AI를 활용한 식물 화학물질의 발견, 미국의 새로운 식품 성분의 승인 경로를 명확히 하는 규정의 발전과 유럽의 신규 식품(Novel Foods) 승인에 힘입어 더욱 가속화되고 있습니다. 다국적 향료 기업들은 블록체인을 활용한 추적성에 기반한 수직 통합형 공급망을 활용하여 부정 혼입의 위험을 줄이고 있습니다. 바이오리파이너리 프로젝트는 농업 폐기물을 가치 있는 식물성 유효 성분으로 전환하여 순환 경제의 목표를 지원하고 있습니다. 초임계 CO2 추출법, 효소 보조 추출법, 초음파 보조 추출법 등 첨단 추출 기술을 통해 용매 사용량과 에너지 소비를 최소화하고 있습니다. 동시에 식품 안전 정책으로 인해 제조업체들은 합성 첨가물을 식물성 대체품으로 대체하도록 장려하고 있으며, 이는 기능성 식품, 영양 보충제, 화장품 및 동물사료에 식물성 성분의 채택을 촉진하고 있습니다.

세계의 식물 추출물 시장 동향 및 인사이트

클린 라벨 수요 급증

합성첨가물에 대한 소비자의 거부감으로 인해 가공식품, 음료, 퍼스널케어 제품에서 제품 재배합의 속도가 빨라지고 있습니다. 북미에서는 새로 출시되는 식품 및 음료에 클린 라벨을 표시하는 것이 점점 더 눈에 띄게 증가하고 있습니다. 소매업체들은 원재료의 투명성을 요구하고 있으며, 식물 추출물의 원산지와 가공 방법을 명시할 수 없는 브랜드는 판매 중단의 위험에 직면해 있습니다. 이러한 추세는 유럽연합(EU)에서 특히 두드러지는데, '농장에서 식탁까지(Farm to Fork)' 전략과 제안된 '패키지 전면 영양표시(Front-of-Pack Nutrition Labelling)' 규정으로 인해 제조업체는 제3자 인증을 통해 '천연' 표시를 제3자 인증을 통해 '천연' 표시를 뒷받침해야 합니다. 이에 따라 유기농 인증 및 비유전자변형(Non-GMO) 식물 추출물에 대한 수요가 증가하고 있습니다. 클린 라벨의 흐름은 착색용 추출물 수요에도 변화를 가져오고 있습니다. 여러 지역에서 합성색소가 금지되면서 제품 개발자들은 자색당근에서 추출한 안토시아닌, 스피룰리나에서 추출한 피코시아닌, 강황에서 추출한 커큐민과 같은 대체품을 선택하게 되었습니다. 그러나 이러한 천연 유래의 선택은 높은 비용, 산성 환경이나 고온 환경에서의 안정성 문제 등 여러 가지 문제를 안고 있습니다.

건강기능식품 규제 확대

규제가 명확해짐에 따라 식물성 보충제 시장 진입이 쉬워졌지만, 컴플라이언스의 복잡성은 여전히 중소 제조업체에게 도전이 되고 있습니다. 2024년 9월, FDA는 신규 식품 성분에 대한 가이던스를 업데이트하여 미국에서 판매되지 않은 식물 추출물에 대한 시판 전 신고 요건을 명확히 했습니다. 이번 업데이트는 새로운 식물화학물질을 도입하는 제품 개발자들의 불확실성을 줄여주었습니다. 유럽에서는 유럽식품안전청(EFSA)이 2025년 4월 'Novel Foods Compendium'을 개정하여 식물 추출물의 허가 절차를 간소화하기 위해 식물 안전성 평가의 일원화된 데이터베이스를 구축했습니다. 예를 들어, 노란 토마토 추출물은 2025년 11월에 하루 최대 30밀리그램의 용량으로 건강기능식품에 사용할 수 있도록 승인되었습니다. 마찬가지로, 2024년 인도 식품안전기준청(FSSAI)은 영양보충제 표시기준을 개정하여 중금속, 농약잔류물, 미생물 오염물질에 대한 로트별 검사를 의무화했습니다. 이러한 기준은 품질 기준을 높이는 한편, 국내 제조업체의 컴플라이언스 비용도 증가시키고 있습니다. 이러한 규제 변화는 주류 건강 관련 채널에서 식물 추출물의 정당성을 뒷받침하는 것이지만, 막대한 검사 및 문서화 비용을 부과하여 지역 공급업체보다 수직적으로 통합된 다국적 기업에 유리하게 작용하는 경향이 있습니다.

원자재 가격 변동

2024년, 마다가스카르의 바닐라 농장은 사이클론으로 인해 큰 피해를 입었습니다. 여기에 중개업자들의 투기적 매수세가 겹치면서 바닐라 가격이 급등했습니다. 이러한 가격 폭등으로 인해 향료 제조업체들은 합성 바닐린을 대체재로 사용하거나 우간다, 파푸아뉴기니 등 다른 지역에서 대체 공급처를 찾아야 하는 상황에 처하게 되었습니다. 동시에 기후 변화로 인해 커피 체리 재배에 적합한 지역이 변화하고 있으며, 이는 에너지 음료와 노오트로픽 보충제에 사용되는 이 인기 있는 원료공급 제약으로 이어지고 있습니다. 예측에 따르면, 브라질의 아라비카 커피 수확량이 감소할 것으로 예상되며, 이는 이러한 문제를 더욱 심각하게 만들 것으로 보입니다. 이러한 공급의 혼란에 대응하기 위해 도러(Dohler)나 마틴 바우어(Martin Bauer)와 같은 기업들은 수직적 통합 전략을 채택하고 있습니다. 이들 기업은 장기적으로 안정적이고 예측 가능한 공급을 확보하기 위해 계약 농업에 대한 투자 및 농림복합경영(Agroforestry) 파트너십 구축에 힘쓰고 있습니다. 그러나 자금력이 부족한 중소 배합업체는 이와 같은 전략을 실행할 수 없어 현물시장 가격 변동에 영향을 많이 받는 상황입니다.

부문 분석

2025년, 허브 및 식물 추출물은 식물 추출물 시장 점유율의 36.02%를 차지했습니다. 커큐미노이드 95%의 표준화된 강황과 5%의 위타놀라이드를 함유한 아슈와간다(Ashwagandha)가 스트레스 및 염증 완화 제품 부문을 주도하고 있습니다. 원자재 생산 증가로 인해 공급망이 강화되고 있습니다. 예를 들어, 인도 농업 및 농민 복지부에 따르면 인도의 심황 생산량은 2024년 102만 톤에서 2025년 120만 톤으로 증가했습니다. 한편, 식물 추출물 시장에서 가장 높은 성장률을 나타낼 것으로 예측되는 것은 에센셜 오일로, CAGR은 8.10%로 예상됩니다. 이러한 성장은 클린 라벨 육류 제품에서 벤조산나트륨 대신 항균 작용을 하는 오레가노와 타임 오일을 사용하고, 기능성 음료에 라벤더와 페퍼민트를 배합하여 라벤더와 페퍼민트에 대한 수요가 증가하고 있기 때문으로 분석됩니다.

소비자의 취향이 합성 향료에서 멀어짐에 따라 스낵의 코팅에 올레오레진이 점점 더 많이 사용되고 있습니다. 또한, 레스베라트롤과 같은 식물성 화학물질의 분리물은 임상 영양 분야에서 프리미엄급으로 자리매김하고 있습니다. EU의 아라라레드 AC 규제 금지에 따라 스피루리나, 파프리카, 비트 뿌리에서 추출한 천연 색소 추출물에 대한 수요가 증가하고 있습니다. 그러나 백단향, 유향, 바닐라의 산지가 지리적으로 집중되어 있어 공급망의 취약성은 여전히 남아있습니다.

허브와 향신료는 2025년 총량의 51.89%를 차지했으며, 이는 아유르베다와 중국 전통의학(TCM)에서 허브와 향신료가 얼마나 중요한 역할을 하는지를 보여줍니다. 그러나 과일 및 채소는 CAGR 8.36%라는 괄목할 만한 성장세를 보이며 향후 급성장할 것으로 예측됩니다. 이러한 상승세는 안정적인 원자재 공급이 뒷받침되고 있으며, 특히 미국 농무부 해외농업국(USDA Foreign Agricultural Service)이 브라질의 오렌지 생산량을 1,350만 톤으로 보고하고 있다는 점이 주목됩니다. 한편, 안토시아닌이 풍부한 블루베리와 엘더베리 추출물은 심혈관계 및 인지기능 건강을 목표로 하는 제형에 포함되고 있습니다. 또한 감귤류 폐기물은 현재 헤스페리딘, d-리모넨, 펙틴 등 고부가가치 제품으로 전환되고 있으며, 과거 매립처리 비용이었던 감귤류 폐기물이 수익성 높은 사업으로 탈바꿈하고 있습니다.

토마토 가공 제품 중 하나인 토마토 착즙 찌꺼기는 자외선 차단제나 전립선 건강 유지에 효과가 있는 것으로 널리 알려진 리코펜으로 효과적으로 전환됩니다. 이 혁신은 과일 유래 식물 추출물 시장의 확대에 크게 기여하고 있습니다. 계절성에 따른 문제를 완화하기 위해 기업들은 동결건조 터널, 콜드체인 물류 등 첨단 기술에 대한 투자를 확대되고 있습니다. 이러한 투자는 원재료의 안정적이고 지속적인 공급을 보장하는 데 필수적이며, 이는 곧 시장의 지속적인 성장을 뒷받침할 수 있습니다.

식물 추출물 시장 보고서는 제품 유형(정유, 올레오레진 등), 원료원(허브-향신료, 과일-채소, 꽃 등), 형태(분말 등), 용도(식품-음료, 건강보조식품-기능성 식품 등), 지역(북미, 유럽, 아시아태평양 등)별로 분류하여 조사하였습니다. 시장 예측은 금액(USD) 및 수량(톤)으로 제공됩니다.

지역별 분석

2025년 북미는 전 세계 매출의 36.03%를 차지했으며, 이는 미국의 600억 달러 규모의 건강보조식품 시장이 주도할 것으로 예측됩니다. 캐나다의 천연 건강 제품 부문은 투명성이 높은 공급망과 제3자 인증을 중시함으로써 표준화된 식물 추출물에 대한 수요를 더욱 촉진했습니다. FDA는 2024년 9월 식물 성분에 관한 지침 개정판을 도입하여 새로운 식품 성분에 대한 신고 요건을 명확히 했습니다. 이번 개정으로 CBD, 라이온스 메인 버섯, 시모스 등 신규 식물 성분을 도입하는 제제 개발자들에게 규제상의 불확실성이 줄어들게 되었습니다. 2025년과 2026년에는 사모펀드 활동이 급증했으며, 2026년 2월 더 리버사이드 컴퍼니(The Riverside Company)의 웨스턴 보태니컬스(Western Botanicals) 인수와 몬테레이 베이 허브 컴퍼니(Monterey Bay Herb Company)의 NP 뉴트라(NP Neutra) 인수가 주목을 받았습니다. 이러한 움직임은 산업 재편에 따른 수익률 확대와 교차판매 기회에 대한 투자자들의 신뢰를 반영하고 있습니다. 멕시코의 식물추출물 부문은 규모는 작지만 미국 시장과의 근접성, 낮은 인건비 등의 장점이 있습니다. Canurta Naturals와 같은 기업들은 이동식 추출 실험실을 도입하여 대마초와 대마의 바이오매스를 현지에서 가공함으로써 운송 비용을 절감하고 휘발성이 높은 테르펜을 보존하고 있습니다.

유럽 시장은 2031년까지 연평균 8.78% 성장할 것으로 예상되며, 지역별로 가장 높은 성장률을 보이고 있습니다. 이러한 성장은 유럽식품안전청(EFSA)의 신규 식품(Novel Foods) 승인과 유기농 인증 및 이력 추적이 가능한 원료에 대한 소비자 수요 증가에 힘입은 바 있습니다. 2025년 4월, EFSA는 '식물 성분 총람(Compendium of Botanicals)'을 업데이트하여 안전성 평가가 완료된 1,600여 종의 식물을 등재했습니다. 이번 개정은 승인 절차를 간소화하고, 신규 추출물 시장 출시 기간을 단축하는 것을 목표로 하고 있습니다. 예를 들어, 노란 토마토 추출물은 2025년 11월에 하루 최대 30밀리그램의 용량으로 건강 보조 식품에 사용할 수 있도록 승인되었습니다. 규제 승인을 위해서는 독성 시험, 알레르기 평가 및 영향 분석이 필요했습니다. 유럽 최대 시장인 독일은 식물성 의약품 분야에서 선도적인 역할을 하고 있습니다. 세인트존스워트, 발레리안, 은행잎 등의 식물 추출물은 특정 적응증에서 법정 건강 보험 적용을 받고 있으며, 이로 인해 건강기능식품과는 다른 의약품 등급공급망을 형성하고 있습니다. 영국은 브렉시트 이후에도 EU의 새로운 식품 규정을 계속 준수하는 한편, 영연방 국가에서 안전성이 확립된 식물 성분에 대해서는 보다 신속한 승인 절차를 모색하고 있습니다. 한편, 프랑스와 이탈리아에서는 유기농 및 바이오다이내믹 인증이 우선시되고 있습니다. 이들 국가의 소비자들은 에코서트(Ecocert)나 데미터(Demeter) 인증을 받은 식물 추출물에 대해 20-30%의 추가 비용을 지불할 의향이 있으며, 이는 재생농업 기반 조달 모델에 대한 수요를 견인하고 있습니다.

아시아태평양, 남미, 중동 및 아프리카는 식물 추출물 시장의 주요 성장 지역으로 부상하고 있습니다. 중국과 인도는 주요 생산국이자 동시에 확대되는 소비시장이라는 이중의 역할을 하고 있습니다. 1,500억 달러 이상의 규모를 자랑하는 중국 전통의학(TCM) 분야는 생약 조제에서 표준화된 추출물 제제로 전환하고 있습니다. 이러한 전환은 국가약품감독관리국의 현대화 노력과 우수의약품제조관리기준(GMP)의 시행으로 뒷받침되고 있습니다. 인도에서는 구자라트, 마하라슈트라, 타밀나두 주에 집중된 식물 추출물 산업이 심황, 아슈와간다, 바코파 모니에리 추출물을 세계 시장에 공급하고 있습니다. 그러나 이 산업은 품질 관리 및 위조와 관련된 문제에 직면하고 있으며, 이는 수출 경쟁력에 영향을 미치고 있습니다. 태국과 인도네시아는 유리한 기후와 정부의 수출 촉진 프로그램을 활용하여 망고스틴, 모링가, 크라톰 등 열대 식물 원료의 비용 효율적인 조달 거점으로 자리매김하고 있습니다. 아마존 열대우림과 세라드 사바나를 포함한 브라질의 생물다양성은 아사이, 갈라나, 코파이바 오일과 같은 새로운 식물 추출물에 있어 큰 잠재력을 가지고 있습니다. 그러나 지속 가능한 조달에 대한 인증의 부재와 원주민의 권리에 대한 미비한 프레임워크는 브라질에서 조달하는 다국적 바이어에게 평판 리스크를 초래하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액 및 수량)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The Plant Extracts Market size was valued at USD 45.31 billion in 2025 and is estimated to grow from USD 48.78 billion in 2026 to reach USD 70.89 billion by 2031, at a CAGR of 7.76% during the forecast period (2026-2031).

This expansion is fueled by clean-label reformulations, AI-driven phytochemical discoveries, and regulatory advancements clarifying new dietary ingredient pathways in the U.S. and Novel Foods authorizations in Europe. Multinational flavor companies are utilizing vertically integrated supply chains, supported by blockchain-enabled traceability to reduce adulteration risks. Biorefinery projects are converting agricultural waste into valuable botanical actives, supporting circular economy objectives. Advanced extraction technologies, such as supercritical CO2, enzyme-assisted, and ultrasonic-assisted methods, are minimizing solvent use and energy consumption. Simultaneously, food security policies are encouraging manufacturers to replace synthetic additives with botanical alternatives, driving their adoption in functional foods, dietary supplements, cosmetics, and animal nutrition.

Global Plant Extracts Market Trends and Insights

Surge in clean-label demand

Consumer rejection of synthetic additives is driving faster reformulation timelines across packaged foods, beverages, and personal care products. In North America, clean-label claims are increasingly featured in new food and beverage launches. Retailers are enforcing ingredient transparency, and brands face the risk of delisting if they fail to disclose the origins or processing methods of botanical extracts. This trend is particularly prominent in the European Union, where the "Farm to Fork" strategy and the proposed "Front-of-Pack Nutrition Labelling" regulation require manufacturers to validate "natural" claims through third-party certifications. This has increased demand for organic-certified and non-GMO botanical extracts. The clean-label movement is also transforming the demand for color extracts. As synthetic dyes are banned in various regions, formulators are opting for alternatives such as anthocyanins from purple carrots, spirulina-derived phycocyanin, and turmeric-based curcumin. However, these natural options present challenges, including higher costs and stability issues in acidic or high-temperature environments.

Expansion of nutraceutical regulations

Regulatory clarity is enhancing market access for botanical supplements, but compliance complexities continue to challenge smaller players. In September 2024, the FDA released updated guidance on new dietary ingredients, specifying pre-market notification requirements for botanical extracts not previously marketed in the U.S. This update reduces uncertainty for formulators introducing novel phytochemicals. In Europe, the European Food Safety Authority revised its Novel Foods Compendium in April 2025, creating a centralized database of botanical safety assessments to simplify authorization pathways for extracts. For example, yellow tomato extract received approval in November 2025 for use in food supplements at doses up to 30 milligrams per day. Similarly, in 2024, India's Food Safety and Standards Authority introduced updated labeling standards for nutraceuticals, requiring batch-specific testing for heavy metals, pesticide residues, and microbial contaminants. While these standards raise quality benchmarks, they also increase compliance costs for domestic manufacturers. These regulatory changes validate botanical extracts in mainstream health channels but impose significant testing and documentation costs, which tend to benefit vertically integrated multinationals over regional suppliers.

Raw-material price volatility

In 2024, Madagascar's vanilla plantations suffered significant damage due to a cyclone, which, combined with speculative hoarding by intermediaries, caused a sharp increase in vanilla prices. This price surge compelled flavor houses to adapt by either utilizing synthetic vanillin as a substitute or exploring alternative sourcing options in regions such as Uganda and Papua New Guinea. At the same time, climate change is altering the geographic viability of coffee-cherry cultivation, leading to supply constraints for this increasingly popular ingredient used in energy drinks and nootropic supplements. Projections indicate a decline in arabica coffee yields in Brazil, further exacerbating these challenges. In response to such disruptions, companies like Dohler and Martin Bauer are adopting vertical integration strategies. They are investing in contract farming and establishing agroforestry partnerships to ensure a stable and predictable supply over the long term. However, smaller formulators, constrained by limited financial resources, are unable to implement similar strategies and remain highly susceptible to the volatility of spot-market pricing.

Other drivers and restraints analyzed in the detailed report include:

- Growth of vegan and plant-based diets

- Advances in green extraction technologies

- Adulteration and quality concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, herbal and botanical extracts accounted for 36.02% of the plant extract market share. Turmeric, standardized to 95% curcuminoids, and ashwagandha, containing 5% withanolides, dominate the segment for stress and inflammation products. Increased raw material production strengthens the supply chain. For instance, India's turmeric production rose from 1.02 million metric tons in 2024 to 1.20 million metric tons in 2025, according to the Ministry of Agriculture and Farmers Welfare. Meanwhile, essential oils are projected to register the fastest growth in the plant extract market, with an 8.10% CAGR. This growth is driven by antimicrobial oregano and thyme oils replacing sodium benzoate in clean-label meats and rising demand for lavender and peppermint due to their integration into functional beverages.

As consumer preference shifts away from synthetic flavors, oleoresins are increasingly used in snack coatings. Additionally, phytochemical isolates like resveratrol are securing a premium position in clinical nutrition. Natural color extracts from spirulina, paprika, and beetroot are gaining momentum following regulatory bans on Allura Red AC in the EU. However, supply chain vulnerabilities persist due to the geographic concentration of sandalwood, frankincense, and vanilla.

Herbs and spices accounted for 51.89% of the 2025 volumes, underscoring their deep-rooted significance in Ayurveda and Traditional Chinese Medicine (TCM). Yet, fruits and vegetables are set to surge ahead, boasting an impressive 8.36% CAGR. This uptick is bolstered by a steady supply of raw materials, highlighted by Brazil's USDA Foreign Agricultural Service reporting the country's orange production at a notable 13.5 million metric tons. Meanwhile, extracts from anthocyanin-rich blueberries and elderberries are being integrated into formulations targeting cardiovascular and cognitive health. Additionally, citrus waste streams are now being transformed into valuable products like hesperidin, d-limonene, and pectin, turning what was once a landfill cost into a profitable venture.

Tomato pomace, a by-product of tomato processing, is being effectively converted into lycopene, which is widely recognized for its benefits in sun-care and prostate health applications. This innovation is significantly contributing to the expansion of the market for fruit-derived plant extracts. To mitigate the challenges posed by seasonality, companies are increasingly investing in advanced technologies such as freeze-drying tunnels and cold-chain logistics. These investments are critical in ensuring a stable and uninterrupted supply of raw materials, thereby supporting the sustained growth of the market.

The Plant Extract Market Report is Segmented by Product Type (Essential Oils, Oleoresins, and More), Source (Herbs and Spices, Fruits and Vegetables, Flowers, and More), Form (Powder, and More), Application (Food and Beverages, Dietary Supplements and Functional Foods, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

Geography Analysis

In 2025, North America contributed 36.03% of global revenue, driven by the U.S.'s USD 60 billion dietary-supplement market. Canada's natural-health-products sector further supported the demand for standardized botanical extracts, emphasizing transparent supply chains and third-party certifications. The FDA introduced an updated botanical-guidance framework in September 2024, clarifying new-dietary-ingredient notification requirements. This update reduced regulatory uncertainties for formulators introducing novel botanicals like CBD, lion's mane mushroom, and sea moss. Private-equity activity surged in 2025 and 2026, highlighted by The Riverside Company's acquisition of Western Botanicals in February 2026 and Monterey Bay Herb Co.'s purchase of NP Nutra. These developments reflected investor confidence in consolidation-driven margin expansion and cross-selling opportunities. Although Mexico's botanical-extract sector is smaller, its proximity to U.S. markets and lower labor costs provide advantages. Companies such as Canurta Naturals are deploying mobile extraction labs to process cannabis and hemp biomass on-site, cutting transportation costs and preserving volatile terpenes.

Europe is projected to grow at 8.78% through 2031, marking the fastest regional growth rate. This growth is supported by the European Food Safety Authority's (EFSA) Novel Foods authorizations and increasing consumer demand for organic-certified, traceable ingredients. In April 2025, the EFSA updated its Compendium of Botanicals, listing over 1,600 plant species with safety assessments. This update aims to streamline authorization pathways and reduce time-to-market for novel extracts. For example, yellow tomato extract was authorized in November 2025 for use in food supplements at doses of up to 30 milligrams per day. Its regulatory approval required toxicological studies, allergenicity assessments, and nutritional-impact analyses. Germany, the largest market in Europe, leads in herbal medicinal products. Botanical extracts such as St. John's wort, valerian, and ginkgo biloba are reimbursed under statutory health insurance for specific indications, creating a pharmaceutical-grade supply chain distinct from dietary supplements. The UK, in its post-Brexit phase, continues to align with EU Novel Foods regulations while exploring faster approval pathways for botanicals with established safety records in Commonwealth nations. Meanwhile, France and Italy are prioritizing organic and biodynamic certifications. Consumers in these countries are willing to pay 20-30% premiums for Ecocert and Demeter-certified botanical extracts, driving demand for regenerative-agriculture sourcing models.

Asia-Pacific, South America, and the Middle East and Africa are emerging as key growth regions in the botanical extract market. China and India are playing dual roles as major producers and expanding consumer markets. China's Traditional Chinese Medicine sector, valued at over USD 150 billion, is shifting from raw-herb dispensing to standardized extract formulations. This transition is supported by modernization initiatives from the National Medical Products Administration and the enforcement of Good Manufacturing Practices. In India, the botanical-extract industry, concentrated in Gujarat, Maharashtra, and Tamil Nadu, supplies global markets with turmeric, ashwagandha, and Bacopa monnieri extracts. However, the industry faces challenges related to quality control and adulteration, which impact export competitiveness. Thailand and Indonesia are positioning themselves as cost-effective sourcing hubs for tropical botanicals such as mangosteen, moringa, and kratom, leveraging favorable climates and government export-promotion programs. Brazil's biodiversity, encompassing the Amazon rainforest and Cerrado savanna, offers significant potential for novel botanical extracts like acai, guarana, and copaiba oil. However, the lack of sustainable-sourcing certifications and underdeveloped indigenous-rights frameworks poses reputational risks for multinational buyers sourcing from Brazil.

- Givaudan SA

- DSM-Firmenich AG

- Symrise AG

- International Flavors and Fragrances Inc.

- Dohler GmbH

- Kalsec Inc.

- Indena SpA

- Archer Daniels Midland Company

- Martin Bauer Group

- Sensient Technologies Corp.

- Ransom Naturals Ltd.

- Frutarom Industries Ltd.

- Arjuna Natural Pvt. Ltd.

- Blue Sky Botanics Ltd.

- Botanica GmbH

- Vidya Herbs Pvt. Ltd.

- Nutra Green Biotechnology Co., Ltd.

- Shaanxi Jiahe Phytochem

- Nexira SAS

- PT Indesso Aroma

- Sabinsa Corporation

- Layn Natural Ingredients Corp.

- OmniActive Health Technologies

- PureCircle (by Ingredion)

- Xi'an Shengtian Bio-chemical Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in clean-label demand

- 4.2.2 Expansion of nutraceutical regulations

- 4.2.3 Growth of vegan and plant-based diets

- 4.2.4 Advances in green extraction technologies

- 4.2.5 Commercial biorefinery-driven agri-waste valorization

- 4.2.6 Integration of AI-led phytochemical discovery pipelines

- 4.3 Market Restraints

- 4.3.1 Raw-material price volatility

- 4.3.2 Adulteration and quality concerns

- 4.3.3 Regulatory inconsistencies worldwide

- 4.3.4 Limited clinical-efficacy data

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Product Type

- 5.1.1 Essential Oils

- 5.1.2 Oleoresins

- 5.1.3 Herbal and Botanical Extracts

- 5.1.4 Phytochemical Isolates

- 5.1.5 Natural Color Extracts

- 5.1.6 Flavour and Fragrance Extracts

- 5.2 By Source

- 5.2.1 Herbs and spices

- 5.2.2 Fruits and vegetables

- 5.2.3 Flowers

- 5.2.4 Roots and Rhizomes

- 5.2.5 Seeds and Grains

- 5.3 By Form

- 5.3.1 Powder

- 5.3.2 Liquid

- 5.3.3 Crystals and Granules

- 5.4 By Application

- 5.4.1 Food and Beverages

- 5.4.2 Dietary Supplements and Functional Foods

- 5.4.3 Pharmaceuticals

- 5.4.4 Cosmetics and Personal Care

- 5.4.5 Animal Nutrition

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Sweden

- 5.5.2.8 Belgium

- 5.5.2.9 Poland

- 5.5.2.10 Netherlands

- 5.5.2.11 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Thailand

- 5.5.3.5 Singapore

- 5.5.3.6 Indonesia

- 5.5.3.7 South Korea

- 5.5.3.8 Australia

- 5.5.3.9 New Zealand

- 5.5.3.10 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 South Africa

- 5.5.5.3 Saudi Arabia

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Givaudan SA

- 6.4.2 DSM-Firmenich AG

- 6.4.3 Symrise AG

- 6.4.4 International Flavors and Fragrances Inc.

- 6.4.5 Dohler GmbH

- 6.4.6 Kalsec Inc.

- 6.4.7 Indena SpA

- 6.4.8 Archer Daniels Midland Company

- 6.4.9 Martin Bauer Group

- 6.4.10 Sensient Technologies Corp.

- 6.4.11 Ransom Naturals Ltd.

- 6.4.12 Frutarom Industries Ltd.

- 6.4.13 Arjuna Natural Pvt. Ltd.

- 6.4.14 Blue Sky Botanics Ltd.

- 6.4.15 Botanica GmbH

- 6.4.16 Vidya Herbs Pvt. Ltd.

- 6.4.17 Nutra Green Biotechnology Co., Ltd.

- 6.4.18 Shaanxi Jiahe Phytochem

- 6.4.19 Nexira SAS

- 6.4.20 PT Indesso Aroma

- 6.4.21 Sabinsa Corporation

- 6.4.22 Layn Natural Ingredients Corp.

- 6.4.23 OmniActive Health Technologies

- 6.4.24 PureCircle (by Ingredion)

- 6.4.25 Xi'an Shengtian Bio-chemical Co., Ltd.