|

시장보고서

상품코드

2044147

색 크라프트지 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Sack Kraft Paper - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

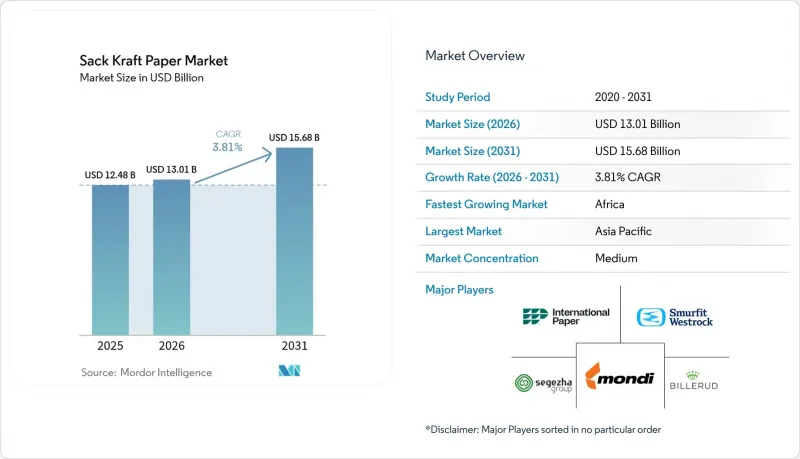

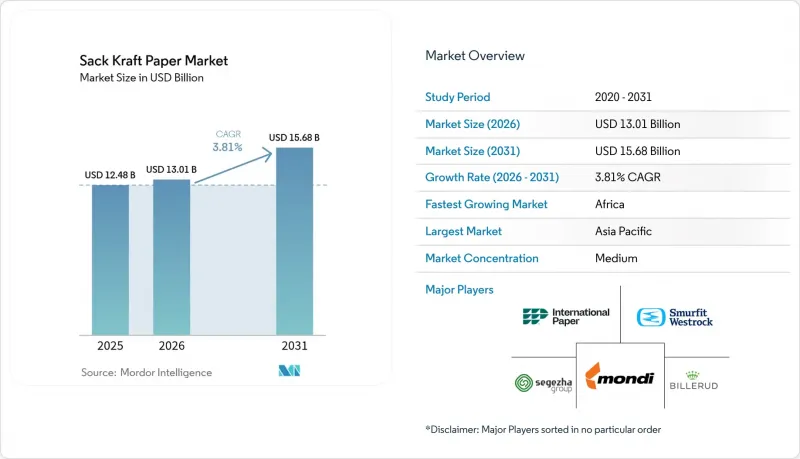

색 크라프트지 시장 규모는 2025년에 124억 8,000만 달러로 평가되었고 2026년 130억 1,000만 달러에서 2031년까지 156억 8,000만 달러에 이를 것으로 예측되며, 2026-2031년까지 연평균 복합 성장률(CAGR)은 3.81%를 나타낼 전망입니다.

이 견조한 총액의 이면에는 구조적 변화가 숨겨져 있습니다. 플라스틱 제품 금지법, 탄소 국경 조정 메커니즘, 디지털화된 공급망으로 인해 시멘트, 식품 원료, 광물 처리 부문에서 직조 폴리프로필렌 벌크 백에서 재활용 가능한 다층 종이 백으로 대체가 가속화되고 있습니다. 통합형 제조업체는 고부가가치 계약을 확보하기 위해 배리어 코팅과 RFID 대응 가공 라인을 갖춘 공장으로 설비 업데이트를 진행하고 있으며, 가공업체는 포장 속도를 두 배로 높이고 인건비를 3분의 1로 줄일 수 있는 FFS(Form Fill Seal) 설비 도입을 서두르고 있습니다. 버진펄프와 사용 후 골판지 용기의 원재료 가격 변동은 여전히 수익률을 압박하고 있지만, 수직 통합과 장기 섬유 계약으로 가격 변동의 영향은 완화되고 있습니다. 운송 시 배출가스 감소의 필요성에 힘입어, 25-50kg의 시멘트 및 비료 용도에서 경량 단층 탄성 종이가 주류가 되고 있습니다. 자동화에 대응하고 가정 쓰레기로 재활용할 수 있는 설계가 미래 수요를 뒷받침하고 있으며, 이로 인해 봉투용 크라프트지 시장은 세계 순환 경제 정책의 전략적 수혜를 받을 수 있는 위치에 있습니다.

세계 색 크라프트지 시장 동향 및 인사이트

플라스틱 금지법으로 종이 대체 가속화

일회용 플라스틱의 금지로 인해 벌크 포장의 폴리프로필렌 직물의 대체 주기가 단축되고 있습니다. 일회용 플라스틱에 대한 규제 움직임으로 인해 벌크 포장용 폴리프로필렌 직조 봉투의 대체 일정이 앞당겨지고 있습니다. 2024년 최종 결정된 유럽 연합(EU)의 '포장 및 포장 폐기물 규정'은 2030년까지 포장재의 65%를 재활용할 수 있도록 의무화하고, 옥소분해성 플라스틱을 전면 금지하고 있습니다. 이로 인해 시멘트 및 비료 유통업체들은 지자체 종이 재활용 시스템의 적용을 받는 다층 크래프트 백으로 전환할 수밖에 없는 상황입니다. 영국에서는 확대된 생산자책임재활용제도(EPR)에 따라 2025년부터 재활용이 불가능한 포장재에 대해 톤당 200파운드의 과징금이 부과될 예정으로, 폴리프로필렌 FIBC의 적재 비용이 18-22% 상승하고 있으며, 이 과징금을 회피할 수 있는 종이 대체품으로의 조달 전환이 진행되고 있습니다. 이 요인은 규정 준수가 의무화되고 즉각적인 대응이 필요하기 때문에 크래프트 종이봉투 시장에 가장 큰 긍정적인 영향을 미치고 있습니다.

시멘트 산업의 탈탄소화, 재활용 가능한 가방에 힘을 실어줍니다.

세계 시멘트 제조업체들은 Scope 3의 포장 관련 배출량을 넷제로 로드맵에 반영하고 있습니다. 2025년 라이프사이클 평가에 따르면, 사용 후 재활용을 고려했을 때 크래프트 백은 동급 폴리프로필렌 백에 비해 CO2 배출량이 60% 더 적은 것으로 입증되었습니다. 대표적인 프로젝트로는 스페인에서 이미 시판 중인 수용성 단층 크래프트 백인 몬디(Mondi)와 세멕스(Cemex)의 솔믹스백(SolmixBag), 2027년까지 인도 소매 포트폴리오의 30%를 재생 크래프트 종이로 전환하겠다는 울트라텍 시멘트(UltraTech Cement)의 약속이 있습니다. 시멘트(UltraTech Cement)의 약속을 들 수 있습니다. 유럽의 순환형 건설 시범사업에서는 재사용 가능한 크래프트 봉투를 대상으로 보증금 반환제도를 검사 도입하여 빈 봉투를 회수한 시공사에 포상금을 지급하고 있습니다. 시멘트가 2025년 수요의 5분의 2 이상을 차지했기 때문에 이 부문의 탈탄소화 선택은 중기적으로 크래프트 백 시장의 궤도를 크게 재조정할 것입니다.

벌크 포장에 PP 직조 FIBC의 보급 확대

전도성 및 정전기 방지 기능을 갖춘 연질 중간 벌크 컨테이너(FIBC)는 화학 물질 및 가연성 분말에서 크래프트 종이로는 대응할 수 없는 안전성과 재사용성 요구를 충족시킵니다. C형 FIBC는 개당 8-12달러인 반면, 동급 정전기 방지 라이너가 있는 다층 크라프트지는 15-20달러로, FIBC가 5-10회 운송 사이클을 완료할 수 있다는 점에서 이 가격 차이는 더욱 확대됩니다. 따라서 플라스틱 수지, 광물 농축물, 자동차 부품의 폐쇄형 공급망에서 폴리프로필렌이 계속 지정되어 색 크라프트지 시장에 -0.6%의 부정적인 영향을 미치고 있습니다.

부문 분석

Form Fill Seal(FFS) 봉지는 봉지용 크라프트지 시장 규모에서 상당한 비중을 차지하고 있으며, CAGR 4.78%를 기록했습니다. 이는 자동화 라인이 시간당 최대 1,800개까지 채울 수 있고, 밸브 시스템보다 2배 빠른 속도이기 때문입니다. 시멘트 및 화학 제조업체는 봉제 작업을 30-40% 줄이고 포장 정확도를 향상시키기 위해 FFS를 채택하고 있으며, 마찰 계수가 제어된 FFS 지원 용지는 밀봉 강도를 유지합니다. 밸브형 백은 2025년 41.32%의 점유율을 차지해, 방진 및 기존 공압식 충전이 주류인 부문에서 여전히 필수적인 역할을 할 것으로 보입니다. 오픈 마우스 유형과 핀치 바텀 유형은 금속 감지 및 직립형 소매 디스플레이가 요구되는 식품 및 종자 용도에서 틈새 시장을 충족시킵니다. 아시아태평양에서는 임금 상승으로 자동화와의 비용 차이가 줄어들면서 FFS에 대한 투자가 증가하고 있습니다. 한편, 북미에서는 창고 관리 소프트웨어와 연동되는 RFID 내장형 FFS 봉투가 주도적인 역할을 하고 있습니다. 전반적으로, 고속 자동 포장 공장으로의 지속적인 전환은 모든 포장 유형에서 색 크라프트지 시장의 지속적인 수요를 뒷받침하고 있습니다.

2세대 FFS 설계는 현재 인라인 RFID 태그 삽입, 가변 데이터 인쇄, 팔레타이징 로봇을 통합하고 있습니다. 컨버터 업체들은 99% 이상의 재고 정확도를 약속하는 턴키 라인을 판매하고 있으며, 이러한 가치 제안은 초기 투자 이상의 이점을 제공합니다. 한편, 유럽의 제지업체들은 재생 크라프트 기판에 요구되는 초음파 밀봉에 대응할 수 있도록 종이의 형성을 조정하고 있습니다. 먼지가 많은 시멘트 환경에서는 밸브가 달린 백이 주류를 이루고 있지만, FFS 시스템은 충전 시 위생적인 장점으로 인해 비료, 반려동물사료, 안료 제조 시설에도 보급되고 있습니다. 따라서 경쟁의 초점은 재료 사양과 기계 호환성에 초점을 맞추고 있으며, 이로 인해 포장 형태가 가방용 크래프트 종이 시장의 결정적인 성장 요인으로 자리 잡고 있습니다.

2025년 기준, 코팅 크라프트와 배리어 크라프트는 색 크라프트지 시장의 37.21%를 차지하며 4.69%의 가장 높은 CAGR을 기록했습니다. 이는 고객이 플라스틱 안감 봉투에서 방습 및 방산 기능을 갖춘 완전 재활용 가능한 종이로 전환하는 것을 반영합니다. 바이오 베이스 코팅은 수증기 투과율을 10 g/m2/24 h 이하로 낮추는데 성공하여 재활용성을 손상시키지 않고 커피, 밀가루, 설탕 등의 벌크 제품에 적용이 가능합니다. 표준 크라프트지는 인장 강도와 인쇄 적성이 장벽 성능을 능가하기 때문에 여전히 시멘트 및 광물 제품의 주력으로 사용되고 있지만, 그 성장은 비교적 완만합니다. 반신축성 및 신축성 등급은 연마제 및 각진 비료용으로 사용되며, 6-8%의 파단 신율로 취급 시 파열을 방지합니다. 나노섬유 프리코팅과 인라인 분산 장벽을 통해 더 얇은 두께의 제품도 50kg 낙하 테스트를 통과할 수 있어 탄소 평가 프로토콜에서 요구하는 경량화 목표를 달성할 수 있도록 지원합니다.

원스텝 배리어 코팅 라인에 투자하면 오프라인 라미네이팅 대비 최대 18%까지 가공 비용을 절감할 수 있으며, 중규모 사용자도 합리적인 가격으로 고성능 제품을 사용할 수 있습니다. 유럽의 커피 로스팅 업체와 아시아의 향신료 거래업체들은 PFAS 화학물질을 피하기 위해 점점 더 많은 광물성 산소 차단제를 지정하고 있습니다. 크레이프 가공 및 습윤 강도 크라프트 지와 같은 특수 하위 등급은 완충재 및 실외 보관의 요구 사항을 충족하고 다양한 제품 라인업을 강화합니다. 이러한 다양한 제품군을 통해 각 성능 수준은 안정적인 고객 기반을 확보할 수 있으며, 색 크라프트지 시장에서 등급 수준의 깊이를 강화할 수 있습니다.

지역별 분석

아시아태평양은 중국의 시멘트 소비와 인도의 농업용 포장 수요에 힘입어 2025년 세계 매출의 32.54%를 차지했습니다. 그러나 인프라 투자 둔화와 플라스틱 금지 조치의 시행 상황의 편차로 인해 단기적인 성장은 억제되고 있습니다. 인건비 상승으로 인해 가공업체들은 FFS(충전 및 밀봉 포장) 자동화를 추진하고 있으며, 고성능 신축성 등급에 대한 수요가 증가하고 있습니다. 베트남과 인도네시아의 생산능력 증설은 동남아시아의 성장 지역에 대응하고 중국의 수입 규제에 대한 헤지를 위한 제지업체들의 전략을 반영한 것입니다. 그러나 환율 변동과 수입 펄프에 대한 의존도로 인해 비용 구조는 여전히 취약한 상태입니다.

아프리카는 CAGR 4.77%로 가장 빠르게 성장하는 지역으로, 2024년 20억 달러에서 2032년 35억 달러로 확대될 나이지리아의 포장 시장이 주도하고 있습니다. 나이지리아와 남아공의 플라스틱 금지 조치와 더불어 연간 20%의 EC 성장률로 인해 시멘트 봉투와 우편용 봉투에 대한 수요가 발생하고 있습니다. 지역 내 제지공장의 40% 이하만이 재생에너지를 이용하고 있어 공급 제약이 지속되고 있으며, FSC 인증 및 EU 시장 접근이 제한되고 있습니다. 아프리카 대륙자유무역지대(AfCFTA)는 역내 운송을 원활하게 하고, 현지 가공 투자 및 지역특화를 촉진하고 있습니다.

유럽과 북미는 인프라 개보수 및 지속가능성 관련 규제에 힘입어 성숙하고 안정적인 수요를 차지하고 있습니다. 2026년부터 시행되는 탄소국경조정관세는 국내 저배출 종이를 장려하고 석탄화력발전소로부터의 수입에 페널티를 부과하는 제도입니다. 남미의 전망은 농업 수출과 밀접한 관련이 있습니다. 브라질의 펄프 생산 확대로 지역 섬유 공급이 증가하는 한편, 안데스 지역의 건설 프로젝트에서 정부가 플라스틱을 단계적으로 폐지함에 따라 종이 봉지 사용이 증가하고 있습니다. 이러한 지역별 미묘한 차이가 결합되어 기회와 위험의 모자이크 패턴이 만들어져 전 세계 봉지용 크라프트지 시장의 확장을 뒷받침하고 있습니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측, 금액

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The sack kraft paper market size was valued at USD 12.48 billion in 2025 and estimated to grow from USD 13.01 billion in 2026 to reach USD 15.68 billion by 2031, at a CAGR of 3.81% during 2026-2031.

The steady headline figure hides a structural transformation as plastic-ban legislation, carbon border adjustment mechanisms and digitized supply chains accelerate substitution of woven polypropylene bulk bags with recyclable multiwall paper sacks across cement, food ingredients and minerals handling. Integrated producers are upgrading mills with barrier coating and RFID-ready converting lines to secure premium contracts, while converters race to install form-fill-seal (FFS) equipment that doubles bagging speeds and cuts labor outlays by one-third. Raw-material volatility in virgin pulp and old corrugated containers continues to squeeze margins, but vertical integration and long-term fiber contracts are mitigating price swings. Lightweight single-ply extensible papers, supported by the need to curb freight emissions, are becoming the format of choice for 25-50 kilogram cement and fertilizer applications. Automation-ready, curbside-recyclable designs underpin future demand, positioning the sack kraft paper market as a strategic beneficiary of circular-economy policies worldwide.

Global Sack Kraft Paper Market Trends and Insights

Plastic-Ban Legislation Accelerating Paper Substitution

Single-use plastic prohibitions are compressing the replacement cycle for woven polypropylene across bulk packaging. Legislative momentum against single-use plastics is compressing the substitution timeline for woven polypropylene sacks across bulk packaging applications. The European Union's Packaging and Packaging Waste Regulation, finalized in 2024, mandates that 65% of packaging materials be recyclable by 2030 and bans oxo-degradable plastics outright, forcing cement and fertilizer distributors to transition to multiwall kraft sacks that qualify for municipal paper recycling streams. In the United Kingdom, the Extended Producer Responsibility scheme imposed a GBP 200 per tonne levy on non-recyclable packaging in 2025, raising the landed cost of polypropylene FIBCs by 18-22% and tilting procurement toward paper alternatives that avoid the surcharge. This driver exerts the largest positive swing on the sack kraft paper market because compliance is mandatory and immediate.

Cement-Sector Decarbonization Favoring Recyclable Sacks

Global cement producers are embedding Scope 3 packaging emissions into net-zero roadmaps. A 2025 life-cycle assessment verified that kraft sacks deliver 60% lower CO2 than polypropylene equivalents when end-of-life recycling is counted. Flagship projects include Mondi and Cemex's SolmixBag, a dissolvable single-ply kraft sack already commercial in Spain, and UltraTech Cement's pledge to shift 30% of its Indian retail portfolio to recycled kraft by 2027. European circular-construction pilots are trialing deposit-return schemes for reusable kraft sacks, rewarding contractors for recovering empty bags. Because cement represented more than two-fifths of 2025 demand, decarbonization choices by this sector meaningfully recalibrate the sack kraft paper market trajectory over the medium term.

Penetration of Woven-PP FIBCs in Bulk Packaging

Conductive and antistatic flexible intermediate bulk containers fill safety and reusability needs that kraft cannot match in chemicals and flammable powders. Type C FIBCs cost USD 8-12 each against USD 15-20 for equivalent multiwall kraft with antistatic liners, a gap widened by their ability to complete 5-10 shipping cycles. Closed-loop supply chains in plastics resins, mineral concentrates and automotive parts therefore continue to specify polypropylene, placing a -0.6% drag on the sack kraft paper market.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce Adoption of Curbside-Recyclable Heavy-Duty Mailers

- Food-Grade Bulk Ingredients Shifting to Certified Paper Sacks

- Volatile Virgin-Fiber and OCC Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Form-fill-seal sacks accounted for a meaningful proportion of the sack kraft paper market size and post a 4.78% CAGR because automated lines fill up to 1,800 units per hour, twice the speed of valve systems. Cement and chemical producers adopt FFS to cut stitching labor by 30-40% and boost bagging accuracy, while FFS-ready papers with controlled coefficient of friction maintain seal integrity. Valve sacks, holding 41.32% share in 2025, remain indispensable where dust control and legacy pneumatic filling dominate. Open-mouth and pinch-bottom formats fill niches in food and seed applications that require metal detection or upright retail display. Asia-Pacific drives FFS investments as rising wages narrow the cost gap versus automation, and North America leads on RFID-embedded FFS sacks that integrate with warehouse management software. Overall, the continuous shift toward high-speed automated packaging plants underpins sustained demand across all packaging types within the sack kraft paper market.

Second-generation FFS designs now integrate inline RFID tag insertion, variable data printing and palletizing robotics. Converters market turnkey lines that promise inventory accuracy above 99%, a value proposition that outweighs the upfront capital. Meanwhile, European mills calibrate paper formation to accommodate ultrasonic sealing demanded by recycled kraft substrates. Although valve sacks dominate in dusty cement environments, FFS systems are infiltrating fertilizer, pet food and pigment facilities due to superior filling hygiene. The competitive battle therefore centers on material specifications and machine compatibility, cementing packaging type as a decisive growth vector for the sack kraft paper market.

Coated and barrier kraft held 37.21% of sack kraft paper market share in 2025 and post the fastest 4.69% CAGR, reflecting customer migration from plastic-lined sacks to fully recyclable papers with moisture and oxygen barriers. Bio-based coatings achieve water-vapor transmission below 10 g/m2/24 h, opening applications in bulk coffee, flour and sugar without compromising recyclability. Standard kraft remains the workhorse for cement and minerals because tensile strength and printability trump barrier performance, though its growth is more subdued. Semi-extensible and extensible grades serve abrasives and jagged fertilizers, with 6-8% elongation at break preventing rupture during handling. Nanofiber pre-coatings and inline dispersion barriers now enable thinner gauges to pass 50-kilogram drop tests, supporting lightweighting targets mandated by carbon assessment protocols.

Investment in single-step barrier coating lines lowers conversion costs by up to 18% versus offline lamination, bringing premium performance within reach of mid-volume users. European coffee roasters and Asian spice traders increasingly specify mineral-based oxygen barriers that avoid PFAS chemistry. Specialty sub-grades such as creped or wet-strength kraft fill cushioning and outdoor storage requirements, rounding out a diverse product spectrum. This breadth ensures that each performance tier finds a stable customer base, reinforcing grade-level depth in the sack kraft paper market.

The Sack Kraft Paper Market Report is Segmented by Packaging Type (Valve Sacks, Open Mouth Sacks, Pinch-Bottom Sacks, Form-Fill-Seal Sacks, and More), Grade (Kraft, Semi-Extensible, Extensible, Coated/Barrier Kraft, and More), Ply/Layer Count (1-Ply, 2-Ply, and More), End-User Industry (Building Materials and Cement, Food and Beverage, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific anchored 32.54% of 2025 global revenue behind China's cement consumption and India's agricultural packaging needs. Yet infrastructure moderation and patchy plastic-ban enforcement temper near-term growth. Rising labor costs push converters toward FFS automation, boosting demand for high-performance extensible grades. Capacity additions in Vietnam and Indonesia reflect mill owners' strategy to serve Southeast Asian growth corridors and hedge against Chinese import restrictions. Currency volatility and imported pulp dependence, however, keep cost structures exposed.

Africa is the fastest-growing region at a 4.77% CAGR, propelled by Nigeria's packaging market, which rises from USD 2 billion in 2024 to USD 3.5 billion by 2032. Plastic bans in Nigeria and South Africa, paired with 20% annual e-commerce growth, create demand for cement sacks and mailers. Supply constraints persist because fewer than 40% of regional mills run on renewable energy, limiting FSC certification and EU market access. The African Continental Free Trade Area eases intra-regional shipments, encouraging localized converting investments and regional specialization.

Europe and North America account for mature but stable demand shaped by infrastructure refurbishment and sustainability regulations. Carbon border adjustment tariffs effective in 2026 incentivize domestic low-emission paper and penalize imports from coal-fired mills. South America's outlook is tied to agricultural exports; Brazilian pulp expansions add regional fiber availability, while Andean construction projects use more paper sacks as governments phase out plastic. Collectively, these geographic nuances create a mosaic of opportunities and risks, sustaining global expansion for the sack kraft paper market.

- Mondi plc

- Smurfit Kappa Group plc

- WestRock Company

- Billerud AB

- International Paper Company

- Segezha Group PJSC

- Stora Enso Oyj

- Gascogne Groupe SA

- Nordic Paper AS

- Natron-Hayat d.o.o.

- Horizon Pulp and Paper Ltd.

- Canfor Corporation

- Klabin S.A.

- SCG Packaging Public Company Limited

- Oji Holdings Corporation

- Nine Dragons Paper Holdings Ltd.

- Sappi Limited

- Heinzel Holding GmbH

- Georgia-Pacific LLC

- Rengo Co., Ltd.

- Daio Paper Corporation

- Ahlstrom Oyj

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value / Supply-Chain Analysis

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Market Drivers

- 4.5.1 Plastic-ban Legislation Accelerating Paper Substitution

- 4.5.2 Cement-sector Decarbonization Favoring Recyclable Sacks

- 4.5.3 E-commerce Adoption of Curbside-recyclable Heavy-duty Mailers

- 4.5.4 Food-grade Bulk Ingredients Shifting to Certified Paper Sacks

- 4.5.5 Radio-frequency-identifiable Sack Papers Simplifying Warehouse Automation

- 4.5.6 Carbon Border Adjustment Mechanisms Boosting EU Demand for Low-Emission Sack Papers

- 4.6 Market Restraints

- 4.6.1 Penetration of Woven-PP FIBCs in Bulk Packaging

- 4.6.2 Volatile Virgin-fiber and OCC Prices

- 4.6.3 Emergence of Soluble Fiber-based Bulk Packaging Films Eroding Niche Applications

- 4.6.4 Regional Shortfall of Renewable Energy Access Limiting Mill Green Certifications

- 4.7 Regulatory Landscape

- 4.8 Technological Outlook

5 MARKET SIZE AND GROWTH FORECASTS, VALUE

- 5.1 By Packaging Type

- 5.1.1 Valve Sacks

- 5.1.2 Open Mouth Sacks

- 5.1.3 Pinch-Bottom Sacks

- 5.1.4 Form-Fill-Seal Sacks

- 5.1.5 Rest of Packaging Type

- 5.2 By Grade

- 5.2.1 Kraft

- 5.2.2 Semi-Extensible

- 5.2.3 Extensible

- 5.2.4 Coated / Barrier Kraft

- 5.2.5 Rest of Grade

- 5.3 By Ply / Layer Count

- 5.3.1 1-Ply

- 5.3.2 2-Ply

- 5.3.3 3-Ply

- 5.3.4 More than 3-Ply

- 5.4 By End-User Industry

- 5.4.1 Building Materials and Cement

- 5.4.2 Food and Beverage Ingredients

- 5.4.3 Chemicals and Fertilizers

- 5.4.4 Agriculture and Animal Feed

- 5.4.5 Minerals and Pigments

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Mondi plc

- 6.4.2 Smurfit Kappa Group plc

- 6.4.3 WestRock Company

- 6.4.4 Billerud AB

- 6.4.5 International Paper Company

- 6.4.6 Segezha Group PJSC

- 6.4.7 Stora Enso Oyj

- 6.4.8 Gascogne Groupe SA

- 6.4.9 Nordic Paper AS

- 6.4.10 Natron-Hayat d.o.o.

- 6.4.11 Horizon Pulp and Paper Ltd.

- 6.4.12 Canfor Corporation

- 6.4.13 Klabin S.A.

- 6.4.14 SCG Packaging Public Company Limited

- 6.4.15 Oji Holdings Corporation

- 6.4.16 Nine Dragons Paper Holdings Ltd.

- 6.4.17 Sappi Limited

- 6.4.18 Heinzel Holding GmbH

- 6.4.19 Georgia-Pacific LLC

- 6.4.20 Rengo Co., Ltd.

- 6.4.21 Daio Paper Corporation

- 6.4.22 Ahlstrom Oyj

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment