|

시장보고서

상품코드

2044179

다층 세라믹 커패시터(MLCC) 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Multilayer Ceramic Capacitor (MLCC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

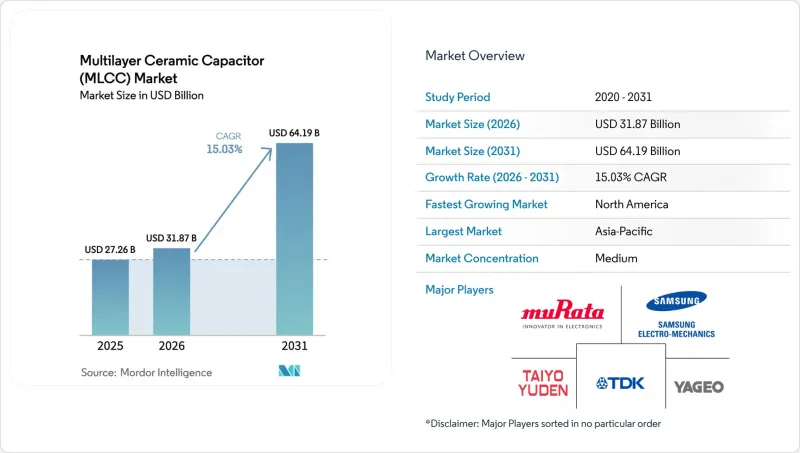

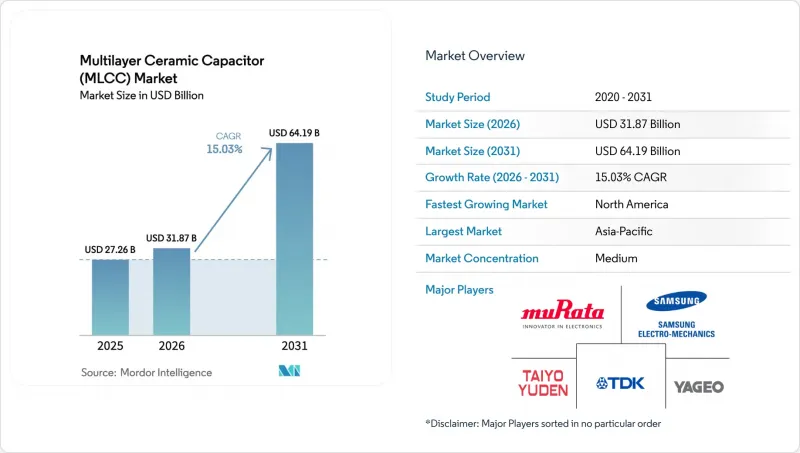

다층 세라믹 커패시터(MLCC) 시장 규모는 2025년 272억 6,000만 달러, 2026년 318억 7,000만 달러에서 2031년까지 641억 9,000만 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 CAGR 15.03%를 기록할 전망입니다.

이러한 성장 궤적은 자동차 전동화, 인공지능(AI) 인프라, 엣지 컴퓨팅이 융합되면서 수동 부품에 대한 수요가 급증하고 기존 공급망에 지속적인 압력이 가해지고 있음을 반영합니다. 클래스 1 온도 안정성 유전체는 안전성이 매우 중요한 설계에서 지속적으로 선호되고 있으며, 0402 패키지는 절대적인 실장 면적 감소보다 초저 등가 직렬 인덕턴스를 중시하는 고성능 서버에서 선호되는 폼팩터로 자리 잡고 있습니다. 지역적으로 분산된 프렌드쇼어링을 통해 인도와 동남아시아에서 생산 능력이 확대되고 있지만, AEC-Q200 부품의 긴 인증 주기로 인해 단기적인 공급은 여전히 부족합니다. 특히 니켈 및 팔라듐 가격 변동으로 적층 세라믹 커패시터 시장 전체에서 비용 리스크가 높아지는 가운데, 티타네이트 바륨 분말과 니켈 전극의 야금 기술을 장악하고 있는 수직계열화 된 주요 업체들이 경쟁 우위를 점하고 있습니다.

세계 적층 세라믹 커패시터(MLCC) 시장 동향과 인사이트

800V EV 아키텍처로 고전압 MLCC 수요 가속화

800V 배터리 플랫폼으로 전환하는 자동차 제조업체들은 1,000V 이상의 동작 마진을 견딜 수 있는 MLCC를 필요로 하고 있으며, 이에 따라 공급업체들은 니켈-팔라듐 전극의 두께를 늘리고, 서브마이크론 수준의 유전체 증착 기술을 고도화하고 있습니다. 삼성 전기기계는 2025년 실리콘 카바이드 인버터용 2,000V의 X7R 시리즈를 출시했습니다. 한편, 무라타의 GCM32 시리즈는 1,000V의 정격과 노이즈 억제를 위한 100nH의 등가 직렬 인덕턴스(등가 직렬 인덕턴스)를 결합하고 있습니다. IDTechEx는 2028년까지 800V 차량이 전체 생산량의 40%를 차지할 것으로 예상하고 있으며, 이로 인해 차량 1대당 MLCC 탑재량은 약 4분의 1로 증가할 것으로 예상하고 있습니다. 자동차 등급의 수명 테스트는 여전히 150℃에서 1,000시간에 달하는 등 인증과 관련된 병목현상은 해소되지 않았지만, 이를 극복한 공급업체는 다층 세라믹 커패시터(MLCC) 시장에서 프리미엄 가격으로 판매할 수 있게 되었습니다.

생성형 AI 서버의 확대로 초저ESL, 고CV MLCC 채택 촉진

소켓당 700W를 소비하는 추론 가속기는 전압 과도 현상을 유발하며, 다이에서 2mm 이내의 위치에 0402 사이즈의 MLCC를 배치해야 합니다. 무라타제작소는 2025년 7월, 두께가 0.6µm에 불과한 800층 적층 구조의 47µ&F 4V 0402 디바이스를 출하하기 시작했습니다. 교세라 AVX는 저ESL 서버용 제품군의 생산 능력을 두 배로 늘렸습니다. 이는 각 GPU 보드에 최대 3,000개의 커패시터가 탑재되어 CPU 시스템보다 훨씬 더 많은 커패시터를 탑재할 수 있기 때문입니다. TrendForce의 보고서에 따르면, 2025년 서버용 MLCC 출하량은 35% 증가하여 서버 출하량 증가율을 크게 상회할 것으로 예측됩니다. 따라서 활성층이 600층을 넘으면 불량률이 높아지기 때문에 일본 정밀부품 업체들은 타사와의 격차를 더욱 벌리고 있습니다.

니켈과 팔라듐의 가격 변동으로 BOM 비용 상승 전망

니켈 가격은 인도네시아의 수출 규제로 2024년 초 42% 급등한 후 2025년 말까지 18% 하락했습니다. 한편, 팔라듐 가격은 러시아공급 불안을 배경으로 트로이온스당 900달러에서 1,400달러 사이를 오갔습니다. 전극 금속 비용이 10% 상승하면 MLCC 완제품 비용은 3-5% 상승하여 이미 연간 가격 하락률이 8%에 육박하는 민생 분야 공급업체를 압박할 것입니다. TDK는 원자재 가격 상승으로 인해 2026년 수동 부품 마진이 120bp 감소하고, 구리 전극의 대체가 가속화되고 있다고 밝혔습니다. 무라타제작소는 니켈 선물 가격에 연동된 분기별 가격 조항을 재협상하여 데이터센터 고객에게 일부 리스크를 전가하고 있습니다. 헤지 프로그램이 없는 중소 아시아계 공급업체들은 2025년 하반기 자동차 생산량을 줄여 공급 부족을 심화시켰습니다.

부문 분석

2025년, 클래스 1 디바이스는 적층 세라믹 커패시터(MLCC) 시장 점유율의 62.69%를 차지할 것으로 예상되며, 이는 자동차 제조업체들이 차량 수명 15년 동안 드리프트 없는 성능에 대한 요구를 반영하고 있습니다. 이 부문은 광대역 갭 인버터와 의료용 전자기기가 제로 온도 계수 세라믹으로 전환함에 따라 전체 다층 세라믹 커패시터 시장보다 빠른 CAGR 15.83%를 나타낼 것으로 예측됩니다. 무라타의 1,250V C0G 시리즈는 ppm 이하의 온도 드리프트를 유지하면서 전기이동에 대응하는 두꺼운 전극으로의 전환을 상징합니다. 반면, Class 2 바륨 티타네이트 부품은 높은 체적 효율이 노화에 따른 용량 손실을 상쇄하기 때문에 여전히 스마트폰 시장을 독점하고 있지만, 안전성이 매우 중요한 설계 분야에서는 점유율을 잃어가고 있습니다.

기판상의 실장 면적과 안정성의 트레이드 오프는 여전히 중요한 과제입니다. 클래스 1 커패시터는 클래스 2 커패시터에 비해 설치 면적이 최대 5배 더 크지만, 예측 가능한 정전 용량으로 인해 비용이 많이 드는 설계 마진을 제거할 수 있기 때문에 ISO 26262를 준수하는 파워트레인 제어 장치에서 중요한 역할을 합니다. 규제 당국은 유전체 선택을 명시적으로 요구하지는 않지만, AEC-Q200의 수명 테스트는 암묵적으로 설계를 클래스 1 배합으로 유도하고 있습니다. 그 결과, MLCC 시장은 양극화 현상이 지속되고 있습니다. 고부가가치 자동차 및 산업용 분야에서는 클래스 1의 안정성이 중요시되는 반면, 민수용 전자기기에서는 클래스 2의 고밀도화가 유지되고 있습니다.

2025년, 다층 세라믹 커패시터(MLCC)는 1,0201 사이즈가 시장의 56.48%를 차지했습니다. 이는 1mm 미만의 소형 부품을 요구하는 스마트폰 및 웨어러블 기기가 견인한 것입니다. 그러나 0402 사이즈의 제품은 연간 16.02%의 속도로 증가하고 있으며, 이는 700W GPU에 인접한 47µF의 디커플링 커패시터를 필요로 하는 AI 서버에 의해 뒷받침되고 있습니다. 무라타제작소는 2025년 7월, 800층 0402 사이즈 부품을 출시하여 이전 세대 대비 정전 용량 밀도를 2배로 높였습니다. 교세라 AVX는 이에 이어 스마트 워치 모듈용 10µ&F 0402 시리즈를 발표했습니다.

0402 사이즈 이하의 제조는 복잡성이 급격히 증가하여 포토리소그래피급 클린룸과 레이저 트림 가공이 필요합니다. 이에 따라 생산능력은 일본과 한국의 주요 3사에 집중되어 2026년 초에는 리드타임이 20주까지 늘어날 것으로 예상되며, 중국 업체들은 범용화된 0603 및 0805 사이즈의 제품으로 경쟁을 벌이고 있습니다. GPU 보드당 3,000개의 MLCC가 탑재됨에 따라 0402 사이즈 부품공급 부족이 지속될 것으로 예상되며, 이는 다층 세라믹 커패시터 시장 전체에서 높은 가격을 유지하는 요인이 될 것으로 보입니다.

지역별 분석

2025년 아시아태평양은 다층 세라믹 커패시터 매출의 57.69%를 차지했습니다. 이는 일본의 정밀 세라믹 기술, 한국의 다품종 생산체제, 그리고 중국의 거대한 가전제품 수출기반을 반영한 것입니다. 중국 공장은 전 세계 MLCC 생산량의 최대 75%를 공급했지만, 지정학적 긴장으로 인해 OEM 업체들은 일본, 한국, 인도의 거점을 통해 듀얼 소싱을 진행하게 되었습니다. 무라타제작소, TDK, 솔라유덴은 모두 2026년 초에 풀가동할 예정이며, 필리핀과 인도에서 생산능력을 확대하여 프렌드쇼어링의 요청에 부응하고 있습니다. 마찬가지로 풀가동 상태인 삼성전기는 BYD의 800V 차량용 부품 공급과 함께 필리핀 생산기지를 강화했습니다.

북미 시장은 2031년까지 연평균 16.07%씩 성장하고 있으며, 반도체 및 수동 부품 공급을 국내로 회귀시키는 'CHIPS and Science Act'의 인센티브에 힘입어 성장하고 있습니다. 마이크로소프트와 아마존과 같은 하이퍼스케일러는 AI 가속기용 초저 ESL 디커플링 부품을 요구하며 2025년 서버용 MLCC 주문량을 두 배로 늘렸습니다. 미국에서 계획된 팹은 인건비 및 AEC-Q200 인증 주기의 장기화로 인해 여전히 지연되고 있어, USMCA의 무역 조건에 따라 멕시코의 거점이 잉여분 조립을 담당하고 있습니다. 캐나다의 점유율은 작지만, 중요 광물 정책이 국내 니켈 및 팔라듐 공급을 촉진하고 있기 때문에 확대될 가능성이 있습니다.

유럽은 2025년에도 15% 중반의 점유율을 유지할 것으로 예상되며, 이는 독일의 자동차 산업 회랑과 북유럽의 재생에너지 프로젝트가 뒷받침하고 있습니다. 유럽연합(EU)의 '칩법'은 현지 생산을 장려하고 있지만, 엄격한 RoHS 및 REACH 표준으로 인해 인증 절차가 길어지고 아시아에 비해 비용이 최대 15%까지 상승하고 있습니다. Wurth Elektronik은 자동차 등급 생산을 확대하고 있지만, 여전히 일본에서 서브마이크론급 유전체 분말을 수입하고 있습니다. 기타 지역에서는 남미, 중동/아프리카가 한 자릿수 초반의 점유율을 차지하고 있으며, 브라질의 전기차 보급과 저인덕턴스 MLCC를 중시하는 걸프 지역 국가들의 데이터센터 건설에 집중되어 성장하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.11The multilayer ceramic capacitor (MLCC) market size is projected to expand from USD 27.26 billion in 2025 and USD 31.87 billion in 2026 to USD 64.19 billion by 2031, registering a 15.03% CAGR between 2026 and 2031. The growth trajectory reflects surging demand for passive components as vehicle electrification, artificial-intelligence infrastructure, and edge computing converge, placing sustained pressure on legacy supply chains. Class 1 temperature-stable dielectrics continue to gain traction in safety-critical designs, while 0402 packages are becoming the preferred form factor for high-performance servers that prize ultra-low equivalent series inductance over absolute footprint savings. Geo-diversified friend-shoring is unlocking incremental capacity in India and Southeast Asia, yet long qualification cycles for AEC-Q200 parts keep near-term supply tight. Competitive dynamics favor vertically integrated leaders that control barium-titanate powders and nickel electrode metallurgy, especially as volatility in nickel and palladium prices raises cost risk across the multilayer ceramic capacitor market.

Global Multilayer Ceramic Capacitor (MLCC) Market Trends and Insights

800 V EV Architectures Accelerate Demand for High-Voltage MLCCs

Automakers shifting to 800 V battery platforms need MLCCs that withstand >=1,000 V operating margins, prompting suppliers to thicken nickel-palladium electrodes and refine sub-micrometer dielectric deposition. Samsung Electro-Mechanics released a 2,000 V X7R family in 2025 for silicon-carbide inverters, while Murata's GCM32 series pairs 1,000 V ratings with 100 nH equivalent series inductance for noise suppression. IDTechEx expects 800 V vehicles to represent 40% of production by 2028, lifting MLCC content per car by roughly one-quarter. Qualification bottlenecks persist because automotive-grade life testing still spans 1,000 hours at 150 °C, yet suppliers mastering these hurdles enjoy premium pricing in the multilayer ceramic capacitor (MLCC) market.

Gen-AI Server Build-Out Spurs Ultra-Low-ESL, High-CV MLCC Adoption

Inference accelerators drawing 700 W per socket create voltage transients that demand 0402 MLCCs positioned within 2 mm of the die. Murata began shipping a 47 µF 4 V 0402 device in July 2025 that stacks 800 layers only 0.6 µm thick. KYOCERA AVX doubled capacity for its low-ESL server portfolio because each GPU board now carries up to 3,000 capacitors, far above CPU systems. TrendForce reported 35% MLCC unit growth in servers during 2025, well ahead of server shipment growth. Japanese precision houses therefore widen their lead as defect rates climb when active layers exceed 600.

Volatile Nickel and Palladium Prices Inflate BOM Costs

Nickel spiked 42% in early 2024 after Indonesian export curbs, then swung 18% lower by late 2025, while palladium fluctuated between USD 900 and USD 1,400 per troy ounce amid Russian supply uncertainty. A 10% rise in electrode-metal cost lifts finished MLCC bills by 3-5%, squeezing suppliers in consumer tiers where annual price erosion already approaches 8%. TDK said raw-material inflation trimmed its passive-component margin by 120 bps in fiscal 2026, accelerating copper electrode substitution. Murata is renegotiating quarterly price clauses tied to nickel futures, passing some risk to data-center clients. Smaller Asian suppliers without hedging programs cut automotive output in late 2025, deepening shortage conditions.

Other drivers and restraints analyzed in the detailed report include:

- On-Device AI and Advanced Wearables Require Sub-1005 Miniature MLCCs

- Geo-Diversified Friend-Shoring of Passive-Component Supply Chains

- Persistent Capacity Mismatch for Automotive-Grade MLCCs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Class 1 devices accounted for 62.69% multilayer ceramic capacitor (MLCC) market share in 2025, reflecting automakers' need for drift-free performance over 15-year vehicle lifespans. The segment is set to grow at a 15.83% CAGR, faster than the broader multilayer ceramic capacitor market size, as wide-bandgap inverters and medical electronics migrate to zero-temp-coefficient ceramics. Murata's 1,250 V C0G series exemplifies the shift toward thicker electrodes that combat electromigration while maintaining sub-ppm temperature tracking. In contrast, Class 2 barium-titanate parts still dominate smartphones because their higher volumetric efficiency offsets aging losses, yet they lose share in safety-critical designs.

The trade-off between board real estate and stability remains central. Class 1 capacitors occupy up to five times the footprint of Class 2 equivalents, yet predictable capacitance eliminates costly design margins, which matters in ISO 26262-compliant powertrain control units. Regulatory bodies do not explicitly mandate dielectric selection, but AEC-Q200 life testing implicitly steers designs toward Class 1 formulations. Consequently, the MLCC market continues to bifurcate: high-value automotive and industrial nodes lean on Class 1 stability, while consumer electronics retain Class 2 density.

The 0201 footprint captured 56.48% of the multilayer ceramic capacitor (MLCC) market in 2025, driven by smartphones and wearables chasing sub-millimetre components. Yet 0402 units are rising 16.02% annually, supported by AI servers that need 47 µF decoupling capacitors contiguous to 700 W GPUs. Murata's July 2025 release of an 800-layer 0402 part doubled capacitance density over its previous generation. KYOCERA AVX followed with a 10 µF 0402 range for smart-watch modules.

Manufacturing complexity scales sharply below 0402, requiring photolithography-grade clean rooms and laser trim. This concentrates capacity among three Japanese and Korean leaders, extending lead times to 20 weeks in early 2026, while Chinese entrants compete in commoditised 0603 and 0805 lines. As GPU boards swell to 3,000 MLCCs each, supply tightness in 0402 parts is likely to persist, underpinning premium price realisation across the multilayer ceramic capacitor market.

The Multilayer Ceramic Capacitor (MLCC) Market Report is Segmented by Dielectric Type (Class 1, and Class 2), Case Size (0 201, 0 402, 0 603, 1 005, 1 210, and More), Voltage Rating (Low-Range Voltage, Mid-Range Voltage, and More), Mounting Type (Surface-Mount, Metal-Cap, and Radial-Lead), End User (Automotive, Consumer Electronics, Industrial, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 57.69% of multilayer ceramic capacitor revenue in 2025, reflecting Japan's mastery of precision ceramics, South Korea's high-mix production, and China's vast consumer-electronics export engine. Chinese factories supplied up to 75% of global MLCC output, yet geopolitical tension spurred OEMs to dual-source through Japanese, Korean, and Indian sites. Murata, TDK, and Taiyo Yuden all ran full utilisation in early 2026 and expanded capacity in the Philippines and India to satisfy friend-shoring mandates. Samsung Electro-Mechanics, likewise running at capacity, channelled parts to BYD's 800 V vehicles while fortifying its Philippine campus.

North America is growing at 16.07% through 2031, buoyed by CHIPS and Science Act incentives that pull semiconductor and passive-component supply back onshore. Hyperscalers such as Microsoft and Amazon doubled server-grade MLCC orders during 2025, chasing ultra-low-ESL decoupling for AI accelerators. Proposed U.S. fabs remain delayed by labour cost and lengthy AEC-Q200 qualification cycles, so Mexican sites pick up overflow assembly under USMCA trade terms. Canada's piece is small but may rise as critical-mineral policies support domestic nickel and palladium supply.

Europe held a mid-teens share in 2025, tied to Germany's automotive corridor and Nordic renewable-energy projects. The European Union Chips Act encourages localisation, though strict RoHS and REACH standards extend qualification and inflate costs by up to 15% versus Asia. Wurth Elektronik is scaling automotive-grade output, yet still imports sub-micron dielectric powders from Japan. Elsewhere, South America, the Middle East, and Africa represent a low-single-digit slice, with growth centring on Brazil's electric-vehicle rollout and Gulf data-center builds that value low-inductance MLCCs.

List of Companies Covered in this Report:

- Murata Manufacturing Co., Ltd.

- Samsung Electro-Mechanics Co., Ltd.

- Taiyo Yuden Co., Ltd.

- Yageo Corporation

- TDK Corporation

- Kyocera AVX Components Corporation

- Walsin Technology Corporation

- Vishay Intertechnology, Inc.

- Wurth Elektronik GmbH and Co. KG

- Guangdong Fenghua Advanced Technology Holding Co., Ltd.

- Maruwa Co., Ltd.

- Samwha Capacitor Group

- Panasonic Holdings Corporation

- Shenzhen Torch Technology Co., Ltd.

- Holy Stone Enterprise Co., Ltd.

- Shenzhen Eyang Technology Development Co., Ltd.

- Johanson Dielectrics, Inc.

- KEMET Corporation (Yageo Group)

- Shenzhen Sunlord Electronics Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 800 V EV Architectures Accelerate Demand for High-Voltage MLCCs

- 4.2.2 Gen-AI Server Build-Out Spurs Ultra-Low-ESL, High-CV MLCC Adoption

- 4.2.3 On-Device AI and Advanced Wearables Require Sub-1 005 Miniature MLCCs

- 4.2.4 Geo-Diversified "Friend-Shoring" of Passive Component Supply Chains

- 4.2.5 Sustainability Mandates Favor Lead-Free and Recycled-Ceramic MLCCs

- 4.2.6 Semiconductor-Subsystem Co-Design Embeds MLCCs inside Chiplets

- 4.3 Market Restraints

- 4.3.1 Volatile Nickel and Palladium Prices Inflate BOM Costs

- 4.3.2 Persistent Capacity Mismatch for Automotive-Grade MLCCs

- 4.3.3 China Price-Led Offensive in Commodity MLCCs Erodes Global Margins

- 4.3.4 Physical Limits on Dielectric Layer Thickness (Less than 1 µm) Stall Capacitance Gains

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Supply-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Dielectric Type

- 5.1.1 Class 1

- 5.1.2 Class 2

- 5.2 By Case Size

- 5.2.1 0 201

- 5.2.2 0 402

- 5.2.3 0 603

- 5.2.4 1 005

- 5.2.5 1 210

- 5.2.6 Other Case Sizes

- 5.3 By Voltage Rating

- 5.3.1 Low Voltage (Less than 500 V)

- 5.3.2 Mid Voltage (500 - 1000 V)

- 5.3.3 High Voltage (Above 1000 V)

- 5.4 By Mounting Type

- 5.4.1 Surface-Mount

- 5.4.2 Metal-Cap

- 5.4.3 Radial-Lead

- 5.5 By End-Use Application

- 5.5.1 Aerospace and Defense

- 5.5.2 Automotive

- 5.5.3 Consumer Electronics

- 5.5.4 Industrial

- 5.5.5 Medical Devices

- 5.5.6 Power and Utilities

- 5.5.7 Telecommunications

- 5.5.8 Rest of End-Use Applications

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 South Korea

- 5.6.3.4 India

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 Rest of the World

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 Murata Manufacturing Co., Ltd.

- 6.4.2 Samsung Electro-Mechanics Co., Ltd.

- 6.4.3 Taiyo Yuden Co., Ltd.

- 6.4.4 Yageo Corporation

- 6.4.5 TDK Corporation

- 6.4.6 Kyocera AVX Components Corporation

- 6.4.7 Walsin Technology Corporation

- 6.4.8 Vishay Intertechnology, Inc.

- 6.4.9 Wurth Elektronik GmbH and Co. KG

- 6.4.10 Guangdong Fenghua Advanced Technology Holding Co., Ltd.

- 6.4.11 Maruwa Co., Ltd.

- 6.4.12 Samwha Capacitor Group

- 6.4.13 Panasonic Holdings Corporation

- 6.4.14 Shenzhen Torch Technology Co., Ltd.

- 6.4.15 Holy Stone Enterprise Co., Ltd.

- 6.4.16 Shenzhen Eyang Technology Development Co., Ltd.

- 6.4.17 Johanson Dielectrics, Inc.

- 6.4.18 KEMET Corporation (Yageo Group)

- 6.4.19 Shenzhen Sunlord Electronics Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment