|

시장보고서

상품코드

2044183

마더보드 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Motherboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

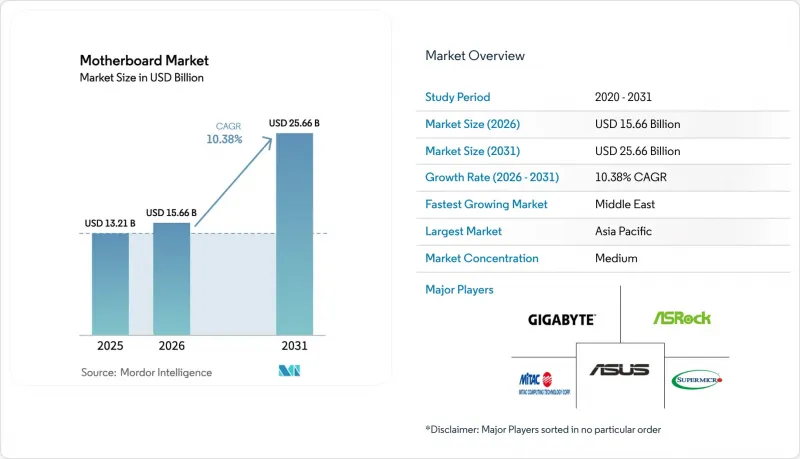

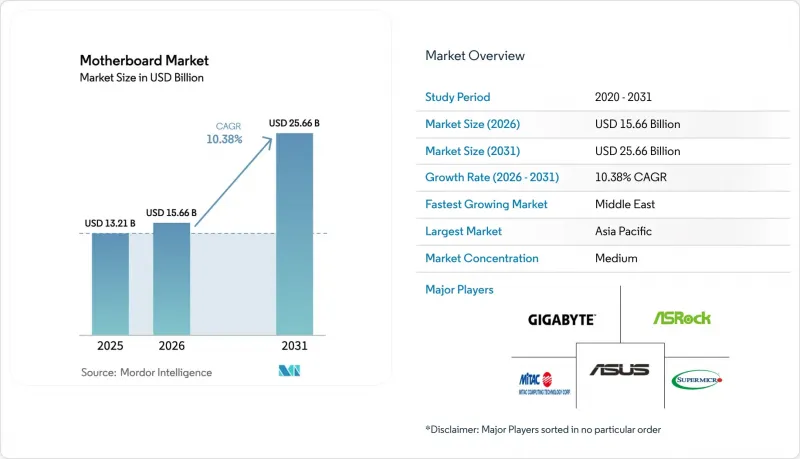

마더보드 시장 규모는 2025년 132억 1,000만 달러, 2026년 156억 6,000만 달러에서 2031년까지 256억 6,000만 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 10.38%를 나타낼 전망입니다.

AI 중심 서버 도입 확대에 따라 하이엔드 서버 보드의 평균 판매 가격은 상승하는 추세입니다. 한편, 소비자 시장에서는 DDR5의 가격 변동에 직면해 있습니다. AMD AM5 및 인텔 LGA-1851 소켓으로의 전환은 업그레이드 시기를 단축하는 한편, 산업용 구매자들은 혹독한 환경을 견딜 수 있는 견고한 설계로 전환하고 있습니다. 아시아태평양은 대만의 ODM 클러스터와 중국의 수탁 제조 거점을 통해 지속적으로 판매량 기반이 되고 있지만, 디지털 인프라에 대한 투자가 가속화되면서 중동이 가장 빠르게 성장하는 지역으로 부상하고 있습니다. 부품에 대한 관세, 다층 PCB 기술자 부족, 중고 기판 수급의 어려움은 단기적인 수요를 억제하고 있지만, 마더보드 시장의 장기적인 성장 궤도를 저해하지는 않습니다.

세계 마더보드 시장 동향 및 인사이트

AI 데이터센터의 서버 마더보드 수요

하이퍼스케일 사업자들은 2024년 AI 인프라를 전년 대비 61% 확대했습니다. 또한, 노드당 최대 12개의 GPU를 지원하는 슈퍼마이크로의 X14 보드는 고밀도 토폴로지가 기판의 복잡성과 수익률을 어떻게 향상시키는지 보여줍니다. 다층 적층, 이중화 VRM, 대역 외 관리 등은 소비자 SKU로는 실현할 수 없는 부품 원가(BOM)의 부가가치를 창출하고 있습니다. 대만의 ODM 업체들은 기판 벤더와의 지리적 근접성을 활용하여 2024년 전 세계 서버 보드 출하량의 60% 이상을 공급했습니다. PCI-SIG CEM 5.0 사양을 준수하는 PCIe 5.0 슬롯의 채택은 신호 무결성 문제를 복잡하게 만드는 한편, 평균 판매 가격(ASP)의 상승을 가져왔습니다. 주요 클라우드 제공업체들이 2027년까지 수십억 달러 규모의 GPU 클러스터에 대한 투자를 계획하고 있는 가운데, 서버 보드는 계속해서 중요한 성장 동력이 될 것입니다.

AM5 및 LGA-1851 플랫폼의 빠른 재생 주기

2024년 하반기 Arrow Lake CPU와 함께 출시된 인텔의 Z890 및 B860 칩셋은 DDR4 지원을 중단하고 Wi-Fi 7 및 Thunderbolt 4를 표준 기능으로 통합하여 채널 재고 전환을 가속화했습니다. 한편, AMD의 AM5 소켓은 2027년까지 칩셋 호환성을 약속하고 있어, 메인보드 제조업체들은 소켓 재설계를 최소화하면서 보급형 B650부터 플래그십 X870E까지 다양한 제품군을 출시할 수 있게 되었습니다. ASRock의 B850 시리즈는 2025년 1월 중급형 가격대로 출시되며, 오버클럭 기능은 탑재하지 않고 PCIe 5.0 M.2를 제공합니다. 이러한 개발 주기의 단축은 신속하게 생산 체제를 전환할 수 있는 기동력 있는 ODM에게는 유리하지만, 회수 기간이 단축됨에 따라 소규모 기업은 수익률 압박에 직면하고 있습니다. 소비자들은 제품 수명이 짧아졌습니다고 느끼고 있으며, 업그레이드 주기가 구독과 같은 주기로 전환되고 있습니다.

세대별 가격 폭등으로 인한 최종 사용자들의 망설임

2025년 초 중급형 LGA-1851 시스템의 경우 메인보드에 200달러, 32GB DDR5-6000 메모리에 150달러, PCIe 5.0 SSD에 120달러, CPU와 GPU를 제외한 총 470달러가 필요했습니다. 이에 비해 2024년 동등한 구성의 경우 320달러였습니다. 아시아태평양에서는 PC 출하량의 39%가 리퍼비시 제품으로, 가격에 대한 민감도가 높은 것으로 나타났습니다. 남미 구매자는 추가 수입 관세에 직면하고 있으며, 브라질의 IPI(공업제품세)로 인해 부품 비용이 10-15% 추가되고 있습니다. 이러한 가격 차이의 확대는 구매 의사를 미루게 하고, 교체 주기가 길어지면서 단기 출하량이 감소하고 있습니다. 벤더들은 기능 한정판 칩셋 SKU 출시, 메모리 번들 판매 및 할부 옵션 등으로 대응하고 있지만, 저소득 지역에서의 가격 탄력성은 여전히 제한적입니다.

부문 분석

ATX는 강력한 확장 슬롯 레이아웃과 충분한 VRM 헤드룸으로 인해 2025년 매출의 45.28%를 차지하며 메인보드 시장에서 가장 큰 점유율을 차지했습니다. 한편, Mini-ITX는 애호가들이 공간 절약형 게이밍 PC를 추구하고 통합업체들이 제한된 인클로저에 엣지 AI 어플라이언스를 도입함에 따라 2031년까지 연평균 복합 성장률(CAGR) 10.41%를 나타낼 것으로 예측됩니다. ATX는 연말연시 성수기를 제외하고는 기업용 리프레시 사이클이 안정적으로 유지되는 반면, Mini-ITX 수요 급증은 고밀도 PCIe 5.0 스토리지 기능을 선보이는 전시회에서의 신제품 발표와 맞물려 있습니다.

PCIe 5.0 레인과 16페이즈 VRM이 Mini-ITX에 도입되어 기존의 성능 격차가 줄어들고 있습니다. ASRock의 'Taichi OCF Mini-ITX'와 기가바이트의 'X870E Aorus Master'는 170mm×170mm 크기의 케이스에 105A의 전원부 스테이지를 탑재해 케이스 크기가 더 이상 성능을 결정짓는 요소가 아님을 보여줍니다. Micro-ATX는 4개의 확장 슬롯과 단순한 6층 PCB 적층의 균형을 유지하면서 저가형 OEM 타워를 위한 주력 제품입니다. Extended-ATX는 주로 듀얼 소켓 서버 및 오버클럭용 메인보드에 채택되고 있으며, 메인보드 시장 규모가 매우 넓어 PCB에 대한 프리미엄 가격 책정을 뒷받침하는 틈새 시장으로 자리 잡고 있습니다.

소비자 및 DIY 빌더는 RGB 조명, 고주사율 출력, 강화된 PCIe 슬롯을 중시하는 e스포츠 카페 및 홈 크리에이터에 힘입어 2025년 매출의 38.72%를 차지할 것으로 예측됩니다. 중국과 인도의 게임 시설은 판매량 증가세가 둔화되고 있음에도 불구하고 높은 평균판매가격(ASP)을 유지하고 있습니다. 반면, 산업용 및 임베디드 부문은 5년간의 부품 로드맵과 IEC 준수 견고성을 필요로 하는 자동화 및 스마트 시티 구축을 통해 CAGR 10.44%의 성장세를 보이며 마더보드 시장 규모를 확대되고 있습니다.

한편, 엔터프라이즈 및 데이터센터 구매자들은 AI 트레이닝을 위해 대역 외 관리, ECC 메모리, 멀티 GPU 토폴로지를 요구하고 있습니다. NVIDIA NVLink 바이패케이션이 탑재된 슈퍼마이크로의 서버 보드는 소비자용 제품에서는 찾아볼 수 없는 디자인적 특징을 구현하고 있습니다. 36-48개월의 긴 생산 주기는 12-18개월의 소비자용 사이클에 비해 설계 변경의 빈도를 줄이고, 총이익률을 향상시킵니다. 게이밍 메인보드는 평균 판매가격(ASP)이 30-50% 더 비싸지만, 산업용 메인보드는 인증 획득, 원격 모니터링 하드웨어, 연장 보증 패키지를 포함하면 가격 차이가 점점 줄어들고 있습니다.

지역별 분석

아시아태평양은 2025년 시장 가치의 36.71%를 차지해, 프로토타입에서 양산까지의 리드타임을 단축하는 대만의 ODM 생태계와 1억 2,000만 대 규모의 중국 조립 기지에 의해 뒷받침되고 있습니다. 일본 업체들은 IEC 인증을 획득한 FA(공장자동화)용 마더보드로 사업을 전환하고 있는 반면, 한국은 메모리 분야의 우위를 살려 기판 설계를 효율화하는 DDR5 모듈을 공급하고 있습니다. 호주 및 뉴질랜드는 주로 기업용 데스크톱과 교육기관 도입에 있어 소규모로 기여하고 있으며, 예측 가능한 업데이트 예산이 탄탄한 수익 기반을 형성하고 있습니다.

중동은 2031년까지 연평균 복합 성장률(CAGR) 10.52%로 가장 빠르게 성장하는 지역입니다. 사우디아라비아의 2025년 1,000억 달러 규모의 디지털 경제와 이 지역의 핀테크 붐은 콜센터와 정부 기관의 업무 부하를 처리하기 위한 저비용 데스크톱 PC 구축에 박차를 가하고 있습니다. 아랍에미리트(UAE)의 200억 달러 규모의 전자기기 분야는 현재 데이터센터 구축을 위해 마더보드를 현지에서 조립하여 수입 장벽을 낮추고 있습니다. 간헐적인 정전 및 광대역 제약으로 인해 광범위한 입력이 가능한 전원공급장치(PSU)와 패시브 냉각 기능을 갖춘 보드에 대한 수요가 증가하고 있으며, 이는 산업용 등급 사양에 부합하는 견고한 SKU의 지역 내 마더보드 시장 점유율을 높이고 있습니다.

북미와 유럽은 성숙한 시장이지만, 관세 정책과 친환경 디자인 규제가 조달을 좌우하는 전략적으로 중요한 지역입니다. 미국의 섹션 301에 따른 25-35%의 관세는 베트남과 멕시코로 생산기지를 분산시키는 계기가 되었습니다. 한편, CHIPS법에 근거한 20억 달러의 보조금은 국내 기판 생산을 지원하는 것입니다. 유럽 수리 가능성에 관한 지침 2024/1799는 벤더에게 7년간의 예비 부품 공급을 의무화하고 있으며, 모듈형 도터보드로 설계를 유도하고 있습니다. 독일과 영국이 AI 서버 도입을 주도하는 한편, 프랑스는 주권 컴퓨팅을 추진하고, 러시아는 현지 조립을 가속화하고 있으며, 이 모든 것이 완만하지만 지속적인 마더보드 시장의 성장을 가속하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.11The motherboard market size is projected to expand from USD 13.21 billion in 2025 and USD 15.66 billion in 2026 to USD 25.66 billion by 2031, registering a CAGR of 10.38% between 2026 to 2031.

Growing AI-centric server rollouts are lifting average selling prices for high-layer server boards even as the consumer segment grapples with DDR5 cost swings. Socket transitions to AMD AM5 and Intel LGA-1851 are compressing upgrade windows, while industrial buyers shift toward ruggedized designs that tolerate harsh environments. Asia-Pacific continues to anchor volume through Taiwan's ODM cluster and China's contract-manufacturing base, yet the Middle East is emerging as the fastest-growing region as digital-infrastructure investments accelerate. Component tariffs, multi-layer PCB skill shortages, and second-hand board availability temper near-term demand but do not derail the long-run trajectory of the motherboard market.

Global Motherboard Market Trends and Insights

Server Motherboard Demand From AI Data-Centres

Hyperscale operators expanded AI infrastructure by 61% year-over-year in 2024, and Supermicro's X14 boards supporting up to 12 GPUs per node illustrate how dense topologies are lifting board complexity and margins. Multi-layer stack-ups, redundant VRMs, and out-of-band management add bill-of-materials value that consumer SKUs cannot match. Taiwan ODMs supplied more than 60% of global server-board volume in 2024, leveraging proximity to substrate vendors. Adoption of PCIe 5.0 slots per PCI-SIG CEM 5.0 spec compounds signal-integrity challenges but secures higher ASPs. With major cloud providers budgeting multi-billion-dollar GPU clusters through 2027, server boards remain a pivotal growth engine.

Rapid AM5 and LGA-1851 Platform Refresh Cycles

Intel's Z890 and B860 chipsets, introduced alongside Arrow Lake CPUs in late 2024, dropped DDR4 support and folded Wi-Fi 7 and Thunderbolt 4 into baseline features, forcing faster channel inventory transitions. AMD's AM5 socket, conversely, pledges chipset compatibility through 2027, allowing board brands to span entry-level B650 to halo X870E with minimal socket redesign. ASRock's B850 series debuted in January 2025 at mid-market price points, providing PCIe 5.0 M.2 without overclocking extras. The compressed cadence benefits agile ODMs that can re-tool quickly, but smaller firms face margin squeeze as payback windows narrow. Consumers confront shorter perceived longevity, nudging upgrade behavior toward subscription-like frequency.

End-User Hesitation Due to Generational Price Jumps

A mid-tier LGA-1851 system in early 2025 required USD 200 for the motherboard, USD 150 for 32 GB DDR5-6000, and USD 120 for a PCIe 5.0 SSD, totaling USD 470 before CPU and GPU, versus USD 320 for a comparable 2024 build. Asia-Pacific sees 39% of PC shipments refurbished, highlighting price sensitivity. South American buyers confront additional import duties, with Brazil's IPI adding 10-15% to component costs. The wider delta delays purchase intent, lengthening replacement cycles and trimming short-run shipments. Vendors respond with cut-down chipset SKUs, bundled memory promotions, and financing options, but elasticity remains limited in low-income regions.

Other drivers and restraints analyzed in the detailed report include:

- AI-Accelerated BIOS Utilities Driving DIY Upgrades

- Growth of Industrial IoT Requiring Rugged Boards

- Skill Shortage In Multi-Layer PCB Manufacturing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

ATX accounted for 45.28% of 2025 revenue, securing the largest motherboard market share for its robust expansion-slot layout and ample VRM headroom. Mini-ITX, however, is forecast to accelerate at a 10.41% CAGR through 2031 as enthusiasts pursue space-efficient gaming rigs and integrators deploy edge-AI appliances in constrained enclosures. Outside holiday peaks, ATX maintains a steady enterprise refresh cadence, while Mini-ITX spikes align with trade-show launches that unveil high-density PCIe 5.0 storage capabilities.

PCIe 5.0 lanes and 16-phase VRMs have migrated into Mini-ITX, eroding the historical performance gap. ASRock's Taichi OCF Mini-ITX and Gigabyte's X870E Aorus Master showcase 105 A power stages inside 170 mm X 170 mm footprints, signaling that footprint no longer dictates capability. Micro-ATX remains the volume workhorse for budget OEM towers, balancing four expansion slots against simpler six-layer PCB stack-ups. Extended-ATX persists mainly in dual-socket servers and showcase overclocking boards, niches where the motherboard market size supports premium pricing on extra-wide PCBs.

Consumer and DIY builders generated 38.72% of 2025 sales, fueled by eSports cafes and home creators who value RGB lighting, high-refresh outputs, and reinforced PCIe slots. Gaming venues in China and India sustain high ASPs despite moderating unit growth. The industrial and embedded segment, by contrast, is on a 10.44% CAGR path that elevates the motherboard market size across automation and smart-city rollouts needing 5-year component roadmaps and IEC-compliant ruggedness.

Enterprise and data-center buyers demand out-of-band management, ECC memory, and multi-GPU topologies for AI training. Supermicro's server boards with NVIDIA NVLink bifurcation exemplify design features absent from the consumer realm. Longer 36-48 month production runs reduce design churn, improving gross margins relative to 12-18 month consumer cadences. Although gaming boards sell at 30-50% ASP premiums, industrial motherboards increasingly match that uplift by layering certifications, remote-monitoring hardware, and extended warranty packages.

The Motherboard Market Report is Segmented by Form Factor (ATX, Micro-ATX, Mini-ITX, and Extended-ATX), End-User Industry (Consumer/DIY, Gaming and ESports Centres, Industrial/Embedded, and Enterprise and Data-Centre), CPU Platform (Intel LGA-1700/1851, AMD AM4/AM5, and More), Application (Desktop PCs, Workstations, Servers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 36.71% of the 2025 value, sustained by Taiwan's ODM ecosystem that compresses prototype-to-production lead times and China's 120 million-unit assembly base. Japanese vendors pivot toward factory-automation motherboards with IEC certifications, while South Korea's memory dominance supplies DDR5 modules that streamline board design. Australia and New Zealand contribute modest volumes, mainly in enterprise desktops and educational deployments, yet predictable refresh budgets create a resilient revenue floor.

The Middle East is the fastest-growing territory at a 10.52% CAGR through 2031. Saudi Arabia's USD 100 billion 2025 digital economy and the region's fintech boom are catalyzing low-cost desktop builds for call-center and government workloads. The United Arab Emirates's USD 20 billion electronics sector now locally assembles motherboards for data-center rollouts, reducing import friction. Intermittent power and broadband constraints drive demand for boards with wide-input PSUs and passive cooling, aligning with industrial-grade specifications and boosting regional motherboard market share for rugged SKUs.

North America and Europe represent mature but strategically important regions where tariff policies and eco-design mandates shape sourcing. The United States' 25%-35% Section 301 duties sparked diversification to Vietnam and Mexico, while USD 2 billion in CHIPS Act grants targets domestic substrate production. Europe's Directive 2024/1799 on repairability obliges vendors to supply spares for seven years, nudging designs toward modular daughtercards. Germany and the United Kingdom spearhead AI server deployments, whereas France promotes sovereign compute and Russia accelerates local assembly, all reinforcing sustained, if moderate, motherboard market growth.

- ASUSTeK Computer Inc.

- GIGABYTE Technology Co., Ltd.

- Micro-Star International Co., Ltd. (MSI)

- ASRock Incorporation

- Super Micro Computer, Inc.

- Advantech Co., Ltd.

- MiTAC Computing Technology Corporation

- Biostar Microtech International Corp.

- EVGA Corporation

- Acer Inc.

- Shenzhen Seavo Technology Co., Ltd.

- Sapphire Technology Ltd.

- AAEON Technology Inc.

- Kontron AG

- Advantech Europe B.V.

- DFI Inc.

- IEI Integration Corp.

- Dell Technologies Inc.

- Intel Corporation

- Lenovo Group Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid AM5 and LGA-1851 Platform Refresh Cycles

- 4.2.2 AI-Accelerated BIOS Utilities Driving DIY Upgrades

- 4.2.3 Growth of Industrial IoT Requiring Rugged Boards

- 4.2.4 Server Motherboard Demand From AI Data-Centres

- 4.2.5 Eco-Design Regulations Favoring Repairable Boards

- 4.2.6 Falling DDR5 Prices Lowering Total Build Costs

- 4.3 Market Restraints

- 4.3.1 End-User Hesitation Due to Generational Price Jumps

- 4.3.2 Skill Shortage in Multi-Layer PCB Manufacturing

- 4.3.3 Geopolitical Tariffs on Key PCB Raw Materials

- 4.3.4 Second-Hand LGA 1151 Boards Cannibalizing Sales

- 4.4 Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Form Factor

- 5.1.1 ATX

- 5.1.2 Micro-ATX

- 5.1.3 Mini-ITX

- 5.1.4 Extended-ATX (E-ATX)

- 5.2 By End-user Industry

- 5.2.1 Consumer / DIY

- 5.2.2 Gaming and eSports Centres

- 5.2.3 Industrial / Embedded

- 5.2.4 Enterprise and Data-centre

- 5.3 By CPU Platform

- 5.3.1 Intel (LGA-1700 / 1851)

- 5.3.2 AMD (AM4 / AM5)

- 5.3.3 ARM-based

- 5.3.4 RISC-V and Others

- 5.4 By Application

- 5.4.1 Desktop PCs

- 5.4.2 Workstations

- 5.4.3 Servers

- 5.4.4 Edge-AI and IoT Gateways

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 Turkey

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ASUSTeK Computer Inc.

- 6.4.2 GIGABYTE Technology Co., Ltd.

- 6.4.3 Micro-Star International Co., Ltd. (MSI)

- 6.4.4 ASRock Incorporation

- 6.4.5 Super Micro Computer, Inc.

- 6.4.6 Advantech Co., Ltd.

- 6.4.7 MiTAC Computing Technology Corporation

- 6.4.8 Biostar Microtech International Corp.

- 6.4.9 EVGA Corporation

- 6.4.10 Acer Inc.

- 6.4.11 Shenzhen Seavo Technology Co., Ltd.

- 6.4.12 Sapphire Technology Ltd.

- 6.4.13 AAEON Technology Inc.

- 6.4.14 Kontron AG

- 6.4.15 Advantech Europe B.V.

- 6.4.16 DFI Inc.

- 6.4.17 IEI Integration Corp.

- 6.4.18 Dell Technologies Inc.

- 6.4.19 Intel Corporation

- 6.4.20 Lenovo Group Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment