|

시장보고서

상품코드

2044079

전자 폐기물 관리 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)E-waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

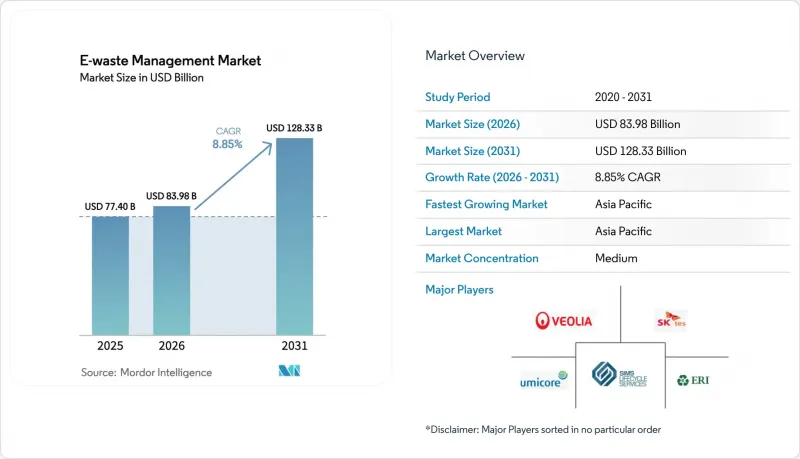

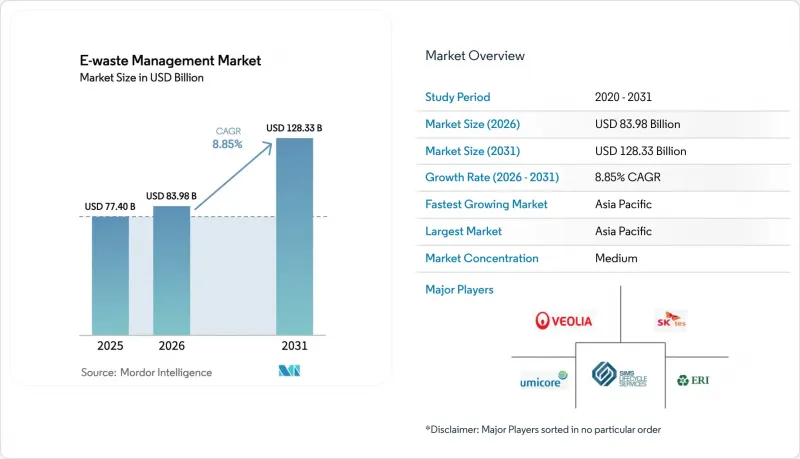

전자 폐기물 관리 시장 규모는 2025년 774억 달러에서 2026년에는 839억 8,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 8.85%로 성장을 지속하여, 2031년까지 1,283억 3,000만 달러에 이를 것으로 예측됩니다.

2025년 바젤협약 개정에 따른 사전동의(PIC) 규정 강화, 유럽연합(EU)의 70-80% 재활용 목표 설정, 인도와 중국의 70-80% 재활용 목표를 설정한 공식적인 생산자책임재활용(EPR) 의무화, 미국 연방정부의 미화 30억 달러 규모의 보조금 지원과 함께 배터리 재활용 공장에 대한 미국 연방정부의 30억 달러 이상의 보조금 지원과 함께 비공식 해체장에서 습식 제련 및 건식 제련 라인을 갖춘 허가된 처리업체로 재료 흐름이 전환되고 있습니다. 정규 재활용업체들은 로봇기술과 주문형 박리용 접착제의 도입을 확대하여 분해비용을 절감하고 있습니다. 한편, 하이퍼스케일 데이터센터의 갱신 주기로 인해 귀금속이 풍부한 고품질 인쇄회로기판이 경제협력개발기구(OECD) 시장에 공급되고 있습니다. 구리, 니켈, 리튬의 견조한 상품 가격은 도시 채굴의 경제성을 뒷받침하고 있으며, 중국, 캐나다, 브라질의 새로운 지방정부 차원의 회수 규정은 합법적인 회수 대상을 확대하여 전자 폐기물 관리 시장의 성장을 더욱 촉진하고 있습니다. 우미코아, 아우르비스 등 금속련업체들이 원료의 안정적 확보를 위해 업스트림 공정인 회수 및 선별 사업에 통합을 추진하면서 경쟁사 간 적대적 관계가 심화되고 있습니다.

세계 전자 폐기물 관리 시장 동향과 인사이트

EU, 인도, 중국의 70-80% EPR 재활용 의무화 목표와 실시간 인증서 거래

EU의 폐전기전자제품(WEEE) 지침, 인도의 '2022년 전자 폐기물 관리 규정', 중국의 보조금 제도에 따라 제조업체는 현재 중량 기준으로 70-80%의 회수율을 달성해야 합니다. 브뤼셀, 뉴델리, 베이징의 실시간 디지털 포털을 통해 제조업체는 재활용 업체로부터 전자 인증서를 구매할 수 있으며, 규정 준수가 거래 가능한 자산으로 전환되어 전자 폐기물 관리 시장에 유동성을 가져오고 있습니다. 인도 포털 사이트에서는 2024년 5월까지 1,200개의 생산자 책임 조직(PRO)이 등록되어 사무처리 비용을 20-30% 절감하고 정식 회수량 증가를 촉진했습니다. 중국은 2025년 허가받은 해체업체에 3억 9,000만 달러를 지원하여 처리 능력을 향상시키고 비정규 처리량을 억제했습니다. 이러한 정책들이 맞물려 자동화 공장에 대한 설비투자를 가속화하고, 2차 원료 공급망을 활성화하고 있습니다.

2025년 바젤협약 전자 폐기물 개정안 강화로 전 세계 사전 동의(PIC) 의무화

2025년 1월 바젤협약 개정으로 전자 스크랩은 유해(A1181) 및 비유해(Y49) 코드로 재분류되어 수출업체는 선적 전에 서면 승인을 받아야 합니다. 규정 준수 관련 서류 처리로 인해 운송 기간이 4-8주 연장되고 운임이 15-25% 상승함에 따라 2025년 상반기 전 세계 국경 간 유통량은 2024년 대비 12% 감소했습니다. EU와 북미의 허가받은 처리업체들은 이전에는 비공식적 집하장으로 유출되던 원료를 확보할 수 있게 되어 처리 능력이 향상되어 전자 폐기물 관리 시장을 지원하게 되었습니다. 소규모 중개업체들은 업무 부담 증가로 인해 이 거래에서 철수하고, 대형 물류업체들 간의 통합이 진행되었습니다. 중기적으로는 이 규정으로 인해 정규 공급망이 정착되고, 규제 대상에서 제외된 사업자의 비용 우위가 축소될 것으로 예측됩니다.

남아시아 및 동남아시아에 뿌리내린 비공식적 해체 생태계가 자재 흐름을 왜곡하고 있습니다.

인도, 파키스탄, 방글라데시, 베트남, 인도네시아, 필리핀의 비공식 재활용 업체들은 여전히 이들 국가에서 폐기되는 전자제품의 70-80%를 처리하고 있으며, 노동자들을 독성 금속에 노출시키는 야적이나 산성 침출법에 의존하고 있습니다. 비공식 사업자들은 환경 규제와 세금을 피하기 위해 허가된 시설보다 20-30% 저렴한 가격을 책정하고 있으며, 이로 인해 원료가 정식 공장에서 유출되어 비공식 시설로 흘러들어가고 있습니다. 세계보건기구(WHO)의 추산에 따르면 전 세계적으로 1,800만 명의 미성년자가 비공식적 폐기물 처리에 종사하고 있으며, 그 중 상당수가 전자 폐기물 처리에 종사하고 있습니다. 대도시권 이외 지역에서는 새로운 EPR(생산자책임재활용(EPR) 포털의 시행 상황에 편차가 있어 불법 처리장이 존속할 수 있는 상황입니다. 이러한 유출은 공인된 처리업체에 의한 회수를 방해하고 전자 폐기물 관리 시장의 수익을 압박하고 있습니다.

부문 분석

2025년, 금속은 전자 폐기물 관리 시장 점유율의 56.96%를 차지했습니다. 이는 플라스틱이나 유리에 비해 금속이 가지고 있는 우수한 본질적 가치를 반영한 것입니다. 현재 폐전자제품에서 구리의 회수량은 정제 수요의 15%를 충족하고 있으며, PCB에서 추출한 금과 팔라듐은 프리미엄 현물 가격으로 거래되고 있습니다. 아우르비스는 2025년까지 루넨과 함부르크의 복합시설에서 100만 톤 이상의 전자 스크랩을 처리하고, 반도체 및 전선 제조업체를 위해 구리, 금, 은을 회수했습니다. 하드디스크 드라이브에서 회수된 희토류 자석은 중국이 수출 쿼터를 축소하는 가운데 네오디뮴과 디스프로슘공급원이 되고 있습니다.

도시광산의 경제성은 LME(런던금속거래소) 가격의 고공행진과 1차 광산의 평균 품위 하락이라는 요인에 의해 뒷받침되고 있으며, 이로 인해 자본이 재활용 공장으로 이동하고 있습니다. 호보켄에 위치한 우미코아의 습식 야금 침출 라인은 리튬 이온 배터리용 블랙매스에서 리튬, 코발트, 니켈의 회수율을 95%까지 끌어올리고 있습니다. ISO 14001 및 R2v3 인증은 조달의 필수 요건이며, 고품질 원료는 인증된 제련소로 집중되고 있습니다. EU의 중요 원자재법에 따른 중요 원자재 할당량이 확정됨에 따라 금속 회수는 CAGR 10.45%로 확대될 것으로 예상되며, 이로 인해 전자 폐기물 관리 시장에서 금속 시장 규모는 더욱 확대될 것으로 예측됩니다.

지역별 분석

아시아태평양은 2025년 전자 폐기물 관리 시장의 44.45%를 차지했으며, 2031년까지 연평균 9.5%의 성장률을 보일 것으로 예측됩니다. 중국은 2025년 3억 9,000만 달러의 해체 보조금을 지급하여 비공식 사업자들이 라이선싱으로 전환하고, 주요 10개 도시의 연간 처리량이 두 배로 증가했습니다. 인도에서 운영 중인 EPR(생산자책임재활용(EPR) 인증 포털은 생산자가 의무를 즉시 거래할 수 있도록 하여, 정식 회수를 가속화하고 미준수 브랜드에 벌칙을 부과하고 있습니다. 일본의 '가전제품 재활용법'과 한국의 '생산자 회수제도'는 모두 회수율이 70%를 넘어 고가금속의 성숙한 유통경로를 형성하고 있습니다. 아세안 신흥경제국들은 국가적 틀을 마련하고 있지만, 여전히 시행에 어려움을 겪고 있으며, 지방에서는 비공식적인 철거장소가 여전히 존재하고 있습니다.

유럽은 2025년 2위를 차지했습니다. 이는 WEEE 지침과 물질을 역내로 유지하기 위한 바젤협약 PIC 규제 강화에 힘입은 것입니다. 그러나 2023년 65% 회수 목표를 달성한 회원국은 3개국뿐이며, EU 전체 평균은 37.5%에 그쳤습니다. 브뤼셀은 현재 더 엄격한 벌금과 CRM 회수 할당량을 제안하고 있으며, 이는 지역의 습식 제련 능력을 향상시킬 수 있습니다. 시장을 선도하는 베올리아, 알바, 스테나메탈은 수출이 줄어드는 상황에서 원료를 확보하기 위해 중소기업 인수를 추진하고 있습니다. 지침 2024/884에 따른 태양광 발전(PV)의 개별 의무로 인해 새로운 유리 대 유리(G2G) 라인이 가동되어 수익원이 다양화될 것입니다.

북미에서는 30억 달러 규모의 IIJA 및 BIL 보조금을 재원으로 처리 용량이 급증하고 있습니다. 레드우드 머티리얼즈, 어센드 엘리먼츠, 아메리칸 배터리 테크놀러지(American Battery Technology)는 신규 기지 개설 및 기존 기지 확장을 추진하고 있으며, 리사이클 사이클(Recycle Cycle)은 글렌코어(Glencore)와 블랙매스(Blackmass)에 대한 인수 계약을 체결하였습니다. 캘리포니아, 뉴욕, 워싱턴의 주정부 EPR 의무화 및 캐나다 각 주의 규제에 따라 ERI와 같은 대형 수거업체들은 국경을 초월한 프로세스 표준화를 추진하고 있습니다. 남미, 중동 및 아프리카는 아직 개발 중이지만, 브라질과 남아프리카공화국에서는 EPR 법안이 제정되어 향후 전자 폐기물 관리 시장의 성장 동력이 될 수 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트와 시장 역학

제5장 시장 규모 및 성장 예측(금액, 10억 달러)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The E-waste Management Market size is expected to grow from USD 77.4 billion in 2025 to USD 83.98 billion in 2026 and is forecast to reach USD 128.33 billion by 2031 at 8.85% CAGR over 2026-2031. Tighter Prior Informed Consent (PIC) rules under the 2025 Basel Convention amendments, formal extended-producer-responsibility (EPR) mandates that set 70-80% recycling targets in the European Union (EU), India, and China, and more than USD 3 billion in U.S. federal grants for battery-recycling plants are together steering material flows away from informal yards toward licensed processors equipped with hydrometallurgical and pyrometallurgical lines. Formal recyclers are scaling robotics and debond-on-demand adhesives to lower disassembly costs, while hyperscale data-center refresh cycles are releasing high-grade printed-circuit boards rich in precious metals into Organization for Economic Cooperation and Development (OECD) markets. Strong commodity prices for copper, nickel, and lithium sustain urban-mining economics, and new provincial take-back rules in China, Canada, and Brazil are enlarging the legal collection pool, further supporting E-waste management market growth. Competitive rivalry is intensifying as metals refiners such as Umicore and Aurubis integrate upstream into collection and sorting in order to secure feedstock certainty.

Global E-waste Management Market Trends and Insights

Mandatory 70-80% EPR Recycling Targets & Real-time Certificate Trading in EU, India, China

The EU Waste Electrical and Electronic Equipment (WEEE) Directive, India's E-waste Management Rules 2022, and China's subsidy scheme now oblige producers to meet 70-80% collection ratios by weight. Real-time digital portals in Brussels, New Delhi, and Beijing let manufacturers buy electronic certificates from recyclers, converting compliance into a tradable asset and injecting liquidity into the E-waste management market. India's portal registered 1,200 Producer-Responsibility Organizations (PROs) by May 2024, trimming paperwork costs 20-30% and driving higher formal collections. China disbursed USD 390 million in 2025 to licensed dismantlers, raising throughput and depressing informal tonnage. The combined policies accelerate capital spending on automated plants and stimulate secondary-material supply chains.

Tightened 2025 Basel Convention E-waste Amendments Mandating Prior-Informed Consent Globally

The January 2025 Basel Convention revisions recategorize electronic scrap under hazardous (A1181) and non-hazardous (Y49) codes, forcing exporters to secure written clearance before shipment. Global transboundary flows fell 12% in the first half of 2025 versus 2024 as compliance paperwork extended transit by 4-8 weeks and raised freight bills 15-25%. Licensed processors in the EU and North America gained feedstock that previously leaked to informal hubs, lifting throughput rates and supporting the E-waste management market. Smaller brokers exited the trade due to the administrative load, prompting consolidation among large logistics providers. Over the medium term, the rule is expected to cement formal supply chains while shrinking the cost advantage of unregulated operators.

Entrenched Informal Dismantling Ecosystems in South & Southeast Asia Skewing Material Flows

Informal recyclers in India, Pakistan, Bangladesh, Vietnam, Indonesia, and the Philippines still treat 70-80% of discarded electronics in these countries, relying on open-burning and acid-leaching methods that expose laborers to toxic metals. Informal operators undercut licensed facilities by 20-30% because they skip environmental controls and taxes, diverting feedstock away from formal plants. Child involvement persists; the World Health Organization (WHO) estimates 18 million minors work in informal waste globally, many in e-waste. Enforcement of new EPR portals is uneven outside metro areas, allowing illegal yards to survive. Such leakage curbs collection for certified processors and drags on the E-waste management market revenue.

Other drivers and restraints analyzed in the detailed report include:

- U.S. IIJA & BIL Funding Waves Fueling USD 3 Billion Battery-Recycling Capacity Build-out

- Debond-On-Demand Adhesives & Modular Design Standards Slashing Disassembly Costs

- 2025 Basel PIC Rules Raising Logistics & Compliance Costs for Cross-border E-scrap Shipments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metals secured 56.96% of the E-waste management market share in 2025, reflecting their superior intrinsic value relative to plastics and glass. Copper yields from end-of-life electronics now meet 15% of refined demand, and gold and palladium extracted from printed-circuit boards command premium spot prices. Aurubis processed more than 1 million t of electronic scrap at its Lunen and Hamburg complexes in 2025, recovering copper, gold, and silver for semiconductor and wire clients. Rare-earth magnets recovered from hard-disk drives add neodymium and dysprosium to the supply pool as China narrows export quotas.

Urban-mining economics benefit from persistent high LME (London Metal Exchange) prices and declining average ore grades in primary mines, which shift capital toward recycling plants. Hydrometallurgical leaching lines at Umicore's Hoboken site uplift lithium-ion black-mass recovery rates to 95% for lithium, cobalt, and nickel. ISO 14001 and R2v3 certifications have become procurement prerequisites, funneling high-grade feedstock into certified smelters. As critical-material quotas under the EU Critical Raw Materials Act firm up, metal recovery is projected to expand at a 10.45% CAGR, further enlarging the E-waste management market size for metals.

The E-Waste Management Market Report is Segmented by Material (Metals, Plastics and More), by Source (IT & Telecommunication Equipment, Consumer Electronics, and More), by Service Type (Collection, Transportation & Sorting, Disposal/Treatment, and More), and by Geography (North America, South America, Europe, Middle East and Africa, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 44.45% of the E-waste management market share in 2025 and is forecast to rise at a 9.5% CAGR through 2031. China awarded USD 390 million of 2025 dismantling subsidies that pushed informal operators toward licensing and doubled annual throughput in its top ten cities. India's live EPR-certificate portal lets producers trade obligations instantly, accelerating formal collections and imposing penalties on non-compliant brands. Japan's Home Appliance Recycling Act and South Korea's producer-take-back scheme both exceed 70% collection, creating a mature flow for high-value metals. Emerging ASEAN economies are drafting national frameworks but still struggle with enforcement; informal yards persist in rural belts.

Europe ranked second in 2025, buoyed by the WEEE Directive and the Basel PIC clampdown that keeps material inside the bloc. Yet only three member states met the 65% collection target in 2023, and the EU-wide average stood at 37.5%. Brussels now proposes tougher fines and CRM-recovery quotas that could lift regional hydrometallurgical capacity. Market leaders Veolia, ALBA, and Stena Metall are buying smaller firms to secure feedstock as exports narrow. Separate PV obligations under Directive 2024/884 will unlock new glass-to-glass lines, diversifying revenue streams.

North America is undergoing a capacity surge, anchored by USD 3 billion of IIJA and BIL grants. Redwood Materials, Ascend Elements, and American Battery Technology opened or expanded sites, and Li-Cycle secured Glencore offtake for its black mass. State EPR mandates in California, New York, and Washington plus Canada's provincial rules encourage large collectors such as ERI to standardize processes across borders. South America, the Middle East, and Africa remain nascent but Brazil and South Africa are drafting EPR bills that could seed future growth for the E-waste management market.

List of Companies Covered in this Report:

- Veolia Environnement SA

- TES - Sustainable IT Lifecycle Services

- Sims Lifecycle Services

- Umicore SA

- Electronic Recyclers International (ERI)

- Stena Metall AB

- ALBA Group

- Capital Environment Holdings Ltd.

- Enviro-Hub Holdings Ltd.

- Sembcorp Industries

- Waste Management Inc.

- Li-Cycle Holdings Corp.

- Aurubis AG

- Boliden AB

- Glencore Recycling

- MBA Polymers Inc.

- Desco Electronic Recyclers

- Enviroserve (Dubai)

- Retriev Technologies (Toxco)

- Tetronics International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights and Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightened 2025 Basel Convention E-Waste Amendments Mandating Prior-Informed Consent Globally

- 4.2.2 Mandatory 70-80 % EPR Recycling Targets & Real-time Certificate Trading in EU, India, China

- 4.2.3 U.S. IIJA & BIL Funding Waves Fueling $3 B+ Battery-Recycling Capacity Build-out

- 4.2.4 Data-Center Server Decommissioning for AI Workloads Releasing High-Grade e-Scrap in OECD

- 4.2.5 Debond-On-Demand Adhesives & Modular Design Standards Slashing Disassembly Costs

- 4.2.6 EU WEEE Directive Revision Drafts Introducing CRM-Focused Recovery Targets & Separate PV Stream

- 4.3 Market Restraints

- 4.3.1 Entrenched Informal Dismantling Ecosystems in South & Southeast Asia Skewing Material Flows

- 4.3.2 2025 Basel PIC Rules Raising Logistics & Compliance Costs for Cross-Border e-Scrap Shipments

- 4.3.3 Solid-State Battery Chemistries Lacking Industrial Recycling Routes & Safety Protocols

- 4.3.4 High-Adhesive, Miniaturized Consumer Devices Breaching New Contamination Thresholds for Plastics

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Insights on E-waste Production

- 4.8 Impact of Global Disruptions on the E-Waste Management Sector

- 4.9 Industry Attractiveness - Porter's Five Forces

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Material

- 5.1.1 Metals

- 5.1.2 Plastics

- 5.1.3 Glass

- 5.1.4 Others

- 5.2 By Source

- 5.2.1 IT & Telecommunication Equipment

- 5.2.2 Consumer Electronics

- 5.2.3 Household Appliances

- 5.2.4 Medical Equipment

- 5.2.5 Industrial Equipment

- 5.2.6 EV Batteries

- 5.2.7 Solar PV Panels

- 5.2.8 Others (Agricultural Equipment, Curb-side waste, construction, etc.)

- 5.3 By Service Type

- 5.3.1 Collection, Trasportation & Sorting

- 5.3.2 Disposal/ Treatment

- 5.3.2.1 Refurbishment & Reuse

- 5.3.2.2 Landfill/ Incineration

- 5.3.3 Recycling & Recovery

- 5.3.3.1 Mechanical Separation

- 5.3.3.2 Hydrometallurgical Process

- 5.3.3.3 Pyrometallurgical Process

- 5.3.3.4 Biometallurgical Process

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.4.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.4.3.8 Rest of Europe

- 5.4.4 Middle East and Africa

- 5.4.4.1 Saudi Arabia

- 5.4.4.2 United Arab Emirates

- 5.4.4.3 Qatar

- 5.4.4.4 Kuwait

- 5.4.4.5 Turkey

- 5.4.4.6 Egypt

- 5.4.4.7 South Africa

- 5.4.4.8 Nigeria

- 5.4.4.9 Rest of Middle East and Africa

- 5.4.5 Asia-Pacific

- 5.4.5.1 China

- 5.4.5.2 India

- 5.4.5.3 Japan

- 5.4.5.4 South Korea

- 5.4.5.5 Australia

- 5.4.5.6 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.4.5.7 Rest of Asia-Pacific

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 Veolia Environnement SA

- 6.4.2 TES - Sustainable IT Lifecycle Services

- 6.4.3 Sims Lifecycle Services

- 6.4.4 Umicore SA

- 6.4.5 Electronic Recyclers International (ERI)

- 6.4.6 Stena Metall AB

- 6.4.7 ALBA Group

- 6.4.8 Capital Environment Holdings Ltd.

- 6.4.9 Enviro-Hub Holdings Ltd.

- 6.4.10 Sembcorp Industries

- 6.4.11 Waste Management Inc.

- 6.4.12 Li-Cycle Holdings Corp.

- 6.4.13 Aurubis AG

- 6.4.14 Boliden AB

- 6.4.15 Glencore Recycling

- 6.4.16 MBA Polymers Inc.

- 6.4.17 Desco Electronic Recyclers

- 6.4.18 Enviroserve (Dubai)

- 6.4.19 Retriev Technologies (Toxco)

- 6.4.20 Tetronics International

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment