|

시장보고서

상품코드

2044128

유럽의 보안 테스트 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Security Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

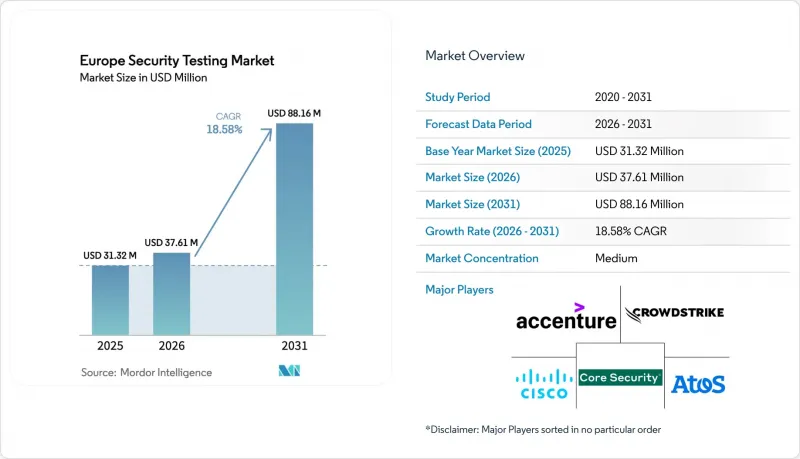

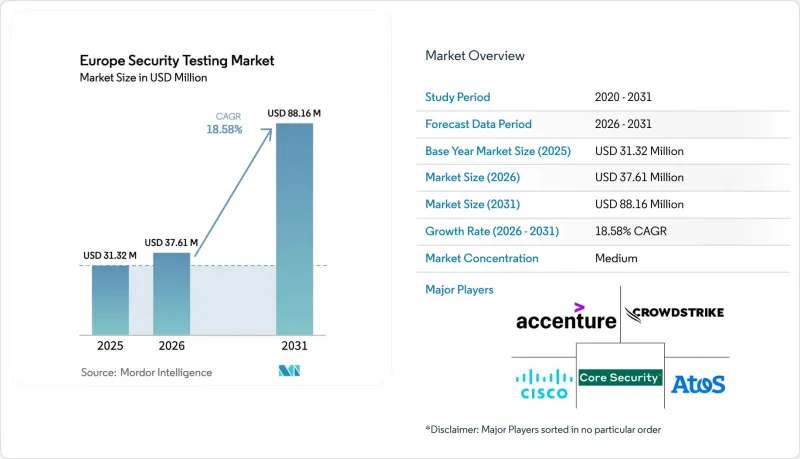

유럽의 보안 테스트 시장 규모는 2025년 3,132만 달러로 평가되었습니다. 2026년 3,761만 달러에서 2031년까지 8,816만 달러로 확대되며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 18.58%를 나타낼 전망입니다.

이러한 견조한 성장은 규제 기한이 속속 도래하고, 중요 인프라에 대한 침해가 급증하고, 클라우드 퍼스트 개발 모델이 빠르게 확산되고 있다는 점이 뒷받침하고 있습니다. 독일의 중견기업(미텔슈탄트) 공장, 프랑스의 공공 부문 디지털 주권 프로그램, 영국의 금융 서비스 탄력성 의제가 조달 우선순위를 형성하고 있는 가운데, 데이터 주권 요구와 온디맨드 확장성을 동시에 충족시키기 위한 표준적인 접근 방식 하이브리드 배포 아키텍처는 데이터 주권의 요구와 온디맨드 확장성을 동시에 충족시키기 위한 표준 접근법으로 자리 잡고 있습니다. 세계 컨설팅 기업, 용도 보안 전문 플랫폼, 그리고 지역 내 유력 기업들이 늘어나는 기술 격차에 대응하기 위해 매니지드 테스트 번들형 구독 서비스를 제공하기 위해 경쟁하면서 벤더 간 경쟁이 치열해지고 있습니다. 동시에 오감지를 억제하는 인공지능(AI) 분석이 구매 결정에 영향을 미치기 시작했으며, 특히 경고 과다 발생에 지친 조직에서는 인공지능(AI) 분석이 구매 결정을 좌우하기 시작했습니다.

유럽의 보안 테스트 시장 동향 및 인사이트

2023년 이후 전력 및 철도 분야 핵심 인프라에 대한 사이버 공격이 강화될 것

2024년부터 2025년까지 유럽의 전력 및 교통 네트워크에 대한 심각한 사고가 68% 급증함에 따라, 지속적인 테스트는 모범 사례에서 이사회 의무로 전환되었습니다. 2024년 독일 철도(Deutsche Bahn)의 랜섬웨어로 인한 혼란과 2024년 말 폴란드 전력회사에 대한 DDoS 공격은 한때 고립된 것으로 여겨졌던 OT(Operational Technology) 환경의 프로토콜 취약성을 드러냈습니다. 규제 당국은 현재 분기별 취약점 점검을 실시하지 않는 사업자에게 전 세계 매출의 최대 2%까지 벌금을 부과하고 있으며, 이에 따라 철도 및 전력망 사업자들은 다년간의 매니지드 테스트 계약을 앞당겨 체결하고 있습니다. Modbus, DNP3, IEC 61850 트래픽을 분석할 수 있는 벤더는 일반적인 자문이 아닌 구체적인 개선 방안으로 연결되는 인사이트를 제공할 수 있기 때문에 계약을 따내고 있습니다. 단기적으로는 OT 전문가들의 쟁탈전으로 인해 컨설팅 공급이 타이트해져 프로젝트 일당이 상승하고 있으며, 툴 제조업체들이 산업용 프로토콜 라이브러리를 자동 스캐너에 직접 통합하는 움직임이 가속화되고 있습니다.

EU의 NIS2 및 DORA 규정 준수 기한 조기화

NIS2를 통해 규제 대상 조직의 수는 약 2만 개에서 16만 개로 확대되었고, DORA는 2만 2천 개의 금융기관에 대해 시나리오에 기반한 엄격한 침투 테스트 의무를 추가했습니다. 이 두 가지 법령이 결합하여 이전에는 자진신고에 의존하던 신규 구매자의 안정적인 수요를 창출하고 있습니다. 독일, 프랑스 등 조기 시행 국가에서는 심각한 취약점 발견 시 72시간 내 테스트 보고서 제출을 요구하고 있으며, 이로 인해 기업들은 온디맨드 방식으로 증거자료를 생성할 수 있는 SaaS 플랫폼으로의 전환을 요구하고 있습니다. 은행에 서비스를 제공하는 클라우드 제공업체와 MSP도 감사를 받아야 하며, 공급망 전반에 걸쳐 컴플라이언스 압박이 확산되고 있습니다. 중기적으로, 이 법적 아키텍처는 보안 테스트가 지속적인 운영 비용으로 자리 잡게 하고, 벤더의 수익 예측을 안정화시키며, 유럽 전역에 걸쳐 수요의 최저선을 높일 수 있습니다.

CREST 인증 보안 테스터 부족

2025년 기준 유럽에서는 최소 6,000명의 CREST 인증 전문가가 필요했지만, 등록자는 4,200명에 불과했습니다. 시니어 테스터의 일당은 2년 동안 40% 상승했으며, 규제 대상 침투 테스트 일정 대기 기간은 최대 3개월까지 늘어났습니다. 일부 구매자는 프로젝트를 지체 없이 진행하기 위해 자격 요건을 낮추어 규제 당국이 의도한 표준화를 저해하고 있습니다. 툴 벤더들은 일시적인 대안으로 지속적인 자동 스캐닝을 내세워 이 간극을 메우고 있지만, 감독 당국은 이러한 자동화가 DORA의 위협 중심적 범위를 충족하는지 여부를 아직 확인하지 못하고 있습니다. 단기적으로는 인력 부족이 유럽의 보안 테스트 시장의 성장을 계속 저해할 것이며, 특히 독일과 네덜란드에서 임금 상승을 가속화할 것입니다.

부문 분석

클라우드 플랫폼은 2025년 매출의 48.23%를 차지했으며, 이는 유럽의 보안 테스트 시장에서 스캔당 과금이라는 경제성과 어플라이언스 오버헤드가 없습니다는 점이 매력적이라는 점을 반영합니다. 기업들이 분기별 취약점 스캔을 위한 빠른 스케일업을 우선순위에 두면서 2026년까지 수요는 견조하게 유지될 것으로 보입니다. 그러나 규제 대상인 은행과 병원이 기밀 데이터를 On-Premise에 보관하고 중앙집중식 정책 적용을 위해 메타데이터만 SaaS 콘솔로 전송하는 하이브리드 접근 방식이 18.73%로 가장 높은 CAGR을 기록했습니다. 이러한 구성은 탄력적인 컴퓨팅 기능을 희생하지 않고 각국의 데이터 주권 관련 법령을 충족시키며, 현지 데이터센터 거점을 보유한 벤더에게 우위를 가져다줍니다.

On-Premise형 어플라이언스는 현재 국방 관련 기업이나 에어 갭화된 OT 플랜트 등 축소되고 있는 틈새 시장을 대상으로 제공되고 있지만, 외부 연결이 금지된 환경에서는 여전히 필수적인 존재입니다. 각 벤더들은 기존 프라이빗 클라우드 스택에 통합할 수 있는 가상 이미지로 제공되는 컨테이너화된 스캐너로 대응하고 있으며, 향후 하이브리드화를 위한 발판을 마련하고 있습니다. 예측 기간 동안 기밀 컴퓨팅 칩셋의 개선과 EU 차원의 인증 체계로 인해 인식된 위험 격차가 줄어들 것으로 예상되며, 도입이 늦어진 기업들도 적어도 부분적인 클라우드 오케스트레이션으로 전환할 것으로 보입니다.

용도 레벨 기술은 2025년 매출의 42.73%를 차지하며, 유럽의 보안 테스트 시장에서 기업의 위험 요인을 결정하는 것은 더 이상 경계 방화벽이 아니라 악용 가능한 코드 경로라는 것을 입증했습니다. 클라우드 애플리케이션 보안 테스트는 마이크로서비스, 서버리스 기능, 임시 컨테이너는 기존 네트워크 프로브로는 검사할 수 없기 때문에 이 카테고리에서 CAGR 19.26%로 가속화되고 있습니다. 정적 분석, 동적 분석, 소프트웨어 구성 분석은 CI/CD 파이프라인 내에서 일상적으로 연계되어 있으며, 대규모 DevOps 조직에서는 매월 수천 건의 스캔이 이루어지고 있습니다.

모바일 및 웹 애플리케이션 테스트는 특히 PSD2의 보안 통신 조항에 묶여 있는 디지털 뱅킹 및 전자상거래 제공업체들 사이에서 여전히 중요한 위치를 차지하고 있습니다. 그러나 가장 큰 혁신의 자금은 클라우드 네이티브 런타임 시각화로 이동하고 있습니다. 대화형 테스트 도구는 코드에 측정 지점을 삽입하고 데이터 흐름의 증거를 상호 연관시켜 오감지를 크게 줄입니다. 현재 벤더 간 차별화 요소는 플랫폼이 GitHub Actions, GitLab CI, Bitbucket의 워크플로우에 얼마나 매끄럽게 통합되는지, 그리고 풀리퀘스트가 병합되기 전에 취약한 오픈소스 라이브러리를 식별할 수 있는지에 달려 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The Europe Security Testing Market size is projected to expand from USD 31.32 million in 2025 and USD 37.61 million in 2026 to USD 88.16 million by 2031, registering a CAGR of 18.58% between 2026 to 2031.

Robust growth is underpinned by synchronized regulatory deadlines, a sharp rise in critical-infrastructure breaches, and the rapid spread of cloud-first development models. Germany's Mittelstand factories, France's public-sector digital-sovereignty programs, and the United Kingdom's financial-services resilience agenda are shaping procurement priorities, while hybrid deployment architectures are becoming the default path to balance data-sovereignty needs with on-demand scalability. Vendor competition is intensifying as global consultancies, pure-play application security platforms, and local champions vie to offer bundled managed-testing subscriptions that address a widening skills gap. At the same time, artificial-intelligence analytics that suppress false positives are beginning to dictate buying decisions, especially among organizations fatigued by alert overload.

Europe Security Testing Market Trends and Insights

Heightened Post-2023 Critical-Infrastructure Cyber-Attacks in Power and Rail

A 68% jump in serious incidents against European power and transport networks between 2024-2025 has moved continuous testing from a best practice to a board mandate. The 2024 ransomware disruption at Deutsche Bahn and the late-2024 DDoS attacks on Polish utilities exposed protocol weaknesses in operational-technology (OT) environments once thought to be insulated. Regulators now fine entities up to 2% of global turnover for failing to run quarterly vulnerability scans, prompting rail and grid operators to pre-book multi-year managed-testing contracts. Vendors able to decode Modbus, DNP3, and IEC 61850 traffic are winning deals because they offer actionable insights instead of generic advisories. In the short term, the scramble for OT specialists is tightening consulting supply, lifting project day rates and encouraging tool makers to embed industrial-protocol libraries directly into automated scanners.

Accelerated EU NIS2 and DORA Compliance Deadlines

NIS2 expanded the pool of regulated organizations from roughly 20,000 to 160,000 and DORA added heavy, scenario-based penetration-test obligations for 22,000 financial entities. Together, the statutes have created a steady pipeline of first-time buyers that previously relied on self-attestation. Early-enforcing states such as Germany and France already ask for test reports within 72 hours of critical findings, pushing enterprises toward SaaS platforms that can generate evidence artifacts on demand. Cloud providers and MSPs serving banks must also undergo audits, cascading compliance pressure through the supply chain. Over the medium term, this legal architecture institutionalizes security testing as a recurring operating expense, smoothing revenue visibility for vendors and raising the baseline demand floor across the continent.

Shortage of CREST-Certified Security Testers

Europe needed at least 6,000 CREST-accredited professionals in 2025 but had only 4,200 on the rolls. Daily rates for senior testers rose 40% in two years, lengthening scheduling queues to as long as three months for regulated penetration tests. Some buyers have downgraded credential requirements to keep projects on track, eroding the standardization regulators intended. Tool vendors are exploiting the gap by touting continuous automated scanning as an interim substitute, but supervisors have yet to confirm whether such automation satisfies DORA's threat-led scope. In the near term, the talent drought will remain a drag on Europe security testing market growth and will amplify wage inflation, especially in Germany and the Netherlands.

Other drivers and restraints analyzed in the detailed report include:

- Shift-Left DevSecOps Adoption in Software Supply-Chain

- Industrial IoT Penetration in German Mittelstand Factories

- Budget Freeze across EU-27 SMEs amid 2024 Credit-Tightening

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud platforms generated 48.23% of 2025 revenue, reflecting the appeal of pay-per-scan economics and zero appliance overhead in the Europe security testing market size. Demand stayed strong into 2026 as enterprises prioritized rapid scale-up for quarterly vulnerability sweeps. Hybrid approaches, however, show the highest 18.73% CAGR because regulated banks and hospitals keep sensitive data on-premise, routing only metadata to SaaS consoles for centralized policy enforcement. The arrangement satisfies national data-sovereignty statutes without sacrificing elastic compute, giving vendors with local datacenter footprints an edge.

On-premise appliances now serve a shrinking niche of defense contractors and air-gapped OT plants, but they remain non-negotiable where external connections are prohibited. Vendors are responding with containerized scanners shipped as virtual images that slot into existing private-cloud stacks, creating a stepping stone toward future hybrid conversions. Over the forecast window, improvements in confidential-computing chipsets and EU-level certification schemes are likely to narrow the perceived risk gap, nudging late adopters toward at least partial cloud orchestration.

Application-level techniques represented 42.73% of 2025 turnover, confirming that exploitable code paths, not perimeter firewalls, now define enterprise exposure across the Europe security testing market. Within this bucket, cloud application security testing is accelerating at 19.26% CAGR because microservices, serverless functions, and ephemeral containers cannot be scanned by legacy network probes. Static analysis, dynamic analysis, and software composition analysis are routinely chained together in CI/CD pipelines, pushing scan counts into the thousands each month for large DevOps shops.

Mobile and web application testing remains relevant, particularly among digital-banking and e-commerce providers bound by PSD2 secure-communication clauses. Yet the deepest innovation capital is migrating to cloud-native runtime visibility, where interactive testing tools instrument code and correlate data-flow evidence to slash false positives. Vendor differentiation now stems from how seamlessly platforms slot into GitHub Actions, GitLab CI, and Bitbucket workflows, and from their ability to flag vulnerable open-source libraries before pull requests are merged.

The Europe Security Testing Market Report is Segmented by Deployment (On-Premise, Cloud, and Hybrid), Type (Network Security Testing Including VPN Testing, and Application Security Testing Including Mobile), Testing Type (SAST, DAST, IAST, and RASP), End-User Industry (Government, BFSI, and More), Testing Tool (Web Application Testing Tool, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Accenture plc

- Atos SE

- Cisco Systems, Inc.

- Core Security, LLC

- CrowdStrike Holdings, Inc.

- Fortinet, Inc.

- Hewlett Packard Enterprise Company

- IBM Corporation

- Tenable Holdings, Inc.

- Micro Focus International plc

- Snyk Limited

- HackerOne, Inc.

- Offensive Security, LLC

- Orange Cyberdefense SAS

- Paladion Networks Private Limited

- PricewaterhouseCoopers International Limited

- Qualys, Inc.

- Securonix, Inc.

- Synopsys, Inc.

- Veracode, Inc.

- Rapid7, Inc.

- Checkmarx Ltd.

- NCC Group plc

- TUV Rheinland AG

- Bureau Veritas S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Heightened Post-2023 Critical-Infrastructure Cyber-Attacks in Power and Rail

- 4.2.2 Accelerated EU NIS2 and DORA Compliance Deadlines

- 4.2.3 Shift-Left DevSecOps Adoption in Software Supply-Chain

- 4.2.4 Industrial IoT Penetration in German Mittelstand Factories

- 4.2.5 Mandatory Penetration-Testing Clauses in European Public-Sector Tenders

- 4.2.6 Quantum-Resistant Crypto Migration Pilots

- 4.3 Market Restraints

- 4.3.1 Shortage of CREST-Certified Security Testers

- 4.3.2 Budget Freeze across EU-27 SMEs amid 2024 Credit-Tightening

- 4.3.3 Fragmented Data-Sovereignty Rules Slowing Cloud-Based Testing

- 4.3.4 False-Positive Fatigue Reducing Test Frequency

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 On-Premise

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By Type

- 5.2.1 Network Security Testing

- 5.2.1.1 VPN Testing

- 5.2.1.2 Firewall Testing

- 5.2.1.3 Other Service Types

- 5.2.2 Application Security Testing

- 5.2.2.1 Mobile Application Security Testing

- 5.2.2.2 Web Application Security Testing

- 5.2.2.3 Cloud Application Security Testing

- 5.2.2.4 Enterprise Application Security Testing

- 5.2.1 Network Security Testing

- 5.3 By Testing Type

- 5.3.1 SAST

- 5.3.2 DAST

- 5.3.3 IAST

- 5.3.4 RASP

- 5.4 By End-User Industry

- 5.4.1 Government

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Manufacturing

- 5.4.5 IT and Telecom

- 5.4.6 Retail

- 5.4.7 Other End-User Industries

- 5.5 By Testing Tool

- 5.5.1 Web Application Testing Tool

- 5.5.2 Code Review Tool

- 5.5.3 Penetration Testing Tool

- 5.5.4 Software Testing Tool

- 5.5.5 Other Testing Tools

- 5.6 By Country

- 5.6.1 United Kingdom

- 5.6.2 Germany

- 5.6.3 France

- 5.6.4 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 Atos SE

- 6.4.3 Cisco Systems, Inc.

- 6.4.4 Core Security, LLC

- 6.4.5 CrowdStrike Holdings, Inc.

- 6.4.6 Fortinet, Inc.

- 6.4.7 Hewlett Packard Enterprise Company

- 6.4.8 IBM Corporation

- 6.4.9 Tenable Holdings, Inc.

- 6.4.10 Micro Focus International plc

- 6.4.11 Snyk Limited

- 6.4.12 HackerOne, Inc.

- 6.4.13 Offensive Security, LLC

- 6.4.14 Orange Cyberdefense SAS

- 6.4.15 Paladion Networks Private Limited

- 6.4.16 PricewaterhouseCoopers International Limited

- 6.4.17 Qualys, Inc.

- 6.4.18 Securonix, Inc.

- 6.4.19 Synopsys, Inc.

- 6.4.20 Veracode, Inc.

- 6.4.21 Rapid7, Inc.

- 6.4.22 Checkmarx Ltd.

- 6.4.23 NCC Group plc

- 6.4.24 TUV Rheinland AG

- 6.4.25 Bureau Veritas S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet Need Analysis