|

시장보고서

상품코드

2044057

임상시험 관리 CRO 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Clinical Trial Management Contract Research Organization (CRO) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

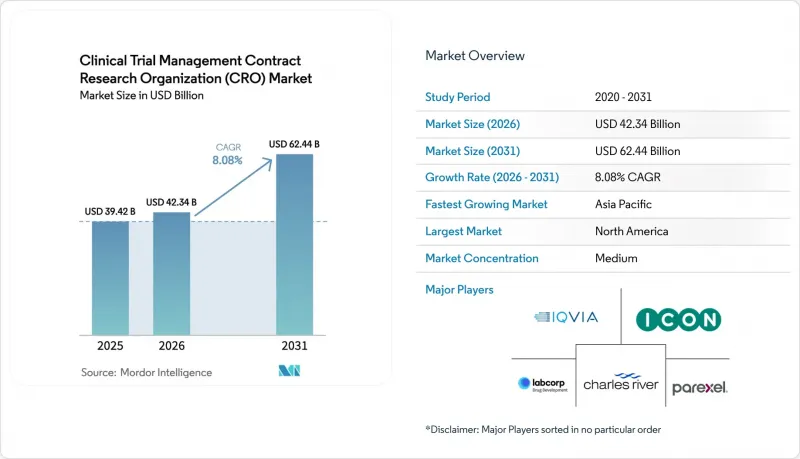

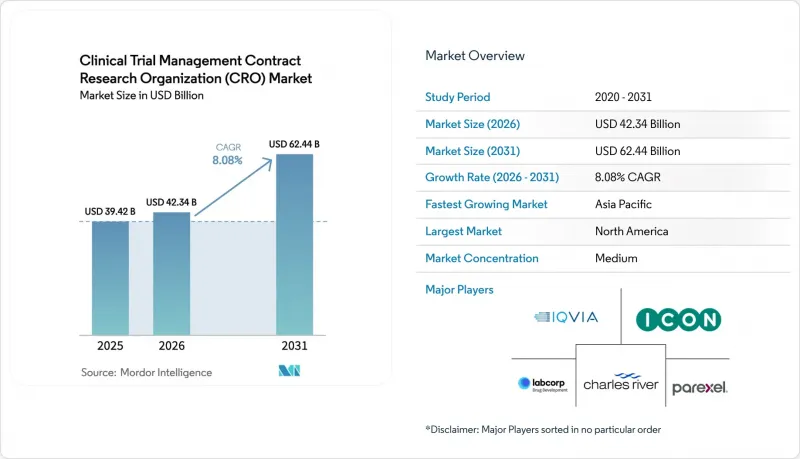

임상시험 관리 CRO 시장은 2025년에 394억 2,000만 달러로 평가되었고 2026년 423억 4,000만 달러에서 2031년까지 624억 4,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 8.08%를 나타낼 전망입니다.

치료법의 복잡성, 강화된 규제 감독, 그리고 높아진 임상시험 인프라 비용으로 인해 임상시험 스폰서들은 세계 임상시험을 원활하게 조정할 수 있는 풀서비스 파트너를 찾고 있습니다. 2024년 FDA가 승인한 하이브리드 및 분산형 모델은 환자 1인당 비용을 15-25% 절감하고 피험자 지속율을 향상시키기 위해 스폰서들의 조달 전략의 핵심이 되고 있습니다. 종양학 분야의 자본 집약적인 프로토콜, 베이즈 적응증 설계, GLP-1 수용체 작용제 심혈관 결과 연구의 급증과 함께, 전문 의료진에 대한 높은 가격 책정이 유지되고 있습니다. 한편, AI를 활용한 환자 매칭 플랫폼과 통합 데이터 레이크는 기술 주도형 CRO에 입찰 경쟁에서 우위를 제공하고 있으며, 스폰서들은 사이클 타임을 단축하고 데이터 무결성을 강화하는 엔드투엔드 솔루션을 높이 평가했습니다. 전반적으로 아웃소싱이 단순한 인력 파견에서 전략적이고 분석 중심의 파트너십으로 전환됨에 따라 임상시험 관리 CRO 시장은 지속적인 두 자릿수 성장이 예상됩니다.

세계 임상시험 관리 CRO 시장 동향 및 인사이트

CRO에 대한 제약 R&D 아웃소싱 증가

2024년에는 스폰서 임상 예산의 대다수가 외부 공급자에게 흘러들어갔습니다. 이는 2020년 대비 5% 증가한 수치로, R&D 부문의 인력 감축과 파이프라인 다각화로 인해 수직적 통합이 어려워진 것이 배경입니다. 중견 바이오기업은 업무의 대부분을 외부에 위탁하고 있으며, 마일스톤 기반 계약을 통해 위험을 전가하면서 종양학 자산 시장 진입을 약 8개월 앞당기고 있습니다. 스폰서들이 아웃소싱 범위를 신약개발 생물학, 독성학 등 업스트림 공정으로 확대하고, 계약 범위가 개별 임상시험에서 여러 자산을 다루는 플랫폼으로 확대되면서 임상시험 관리 CRO 시장은 수혜를 입고 있습니다. 위험분담 조항은 인센티브를 일치시키는 한편, CRO의 재무상황에 압력을 가하고 있으며, 대형 기업들은 현금 준비금을 늘리거나 리볼빙 크레딧 라인을 확보하도록 촉구하고 있습니다. 정부 보조금, 특히 2024년 NIH의 32억 달러의 인프라 자금은 학술 연구를 CRO의 지원으로 유도하고, 대상 고객 기반을 확대하는 데 기여하고 있습니다.

임상시험 및 규제 요건의 복잡성 증가

2024년, 규제 당국이 보다 광범위한 인구통계학적 대표성을 요구한 결과, 150개 기관에서 800명의 환자를 등록한 임상 3상 종양학 시험의 중앙값은 150개 기관에서 800명의 환자를 등록했습니다. 2024년 3월 FDA 지침에 명시된 베이즈 적응증 설계는 스폰서의 약 1/3만이 보유하고 있는 전문적 생물통계학적 기술을 필요로 하며, CRO의 분석팀에 대한 의존도를 높이고 있습니다. 2025년 1월부터 전면 시행되는 유럽 임상시험 규정은 CTIS를 통한 일원화된 신청과 보고 기한의 엄격화를 요구하고 있어, 대형 CRO만이 여유 있게 대응할 수 있는 IT 투자가 필수적입니다. 일본의 RWE(Real World Evidence) 의무화, 중국의 ICH E6(R3) 준수 등으로 컴플라이언스의 장벽은 더욱 높아지고 있습니다. 그 결과, 규모와 자본집약도에 따른 업계 재편이 진행되어 중소형 기업의 임상시험 관리 CRO 시장 진입장벽이 높아지고 있습니다.

임상시험 수행기관의 용량 제약과 피험자 모집의 과제

2024년, 북미 임상시험 시설의 가용성은 8% 감소했습니다. 이는 연구자의 번아웃으로 인해 연구책임자가 관여를 줄였기 때문입니다. 시설 가동 개시까지 16주로 늘어났으며, 첫 환자 등록(First-Patient-In) 일정이 지연되었습니다. 또한, 종양학 분야의 피험자 모집 실패율은 37%에 달했습니다. 예측 분석 플랫폼은 위험을 줄일 수 있지만, 수년간의 데이터 히스토리를 필요로 하기 때문에 ROI 실현이 늦어집니다. 인도의 240개 신규 인증 시설과 중국의 60일 승인은 도움이 되지만, 언어와 동의서의 뉘앙스 차이로 인해 가동이 지연되고 시설 부족이 발생하여 일시적으로 임상시험 관리 CRO 시장의 성장을 둔화시키고 있습니다.

부문 분석

2025년 임상 서비스는 임상시험 관리 CRO 시장 매출의 54.1%를 차지해, 이는 프로토콜, 데이터, 규제 관련 결과물에 대한 단일 벤더의 책임 체계에 대한 스폰서의 분명한 중요성을 반영하고 있습니다. 복잡한 종양학 및 GLP-1 메가 임상시험에서 통합 실행 모델이 평가됨에 따라 풀 서비스 계약 임상시험 관리 CRO 시장 규모는 계속 확대되고 있습니다. 통일된 품질 관리로 인해 반품 및 검사 지적사항이 줄어들기 때문에 스폰서들은 더 높은 수수료를 받아들인다. 2031년까지 연평균 복합 성장률(CAGR) 8.56%로 예측되는 신약개발 아웃소싱은 동물실험 시설이나 분석 실험실을 보유하지 않은 플랫폼형 바이오텍 기업들 사이에서 성장세를 보이고 있습니다. 동시에 리얼월드에비던스(RWE) 가이드라인에 따라 시판 후 의무가 증가함에 따라 약물감시 및 메디컬 라이팅에 대한 수요도 증가하고 있습니다.

기능적 서비스 제공업체(FSP)는 2025년 큰 폭의 매출 성장을 기록했으며, 자금난에 시달리는 바이오텍 기업에게 매력적인 변동형 계약 조건으로 전담 생물통계학자, 데이터 관리자, 의료 작가를 제공했습니다. 그러나 FSP의 계약을 세계 임상 3상 시험 규모로 확대하기 위해서는 인력 증원과 중앙집권적 거버넌스를 결합한 하이브리드 모델이 필요합니다. AI를 활용한 스크리닝으로 인해 신약개발 분석에 소요되는 시간이 단축되고 수익률이 압박을 받으면서 CRO 업체들은 고액의 라이선싱 비용을 기대할 수 있는 독자적인 세포 모델과 질병 모델 특허를 서둘러 획득하고 있습니다. 임상시험 관리 CRO 업계에서는 장기적인 수익성 결정 요인으로 단순한 인원수가 아닌 기술 소유권이 점점 더 중요하게 여겨지고 있습니다.

2025년 기준 종양학 분야는 임상시험 관리 CRO 시장의 30.40%를 차지했습니다. 고용량 항체 약물 복합체(ADC) 프로토콜은 전문 투약 센터와 복잡한 안전성 모니터링이 필요하며, 건당 계약 금액이 1억 달러가 넘는 요인으로 작용하고 있습니다. 감염병 분야는 시장 규모는 작지만, 각국 정부의 팬데믹 대응 플랫폼에 대한 투자로 인해 CAGR 8.99%로 가장 빠르게 성장하고 있는 분야입니다. GLP-1 수용체 작용제를 중심으로 한 심혈관 및 대사 결과 시험은 5,000명 이상의 환자를 등록하고 5-7년 동안 CRO와 스폰서를 연결하는 장기 추적 관찰을 수반하는 대형 프로젝트를 창출하고 있습니다.

신경학 분야 연구는 희귀질환의 피험자 모집에 어려움을 겪고 있지만, 분산형 인지기능 평가는 피험자의 부담을 줄이고 지리적 범위가 넓어지기 때문에 여전히 수익성이 높은 분야입니다. 면역학 분야의 임상시험에서 멀티오믹스 바이오마커에 대한 의존도가 높아지면서 CRO는 중앙검사실과의 제휴를 강화해야 하는 상황에 직면해 있습니다. 호흡기 프로젝트는 COVID-19가 진정되면서 2024년 둔화됐지만, 장기 코로나 및 천식 생물학적 제제가 그 하락을 부분적으로 상쇄하고 있습니다. 2024년 4월 마스터 프로토콜 관련 지침은 다군 다약제 플랫폼을 운영할 수 있는 심도 깊은 치료 영역의 지식을 가진 CRO에 유리하게 작용하고 있으며, 임상시험 관리 CRO 시장에서 차별화를 촉진하고 있습니다.

'임상시험 관리 CRO 시장 보고서'는 서비스 유형(신약개발 지원 서비스, 전임상 서비스 등), 치료 영역(종양학, CNS/신경학 등), 임상 단계(전임상, 임상 1상 등), 최종 사용자(제약/바이오제약 기업 등), 지역(북미, 유럽 등) 별로 분류되어 있습니다. 분류되어 있습니다. 시장 예측은 금액(USD)으로 표시됩니다.

지역별 분석

북미는 임상시험 관리 CRO 시장의 중심지로서 2025년 매출의 38.90%를 차지했습니다. 이는 촘촘한 임상시험자 네트워크, 다수의 스폰서 기업, 그리고 빠른 FDA의 지침 주기 덕분입니다. 그러나 임상 3상 시험의 환자 1인당 평균 비용은 6만 달러에 달하며, 이는 지리적 분산화를 촉진하고 있습니다. 2024년 FDA의 승인을 받은 분산형 모델은 병원 방문 빈도를 줄이고 EMR(전자의무기록) 기반의 엔드포인트를 활용하여 직접 비용을 약 5분의 1로 줄였습니다. 그럼에도 불구하고 시설용량에 대한 압박은 계속되고 있으며, 2024년 미국 내 시설에서 12개의 프로토콜을 동시에 관리함에 따라 이탈률이 증가하여 CRO는 모니터링 예산을 증액할 수밖에 없는 상황입니다. 아시아태평양은 중국의 60일 승인 제도와 인도의 240개 신규 인증 시설에 힘입어 2031년까지 연평균 복합 성장률(CAGR) 8.32%로 확대될 것으로 예측됩니다. 2024년 ICH E6(R3)에 대한 조화로 중국의 데이터 수용성에 대한 스폰서들의 우려가 완화되었습니다. 인도의 기업형 병원 네트워크는 표준화된 전자 기록을 제공하지만, 지역별로 윤리 위원회가 존재하기 때문에 사이클 타임의 편차가 발생합니다. 2024년에 도입된 일본의 영어 신청 루트는 서류 작성의 리드 타임을 단축시키지만, 고령화가 진행되면서 미치료 환자 모집에 어려움을 겪고 있습니다. 동남아시아 국가들은 50%에 가까운 비용 절감을 무기로 초기 단계의 종양학 시험을 유치하고 있지만, 규제 당국의 처리 능력이 이를 따라잡지 못해 신청 서류 심사 기간이 길어지고 있습니다.

2025년 1월 CTIS 도입으로 27개 회원국의 신청이 통일된 후, 유럽은 안정적인 점유율을 유지했습니다. 중앙집중화된 포털을 통해 업무 부담은 줄었지만, 브렉시트로 인해 영국 임상시험기관은 중복 신청이 의무화되어 과거에는 연속적이었던 지역이 분절되고 있습니다. 동유럽은 환자 1인당 비용이 40-50% 낮지만, 지정학적 위험으로 인해 2024년 임상시험 실시 건수는 12% 감소했습니다. 중동 및 아프리카 및 남미는 신흥 지역입니다. 남아공은 윤리 심사의 조화와 질병 역학 상황으로 인해 사하라 이남 아프리카의 교두보로 자리매김하고 있지만, 브라질의 ANVISA 심사 지연은 신속한 시험 시작에 걸림돌로 작용하고 있습니다. 이러한 추세와 더불어 임상시험 관리 CRO 시장은 특정 지역에 과도하게 의존하지 않고 균형 잡힌 지역적 성장을 누리고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The Clinical Trial Management Contract Research Organization Market was valued at USD 39.42 billion in 2025 and expected to grow from USD 42.34 billion in 2026 to reach USD 62.44 billion by 2031, at a CAGR of 8.08% during the forecast period (2026-2031).

Growing therapeutic complexity, tighter regulatory oversight, and the escalating costs of in-house trial infrastructure push sponsors toward full-service partners that can coordinate global studies seamlessly. Hybrid and decentralized models, validated by the FDA in 2024, shave 15-25% off per-patient costs and improve retention, making them a centerpiece of sponsor sourcing strategies. Oncology's capital-intensive protocols, Bayesian adaptive designs, and the surge of GLP-1 cardiovascular outcome studies collectively sustain premium pricing for specialist providers. Meanwhile, AI-enabled patient matching platforms and unified data lakes give technology-forward CROs an edge in bid defense, while sponsors reward end-to-end offerings that compress cycle times and bolster data integrity. Altogether, the Clinical Trial Management CRO market is positioned for durable double-digit expansion as outsourcing shifts from transactional staffing to strategic, analytics-driven partnerships.

Global Clinical Trial Management Contract Research Organization (CRO) Market Trends and Insights

Increasing Pharmaceutical R&D Outsourcing to CROs

More than half of all sponsor clinical budgets flowed to external providers in 2024, up 5 percentage points since 2020, as leaner R&D headcounts and pipeline diversity made vertical integration less feasible. Mid-cap biotechs outsourced majority of operations, using milestone-based contracts that shift risk yet accelerate market entry by roughly eight months for oncology assets. The Clinical Trial Management CRO market benefits because sponsors now extend outsourcing upstream into discovery biology and toxicology, enlarging deal scope from individual trials to multi-asset platforms. Risk-sharing terms align incentives but pressure CRO balance sheets, prompting larger players to build cash reserves or secure revolving credit lines. Government grant flows, particularly the NIH's USD 3.2 billion infrastructure pool in 2024, funnel academic studies toward CRO support, broadening the addressable client base.

Rising Complexity of Clinical Trials and Regulatory Requirements

Median Phase III oncology trials enrolled 800 patients across 150 sites in 2024, as regulators insisted on broader demographic representation . Bayesian adaptive designs, codified in FDA guidance in March 2024, require specialized biostatistical skills available to only about one-third of sponsors, increasing reliance on CRO analytics teams. Europe's Clinical Trial Regulation, fully live from January 2025, will require centralized submission via CTIS and tightened reporting timelines, compelling IT investments that only large CROs can absorb comfortably. Japan's real-world evidence mandate and China's alignment with ICH E6(R3) further elevate compliance hurdles. As a result, scale and capital intensity force consolidation, lifting the Clinical Trial Management CRO market entry barrier for smaller firms.

Investigator Site Capacity Constraints and Patient Recruitment Challenges

North American site availability fell 8% in 2024 because burnout prompted principal investigators to scale back commitments. Activation timelines stretched to 16 weeks, delaying first-patient-in schedules, while oncology recruitment failure hit 37%. Predictive analytics platforms mitigate risk but require multi-year data histories, delaying ROI. India's 240 newly certified sites and China's 60-day approvals offer relief, yet linguistic and consent-form nuances slow turn-on, reinforcing site shortfalls that temporarily temper Clinical Trial Management CRO market growth.

Other drivers and restraints analyzed in the detailed report include:

- Growing Prevalence of Chronic Diseases Driving Trial Volume

- Adoption of Decentralized and Hybrid Trial Models

- Data Integrity Concerns and Regulatory Scrutiny of CRO Operations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Clinical Services captured 54.1% of the Clinical Trial Management CRO market revenue in 2025, reflecting a clear sponsor bias for single-vendor accountability around protocol, data, and regulatory deliverables. The Clinical Trial Management CRO market size for full-service contracts continues to widen as complex oncology and GLP-1 mega-trials reward integrated execution models. Sponsors accept higher fees because unified quality oversight reduces re-work and inspection findings. Discovery outsourcing, forecast at 8.56% CAGR to 2031, gains traction with platform biotechs that lack vivaria or assay labs. Concurrently, pharmacovigilance and medical-writing demand rises as post-marketing commitments multiply under real-world evidence guidelines.

Functional service providers (FSPs) reported significant revenue growth in 2025, supplying embedded biostatisticians, data managers, and medical writers on variable terms that appeal to cash-constrained biotechs. Yet scaling FSP engagements to global Phase III demands hybrid models that blend staff augmentation with centralized governance. AI-driven screening has trimmed labor hours in discovery assays, pressuring margins, so CROs race to patent proprietary cell and disease models that command premium licensing fees. The Clinical Trial Management CRO industry increasingly views technology ownership, not merely headcount, as the determinant of long-run profitability.

Oncology held 30.40% of the Clinical Trial Management CRO market share in 2025. High-dose antibody-drug conjugate protocols require specialized infusion centers and intricate safety monitoring, driving per-study values above USD 100 million. Infectious diseases, while a smaller base, is the fastest-growing segment at 8.99% CAGR as governments invest in pandemic readiness platforms. Cardiovascular-metabolic outcome trials, catalyzed by GLP-1 classes, enroll 5,000+ patients, creating blockbuster engagements with longitudinal follow-up that stick CROs to sponsors for 5-7 years.

Neurology studies struggle with rare-disease recruitment, but the segment remains lucrative because decentralized cognitive assessments lower participant burden and extend geographic reach. Immunology trials increasingly depend on multi-omics biomarkers, pushing CROs to build central lab alliances. Respiratory projects moderated in 2024 after COVID-19 tapering; however, long-COVID and asthma biologics partially offset the dip. Master protocol guidance from April 2024 favors CROs with deep therapeutic benches capable of running multi-arm, multi-drug platforms, enhancing differentiation within the Clinical Trial Management CRO market.

The Clinical Trial Management Contract Research Organization (CRO) Market Report is Segmented by Service Type (Discovery Services, Pre-Clinical Services and More), Therapeutic Area (Oncology, CNS / Neurology and More), Clinical Phase (Pre-Clinical, Phase I and More), End-User (Pharmaceutical and Biopharmaceutical Companies, and More), and Geography (North America, Europe, and More). Market Forecasts are in Value (USD).

Geography Analysis

North America generated 38.90% of 2025 revenue as the Clinical Trial Management CRO market anchor, owing to dense investigator networks, high sponsor headcount, and swift FDA guidance cycles. Yet average Phase III per-patient costs reached USD 60,000, motivating geographic diversification. Decentralized models, cleared by the FDA in 2024, cut site visit frequency and leverage EMR-based endpoints, reducing direct costs by about one-fifth. Still, site capacity pressures persist; U.S. centers managed 12 concurrent protocols in 2024, elevating deviation rates that compel CROs to raise monitoring budgets. Asia-Pacific will expand at 8.32% CAGR through 2031, underpinned by China's 60-day approvals and India's 240 newly certified sites. Harmonization with ICH E6(R3) in 2024 calmed sponsor concerns about Chinese data acceptability . India's corporate hospital networks provide standardized electronic records, but regional ethics committees add cycle time variability. Japan's English-language pathway, introduced in 2024, trims documentation lead times, though its aging population complicates naive-patient recruitment. Southeast Asian countries entice early-phase oncology trials with cost savings near 50%, yet regulator capacity lags, extending dossier review.

Europe retained stable share after the January 2025 CTIS launch unified submissions across 27 member states. Centralized portals slice administrative load, but Brexit imposes duplicate filings for U.K. sites, fragmenting what was once a contiguous region. Eastern Europe offers 40-50% lower per-patient costs but geopolitical risk reduced trial placements 12% in 2024. The Middle East & Africa and South America are emerging zones; South Africa's harmonized ethics approvals and disease epidemiology position it as the sub-Saharan beachhead, while Brazil's ANVISA backlog remains a gating factor for rapid study start-ups. Collectively, these dynamics ensure the Clinical Trial Management CRO market enjoys balanced regional growth without over-reliance on any single geography.

- Allucent

- Caidya

- Charles River Labs

- Ergomed

- Fortrea

- ICON

- IQVIA

- LabCorp

- Linical

- MedPace

- Novotech

- Orphan-Reach

- Parexel International

- Precision for Medicine

- PROMETRIKA

- Quanticate

- Simbec Orion

- Syneos Health

- Thermo Fisher Scientific

- Veristat

- Worldwide Clinical Trials

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Pharmaceutical R&D Outsourcing

- 4.2.2 Rising Trial and Regulatory Complexity

- 4.2.3 Growing Chronic-Disease Trial Volume

- 4.2.4 Adoption of Decentralized and Hybrid Models

- 4.2.5 Technological Advancements in AI And Data Analytics for Trial Optimization

- 4.2.6 Expansion of Rare-Disease and Orphan-Drug Development Programs

- 4.3 Market Restraints

- 4.3.1 Investigator-Site Capacity and Recruitment

- 4.3.2 Data-Integrity Scrutiny of CRO Operations

- 4.3.3 High Costs of Clinical Trials Are Limiting Sponsor Budgets and Trial Starts

- 4.3.4 Shortage of Qualified Clinical Research Professionals and Investigator Burnout

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Service Type

- 5.1.1 Discovery Services

- 5.1.2 Pre-clinical Services

- 5.1.3 Clinical Services

- 5.1.4 Others

- 5.2 By Therapeutic Area

- 5.2.1 Oncology

- 5.2.2 CNS / Neurology

- 5.2.3 Cardiovascular & Metabolic

- 5.2.4 Infectious Diseases

- 5.2.5 Immunology / Inflammatory

- 5.2.6 Respiratory

- 5.2.7 Others

- 5.3 By Clinical Phase

- 5.3.1 Pre-clinical

- 5.3.2 Phase I

- 5.3.3 Phase II

- 5.3.4 Phase III

- 5.3.5 Phase IV

- 5.4 By End-Users

- 5.4.1 Pharmaceutical and Biopharmaceutical Companies

- 5.4.2 Medical Devices companies

- 5.4.3 Academic & Research Institutes

- 5.4.4 Government & Non-Profit Organisations

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Allucent

- 6.3.2 Caidya

- 6.3.3 Charles River Labs

- 6.3.4 Ergomed

- 6.3.5 Fortrea

- 6.3.6 ICON plc

- 6.3.7 IQVIA

- 6.3.8 Labcorp Drug Development

- 6.3.9 Linical

- 6.3.10 Medpace

- 6.3.11 Novotech

- 6.3.12 Orphan-Reach

- 6.3.13 Parexel

- 6.3.14 Precision for Medicine

- 6.3.15 PROMETRIKA

- 6.3.16 Quanticate

- 6.3.17 Simbec Orion

- 6.3.18 Syneos Health

- 6.3.19 Thermo Fisher

- 6.3.20 Veristat

- 6.3.21 Worldwide Clinical Trials

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment