|

시장보고서

상품코드

2044100

마일드 하이브리드 자동차 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Mild Hybrid Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

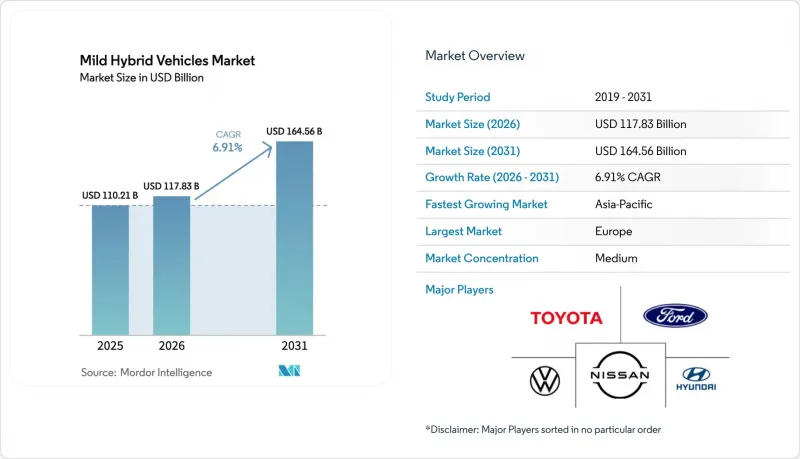

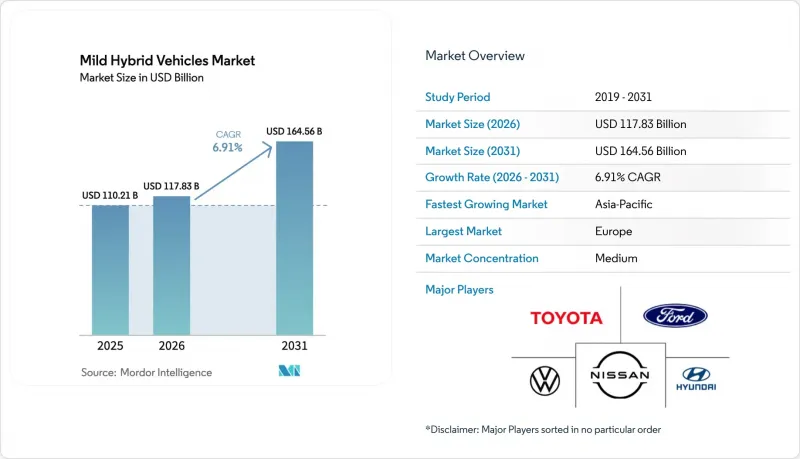

마일드 하이브리드 자동차 시장 규모는 2025년 1,102억 1,000만 달러로 평가되었습니다. 2026년 1,178억 3,000만 달러로 확대되어 2031년까지 1,645억 6,000만 달러에 이를 것으로 예상됩니다.

예측 기간(2026-2031년)의 CAGR은 6.91%를 나타낼 것으로 전망됩니다.

단기적인 전망은 유럽의 디젤차 단계적 퇴출 의무화, 리튬 이온 배터리 가격 하락, 그리고 플러그인 하이브리드 차량의 자본 비용의 일부에 불과한 48V 호환 솔루션을 선호하는 규제 동향에 의해 형성되고 있습니다. 완성차 업체들은 여전히 불안정한 경제성을 가진 완전전기차(BEV)로의 전면적인 전환을 피하고, 강화되는 CO2 규제에 대응하기 위해 마일드 하이브리드 차량을 도입하고 있습니다. Tier 1 공급업체들은 LV148 전기 표준을 중심으로 파워트레인을 재설계하고 있으며, 차량 1대당 평생 수익을 높이는 OTA(Over The Air) 기능의 수익 창출을 목표로 하고 있습니다. 한편, 나트륨 이온 배터리의 상용화로 비용에 민감한 소형 상용차 및 보급형 차량용 48V 배터리 팩의 가격이 낮아져 인도, 브라질, 동남아시아의 대상 시장이 확대되고 있습니다.

세계의 마일드 하이브리드 자동차 시장 동향 및 인사이트

전 세계 CO2 배출 규제 및 연비 규제 강화

유럽의 배출가스 규제 목표는 위반에 대한 처벌로 뒷받침되며, 48V 마일드 하이브리드는 가장 비용 효율적인 규제 대응 솔루션으로 자리매김하고 있습니다. 내연기관의 합성연료 사용을 허용하는 EU의 개정 목표에도 불구하고, 이러한 하이브리드 자동차는 여전히 유효한 선택입니다. 인도에서는 개정된 규정에 따라 마일드 하이브리드를 지속적으로 지원하는 '슈퍼 크레딧' 제도가 도입되었습니다. 마찬가지로, 중국의 플러그인 자동차 규제 변경으로 인해 예산이 48V 솔루션으로 전환되고 있으며, 이는 고급 자동차 세율 인하 및 정부 인센티브를 활용하고 있습니다. 이러한 규제 변화의 일관성은 OEM의 의사결정 과정을 가속화하고 있습니다. 그 결과, 특히 배터리 전기자동차(BEV)를 경쟁력 있는 규모로 출시할 수 없는 제조업체의 경우, 마일드 하이브리드는 틈새 시장에서 주류 선택으로 전환되고 있습니다.

저비용 48V 아키텍처로 대규모 전기화를 가능하게 하는 저비용 48V 아키텍처

자동차 제조업체들은 벨트식 스타터 제너레이터의 장점을 잘 알고 있습니다. 이는 제조 비용을 약간 증가시키고, 연료 소비를 크게 줄이며, 대량 생산 모델에서 빠른 투자 회수를 실현할 수 있습니다. 메르세데스-벤츠, BMW, 폭스바겐이 LV148 인터페이스를 채택함에 따라, 제조업체들은 플랫폼 간 부품을 공통화할 수 있게 되었습니다. 이 추가 전력 용량은 전기 터보차저, 액티브 서스펜션, 스티어 바이 와이어 기능과 같은 기술적 진보를 가능하게 합니다. 보쉬는 중국에서 48V 모듈의 양산을 시작했으며, 업계의 예측에 따르면, 그 보급은 더욱 확대될 것으로 보입니다. 그 결과, 48V 시스템은 비용에 민감한 부문에서 선호되는 전동화 옵션으로 자리 잡고 있습니다.

BEV 비용 하락으로 마일드 하이브리드의 가격 우위 축소

리튬 이온 배터리 팩의 가격이 크게 하락하고 있으며, 중국 셀 제조업체는 이미 낮은 비용으로 견적을 제시하고 있습니다. 이러한 추세로 인해 배터리 전기자동차(BEV)와 48V 마일드 하이브리드 파워트레인 간의 전통적인 비용 격차가 줄어들고 있습니다. 테슬라와 BYD는 중국 내 BEV의 엔트리 모델 가격을 동급 내연기관 세단과 동일한 수준으로 조정했습니다. 포드도 새로운 플랫폼을 채택한 저렴한 가격대의 중형 크로스오버 차량을 출시할 계획을 밝혔습니다. BEV의 총소유비용이 지속적으로 감소함에 따라, 소비자들은 특히 규제가 엄격한 지역에서 마일드 하이브리드가 제공하는 연료비 절감 효과와 BEV의 무공해 장점 및 잠재적으로 높은 재판매 가치를 비교 검토하고 있습니다. 유럽 자동차 제조업체들은 BEV 가격의 급락으로 인해 최근 48V 시스템에 대한 투자가 훼손되어 투자 회수 기간이 크게 단축될 수 있다는 우려를 표명하고 있습니다. 그 결과, 마일드 하이브리드 자동차 시장은 특히 충전 인프라가 구축되고 정부 인센티브가 완전 전기화를 점점 더 촉진하고 있는 지역에서 수익률 압박에 직면하고 있습니다.

부문 분석

2025년 승용차는 마일드 하이브리드 자동차 시장 점유율의 68.12%를 차지했습니다. 이는 자동차 제조업체들이 대량 생산되는 세단이나 SUV에 48V 시스템을 도입했기 때문입니다. 소형 상용차는 절대적인 숫자는 적지만, 2031년까지 연평균 복합 성장률(CAGR) 8.17%로 확대될 것으로 예상되며, 거점 충전보다 빠른 급유를 중시하는 플릿 계약을 통해 마일드 하이브리드 차량 시장에 추가 판매량을 추가할 것으로 예측됩니다. 유럽과 북미의 2교대 배송 루트는 현재의 인프라 제약 하에서 48V 밴이 BEV보다 총비용을 낮출 수 있는 이유를 여실히 보여주고 있습니다.

LCV(소형상용차)가 가장 큰 성장세를 보이고 있는 시장은 킬로미터당 비용이 조달을 좌우하는 시장입니다. 특히 인도와 동남아시아에서는 연료 보조금이 디젤 차량의 경제성을 떨어뜨리고 있기 때문에 나트륨 이온 배터리 팩이 비용 격차를 더욱 좁히고 있습니다. 중형 및 대형 트럭은 48V에서는 피크 출력이 제한적이기 때문에 여전히 틈새 시장에 머물러 있습니다. 이러한 가동 주기는 수소연료전지 및 800V 구동 시스템으로 전환되고 있습니다.

48V 토폴로지는 2025년 마일드 하이브리드 자동차 시장 점유율의 73.88%를 차지했고 2031년까지 연평균 복합 성장률(CAGR) 8.91%를 나타낼 것으로 예측되며, 12V 스타트-스톱 시스템이 선두를 차지하면서 그 주도권을 더욱 확대할 것으로 보입니다. OEM의 전환은 부품의 인터페이스를 표준화하고 통합 시간을 크게 단축하는 LV148 버스를 통해 촉진되고 있습니다. 단일 P0 모듈은 전체 하이브리드 비용의 약 30%로 10-17%의 연료를 절약할 수 있어 대량 생산 플랫폼에 매력적인 비용 대비 성능을 제공합니다.

풀 하이브리드 아키텍처는 CO2 슈퍼 크레딧 획득에 있어 여전히 중요하지만, 높은 가격대로 인해 일본과 EU의 일부 지역 외에는 보급이 제한되고 있습니다. 한편, 24V 솔루션은 저속 오프하이웨이 기계로 발판을 마련하고 있지만, 전 세계 판매량에 대한 기여도는 극히 미미합니다. 따라서 향후 10년간 48V 솔루션이 신규 마일드 하이브리드 자동차 시장 점유율을 지배할 것으로 예측됩니다.

지역별 분석

유럽은 1km당 93.6g의 엄격한 CO2 배출 규제와 디젤 차량의 대체 수요에 힘입어 2025년 판매량의 48.74%를 차지했습니다. 독일, 프랑스, 이탈리아, 스페인 등 4개국이 이 지역 등록대수의 3분의 2 이상을 차지하고 있습니다. 아우디의 3.0리터 V6와 스텔란티스가 곧 출시할 1.6리터 유닛과 같은 디젤 마일드 하이브리드 모델은 자동차 제조업체가 유로 7 입자상 물질 규제를 충족하는 동시에 선택적 촉매 후처리 시스템의 복잡성을 피할 수 있도록 돕고 있습니다. 동유럽은 연료 가격이 낮고 인프라 구축이 더디게 진행되어 보급이 늦어지고 있지만, 영국의 적극적인 무공해 규제로 인해 영국 내 마일드 하이브리드 자동차 시장 기회는 줄어들고 있습니다.

아시아태평양은 가장 빠르게 성장하는 지역으로 2031년까지 연평균 복합 성장률(CAGR)이 8.11%를 나타낼 것으로 예측됩니다. 중국은 현재 사치세 기준치 이하의 48V 패키지를 우대하는 PHEV 크레딧을 강화하여 이 지역을 주도하고 있습니다. 인도의 CAFE-III의 슈퍼 크레딧 제도에 따라 마일드 하이브리드 차량은 FAME II 보조금을 계속 받을 수 있으며, 인도네시아, 태국, 베트남에서는 하이브리드 차량에 대한 소비세 환급 조치가 도입되고 있습니다. 반면, 일본 제조업체는 국내 시장용 풀 하이브리드 차량에 주력하는 반면, 비용에 민감한 아세안 국가에는 48V 시스템을 수출하고 있어 지역 내 규제의 차이가 부각되고 있습니다.

북미 시장은 꾸준한 성장이 예상되며, 완만한 확대가 예상됩니다. 미국에서는 충전 환경 문제를 이유로 하이브리드 차량으로 돌아가는 소비자들이 늘어나면서 하이브리드 차량 보급이 크게 확대되고 있습니다. 스텔란티스와 포드는 트럭과 SUV 라인업을 개편하고 BEV(배터리 전기자동차)의 가격적 도전에 대비하기 위해 벨트식 시동 발전기를 내장하고 있습니다. 한편, 남미 자동차 시장은 주로 지역 세제 혜택의 영향을 받고 있습니다. 예를 들어, 상파울루주의 IPVA 면제 조치로 인해 현재 현지에서 하이브리드 자동차를 조립하는 자동차 제조업체는 우위를 점하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액(달러) 및 수량(단위))

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The mild hybrid vehicles market size is projected to grow from USD 110.21 billion in 2025 to USD 117.83 billion in 2026 and is forecast to reach USD 164.56 billion by 2031, growing at a CAGR of 6.91% during the forecast period (2026-2031).

The near-term outlook is shaped by diesel phase-out mandates in Europe, lithium-ion price deflation, and a regulatory tilt that rewards 48V compliance solutions at a fraction of the cost of plug-in hybrid capital costs. Automakers are deploying mild hybrids to bridge tightening CO2 rules without committing to the still-volatile economics of full battery-electric vehicles. Tier-one suppliers are redesigning powertrains around the LV148 electrical standard, aiming to monetize over-the-air features that lift lifetime revenue per vehicle. Meanwhile, the commercialization of sodium-ion batteries is lowering 48V pack costs for cost-sensitive light vans and entry-level cars, broadening the addressable market in India, Brazil, and Southeast Asia.

Global Mild Hybrid Vehicles Market Trends and Insights

Tightening Global CO2 / Fuel-Economy Mandates

European fleet targets for emissions, supported by penalties for non-compliance, have positioned 48V mild hybrids as the most cost-effective compliance solution . These hybrids remain relevant even with the bloc's updated goals, which allow internal combustion engines to run on synthetic fuels. In India, updated regulations introduce super-credits that continue to support mild hybrids. Similarly, changes in China's plug-in rules are redirecting budgets toward 48V solutions, which benefit from reduced luxury tax bands and government incentives. The alignment of these regulatory changes is accelerating OEM decision-making processes. As a result, mild hybrids are shifting from a niche market to a mainstream option, particularly for manufacturers unable to scale battery electric vehicles competitively.

Low-Cost 48V Architecture Enabling Mass Electrification

Automakers are recognizing the advantages of a belt-starter-generator, which slightly increases build costs but significantly reduces fuel consumption, offering a quick return on investment for high-volume models. With Mercedes-Benz, BMW, and Volkswagen adopting the LV148 interface, manufacturers can now pool parts across platforms. This additional electrical capacity enables advancements such as electric turbocharging, active suspension, and steer-by-wire features. Bosch has commenced large-scale production of 48V modules in China, and industry projections indicate widespread adoption . As a result, the 48V system is becoming the preferred electrification option for cost-sensitive segments.

Falling BEV Costs Compress Mild-Hybrid Price Advantage

Lithium-ion pack prices have declined significantly, with Chinese cell manufacturers already quoting lower costs. This trend is reducing the historical cost gap between battery-electric vehicles (BEVs) and 48V mild hybrid powertrains. Tesla and BYD have adjusted the entry-level prices of their BEVs in China to match those of comparable internal-combustion sedans. Ford has also indicated plans to introduce an affordable midsize crossover on its new platform. As the total cost of ownership for BEVs continues to decrease, consumers are comparing the fuel savings offered by mild hybrids with the zero-emission benefits and potentially higher resale values of BEVs, particularly in regulated areas. European OEMs have expressed concerns that a rapid decline in BEV prices could undermine their recent investments in 48V systems, significantly reducing the payback period. As a result, the mild hybrid vehicle market is experiencing margin pressures, especially in areas where charging infrastructure is improving, and government incentives increasingly favor full electrification.

Other drivers and restraints analyzed in the detailed report include:

- Declining Lithium-Ion Prices and Sodium-Ion Emergence

- Diesel Phase-Out in Europe Accelerating OEM Rollouts

- Inconsistent Hybrid Incentives in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger cars accounted for 68.12% of the mild hybrid vehicles market share in 2025, as OEMs deployed 48V systems across high-volume sedans and SUVs. Light commercial vans, though smaller in absolute numbers, are forecast to expand at an 8.17% CAGR to 2031, adding incremental volume to the mild hybrid vehicle market via fleet contracts that favor quick refueling over depot charging. Dual-shift courier routes in Europe and North America illustrate why 48V vans deliver lower total cost than BEVs under present infrastructure constraints.

LCV momentum is strongest where pay-per-kilometer economics dominate procurement. Sodium-ion packs further close the cost gap, especially in India and Southeast Asia, where fuel subsidies narrow diesel economics. Medium and heavy trucks remain a niche because 48V limits peak power; those duty cycles are migrating toward hydrogen fuel cells and 800-volt traction systems.

The 48V topology captured 73.88% of the mild hybrid vehicles market share in 2025 and is on track for an 8.91% CAGR through 2031, widening its leadership as 12V start-stop systems plateau. OEM migrations are catalyzed by the LV148 bus, which standardizes component interfaces and slashes integration time. A single P0 module yields 10-17% fuel savings at roughly 30% of full-hybrid cost, an attractive ratio for mass-market platforms.

Full-hybrid architectures remain relevant for CO2 super-credits, yet their premium limits penetration outside Japan and select EU segments. Conversely, 24V solutions find footholds in low-speed off-highway machinery but contribute marginally to global volume. The 48V pathway is therefore expected to dominate the new mild-hybrid vehicle market share throughout the decade.

The Mild Hybrid Vehicles Market Report is Segmented by Vehicle Type (Passenger Cars, Light Commercial Vehicles, and Medium and Heavy Commercial Vehicles), Hybrid System (12V, 24V, and 48V), Propulsion Type (Gasoline and Diesel), Battery Type (Lithium-Ion, Nickel-Metal Hydride, and Others), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Europe captured 48.74% of 2025 volume, buoyed by stringent 93.6 g CO2/km fleet rules and diesel-replacement demand. Germany, France, Italy, and Spain collectively generate more than two-thirds of regional registrations. Diesel-mild-hybrid variants-such as Audi's 3.0-liter V6 and Stellantis' upcoming 1.6-liter unit-help automakers meet Euro 7 particle metrics while avoiding selective-catalytic after-treatment complexity. Eastern European uptake lags due to lower fuel prices and slower infrastructure rollout, whereas the United Kingdom's aggressive zero-emission mandate is compressing the local mild hybrid window.

Asia-Pacific is the fastest-growing cluster, with an 8.11% CAGR through 2031. China steers the region with PHEV credit tightening that now favors 48V packages able to slip under luxury-tax thresholds. India's CAFE-III super-credits keep mild hybrids eligible for FAME II subsidies, and Indonesia, Thailand, and Vietnam deploy hybrid-targeted excise rebates. While Japanese manufacturers focus on full hybrids for their domestic market, they export 48V systems to budget-conscious ASEAN neighbors, highlighting the regulatory differences within the region.

North America is set to grow at a steady pace, with moderate expansion projected. In the United States, hybrid vehicle adoption has increased significantly, driven by some consumers turning back to hybrids due to charging challenges. Stellantis and Ford are updating their truck and SUV lineups, integrating belt-starter-generators as a buffer against potential BEV affordability challenges. Meanwhile, South America's automotive landscape is largely influenced by regional tax incentives. For instance, Sao Paulo's IPVA waiver currently gives OEMs that assemble hybrids locally an edge.

- Ford Motor Company

- General Motors Company

- Honda Motor Company Ltd

- Hyundai Motor Company

- Kia Motors Corporation

- Nissan Motor Co. Ltd.

- Mitsubishi Motors Corporation

- Toyota Motor Corporation

- Suzuki Motor Corporation

- Volkswagen AG

- BMW AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening Global CO2/ Fuel-Economy Mandates

- 4.2.2 Low-Cost 48V Architecture Enabling Mass Electrification

- 4.2.3 Declining Lithium-Ion Battery Prices and Sodium-Ion Emergence

- 4.2.4 Diesel Phase-Out in Europe Accelerating OEM Rollouts

- 4.2.5 Fleet Demand for Fuel-Efficient Light-Commercial Vans

- 4.2.6 OTA Software Upgrades Unlocking 48V Feature Revenues

- 4.3 Market Restraints

- 4.3.1 Falling BEV Costs Compress Mild-Hybrid Price Advantage

- 4.3.2 Thermal and EMC Limits on High-Power 48V Components

- 4.3.3 Tariff Volatility on Power-Electronics Supply Chain

- 4.3.4 Inconsistent Hybrid Incentives in Emerging Markets

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Investment and Funding Landscape

- 4.9 Patent Analysis

5 Market Size and Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Light Commercial Vehicles (LCVs)

- 5.1.3 Medium and Heavy Commercial Vehicles (MHCVs)

- 5.2 By Hybrid System

- 5.2.1 12V Mild Hybrid System

- 5.2.2 24V Mild Hybrid System

- 5.2.3 48V Mild Hybrid System

- 5.3 By Propulsion Type

- 5.3.1 Gasoline Mild Hybrid

- 5.3.2 Diesel Mild Hybrid

- 5.4 By Battery Type

- 5.4.1 Lithium-Ion

- 5.4.2 Nickel-Metal Hydride (NiMH)

- 5.4.3 Others (e.g., Sodium-ion, LTO)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Turkey

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Ford Motor Company

- 6.4.2 General Motors Company

- 6.4.3 Honda Motor Company Ltd

- 6.4.4 Hyundai Motor Company

- 6.4.5 Kia Motors Corporation

- 6.4.6 Nissan Motor Co. Ltd.

- 6.4.7 Mitsubishi Motors Corporation

- 6.4.8 Toyota Motor Corporation

- 6.4.9 Suzuki Motor Corporation

- 6.4.10 Volkswagen AG

- 6.4.11 BMW AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment