|

시장보고서

상품코드

2044053

SSD 캐싱 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)SSD Caching - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

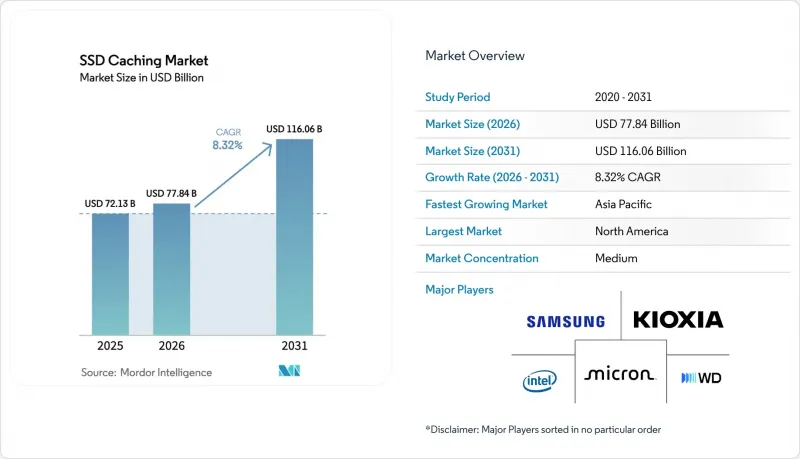

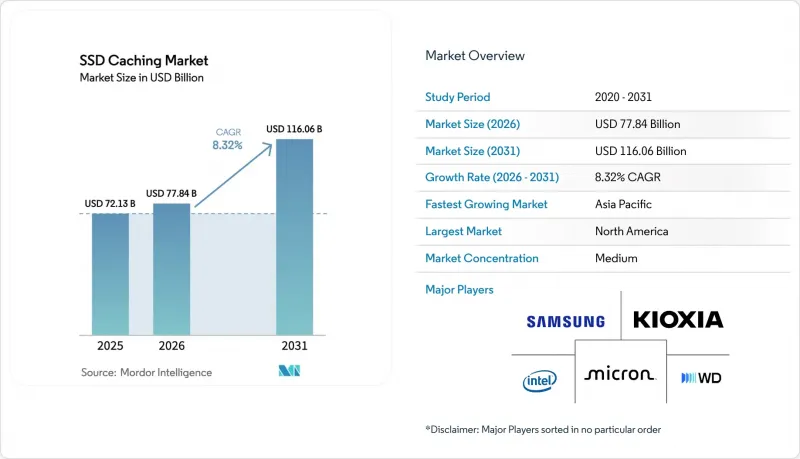

SSD 캐싱 시장 규모는 2025년 721억 3,000만 달러에서 2026년에는 778억 4,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 8.32%로 성장을 지속하여, 2031년에는 1,160억 6,000만 달러에 이를 것으로 예측됩니다.

저지연 데이터 서비스에 대한 끊임없는 수요, PCIe 5.0 및 Compute Express Link(CXL)의 대중화, 그리고 기업 내 소버린 AI 워크플로우 채택이 단기적으로 수익성을 높이고 있습니다. 하드웨어의 점유율은 여전히 지배적이지만, 가상화로 인해 성능 계층이 물리적 미디어에서 분리됨에 따라 소프트웨어 정의 계층화로의 전환은 분명합니다. 하이퍼스케일러가 NVMe-over-Fabrics를 표준 서비스로 제공하면서 클라우드 네이티브 도입이 가속화되고 있습니다. 반면, On-Premise형 어레이는 종량제를 통해 점유율을 지키고 있습니다. 경쟁의 초점은 단순한 용량에서 프로토콜의 상호운용성과 내구성으로 옮겨가고 있으며, NAND 제조와 펌웨어 로드맵을 모두 보유한 벤더에게 기회가 주어지고 있습니다. 공급망 변동, 지정학적 수출 규제, 새로운 데이터 주권 규제가 여전히 주요 역풍으로 작용하고 있지만, SSD 캐싱 시장에서는 수직적 통합과 유연한 라이선싱을 결합한 벤더가 여전히 우위를 점하고 있습니다.

