|

시장보고서

상품코드

2044068

데이터센터 서버 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Data Center Server - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

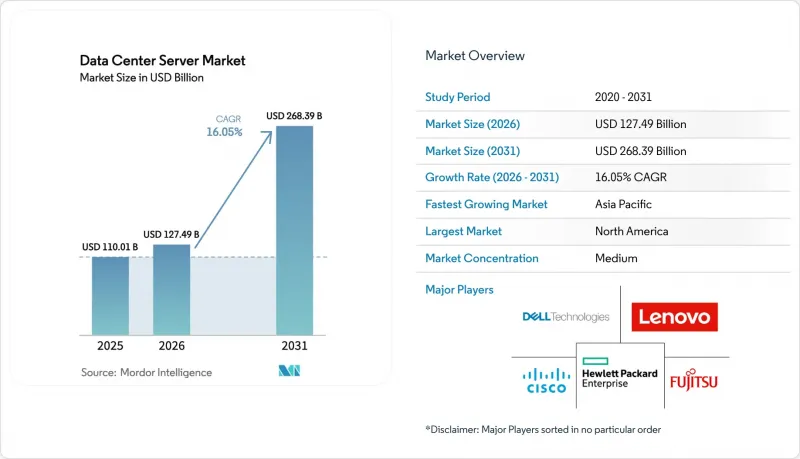

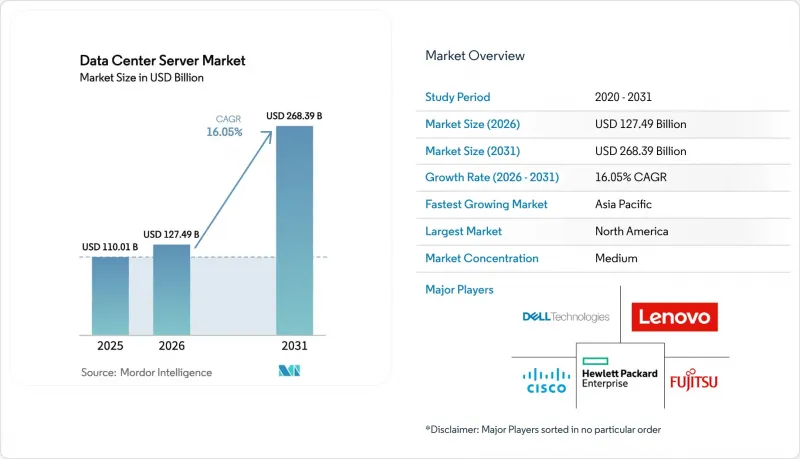

데이터센터 서버 시장 규모는 2025년 1,100억 1,000만 달러에서 2026년에는 1,274억 9,000만 달러로 확대되어 2031년까지 2,683억 9,000만 달러에 이를 것으로 예상되고 있으며 2026년부터 2031년까지 CAGR 16.05%로 성장할 전망입니다.

인공지능(AI) 훈련 실행 증가, 엣지 인프라의 급속한 확장, 액체 냉각의 채택으로 인해 업데이트 주기가 단축되면서 견조한 수요를 뒷받침하고 있습니다. 유럽과 중동의 소버린 AI 의무화는 On-Premise형 클러스터를 촉진하고 있으며, 데이터센터 서버 시장을 퍼블릭 클라우드에 집중되어 있던 것을 분산시키고 있습니다. 하이퍼스케일 사업자들은 80kW 이상의 GPU 고밀도 랙을 표준화하고 있으며, OEM 업체들은 DTC(Direct-to-Chip) 수냉 방식에 대응하기 위해 섀시를 재설계해야 하는 상황입니다. 고대역폭 메모리 공급 제약으로 인해 하이퍼스케일 사업자들은 다년간의 부품 계약을 체결하도록 유도하고 있으며, 그 결과 중기적으로 안정적인 출하 전망을 보이고 있습니다.

세계 데이터센터 서버 시장 동향 및 인사이트

GPU 고밀도 서버가 필요한 AI 및 ML 워크로드가 급증하고 있습니다.

대규모 언어 모델 훈련에는 이미 1만 개 이상의 NVIDIA H100 또는 AMD MI300X 가속기가 장착된 클러스터가 사용되고 있으며, 랙의 전력 소비는 기존의 공랭식 냉각으로는 감당할 수 없는 수준까지 증가했습니다. Meta는 2026년 말까지 35만 개의 H100에 해당하는 GPU를 도입할 계획이며, 이는 2년 이내에 약 175메가와트의 추가 부하에 해당합니다. 마이크로소프트는 GPT-4 사용자를 위해 1초 미만의 추론 지연 시간을 유지하기 위해 여러 Azure 리전에 전용 GPU 클러스터를 배치했습니다. 이는 비용과 마찬가지로 지연시간 목표가 서버의 설치 위치를 결정하는 중요한 요소로 작용하고 있음을 보여줍니다. 기존 CPU 중심의 랙은 멀티모달 학습에 필요한 메모리 대역폭과 NVLink 패브릭이 부족하여 리프레시 주기가 짧아지고 있습니다. 따라서 공급업체들은 수냉식 GPU 트레이를 표준 구성으로 출하하여 리드타임을 절반으로 줄이고, 하드웨어를 하이퍼스케일러 도입 일정에 맞추기 위해 수냉식 GPU 트레이를 표준 구성으로 출하하고 있습니다.

하이퍼스케일 및 에지 데이터센터 확장의 모멘텀

Amazon Web Services는 2030년까지 신규 용량에 1,500억 달러를 투자할 것을 약속하고 있으며, 이는 컴퓨팅 수요의 성장이 포화상태에 이르지 않았음을 시사합니다. 구글은 사우디아라비아의 NEOM 존에 1기가와트 규모의 캠퍼스를 건설 중입니다. 이 시설은 해수 냉각을 활용하여 전력사용효율(PUE) 1.1 미만을 달성하고 있으며, 사막 지역에서의 전개에 있어 모범사례가 될 수 있습니다. 5G 스탠드얼론 코어를 지원하기 위해 이미 미국에서 47개의 엣지 노드를 운영하고 있으며, 각 노드에는 최대 50대의 저지연 서버가 설치돼 있습니다. 주요 코로케이션 업체들은 테넌트에게 전체 스위트를 임대하지 않고도 AI 수요를 수용하기 위해 기존 홀에 30kW 규모의 전원 공급 설비를 추가하고 있습니다. 따라서 하이퍼스케일과 엣지 모델의 융합으로 전통적인 계층 분류가 모호해지고, 조달 기준도 재구축되고 있습니다.

고급 서버 부품공급망 변동성

HBM의 생산은 여전히 SK하이닉스와 마이크론에 집중되어 있으며, 그 결과 NVIDIA H200 서버의 리드타임은 40주, Blackwell 시스템의 대기시간은 52주에 이르고 있습니다. SK하이닉스는 HBM3e의 수율을 70%까지 끌어올렸지만, 생산능력은 2026년 중반까지 풀가동 상태입니다. 엔비디아는 수년간의 물량을 사전 계약한 고객에게 칩을 할당하고 있으며, 이러한 규모를 갖추지 못한 중견 업체들은 소외되고 있습니다. TSMC의 CoWoS 패키징 라인의 가동률이 95%를 넘어섰으며, 2026년 하반기 이후에나 상황이 완화될 것으로 예측됩니다. 그 결과, AI 최적화 서버에는 25%-30%의 프리미엄이 추가되어 고정 요금 계약에 묶여 있는 코로케이션 사업자의 수익률을 압박하고 있습니다.

부문 분석

기업들이 동시 가동 시 유지보수 비용을 전액 부담하지 않으면서도 중복성을 추구하는 가운데, 2025년 Tier 3 사이트가 데이터센터 서버 시장의 56.72%를 차지하며 시장을 장악했습니다. 다운타임으로 인한 페널티 증가에 직면한 금융 및 헬스케어 기업에 힘입어 Tier 4 도입이 CAGR 17.54%로 가속화되고 있습니다. 업타임 인스티튜트에 따르면, 2025년 신규 프로젝트의 23%가 Tier 4 인증을 요구하고 있으며, 이는 2023년 대비 9포인트 증가한 수치입니다. 고사양 시설의 경우, 서버당 800-1,200달러의 추가 비용이 들지만 단일 경로의 장애로부터 시스템을 보호하기 위해 이중 전원 공급 장치와 독립적인 냉각 루프가 통합되어 있습니다. Tier 1 및 Tier 2 환경은 단시간의 중단이 허용되고, 설비 투자 예산이 여전히 엄격한 엣지 영역에서 계속 활용되고 있습니다.

하이퍼스케일러 기업들이 기존의 계층 분류를 뛰어넘어 200밀리초 이내에 영역 간 워크로드를 라우팅하는 고유한 내결함성 체계를 도입함에 따라 아키텍처의 분화도 동시에 일어나고 있습니다. 바젤 위원회의 업무 연속성 가이드라인은 은행에 Tier 3를 최소 기준으로 삼을 것을 촉구하고 있으며, 이는 간접적으로 서버 조달 결정에 영향을 미치고 있습니다. 코로케이션 시설 소유주는 용량을 단계적으로 확장할 수 있는 모듈형 UPS 시스템을 채택하여 불확실한 테넌트의 성장에 따라 자금 유출입을 조정하고 있습니다.

2025년에는 하이퍼스케일 캠퍼스가 시장 점유율의 58.94%를 차지해, AI 트레이닝 클러스터가 50만 평방피트 이상의 부지를 선호하는 경향이 두드러졌습니다. 메타(Meta)와 마이크로소프트(Microsoft)가 기가 와트 규모의 공원을 가동하면서 이 부문은 2031년까지 연평균 복합 성장률(CAGR) 17.48%를 나타낼 것으로 예측됩니다. 대규모 지역형 데이터센터는 제2계층 클라우드 공급자 수요를 충족시키고, 중간 규모의 시설은 미드마켓 코로케이션을 지원합니다. 소규모 엣지 사이트는 많이 존재하지만, 서버 대수가 제한적이기 때문에 데이터센터 서버 시장 규모에 대한 기여도는 미미합니다.

OEM 업체들은 맞춤형 기판, 자체 펌웨어, 적시 물류를 필요로 하는 하이퍼스케일 고객을 중심으로 영업팀을 재편하고 있습니다. Quanta, Wistron 등 OEM 업체들은 수익률을 희생하더라도 양산을 우선시하여 클라우드 고객에게 분기당 5만대 규모공급을 하고 있습니다. 중견기업들은 도입을 간소화하는 동시에 벤더 종속성을 강화하는 컨버지드 인프라를 선호하는 경향이 있습니다. 엣지 사업자들은 산업용 온도 환경에 적합한 견고한 블레이드 서버를 선호하며, 이 틈새 시장은 전문 공급업체가 주도하고 있습니다.

지역별 분석

2025년 북미는 하이퍼스케일 설비투자와 액체냉각의 조기 도입에 힘입어 시장 점유율 39.83%를 차지했습니다. 이 지역은 성숙한 전력망, 풍부한 광섬유, 그리고 상승하는 토지 비용을 상쇄할 수 있는 세제 혜택의 혜택을 누리고 있습니다. 소버린 클라우드에 대한 요구사항이 적기 때문에 빠른 용량 증설을 원하는 기업에게 멀티테넌트 코로케이션은 여전히 매력적인 선택이 될 수 있습니다. 그러나 버지니아주 북부와 캘리포니아주에서 인허가 절차가 지연되면서 건설 기간이 길어지고 있으며, 사업자들은 상호 연결 승인이 빠른 중서부 및 산간 서부 지역으로 이전을 모색하고 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR)이 18.01%로 가장 빠르게 성장하는 지역입니다. 중국에서는 수출 규제로 인해 최첨단 GPU에 대한 접근이 제한되면서 국내 서버 벤더를 선호하고 있으며, 수요는 인스퍼와 화웨이의 플랫폼으로 이동하고 있습니다. 인도의 생산 연동형 인센티브 제도는 Foxconn과 Wistron의 조립공장을 유치하여 수입 관세를 절감하고, 현지 클라우드 제공업체의 리드타임을 단축하고 있습니다. 일본에서는 케이블의 근접성과 강력한 송전망을 배경으로 투자가 도쿄와 오사카에 집중되어 있는 반면, 지방 도시에서는 용량 제약에 직면해 있습니다.

유럽에서는 재생에너지 도입 의무화로 수력, 풍력 발전으로 탄소 강도가 낮은 북유럽과 아일랜드에 하이퍼스케일러의 진출이 촉진되어 시장이 안정화되고 있습니다. 프랑크푸르트와 암스테르담의 엄격한 물 사용 규제로 인해 개발업체들은 폐쇄 루프 냉각이나 브라운필드로의 전환을 강요받고 있습니다. 중동 및 아프리카는 새로운 성장축으로 부상하고 있으며, 사우디아라비아와 아랍에미리트는 경제를 탄화수소 의존에서 벗어나기 위해 디지털 인프라에 500억 달러 이상을 투자할 것을 약속하고 있습니다. 남미는 여전히 상대적으로 규모가 작지만, 브라질의 데이터 보호법으로 인해 국경을 넘어선 데이터 전송을 피하기 위한 현지 진출이 촉진되고 있습니다. 아프리카의 신생 서버 시장은 남아공과 나이지리아에 집중되어 있으며, 디젤-태양광 하이브리드 시스템이 불안정한 전력망을 보완하고 있지만, 총 비용은 선진국 벤치마크보다 최대 40% 이상 높습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The Data Center Server Market size is expected to increase from USD 110.01 billion in 2025 to USD 127.49 billion in 2026 and reach USD 268.39 billion by 2031, growing at a CAGR of 16.05% over 2026-2031.

Escalating artificial-intelligence training runs, rapid edge buildouts, and the adoption of liquid cooling are shortening refresh cycles and underpinning robust demand. Sovereign-AI mandates in Europe and the Middle East are encouraging on-premises clusters, fragmenting the data center server market away from public-cloud concentration. Hyperscale operators are standardizing on GPU-dense racks that exceed 80 kilowatts, forcing OEMs to redesign chassis around direct-to-chip liquid cooling. Supply constraints for high-bandwidth memory are prompting hyperscalers to lock in multiyear component contracts, which, in turn, stabilize medium-term shipment visibility.

Global Data Center Server Market Trends and Insights

Proliferation of AI and ML Workloads Demanding GPU-Dense Servers

Training runs for large language models already involve clusters that exceed 10,000 NVIDIA H100 or AMD MI300X accelerators, elevating rack power to levels that conventional air-cooling cannot support. Meta plans to deploy 350,000 H100-equivalent GPUs by end-2026, translating into roughly 175 megawatts of incremental load in less than two years. Microsoft provisioned dedicated GPU clusters across multiple Azure regions to maintain sub-second inference latency for GPT-4 users, highlighting how latency targets now drive server location as strongly as cost. Older CPU-centric racks lack the memory bandwidth and NVLink fabric needed for multimodal training, which is compressing refresh cycles. Server vendors are therefore shipping liquid-cooled GPU trays as baseline configurations, halving lead times and aligning hardware with hyperscaler deployment schedules.

Hyperscale and Edge Data-Center Build-Out Momentum

Amazon Web Services committed USD 150 billion through 2030 for new capacity, signaling that compute-demand growth remains far from saturation. Google is erecting a 1-gigawatt campus in Saudi Arabia's NEOM zone that leverages seawater cooling to achieve sub-1.1 power-usage effectiveness, which could serve as a template for desert deployments. Verizon already operates 47 edge nodes across the United States to support 5G standalone cores, each housing up to 50 low-latency servers. Colocation leaders are retrofitting legacy halls with 30 kilowatt feeds to capture AI demand without forcing tenants to lease entire suites. The convergence of hyperscale and edge models is therefore blurring traditional tier classifications and reshaping procurement criteria.

Supply-Chain Volatility for Advanced Server Components

HBM production remains concentrated in SK Hynix and Micron, resulting in 40-week lead times for NVIDIA H200 servers and 52-week waits for Blackwell systems. SK Hynix raised HBM3e yields to 70%, yet capacity is fully booked until mid-2026. NVIDIA allocates chips to customers that pre-commit multi-year volumes, sidelining mid-tier providers lacking such scale. TSMC's CoWoS packaging lines are operating above 95% utilization with relief not expected until late 2026. As a result, AI-optimized servers carry 25%-30% premiums, eroding margins for colocation landlords bound by fixed-rate contracts.

Other drivers and restraints analyzed in the detailed report include:

- Liquid-Cooling-Ready Server Designs Enabling More than 80 kW Racks

- Adoption of Cloud-Computing Services

- Rising CapEx for Data-Center Construction

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tier 3 sites dominated the data center server market, accounting for 56.72% of the market in 2025, as enterprises sought redundancy without the full cost of concurrent maintainability. Tier 4 adoption is accelerating at a 17.54% CAGR, driven by financial and healthcare firms confronting rising downtime penalties. The Uptime Institute noted that 23% of new projects in 2025 requested Tier 4 certification, up nine points from 2023. High-specification facilities integrate dual power supplies and independent cooling loops, adding USD 800-USD 1,200 per server but safeguarding against single-path failure. Tier 1 and Tier 2 environments persist at the edge, where brief outages are tolerable, and capex budgets remain tight.

A parallel architectural divergence is emerging as hyperscalers deploy custom resilience schemes that bypass traditional tier labels, routing workloads across zones in under 200 milliseconds. Basel Committee operational resilience guidelines are nudging banks toward Tier 3 minimums, indirectly influencing server procurement decisions. Colocation landlords are adopting modular UPS systems that scale capacity incrementally, aligning cash outflow with uncertain tenant growth.

Hyperscale campuses captured 58.94% of the market share in 2025, underscoring how AI training clusters favor footprints exceeding 500,000 square feet. The segment is tracking a 17.48% CAGR through 2031 as Meta and Microsoft commission gigawatt-scale parks. Large regional halls fill the gap for second-tier cloud providers, while medium facilities support mid-market colocation. Small edge sites, though numerous, contribute modestly to the data center server market size because they have limited server counts.

OEMs are reorganizing sales teams around hyperscale accounts that demand custom boards, proprietary firmware, and just-in-time logistics. Original design manufacturers such as Quanta and Wistron are exchanging margin for volume, delivering 50,000-unit quarters to cloud clients. Medium enterprises gravitate toward converged infrastructure that simplifies deployment but increases vendor lock-in. Edge operators favor rugged blades rated for industrial temperatures, a niche dominated by specialist suppliers.

The Data Center Server Market Report is Segmented by Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Size (Small, Medium, Large, and Hyperscale), Data Center Type (Colocation, and More), Form Factor (Half-Height Blades, Full-Height Blades, and Quarter-height/Micro-blades), Application/Workload (Virtualization and Private Cloud, HPC, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 39.83% of the market share in 2025, driven by hyperscale capital expenditure and early liquid-cooling deployments. The region benefits from mature power grids, abundant fiber, and tax incentives that offset rising land costs. Sovereign-cloud requirements are modest, so multitenant colocation remains attractive for enterprises seeking rapid capacity additions. However, permitting delays in Northern Virginia and California are lengthening construction timelines, nudging operators toward Midwest and Mountain-West alternatives with faster interconnection approvals.

Asia-Pacific is the fastest-growing region at an 18.01% CAGR through 2031. China is prioritizing domestic server vendors after export controls curtailed access to leading-edge GPUs, redirecting demand toward Inspur and Huawei platforms. India's production-linked incentive scheme is attracting Foxconn and Wistron assembly plants, reducing import duties and shortening lead times for local cloud providers. Japan clusters investments around Tokyo and Osaka due to cable proximity and resilient grids, while regional cities struggle with capacity caps.

Europe is stabilizing as renewable-energy mandates encourage hyperscalers to expand in the Nordics and Ireland where hydro and wind lower carbon intensity. Stringent water-usage regulations in Frankfurt and Amsterdam push developers toward closed-loop cooling and brownfield conversions. The Middle East and Africa are emerging corridors as Saudi Arabia and the United Arab Emirates pledge more than USD 50 billion for digital infrastructure that diversifies economies away from hydrocarbons. South America remains comparatively small, yet Brazil's data-protection law is stimulating local deployments to avoid cross-border data transfers. Africa's nascent server market concentrates in South Africa and Nigeria where diesel-solar hybrids mitigate unreliable grids, although total cost exceeds developed-market benchmarks by up to 40%.

- Dell Technologies

- Hewlett Packard Enterprise

- Lenovo Group Limited

- Fujitsu Limited

- Cisco Systems Inc.

- Kingston Technology Co. Inc.

- Huawei Technologies Co. Ltd.

- Inspur Group

- IBM Corporation

- Atos SE

- Super Micro Computer Inc.

- Quanta Cloud Technology

- ZT Systems

- Hon Hai / Foxconn Technology Group

- Advanced Micro Devices

- NVIDIA Corporation

- Oracle Corporation

- NEC Corporation

- Arista Networks

- Broadcom Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Adoption of Cloud Computing Services

- 4.2.2 Large-Scale Commercialization of 5G Networks

- 4.2.3 Hyperscale and Edge Data Center Build-Out Momentum

- 4.2.4 Proliferation of AI and ML Workloads Demanding GPU-Dense Servers

- 4.2.5 Liquid-Cooling-Ready Server Designs Enabling More than 80 kW Racks

- 4.2.6 Shift Toward ARM and RISC-V Architectures to Cut Total Cost of Ownership

- 4.3 Market Restraints

- 4.3.1 Rising CapEx for Data Center Construction

- 4.3.2 Escalating Cyber-Security and Ransomware Risks

- 4.3.3 Supply-Chain Volatility for Advanced Server Components (HBM, GPUs)

- 4.3.4 Power-Grid Constraints and Permitting Delays in Tier-1 Metros

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Tier Type

- 5.1.1 Tier 1 and 2

- 5.1.2 Tier 3

- 5.1.3 Tier 4

- 5.2 By Data Center Size

- 5.2.1 Small Data Center

- 5.2.2 Medium Data Center

- 5.2.3 Large Data Center

- 5.2.4 Hyperscale Data Center

- 5.3 By Data Center Type

- 5.3.1 Colocation Data Center

- 5.3.2 Hyperscalers Data Center/CSPs

- 5.3.3 Enterprise and Edge Data Center

- 5.4 By Form Factor

- 5.4.1 Half-height Blades

- 5.4.2 Full-height Blades

- 5.4.3 Quarter-height / Micro-blades

- 5.5 By Application / Workload

- 5.5.1 Virtualisation and Private Cloud

- 5.5.2 High-Performance Computing (HPC)

- 5.5.3 Artificial Intelligence/Machine Learning and Data Analytics

- 5.5.4 Storage-centric

- 5.5.5 Edge / IoT Gateways

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Dell Technologies

- 6.4.2 Hewlett Packard Enterprise

- 6.4.3 Lenovo Group Limited

- 6.4.4 Fujitsu Limited

- 6.4.5 Cisco Systems Inc.

- 6.4.6 Kingston Technology Co. Inc.

- 6.4.7 Huawei Technologies Co. Ltd.

- 6.4.8 Inspur Group

- 6.4.9 IBM Corporation

- 6.4.10 Atos SE

- 6.4.11 Super Micro Computer Inc.

- 6.4.12 Quanta Cloud Technology

- 6.4.13 ZT Systems

- 6.4.14 Hon Hai / Foxconn Technology Group

- 6.4.15 Advanced Micro Devices

- 6.4.16 NVIDIA Corporation

- 6.4.17 Oracle Corporation

- 6.4.18 NEC Corporation

- 6.4.19 Arista Networks

- 6.4.20 Broadcom Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment