|

시장보고서

상품코드

2044007

프라임 연마 웨이퍼 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Prime Polished Wafer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

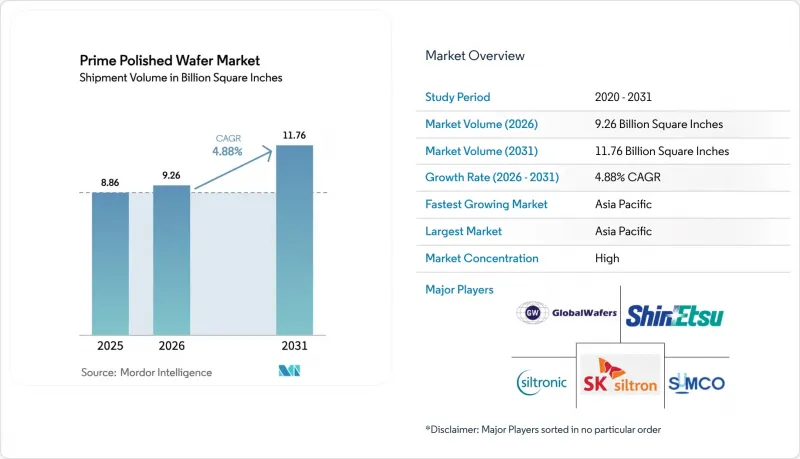

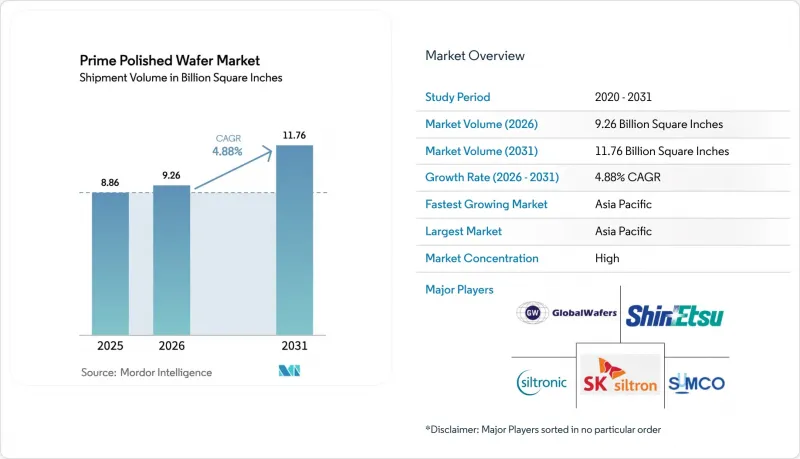

프라임 연마 웨이퍼 시장 규모는 2025년에 88억 6,000만 평방인치로 평가되었습니다. 2026년에 92억 6,000만 평방인치가 되어, 2031년까지 117억 6,000만 평방인치에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 4.88%를 나타낼 전망입니다.

반도체 제조업체들은 첨단 로직 노드, 자동차 전동화, 고대역폭 메모리로 자본을 재분배하고 있으며, 이들 분야는 기존 가전제품의 제품 주기보다 훨씬 더 빠르게 웨이퍼 표면적을 소비하고 있습니다. 파운드리 업체들의 3nm 이하 공정 기술로의 전환과 실리콘관통전극(TSV) 패키징의 확대가 맞물리면서 이미 프라임 연마 웨이퍼 시장을 독점하고 있는 직경 300mm급에 대한 수요가 집중되고 있습니다. 아시아태평양의 위탁생산 기반 덕분에 아시아태평양은 여전히 선도적인 위치를 유지하고 있지만, 미국과 유럽에서는 비용 증가라는 대가를 치르더라도 인센티브 정책을 통해 전략적 생산능력을 국내로 회귀시키려 하고 있습니다. 공급업체들은 새로운 결정 성장 설비에 대한 투자에 대해 여전히 신중한 태도를 보이고 있습니다. 이는 300mm 고순도 잉곳 생산 라인 1기당 비용이 200만-500만 달러에 달하고, 인증 획득까지 2년이 소요될 수 있기 때문입니다.

세계의 프라임 연마 웨이퍼 시장 동향과 인사이트

전기차 보급 확대와 800V 차량 플랫폼으로의 전환

800V 아키텍처를 채택한 전기자동차는 실리콘 소자보다 훨씬 더 많은 프라임 연마 웨이퍼를 소비하는 실리콘 카바이드(SiC) 트랙션 인버터를 필요로 합니다. Wolfspeed가 2025년 9월부터 200mm SiC 상용화를 시작하면서 웨이퍼당 칩 수가 약 85% 증가했지만, 7-14일이 소요되는 결정 성장 주기로 인해 여전히 공급에 병목현상이 발생하고 있습니다. 이미 여러 대형 자동차 제조업체들이 최대 1,200V까지 SiC MOSFET의 인증을 추진하고 있어 수요를 확실히 끌어올리고 있습니다.

800V 충전 인프라의 신속한 정비

유럽과 중국에서는 정류 및 역률 개선을 위해 SiC 모듈을 내장한 150-350kW급 충전소가 수천 개 규모로 증설되고 있습니다. 각 초고속 충전기에는 여러 개의 200mm 웨이퍼가 필요하기 때문에 프라임 연마 웨이퍼 시장에 2차적인 수요가 발생하고 있습니다. 보조금으로 인해 설치 일정이 가속화되고 있으며, 공급업체가 새로운 황소 생산 능력을 강화할 수 있는 여지가 압박을 받고 있습니다.

200mm 기판 공급 부족

200mm SiC 부울은 긴 성장 시간과 특수 용광로가 필요합니다. 자동차 OEM이 다년 계약을 체결함에 따라 소규모 고객의 기판 리드 타임이 40주 이상에 달하고, 그 결과 프라임 연마 웨이퍼 시장의 다른 업체들은 물량을 확보하기 위해 분주하게 움직이고 있습니다.

부문 분석

2025년 기준, 300mm 클래스는 프라임 연마 웨이퍼 시장 점유율의 73.39%를 차지했으며, 2031년까지 연평균 복합 성장률(CAGR) 5.55%를 나타낼 것으로 예측됩니다. TSMC의 2026년 설비투자 계획 560억 달러 중 70-80%가 3nm 이하 로직 반도체에 투입될 예정이라는 점은 TSMC의 지속적인 대구경 공정으로의 전환을 뒷받침합니다. 고대역폭 메모리와 AI 가속기는 기존 워크로드 대비 서버당 4-8배의 웨이퍼 면적을 필요로 하기 때문에 이 직경의 프라임 연마 웨이퍼 시장 규모는 계속 확대될 것입니다. 인텔이 애리조나주에 건설하는 1,650억 달러 규모의 '기가팹' 클러스터와 세계 웨이퍼의 텍사스 생산라인은 지역적 중복성을 높이고 국내 조달 규정을 충족시키면서 새로운 물류 허브를 창출할 것입니다.

200mm 부문은 아날로그, 혼합 신호 및 전력 장치, 특히 경제성 측면에서 여전히 작은 직경이 유리한 SiC MOSFET에 필수적인 요소로 남아 있습니다. Okmetic의 핀란드 확장 및 Wolfspeed의 200mm SiC 웨이퍼는 공급업체가 주류 실리콘과 특수 요구 사항을 모두 충족하는 듀얼 트랙 전략을 보여줍니다. 150mm 이하의 포맷은 감소하는 추세이지만, 기존의 자동차 마이크로컨트롤러 및 RF GaAs 디바이스는 여전히 사용되고 있습니다. 결정 성장 기술의 발전으로 결함 밀도가 낮아짐에 따라 2028년 이후에는 200mm SiC 공급이 완화될 가능성이 있지만, 당분간은 공급 부족이 지속되어 가격이 고공행진을 지속하고 있으며, 팹 간 복수 공급처 확보 움직임이 강화되고 있습니다.

"프라임 연마 웨이퍼 시장 보고서는 웨이퍼 직경(150mm 이하, 200mm, 300mm), 반도체 소자 유형(로직, 메모리, 아날로그, 디스크리트, 기타), 최종 사용자(가전, 산업용, 통신, 자동차, 기타), 지역(북미, 유럽, 아시아태평양, 남미, 중동, 아프리카) 별로 분류되어 있습니다. 아시아태평양, 남미, 중동 및 아프리카)로 분류됩니다. 시장 예측은 수량(평방인치) 기준으로 제공됩니다.

지역별 분석

아시아태평양은 2025년 전 세계 프라임 연마 웨이퍼 출하량의 81.39%를 차지했으며, 2031년까지 연평균 5.21%의 성장률을 나타낼 것으로 전망됩니다. TSMC, 삼성, SK실트론 등 지역 대기업들은 프론트엔드, 패키징, 테스트가 통합된 고도로 연계된 클러스터를 지속적으로 확장하고 있습니다. 중국 SMIC는 2026년월4만장(12인치 환산)의 웨이퍼 생산능력을 증설하고, 장비 수출 규제에도 불구하고 95.7%의 가동률을 달성했습니다. 중국의 475억 달러 규모의 IC기금 3단계 보조금이 국내 SiC 공급망을 지원하고 있습니다.

북미에서는 390억 달러 규모의 CHIPS 법에 따른 인센티브를 활용하여 수십년동안 지속된 오프쇼어링의 흐름을 되돌리려고 하고 있습니다. GlobalWafers의 35억 달러 규모의 텍사스 공장, 인텔의 애리조나 기가팹, Wolfspeed의 SiC 메가팹과 함께 지역 전체에서 프라임 연마 웨이퍼에 대한 수요가 급증하고 있습니다. 또한, 조립 및 테스트 분야에서 멕시코의 역할 확대는 다운스트림 공정에 대한 수요를 더욱 촉진하고 있습니다.

유럽은 첨단 로직 분야에서는 여전히 팹 부족에 직면해 있지만, 전략 소재 분야에서는 우위를 점하고 있습니다. ST마이크로일렉트로닉스는 이탈리아에서 SiC 사업 확장을 위해 29억 유로(32억 달러)를 확보했으며, TSMC가 운영하는 드레스덴 공장에 대한 논의도 진행 중입니다. 이 공장이 완공되면 300mm 자동차용 반도체 생산능력을 국산화하게 됩니다. 소이텍(Soitec)과 실트로닉(Siltronic)은 지역 기반의 SOI 및 고평탄도 기판을 제공하고 있으며, 이를 통해 유럽은 프라임 연마 웨이퍼 시장의 밸류체인에서 중요한 위치를 유지하고 있습니다. 남미, 중동 및 아프리카 전역에서 진행되고 있는 신규 투자는 최종 시장과 가까운 곳에서 자동차 및 산업용 고객에게 서비스를 제공하는 성숙한 노드 팹에 우선순위를 두는 경향이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The prime polished wafer market size is projected to be 8.86 billion square inches in 2025, 9.26 billion square inches in 2026, and reach 11.76 billion square inches by 2031, growing at a CAGR of 4.88% from 2026 to 2031.

Semiconductor manufacturers are reallocating capital toward advanced logic nodes, automotive electrification, and high-bandwidth memory, all of which consume wafer surface area far more rapidly than traditional consumer-electronics refresh cycles. Foundries' shift to sub-3 nm process technology, coupled with the ramp-up of through-silicon-via packaging, is concentrating demand in the 300 mm diameter class that already dominates the prime polished wafer market. Asia-Pacific's contract manufacturing base keeps the region in a leadership position, while the United States and Europe are using incentive packages to on-shore strategic capacity despite the resulting cost penalties. Suppliers remain cautious on new crystal-growth investments because each 300 mm high-purity ingot line ranges from USD 2 million to USD 5 million and can take two years to qualify.

Global Prime Polished Wafer Market Trends and Insights

Rising EV Penetration and Shift Toward 800-V Vehicle Platforms

Electric vehicles adopting 800-volt architectures require silicon-carbide traction inverters that consume far larger prime polished wafer volumes per car than silicon devices. Wolfspeed's commercial 200 mm SiC launch in September 2025 increases chips-per-wafer by roughly 85%, yet supply is still bottlenecked by 7- to 14-day crystal-growth cycles. Multiple major automakers already qualify SiC MOSFETs rated up to 1,200 V, pushing demand firmly upward.

Rapid Build-Out of 800-V Charging Infrastructure

Europe and China are adding thousands of 150- to 350-kW charging stalls that embed SiC modules for rectification and power-factor correction. Each ultra-fast charger needs multiple 200 mm wafers, creating a second-order pull on the prime polished wafer market. Subsidies accelerate installation schedules, compressing suppliers' ability to add new boule capacity.

Limited Availability of 200 mm Substrates

200 mm SiC boules require long growth times and specialized furnaces. Substrate lead times stretch beyond 40 weeks for smaller customers as automotive OEMs lock in multi-year contracts, leaving the rest of the prime polished wafer market scrambling for allocation.

Other drivers and restraints analyzed in the detailed report include:

- High-Temperature, High-Frequency Performance Advantages Over Si

- Government Incentives for Wide-Band-Gap Fabs

- Packaging-Induced Thermo-Mechanical Stress

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 300 mm class accounted for 73.39% of prime polished wafer market share in 2025 and is forecast to grow at a 5.55% CAGR through 2031. TSMC's USD 56 billion capital plan for 2026, of which 70-80% goes to sub-3 nm logic, underscores the relentless shift toward large-diameter processing. The prime polished wafer market size for this diameter will continue expanding as high-bandwidth memory and AI accelerators require four-to-eight times more wafer area per server than conventional workloads. Intel's USD 165 billion Arizona "gigafab" cluster and GlobalWafers' Texas line add regional redundancy, satisfying domestic-content rules while creating new logistic hubs.

The 200 mm segment remains essential for analog, mixed-signal, and power devices, particularly SiC MOSFETs where the economics still favor smaller diameters. Okmetic's Finnish expansion and Wolfspeed's 200 mm SiC wafers show the dual-track strategy of suppliers addressing both mainstream silicon and specialty needs. Up-to-150 mm formats are declining, yet they persist in legacy automotive microcontrollers and RF GaAs devices. As crystal-growth breakthroughs reduce defect densities, 200 mm SiC supply could loosen post-2028, but near-term scarcity keeps prices elevated and reinforces multi-sourcing behavior among fabs.

The Prime Polished Wafer Market Report is Segmented by Wafer Diameter (Up To 150 Mm, 200 Mm, 300 Mm), Semiconductor Device Type (Logic, Memory, Analog, Discrete, Other), End-User (Consumer Electronics, Industrial, Telecommunications, Automotive, Other), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts are Provided in Terms of Volume (Square Inches).

Geography Analysis

Asia-Pacific shipped 81.39% of global prime polished wafer volumes in 2025 and is set to grow at 5.21% CAGR through 2031. Regional giants such as TSMC, Samsung, and SK Siltron continue expanding deeply integrated clusters that bundle front-end, packaging, and testing. China's SMIC added 40 k 12-inch-equivalent wafers per month in 2026, achieving 95.7% utilization despite tool export controls. Subsidies under China's USD 47.5 billion IC Fund Phase III buttress domestic SiC supply chains.

North America is reversing decades of offshoring by tapping USD 39 billion in CHIPS incentives. GlobalWafers' USD 3.5 billion Texas plant, Intel's Arizona gigafab, and Wolfspeed's SiC mega-facility collectively drive a region-wide surge in demand for prime polished wafers. Mexico's ascending role in assembly and test adds downstream pull.

Europe remains fab-constrained for leading-edge logic yet excels in strategic materials. STMicroelectronics secured EUR 2.9 billion (USD 3.2 billion) to scale SiC in Italy, and discussions continue on a potential TSMC-run Dresden fab that would localize 300 mm automotive capacity. Soitec and Siltronic provide regionally anchored SOI and high-flatness substrates, keeping Europe relevant in the prime polished wafer market value chain. Emerging investments across South America and the Middle East and Africa favor mature-node fabs servicing automotive and industrial customers close to end markets.

- Shin-Etsu Handotai Co., Ltd.

- SUMCO Corporation

- GlobalWafers Co., Ltd.

- Siltronic AG

- SK Siltron Co., Ltd.

- Soitec SA

- Okmetic Oyj

- Wafer Works Corporation

- Ferrotec Holdings Corporation

- Hangzhou Crystal Silicon Technology Co., Ltd.

- Poshing Electronics Co., Ltd.

- MiCo Co., Ltd.

- Tokuyama Corporation

- Topsil Semiconductor Materials A/S

- GCL Technology Holdings Limited

- Zhejiang Jingsheng Mechanical & Electrical Co., Ltd.

- II-VI Incorporated

- AEPI Group (Sil'Tronix Silicon Technologies)

- Advantest Corporation

- Shanghai SIM-AXIS Semiconductor Materials Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value-Chain Analysis

- 4.3 Regulatory Landscape

- 4.4 Impact of Macroeconomic Factors

- 4.5 Technology Analysis

- 4.6 Regulatory Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Market Drivers

- 4.8.1 Rising EV Penetration and Shift Toward 800-V Vehicle Platforms

- 4.8.2 Rapid Build-Out of 800-V Charging Infrastructure

- 4.8.3 High-Temperature, High-Frequency Performance Advantages Over Si

- 4.8.4 Government Incentives for Wide-Band-Gap Fabs

- 4.8.5 Emergence of Vertically-Integrated SiC Supply Chains in China

- 4.8.6 Novel 200 mm Bulk-Growth Breakthroughs Lowering Defect Density

- 4.9 Market Restraints

- 4.9.1 Limited Availability of 200 mm Substrates

- 4.9.2 Packaging-Induced Thermo-Mechanical Stress

- 4.9.3 Capital-Intensive Crystal-Growth Equipment

- 4.9.4 Recycling Challenges for SiC Kerf Waste

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By Wafer Diameter

- 5.1.1 Up to 150 mm

- 5.1.2 200 mm

- 5.1.3 300 mm

- 5.2 By Semiconductor Device Type

- 5.2.1 Logic

- 5.2.2 Memory

- 5.2.3 Analog

- 5.2.4 Discrete

- 5.2.5 Other Semiconductor Device Types (Optoelectronics, Sensors, Micro)

- 5.3 By End-User

- 5.3.1 Consumer Electronics

- 5.3.1.1 Mobile and Smartphones

- 5.3.1.2 PCs and Servers

- 5.3.2 Industrial

- 5.3.3 Telecommunications

- 5.3.4 Automotive

- 5.3.5 Other End-User Applications

- 5.3.1 Consumer Electronics

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Taiwan

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.5 Middle East

- 5.4.6 Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Shin-Etsu Handotai Co., Ltd.

- 6.4.2 SUMCO Corporation

- 6.4.3 GlobalWafers Co., Ltd.

- 6.4.4 Siltronic AG

- 6.4.5 SK Siltron Co., Ltd.

- 6.4.6 Soitec SA

- 6.4.7 Okmetic Oyj

- 6.4.8 Wafer Works Corporation

- 6.4.9 Ferrotec Holdings Corporation

- 6.4.10 Hangzhou Crystal Silicon Technology Co., Ltd.

- 6.4.11 Poshing Electronics Co., Ltd.

- 6.4.12 MiCo Co., Ltd.

- 6.4.13 Tokuyama Corporation

- 6.4.14 Topsil Semiconductor Materials A/S

- 6.4.15 GCL Technology Holdings Limited

- 6.4.16 Zhejiang Jingsheng Mechanical & Electrical Co., Ltd.

- 6.4.17 II-VI Incorporated

- 6.4.18 AEPI Group (Sil'Tronix Silicon Technologies)

- 6.4.19 Advantest Corporation

- 6.4.20 Shanghai SIM-AXIS Semiconductor Materials Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment