|

시장보고서

상품코드

2044133

전기생리학 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Electrophysiology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

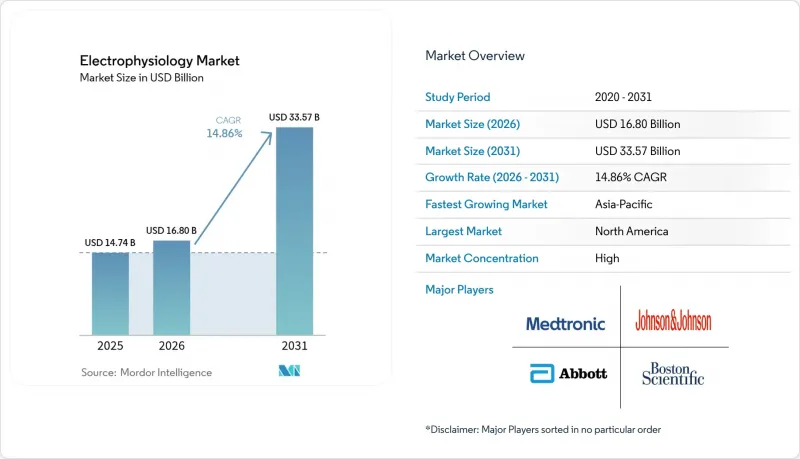

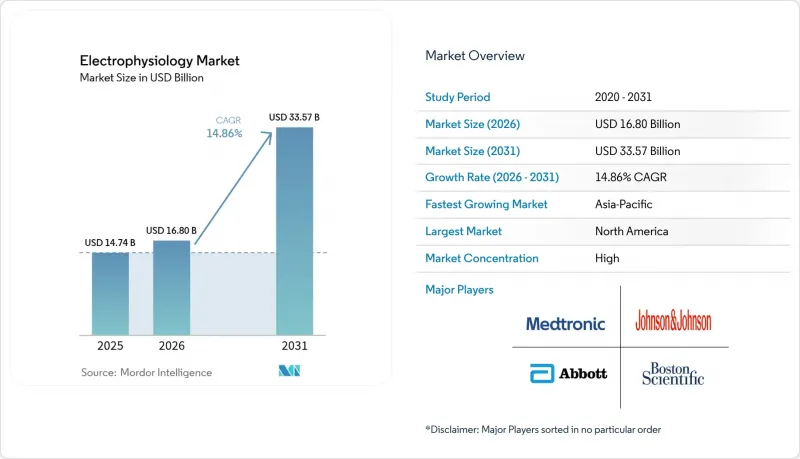

전기생리학 시장 규모는 2025년 147억 4,000만 달러에서 2026년에는 168억 달러로 확대되어 2026년부터 2031년까지 CAGR 14.86%로 성장을 지속하여, 2031년에는 335억 7,000만 달러에 이를 것으로 예측됩니다.

이러한 성장은 펄스필드절제술(PFA) 기술의 급속한 보급, 고령화에 따른 시술 건수 증가, 심방세동 환자의 외래 진료로의 꾸준한 전환에 힘입은 바 있습니다. 특히, 메디케어의 급여 범위 확대가 첨단 검사실에 대한 설비투자를 뒷받침하는 한편, 산업 구조조정으로 인해 지적재산권은 소수의 대형 의료기기 제조업체에 집중되고 있습니다. 아시아태평양은 다른 어떤 지역보다 빠른 속도로 신규 설비를 증설하고 있지만, 북미는 여전히 가장 큰 수익원이 되고 있습니다. 이러한 요인들이 복합적으로 작용하여 2030년까지 전기생리학 시장은 다른 많은 심혈관 기기 분야를 능가하는 성장세를 보일 것으로 예측됩니다.

세계 전기생리학 시장 동향 및 인사이트

심방세동 유병률 증가

인구 고령화에 따라 심방세동 발생률이 증가하고 있으며, 유럽 내 심방세동 유병률은 향후 30년간 2배로 증가할 것으로 예측됩니다. 신흥국에서는 젊은 층에서도 좌식 생활습관으로 인한 부정맥이 나타나면서 기존 대상층을 넘어 환자층이 확대되고 있습니다. 지속형 심방세동은 시술 시간을 단축하고 소작 부위의 품질을 향상시키는 첨단 매핑 및 듀얼 에너지 시스템에 대한 수요를 주도하고 있습니다. 아시아태평양의 정부 지원 스크리닝 프로그램으로 인해 미진단 사례가 더 많이 발견되어 이미 부족한 전기생리학 검사실의 환자 수가 증가하고 있습니다. 환자 1인당 연간 45,000달러가 넘는 뇌졸중 예방비용은 조기 절제술 치료를 승인하는 데 있어 보험자 입장에서 강력한 경제적 근거가 되고 있습니다.

절제 및 매핑 시스템의 급속한 혁신

PFA는 고주파 절제술 이후 가장 획기적인 치료법입니다. 조직 선택성으로 열 손상을 방지하고, 안전 마진을 향상시키며, 시술자의 자신감을 높여줍니다. 인공지능(AI)을 활용한 매핑 소프트웨어는 계획 시간을 단축하고 첫 번째 격리 성공률을 높입니다. 듀얼 에너지 카테터로 복잡한 부정맥의 단회 시술이 가능해졌고, 절제술 재시술률이 10% 미만으로 낮아졌습니다. 왼쪽 다리 블록 영역 페이싱과 같은 리드리스 페이싱 기술의 발전은 하드웨어와 관련된 합병증을 해소하고 새로운 시술의 길을 열어주었습니다. 이러한 발전은 의사의 도입 장벽을 낮추고 전기생리학 시장을 확대하는 데 기여하고 있습니다.

훈련된 전기생리학자 및 EP 간호사 부족

펠로우십 프로그램에서는 연간 3-4명의 연수생을 받아들이고 있지만, 실제로는 8-10명의 졸업생이 필요한데, 이것이 성장의 걸림돌이 되고 있습니다. 새로운 PFA 기술에서도 숙련도에 도달하기 위해서는 여전히 50-100건의 지도하에 케이스 경험이 필요합니다. 병원에서는 교육 기간을 8개월로 단축하는 크로스 트레이닝 커리큘럼을 시범적으로 도입하고 있지만, 만약 그 자리를 채우지 못하면 해당 부서의 수익이 연간 최대 300만 달러까지 감소할 수 있습니다. 전문의협회는 인증 취득을 가속화하기 위해 '2+2' 교육 모델을 제안하고 있습니다. 한편, AI를 활용한 문서 작성 업무의 자동화로 기존 전문의는 더 많은 시술에 집중할 수 있게 됩니다.

부문 분석

PFA의 우수한 안전성을 뒷받침하는 임상적 증거로 인해 자본 예산이 기존 전파 및 냉동 치료 플랫폼으로 이동하고 있습니다. AI의 통합으로 포인트별 안내가 빨라지고, 시술의 효율성이 향상되어 매핑 및 내비게이션 시스템의 도입이 가속화되고 있습니다. 기록 시스템은 클라우드 기반으로 전환되고 있으며, 원격지에서 영상 진단이 가능해져 필요한 인력을 줄이고 있습니다. 진단용 카테터는 단일 기기가 아닌 풀 서비스형 플랫폼으로 통합되면서 완만한 성장세를 보이고 있습니다. 하이브리드 수술실 도입에 따라 검사 영상 진단 하드웨어에 대한 수요도 증가하고 있으며, 이는 전기생리학 산업의 병원 투자 주기를 뒷받침하고 있습니다.

경쟁적 차별화는 개별 기기에서 시스템 수준의 통합으로 이동하고 있습니다. 원활한 소프트웨어 및 하드웨어 생태계를 제공하는 공급업체는 병원의 지지를 확고히 하고 소모품으로 지속적인 수익을 창출하고 있습니다. 액세스 디바이스는 여전히 필요하지만, 그 중 상당수는 상품화되어 있습니다. 공급업체는 이를 수익 창출의 수단으로 삼는 것이 아니라, 제품 포트폴리오를 강화하기 위해 활용하고 있습니다. 전반적으로 전기생리학 시장은 제품 통합의 혜택을 받고 있으며, 이는 구매 결정을 단순화하고 기술 업데이트를 가속화하고 있습니다.

지역별 분석

북미 시장은 광범위한 보험 적용 범위와 높은 기기 보급률에 힘입어 성장하고 있습니다. 2025년 의사 보수표 2.93% 삭감이 성장을 억제하는 요인으로 작용하고, 심방세동 발병률 상승으로 시술 건수는 견조하게 유지되고 있습니다. 유럽은 성숙한 시장 패턴을 보이고 있으며, 의료기기 규정(MDR)에 기반한 표준화를 통해 회원국 간 기술 이전이 원활하게 이루어지고 있습니다. 병원의 통합으로 구매력이 집중되고 수량에 따른 할인이 촉진되는 한편, 매핑 시스템의 업데이트 주기도 빨라지고 있습니다.

아시아태평양이 가장 높은 CAGR을 기록했는데, 이는 중국의 '건강 중국 2030' 이니셔티브에 따라 카테터 검사실 건설에 대한 보조금이 지급되고 고급 절제술에 대한 보험 환급이 가능해졌기 때문입니다. 인도의 민간 부문은 카테터 검사실에 많은 투자를 하고 있으며, 한 대형 체인은 2,200개의 병상과 AI 기반 전기생리학(EP) 스위트를 추가하고 있습니다. 일본은 1인당 시술률이 높은 수준을 유지하고 있으며, 최근 보스턴 사이언티픽의 FARAPULSE가 승인된 것은 새로운 PFA 시스템에 대한 규제 당국의 빠른 수용을 시사하고 있습니다.

아랍에미리트(UAE)는 GDP 대비 의료비 비중을 5%에서 5.4%로 끌어올리며 복잡한 절제술에 대한 수요를 촉진하는 등 중동에서는 의료관광이 타겟이 되고 있습니다. 라틴아메리카에서는 제한적인 가능성을 볼 수 있습니다. 브라질의 경제 회복으로 설비투자 예산이 증가하고 있지만, 수입 관세와 라이선스 요건으로 인해 새로운 플랫폼의 도입이 지연되고 있습니다. 현지 제조 파트너십과 유연한 자금 조달을 통해 이러한 장벽이 완화되어 다양한 지역에서 전기생리학 시장은 꾸준한 상승세를 유지하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측(금액 : 달러)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The Electrophysiology Market size is expected to grow from USD 14.74 billion in 2025 to USD 16.80 billion in 2026 and is forecast to reach USD 33.57 billion by 2031 at 14.86% CAGR over 2026-2031.

This growth rests on swift adoption of pulsed field ablation (PFA) technologies, rising procedural volumes tied to aging populations, and the steady shift of atrial fibrillation cases to outpatient settings. Broader reimbursement, especially from Medicare, is sustaining capital investment in advanced laboratories while industry consolidation concentrates intellectual property in the hands of a few large device makers. Asia-Pacific is adding new capacity at a faster pace than any other region, but North America still delivers the largest revenue pool. Collectively, these factors position the electrophysiology market to outpace many other cardiovascular device categories through 2030.

Global Electrophysiology Market Trends and Insights

Rising Prevalence of Atrial Fibrillation

Atrial fibrillation incidence is climbing as populations age, with European prevalence expected to double over the next three decades. Younger cohorts in emerging countries are now presenting with arrhythmias tied to sedentary lifestyles, expanding the candidate pool beyond traditional demographics. Persistent forms of the disease are driving demand for sophisticated mapping and dual-energy systems that shorten procedure time and improve lesion quality. Government-funded screening programs in Asia-Pacific detect more undiagnosed cases, adding volume to already strained electrophysiology laboratories. Stroke prevention costs of more than USD 45,000 per patient per year provide payers with a strong financial rationale to approve early ablation interventions.

Rapid Innovation in Ablation & Mapping Systems

PFA is the most disruptive modality since radiofrequency ablation. Its tissue-selective properties avoid thermal injury, improving safety margins and boosting operator confidence. Artificial-intelligence-guided mapping software reduces planning time and raises first-pass isolation rates.Dual-energy catheters now permit single-session treatment of complex arrhythmias, lowering repeat ablation incidence below 10%. Leadless pacing developments, such as left bundle branch area pacing, remove hardware complications and open new procedural pathways. Together, these advances expand the electrophysiology market by reducing barriers to physician adoption.

Shortage of Trained Electrophysiologists and EP Nurses

Fellowship programs accommodate 3-4 trainees annually when 8-10 graduates are needed, constraining growth. New PFA technologies still require 50-100 supervised cases to reach competence. Hospitals are piloting cross-training curricula that shorten onboarding to eight months, but unfilled positions can reduce departmental revenue by up to USD 3 million per year. Professional societies propose two-plus-two training models to accelerate certification. Meanwhile, AI-driven automation of documentation tasks frees existing specialists to handle more procedures.

Other drivers and restraints analyzed in the detailed report include:

- Growing Preference for Minimally-Invasive Catheter Procedures

- Accelerated Adoption of Pulsed Field Ablation Systems

- High Capital Cost of State-of-the-Art EP Labs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Clinical evidence confirming PFA's superior safety is diverting capital budgets away from legacy radiofrequency and cryo platforms. Mapping and navigation systems gain momentum because AI integration delivers faster point-by-point guidance, boosting procedure efficiency. Recording systems shift to cloud-based formats, allowing off-site interpretation and lowering staffing needs. Diagnostic catheters grow slowly as they bundle into full-service platforms rather than independent devices. Laboratory imaging hardware rises in tandem with hybrid operating room installations, anchoring hospital investment cycles in the electrophysiology industry.

Competitive differentiation is moving from individual devices to system-level integration. Suppliers that offer seamless software-hardware ecosystems lock in hospital preferences and create recurring revenue from consumables. Access devices remain necessary but mostly commoditized; suppliers leverage them to complete portfolios rather than drive profit. Overall, the electrophysiology market benefits from product convergence that simplifies purchasing decisions and accelerates technology refresh.

The Electrophysiology Market Report Segments the Industry Into by Product Type (Ablation Catheters, Diagnostic Catheters, Laboratory Devices, Mapping & Navigation Systems, and More), Indication (Atrial Fibrillation, Atrial Flutter, and More ), End User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America is supported by broad insurance coverage and high device adoption. Physician fee-schedule cuts of 2.93% in 2025 temper growth, yet procedure volumes stay resilient due to rising atrial fibrillation incidence. Europe follows a mature pattern, with standardization under the Medical Device Regulation easing technology migration across member states. Hospital consolidation concentrates purchasing power, encouraging volume-based discounts but also accelerating refresh cycles for mapping systems.

Asia-Pacific records the fastest CAGR, as China's Healthy China 2030 initiative subsidizes catheter-laboratory construction and reimburses advanced ablation procedures. India's private sector invests heavily in catheter labs, with one leading chain adding 2,200 beds and AI-enabled EP suites. Japan maintains high per-capita procedure rates and recently cleared Boston Scientific's FARAPULSE, signaling quick regulatory acceptance for new PFA systems.

The Middle East targets medical tourism, with the United Arab Emirates increasing healthcare spending from 5% to 5.4% of GDP, bolstering demand for complex ablations. Latin America offers selective promise: Brazil's economic rebound lifts capital budgets, but import duties and licensing requirements slow roll-outs of newer platforms. Local manufacturing partnerships and flexible financing mitigate these hurdles, keeping the electrophysiology market on a steady upward trajectory across diverse regions.

- AtriCure

- BIOTRONIK

- Boston Scientific

- CardioFocus Inc.

- CathVision ApS

- GE HealthCare Technologies Inc.

- Imricor Medical Systems

- Johnson & Johnson

- Kardium

- Koninklijke Philips

- Lepu Medical

- Medtronic

- MicroPort

- OSYPKA

- Siemens Healthineers

- Stereotaxis

- Synaptic Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Atrial Fibrillation & Other Arrhythmias

- 4.2.2 Rapid Technology Innovation in Ablation & Mapping Systems

- 4.2.3 Growing Preference for Minimally Invasive Catheter Procedures

- 4.2.4 Accelerated Adoption of Pulsed Field Ablation (PFA) Systems

- 4.2.5 Broader Reimbursement & EP-Lab Build-Outs in Emerging Markets

- 4.2.6 Hybrid "One-Stop" EP-OR Centers Lifting Procedure Throughput

- 4.3 Market Restraints

- 4.3.1 Shortage of Trained Electrophysiologists and EP Nurses

- 4.3.2 High Capital Cost of State-Of-The-Art EP Labs

- 4.3.3 Payer Caution Over Long-Term PFA Safety/Efficacy Evidence

- 4.3.4 Radiation-Dose Scrutiny Delaying Fluoroscopy-Based Installs

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Ablation Catheters

- 5.1.2 Diagnostic Catheters

- 5.1.3 Laboratory Devices

- 5.1.4 Mapping & Navigation Systems

- 5.1.5 EP Recording Systems

- 5.1.6 Access Devices

- 5.1.7 Other Products

- 5.2 By Indication

- 5.2.1 Atrial Fibrillation

- 5.2.2 Atrial Flutter

- 5.2.3 AV Nodal Re-entry Tachycardia (AVNRT)

- 5.2.4 Ventricular Tachycardia

- 5.2.5 Other Arrhythmias

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Specialty Cardiac Centers

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AtriCure, Inc.

- 6.3.2 Biotronik SE & Co. KG

- 6.3.3 Boston Scientific Corporation

- 6.3.4 CardioFocus Inc.

- 6.3.5 CathVision ApS

- 6.3.6 GE HealthCare Technologies Inc.

- 6.3.7 Imricor Medical Systems

- 6.3.8 Johnson & Johnson

- 6.3.9 Kardium Inc.

- 6.3.10 Koninklijke Philips N.V.

- 6.3.11 Lepu Medical Technology

- 6.3.12 Medtronic

- 6.3.13 MicroPort Scientific Corporation

- 6.3.14 Osypka AG

- 6.3.15 Siemens Healthineers

- 6.3.16 Stereotaxis Inc.

- 6.3.17 Synaptic Medical