세계 SSD 캐싱 시장 동향 및 인사이트

NVMe 기반 데이터센터 도입 가속화

NVMe-over-Fabrics는 SATA와 SAS를 대체하여 지연시간을 밀리초에서 마이크로초 단위로 획기적으로 단축하고, 각 드라이브가 훨씬 더 높은 IOPS를 실현할 수 있게 해줍니다. 인텔은 2026년 1분기 제온 플랫폼의 NVMe SSD 탑재율이 75%를 넘어섰다고 보고하고 있으며, 하이퍼스케일러를 통한 표준화가 진행되고 있다는 점을 뒷받침하고 있습니다. 키옥시아의 PCIe 5.0 CD9P 드라이브는 14GB/s의 읽기 속도를 구현하여 하나의 장치로 3대의 Gen4 장치를 대체하여 랙 수, 전력, 냉각 비용을 절감할 수 있습니다. 이러한 변화는 기존의 블록 프로토콜 SAN에 부담을 주며, 기업들은 소프트웨어 정의 스토리지 패브릭으로 향하고 있습니다. 라이선스 오버헤드가 발생하지만, 100마이크로초 미만의 캐시 히트를 달성할 수 있습니다.

전사적으로 증가하는 데이터 분석 워크로드

생성형 AI 워크로드의 폭발적인 증가와 함께 2025년 세계 데이터 웨어하우스 쿼리량은 전년 대비 42% 증가하여 지속적인 무작위 판독에 대한 수요가 증가했습니다. 델에 따르면, 금융 서비스 업계 고객의 경우 NVMe 캐시를 통합한 PowerStore 어레이 출하량이 63% 증가했다고 합니다. SSD 캐싱을 통해 기업들은 핫한 데이터 세트를 전체 용량의 극히 일부에 스테이징하여 서비스 수준 계약(SLA)을 유지하면서 비용이 많이 드는 용량 업그레이드를 미룰 수 있습니다. 접속 패턴의 변화 속에서 캐시 적중률을 안정화하기 위해 머신러닝 기반의 프리페칭이 부상하고 있습니다.

엔터프라이즈용 SSD 캐싱의 높은 초기 투자 비용

기업용 NVMe SSD의 가격은 1GB당 0.80-1.20달러인 반면, 니어라인 HDD는 0.05달러로, 16-24배의 가격 차이가 업그레이드의 장벽으로 작용하고 있습니다. 마이크론의 2025년 15% 가격 인상은 AI 서버가 웨이퍼 생산량을 흡수하면서 지난 수년간의 평균판매가격(ASP) 하락 추세를 반전시켰습니다. 퓨어스토리지의 '에버그린//포에버(Evergreen//Forever)'와 같은 소비량 기반 프로그램은 설비투자를 줄여주지만, 보급률은 여전히 20% 미만에 머물러 있어, 하이퍼스케일러가 앞서가는 반면, 중견 구매자가 Gen4 자산을 활용하는 데 어려움을 겪는 양극화된 시장이 형성되고 있습니다. 양극화된 시장이 형성되고 있습니다.

부문 분석

2025년 라이트스루는 45.88%의 시장 점유율을 유지하며, 트랜잭션 데이터베이스가 동기식 내구성을 요구하는 가운데 SSD 캐싱 시장의 기반이 되고 있습니다. 대규모 금융 및 EC 플랫폼은 모든 쓰기가 원본 데이터에 미러링되기 때문에 데이터 유출에 대한 우려를 없애기 때문에 이 디자인을 선호합니다. 그러나 2031년까지 연평균 복합 성장률(CAGR) 9.34%로 가장 빠르게 성장할 것으로 예상되는 것은 라이트어라운드 방식입니다. 이는 쓰기 속도보다 읽기 레이턴시가 우선시되는 분석 워크로드를 반영합니다. 현재 소프트웨어 정의 어레이를 통해 관리자는 볼륨별로 캐시 모드를 전환할 수 있어 기존 컨트롤러에 없던 유연성을 제공함으로써 SSD 캐싱 시장 내 워크로드 분산을 지원하고 있습니다.

PCIe 5.0의 급격한 대역폭 증가로 인해 쓰기 바이패스형 어레이의 처리 능력을 압박하지 않고, 인입 트래픽이 캐시를 우회할 수 있게 되어 기존의 병목현상을 해소할 수 있게 되었습니다. Snowflake와 Databricks는 읽기 비율이 95%에 달하는 클라우드 웨어하우스에 이 모델을 표준화하고 있으며, 이는 아키텍처의 광범위한 전환을 시사하고 있습니다. 한편, 라이트백 방식은 혼합 워크로드를 위해 존속하고 있지만, 배터리 백업이 가능한 휘발성 버퍼와 비휘발성 메모리 모듈에 의존하고 있습니다. 전반적으로 다양한 캐시 모드의 등장으로 구매자의 선택의 폭이 넓어지고, SSD 캐시 시장 전체에서 기능적 경쟁이 심화되고 있습니다.

2025년에는 하드웨어가 68.63%의 시장 점유율을 차지했지만, 기업들이 논리적 성능 계층과 기본 미디어를 분리함에 따라 소프트웨어 정의 캐싱 플랫폼은 2031년까지 연평균 복합 성장률(CAGR) 9.56%를 나타낼 것으로 예측됩니다. DataCore SANsymphony와 같은 플랫폼은 모든 블록 장치를 캐시 계층으로 변환하고, 노후화된 SAS 드라이브에서 잔존 가치를 추출하고, PCIe 5.0 SSD를 동일한 클러스터에 통합합니다. 이러한 변화는 벤더 종속성을 줄여주지만, 드라이브 제조업체들이 차별화를 위해 더 스마트한 펌웨어를 탑재하도록 압력을 가하고 있습니다.

마이크론의 9550 SSD는 핫 데이터를 예측하는 온컨트롤러형 머신러닝 기능을 통합했습니다. 삼성의 Flexible Data Placement 기능을 통해 호스트는 동일한 드라이브 내 고내구성 SLC 영역으로 쓰기를 유도할 수 있습니다. 이러한 혁신은 SSD 캐싱 시장에서 하드웨어와 소프트웨어 기능 세트의 경계를 모호하게 만들고, 구매자들이 총소유비용(TCO) 프레임워크를 재검토하도록 유도하고 있습니다.

지역별 분석

2025년에는 북미가 38.84%의 시장 점유율을 차지하며 1위를 차지했습니다. 이는 버지니아, 오리건, 텍사스에 위치한 하이퍼스케일 캠퍼스가 매달 수천 대의 PCIe 5.0 드라이브를 소비하고 있다는 점이 뒷받침하고 있습니다. 'CHIPS and Science Act'에 따른 연방 정부의 인센티브는 국내 조립을 장려하고 있으며, FIPS 140-3과 같은 암호화 요구 사항으로 인해 인증된 보안 펌웨어가 탑재된 드라이브만 공급업체 후보로 남아있습니다. 그러나 갱신 주기가 5년 이상으로 길어지고 있으며, 다른 지역에 비해 성장이 완만하게 이루어지고 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 9.91%로 가장 높은 성장률을 나타낼 것으로 예측됩니다. 중국의 '14차 5개년 계획'은 엔터프라이즈 스토리지 자급률 70%를 목표로 하고 있으며, 국산 컨트롤러와 NAND 개발을 촉진하고 있습니다. SK하이닉스는 캐시 코히런트 메모리가 SSD 캐싱 시장의 일부를 대체할 것이라는 전망에 따라 2028년까지 CXL 모듈 생산 능력을 3배로 확대하기 위해 39억 달러를 투자하고 있습니다. 인도에서는 '디지털 개인정보 보호법'을 계기로 한 데이터센터 확장으로 대상 상면적이 2배로 늘어나면서 고온다습한 환경에 적합한 캐시 디바이스에 대한 지역적 수요가 증가하고 있습니다.

유럽, 중동 및 아프리카는 규모는 작지만 전략적으로 중요한 클러스터를 형성하고 있습니다. GDPR(EU 개인정보보호규정)은 역내 캐싱을 의무화하고 있으며, NVMe 어레이를 사전 설치한 코로케이션 사업자가 그 혜택을 누리고 있습니다. 유럽에서는 독일과 영국이 투자를 주도하고 있으며, 사우디아라비아와 UAE는 미국과 중국 하이퍼스케일러에 대한 의존도를 낮추기 위해 소버린 클라우드 클러스터에 자금을 투입하고 있습니다. 마이크로소프트 애저의 나이지리아와 이집트로의 진출은 향후 수요 증가를 예고하고 있지만, 불안정한 전력망과 제한된 광섬유 회선으로 인해 아프리카 전역의 보급이 여전히 제한되어 있어 이 지역의 SSD 캐싱 시장 점유율 확대에 걸림돌이 되고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The SSD caching market size is expected to grow from USD 72.13 billion in 2025 to USD 77.84 billion in 2026 and is forecast to reach USD 116.06 billion by 2031 at 8.32% CAGR over 2026-2031.

Unrelenting demand for low-latency data services, the mainstreaming of PCIe 5.0 and Compute Express Link (CXL), and enterprise adoption of sovereign-AI workflows are lifting near-term revenue. Hardware share stays dominant, yet the pivot toward software-defined tiering is unmistakable as virtualization decouples performance tiers from physical media. Cloud-native deployments are accelerating because hyperscalers now expose NVMe-over-Fabrics as a routine service, while on-premise arrays defend share through consumption-based pricing. Competitive energy has moved from raw capacity to protocol interoperability and endurance, creating space for vendors that own both NAND fabrication and firmware road maps. Supply-chain volatility, geopolitical export controls, and emerging data-sovereignty rules remain the chief headwinds, but the SSD caching market continues to reward providers that combine vertical integration with flexible licensing.

Global SSD Caching Market Trends and Insights

Accelerated Adoption of NVMe-Based Data Centers

NVMe-over-Fabrics is replacing SATA and SAS, slashing latency from milliseconds to microseconds and allowing each drive to serve order-of-magnitude more IOPS. Intel reported that NVMe SSD attach rates in Xeon platforms exceeded 75% in Q1 2026, underscoring hyperscaler standardization. Kioxia's PCIe 5.0 CD9P drive delivers 14 GB/s reads, enabling one device to replace three Gen4 units and cut rack count, power, and cooling. The switch strains legacy block-protocol SANs, pushing enterprises toward software-defined storage fabrics that add license overhead but unlock sub-100-microsecond cache hits.

Rising Data Analytics Workloads Across Enterprises

Global data-warehouse query volumes expanded 42% year-over-year in 2025 as generative-AI workloads exploded, intensifying demand for sustained random reads. Dell noted a 63% shipment jump for PowerStore arrays with integrated NVMe caching among financial-services customers. SSD caches permit enterprises to stage hot datasets on a fraction of total capacity, postponing costly capacity upgrades while maintaining service-level agreements. Machine-learning-based prefetching is emerging to stabilize cache-hit ratios amid shifting access patterns.

High Upfront Capital Expenditure for Enterprise SSD Caches

Enterprise NVMe SSDs cost USD 0.80-1.20 per gigabyte versus USD 0.05 for nearline HDDs, a 16-24X delta that deters upgrades. Micron's 15% price hike in FY2025 reversed years of ASP declines as AI servers absorbed wafer output. Consumption-based programs like Pure Storage's Evergreen//Forever mitigate capex but remain sub-20% penetrated, creating a bifurcated market where hyperscalers advance and mid-tier buyers sweat Gen4 assets.

Other drivers and restraints analyzed in the detailed report include:

- Demand for Low-Latency Edge Computing Infrastructure

- Growth in Hyperconverged Infrastructure Deployments

- Complexity in Maintaining Multi-Tier Storage Architectures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Write-through retained 45.88% of the market share in 2025, anchoring the SSD caching market as transactional databases insist on synchronous durability. Large financial and e-commerce platforms favor the design because every write is mirrored to the origin, eliminating data-loss concerns. Yet write-around will post the fastest growth at a 9.34% CAGR through 2031, reflecting analytics workloads where read latency trumps write speed. Software-defined arrays now let administrators toggle among caching modes per volume, injecting flexibility legacy controllers lack, and supporting the widening workload split within the SSD caching market.

The surge of PCIe 5.0 bandwidth permits ingest traffic to bypass cache without choking write-around arrays, removing a historic bottleneck. Snowflake and Databricks have standardized on the model for cloud warehouses that show 95% read ratios, signaling a broad architectural pivot. Meanwhile, write-back persists for mixed workloads but depends on battery-backed volatile buffers or persistent memory modules. Overall, the panoply of caching modes expands buyer choice and intensifies feature competition across the SSD caching market.

Hardware accounted for 68.63% of market share in 2025, but software-defined caching platforms are on pace for a 9.56% CAGR through 2031 as enterprises decouple logical performance layers from the underlying media. Platforms such as DataCore SANsymphony convert any block device into a cache tier, squeezing residual value from aging SAS drives and sliding PCIe 5.0 SSDs into the same cluster. This shift lowers vendor lock-in, though it pressures drive makers to embed smarter firmware to differentiate.

Micron's 9550 SSD integrates on-controller machine learning that predicts hot data. Samsung's Flexible Data Placement allows hosts to steer writes to high-endurance SLC within the same drive. These innovations blur the boundaries between hardware and software feature sets in the SSD caching market, prompting buyers to reassess total-cost-of-ownership frameworks.

The SSD Caching Market Report is Segmented by Architecture (Write-Through, Write-Back, and Write-Around), Component (Hardware and Software), Deployment Model (On-Premise and Cloud), Application (Enterprise Servers and Personal Computing), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 38.84% of the market share in 2025, anchored by hyperscale campuses in Virginia, Oregon, and Texas that consume thousands of PCIe 5.0 drives per month. Federal incentives under the CHIPS and Science Act encourage domestic assembly, and encryption mandates such as FIPS 140-3 narrow the supplier field to drives with certified secure firmware. Replacement cycles, however, lengthen beyond five years, moderating growth relative to other regions.

Asia-Pacific will post the fastest 9.91% CAGR through 2031. China's 14th Five-Year Plan targets 70% self-sufficiency in enterprise storage, spurring indigenous controller and NAND development. SK hynix is spending USD 3.9 billion to triple CXL module capacity by 2028, betting that cache-coherent memory will displace parts of the SSD caching market. India's data-center build-out, propelled by the Digital Personal Data Protection Act, doubles addressable floor space and lifts regional demand for cache devices tuned to humid, high-temperature environments.

Europe, the Middle East and Africa form a smaller but strategic cluster. GDPR compels in-region caching, benefitting colocation operators that pre-install NVMe arrays. Germany and the United Kingdom lead European spend, while Saudi Arabia and the UAE bankroll sovereign-cloud clusters to cut reliance on U.S. or Chinese hyperscalers. Microsoft Azure's expansion into Nigeria and Egypt highlights future pull, yet broad African adoption remains gated by inconsistent power grids and limited fiber, restraining the SSD caching market share there.

- Samsung Electronics Co., Ltd.

- Intel Corporation

- Kioxia Holdings Corporation

- Western Digital Corporation

- Micron Technology, Inc.

- SK hynix Inc.

- ASTERA LABS, INC.

- Kingston Technology Company, Inc.

- Hewlett Packard Enterprise Company

- Dell Technologies Inc.

- NetApp, Inc.

- Lenovo Group Limited

- Huawei Technologies Co., Ltd.

- Inspur Group Co., Ltd.

- Pure Storage, Inc.

- DataCore Software Corporation

- Nutanix, Inc.

- Montage Technology

- AccelStor, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Adoption of NVMe-Based Data Centers

- 4.2.2 Rising Data Analytics Workloads Across Enterprises

- 4.2.3 Demand for Low-Latency Edge Computing Infrastructure

- 4.2.4 Growth in Hyperconverged Infrastructure Deployments

- 4.2.5 Mainstreaming of PCIe 5.0 and CXL Protocol Support

- 4.2.6 Enhanced SSD Endurance Through AI-Enabled Wear-Leveling

- 4.3 Market Restraints

- 4.3.1 High Upfront Capital Expenditure for Enterprise SSD Caches

- 4.3.2 Complexity in Maintaining Multi-Tier Storage Architectures

- 4.3.3 Limited Performance Gains for Write-Intensive Workloads

- 4.3.4 Supply Chain Volatility in Advanced NAND Components

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Supply-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Architecture

- 5.1.1 Write-Through

- 5.1.2 Write-Back

- 5.1.3 Write-Around

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.2 Software

- 5.3 By Deployment Model

- 5.3.1 On-Premise

- 5.3.2 Cloud

- 5.4 By Application

- 5.4.1 Enterprise Servers

- 5.4.2 Personal Computing

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Nigeria

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Samsung Electronics Co., Ltd.

- 6.4.2 Intel Corporation

- 6.4.3 Kioxia Holdings Corporation

- 6.4.4 Western Digital Corporation

- 6.4.5 Micron Technology, Inc.

- 6.4.6 SK hynix Inc.

- 6.4.7 ASTERA LABS, INC.

- 6.4.8 Kingston Technology Company, Inc.

- 6.4.9 Hewlett Packard Enterprise Company

- 6.4.10 Dell Technologies Inc.

- 6.4.11 NetApp, Inc.

- 6.4.12 Lenovo Group Limited

- 6.4.13 Huawei Technologies Co., Ltd.

- 6.4.14 Inspur Group Co., Ltd.

- 6.4.15 Pure Storage, Inc.

- 6.4.16 DataCore Software Corporation

- 6.4.17 Nutanix, Inc.

- 6.4.18 Montage Technology

- 6.4.19 AccelStor, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment