|

시장보고서

상품코드

2044188

침투 테스트 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Penetration Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

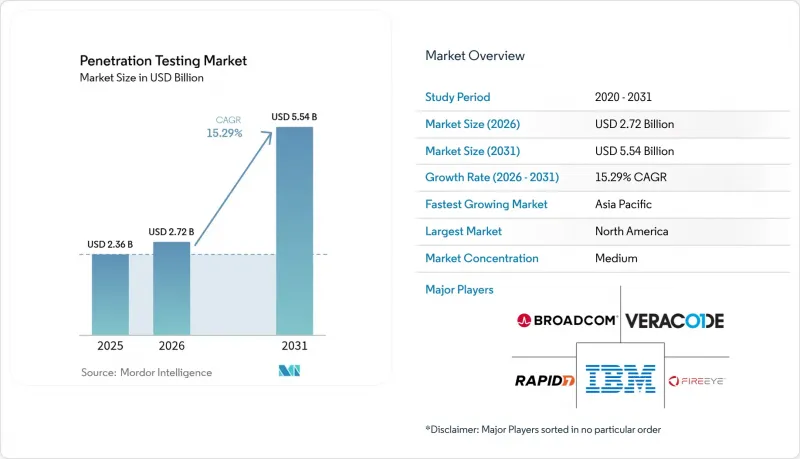

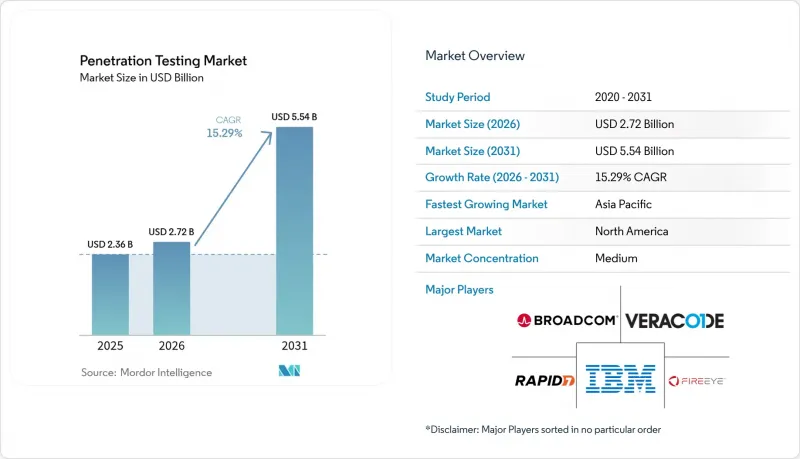

침투 테스트 시장 규모는 2025년 23억 6,000만 달러, 2026년 27억 2,000만 달러에서 2031년까지 55억 4,000만 달러로 확대될 것으로 예측되고 있으며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 15.29%를 나타낼 전망입니다.

클라우드 워크로드의 급속한 확산, 생성형 AI를 활용한 공격의 급증, 규제 준수 기한의 단축으로 인해 침투 테스트는 일회성 감사에서 상시 운영 관리로 전환되고 있습니다. 기업들은 현재 예방적 검증을 공격자가 몇 시간 내에 악용할 수 있는 공개된 취약점에 대한 필수적인 보험으로 인식하고 있습니다. HIPAA와 PCI DSS 버전 4.0에 따른 연례 테스트 의무화, 유럽연합(EU)의 '디지털 운영 탄력성 법(DORA)'과 NIS2로 인해 내부 의사결정 주기가 단축되고, 다년 계약 금액이 증가하고 있습니다. 각 벤더들은 테스트 기간을 몇 주에서 며칠로 단축하는 자율형 레드팀 에이전트로 이에 대응하고 있으며, CI/CD 파이프라인과의 통합을 통해 개발자가 커밋마다 테스트를 실행할 수 있도록 하고 있습니다. 따라서 경쟁 환경은 지속적인 커버리지, 규제 대응 현황 가시성, 상세한 보고 기능을 겸비한 플랫폼이 유리합니다.

세계 침투 테스트 시장 동향 및 인사이트

전 분야에 걸친 사이버 보안 리스크 증가

현재 취약점이 공개된 후 몇 시간 내에 공개형 익스플로잇 킷이 등장하고 있어 방어 측의 대응 시간이 단축되고, 침투 테스트의 빈도를 높여야 하는 상황입니다. Dragos의 조사에 따르면, 2026년에는 26개의 위협 그룹이 OT(Operational Technology)를 적극적으로 탐색하고 있으며, 산업 환경이 더 이상 은폐성과 안전성을 누리지 못한다는 것을 보여줍니다. 폴란드의 전력망에 대한 조직적인 공격으로 인해 미국 사이버 보안 인프라 보안청(CISA)은 중요 인프라 사업자에게 분기별 테스트를 요청하며, 연례적인 테스트 주기에 대한 규제 당국의 인내심이 한계에 다다랐음을 시사했습니다. 펜테라가 500명의 보안 책임자를 대상으로 실시한 설문조사에 따르면, 67%가 전년도에 최소 1회 이상 침해 피해를 입었고, 테스트 예산의 중앙값은 18만 7,000달러로 상승했습니다. 이는 경영진이 현재 예방적 검증을 감사를 위한 사치품이 아닌 보험으로 인식하고 있다는 것을 반증합니다. 이러한 데이터를 종합하면, 위협의 속도가 빨라짐에 따라 지속적인 침투 테스트에 대한 수요가 직접적으로 확대되고 있음을 알 수 있습니다.

보안 평가 및 컴플라이언스 감사에 대한 수요 증가

다층적인 산업 프레임워크로 인해 침투 테스트의 의무 조항이 겹겹이 쌓여 조직은 여러 감사를 하나의 프로그램으로 통합해야 합니다. 2025년 3월부터 시행되는 PCI DSS 버전 4.0은 모든 가맹점에 대해 연례 테스트와 함께 이전에는 선택 사항이었던 세분화 및 무선 평가가 의무화됩니다. FDA의 시판 전 지침은 의료기기 제조업체가 모든 신청서에 테스트 결과를 포함하고 시판 후 증거를 유지하도록 요구하고 있으며, 그 범위는 병원부터 공급업체까지 확대되고 있습니다. FedRAMP 3.0은 연방정부 클라우드 제공업체에 대해 분기별 스캔과 연례 테스트를 의무화하고 있으며, 초안 단계에 있는 4.0에서는 영향력이 큰 시스템에 대해 그 빈도를 두 배로 늘릴 것을 제안하고 있습니다. 뉴욕주의 개정된 23 NYCRR 500 규정은 이사회가 30일 이내에 침투 테스트 결과를 검토하도록 요구하고 있으며, 이는 테스트가 단순한 기술적 연습에서 거버넌스의 결과물로 격상된 것입니다. 이러한 중복 감사로 인해 기업들은 하나의 계약으로 여러 규정집에 대응할 수 있는 매니지드 서비스 제공업체를 찾고 있습니다.

숙련된 테스터의 부족과 높은 비용

인증된 침투 테스터에 대한 전 세계 수요는 공급을 크게 초과하고 있으며, 이로 인해 계약 비용이 치솟고 프로젝트 대기 시간이 길어지고 있습니다. ISC2의 조사에 따르면, 95%의 조직이 사이버 보안 인력이 부족하다고 답했으며, 공격 테스트 담당자는 채용이 가장 어려운 세 가지 직종 중 하나로 꼽혔습니다. 영국은 2024년 기준으로 여전히 11,200명의 사이버 보안 인력이 부족하며, 특히 공격적인 역할의 채용에 가장 오랜 시간이 걸리고 있습니다. 고급 OSCP 자격증의 합격률은 여전히 50% 미만으로 학습 곡선이 가파르고 인재 파이프라인의 성장이 느리다는 것을 보여줍니다. 따라서 기업들은 일상 업무의 자동화에 눈을 돌리고 있지만, 범위 설정, 소셜 엔지니어링 및 공격 후 분석에는 여전히 인간의 전문 지식이 필요합니다. 이러한 인력 부족은 서비스 제공 능력을 제한하고 있으며, 수요 증가에도 불구하고 시장 성장을 저해하고 있습니다.

부문 분석

2025년 침투 테스트 시장에서 네트워크 평가는 38.23%의 점유율을 차지하여 경계 방어와 횡방향 이동 방어가 여전히 우선순위를 차지하고 있음을 보여줍니다. 그러나 멀티 클라우드 도입에 힘입어 클라우드 침투 테스트는 2031년까지 연평균 복합 성장률(CAGR) 16.63%로 확대될 것으로 예상되며, 가장 빠르게 성장하는 분야가 될 것으로 전망됩니다. 이러한 변화는 기존 네트워크의 범위를 벗어난 컨테이너 오케스트레이션, 서버리스 기능, API 중심의 아키텍처를 반영하고 있습니다. Bishop Fox는 2026년 CloudFox 툴킷을 Google Cloud Platform으로 확장하여 클라우드 네이티브 테스트 방법이 성숙기에 접어들었음을 보여주었습니다. 공격자들이 채널을 넘나들며 API와 크리덴셜 스터핑 기법을 자주 재사용하기 때문에 모바일과 웹 용도의 테스트가 통합되고 있습니다. 소셜 엔지니어링 연습에서는 생성형 AI를 통해 가능해진 트렌드로 딥페이크 음성이나 동영상에 의한 공격을 시뮬레이션하는 것이 가능해졌습니다. 무선 테스트의 범위가 확대되어 공장 및 물류 센터의 Wi-Fi 6E 및 5G 프라이빗 네트워크도 테스트 대상에 포함됩니다. 산업 자산 소유자가 다운타임을 피하기 위해 샌드박스 환경에서 생산 환경을 재현하기 시작하면서 IoT 및 운영 기술(OT)에 대한 평가도 증가하고 있습니다.

네트워크, 클라우드, 용도 범위를 통합한 하이브리드형 침투 테스트 시장 규모가 확대되고 있습니다. 이는 구매자가 여러 프레임워크에 걸친 단일 계약을 선호하기 때문입니다. 컴플라이언스 주기가 엄격해지면서 통합 대시보드와 자동 재테스트를 제공하는 벤더들이 계약을 따내고 있습니다. 지속적인 검증에 대한 기대는 빠르게 증가하고 있으며, Bishop Fox의 Cosmos AI는 평가 시간을 40% 단축한다고 주장하고, HackerOne의 에이전트 서비스는 며칠이 아닌 몇 시간 내에 결과를 보고합니다. 이러한 효율화를 통해 보안팀은 예산을 늘리지 않고도 더 빈번한 테스트 일정을 잡을 수 있습니다. 위협 행위자가 공개된 취약점을 몇 시간 만에 악용하는 상황에서 기업들은 단순히 취약점의 존재를 확인하는 데 그치지 않고, 실제로 악용 가능한지 여부를 검증하는 방식으로 전환하고 있습니다. 그 결과, 일시적인 네트워크 스캔에서 CI/CD 파이프라인에 직접 통합되는 상시 가동형 클라우드 및 용도 프로브에 대한 수요가 증가하고 있습니다.

2025년 기준, 많은 규제 대상 산업이 여전히 On-Premise 관리를 선호하기 때문에 On-Premise 구축이 침투 테스트 시장의 59.21%를 차지했습니다. 그러나 DevSecOps 사이클에 부합하는 탄력적인 확장 및 신속한 기능 업데이트에 힘입어 클라우드 제공 플랫폼은 2031년까지 연평균 복합 성장률(CAGR) 15.61%를 나타낼 것으로 예측됩니다. Aikido Infinite는 개발자가 서버를 프로비저닝하지 않고도 커밋할 때마다 침투 테스트를 실행할 수 있도록 하여 SaaS 제공의 운영 편의성을 보여주고 있습니다. PCI DSS 4.0에서는 클라우드 기반 테스트가 카드 회원 데이터 규칙을 충족하는 것이 명확해져 오랫동안 남아있던 장벽이 제거되었습니다. 현재 하이브리드 환경이 엔터프라이즈 아키텍처의 주류로 자리 잡으면서 클라우드 워크로드와 On-Premise 자산에 대한 가시성이 필수적으로 요구되고 있습니다.

On-Premise 침투 테스트 시장은 주권 관련 규정으로 인해 외부와의 연결이 차단된 정부 및 국방 네트워크에서 여전히 견조한 성장세를 보이고 있습니다. 이러한 환경에서도 벤더들은 접속이 가능하면 익명화된 조사 결과를 동기화할 수 있는 가상 어플라이언스를 제공합니다. 더 넓은 시장에서는 구독 가격 체계로 인해 지출이 자본 지출에서 운영 예산으로 전환되고 승인 절차가 간소화되었습니다. 매니지드 서비스 제공업체들은 이사회 차원의 보고 요건을 충족하는 구두 보고와 함께 클라우드 테스트 대시보드를 번들로 제공하는 경우가 많아지고 있습니다. 또한, 테스트 결과를 REST API를 통해 티켓 관리 시스템으로 직접 가져와 패치 검증을 빠르게 할 수 있다는 점도 구매자들로부터 좋은 평가를 받고 있습니다. 지속적인 배포가 보편화됨에 따라, 조직은 클라우드를 단순한 선택이 아닌, 법령에 의해 금지되지 않는 한 기본 옵션으로 간주하고 있습니다.

지역별 분석

북미는 2025년 침투 테스트 시장의 38.27%를 차지했습니다. 이는 HIPAA, PCI DSS 4.0, FedRAMP와 같은 성숙한 규제 프레임워크에 의해 뒷받침되고 있으며, 이는 연간 또는 반기별 테스트 주기를 공식적으로 규정하고 있습니다. 미국의 금융기관들은 위협 중심 테스트를 운영 탄력성 프로그램에 통합하고 있으며, 캐나다의 의료 개인정보 보호 법령은 병원들이 지속적인 검증을 도입할 것을 촉구하고 있습니다. 멕시코의 급성장하는 핀테크 생태계도 침투 테스트를 국경 간 결제 라이선스에 포함시켜 지역적 수요를 확대되고 있습니다. 벤처 자금은 실리콘밸리와 보스턴에 집중되어 있으며, 이로 인해 현지 플랫폼 벤더들은 국내 고객을 위해 테스트 주기를 단축하는 AI 에이전트를 반복적으로 개발하고 있습니다. 그 결과, 북미는 새로운 도구와 서비스 모델의 기준이 되는 시장으로 자리매김하고 있습니다.

아시아태평양에서는 2031년까지 연평균 복합 성장률(CAGR) 16.26%로 침투 테스트 시장이 확대될 것으로 예상되며, 이는 지역별로 가장 높은 성장 궤도를 보일 것으로 예측됩니다. 인도에서는 사이버 보안 인력이 30%-50% 부족하기 때문에 기업들은 자동화 플랫폼 도입을 촉진하고 있습니다. 한편, 중국에서는 데이터 현지화 규정에 따라 개인정보를 취급하는 모든 시스템에 대한 국내 테스트가 의무화되어 있습니다. 일본의 개정된 개인정보보호법 및 한국의 중요 인프라 관련 규정으로 인해 연례 테스트가 기업 지배구조에 더 많이 포함되고 있습니다. 인도네시아와 필리핀에서 디지털 결제의 급속한 확산은 지역 게이트웨이에 연결되는 소규모 가맹점에 대한 검증의 필요성을 강조하고 있습니다. 이러한 요인들이 복합적으로 작용하여 수요가 급증하고 있으며, 세계 벤더들이 지역 내 클라우드 PoP(Point of Presence)와 현지 언어로 된 보고서를 제공하는 것을 정당화하는 요인이 되고 있습니다.

유럽에서는 'Digital Operational Resilience Act(Digital Operational Resilience Act)', 'NIS2', 그리고 향후 시행될 'Cyber Resilience Act'에 의해 컴플라이언스의 최소기준이 수립되어 있으며, 이에 따라 침투 테스트는 모범 사례에서 법적 의무로 격상되고 있습니다. 독일 연방정보보안청(BSI)은 2025년 중요 인프라를 위한 분야별 플레이북을 발표했고, 프랑스는 SecNumCloud 프레임워크를 확장하여 서비스 제공업체에 대한 의무적 테스트를 포함하도록 했습니다. 영국 국가사이버보안센터(NCSC)는 브렉시트 이후 기준을 유럽 대륙의 규범과 일치시키기 위해 기밀 데이터를 취급하는 모든 기업에 대해 연례 테스트를 권장하고 있습니다. 남미, 중동 및 아프리카는 브라질의 데이터 보호법과 걸프만 국가들의 국가 사이버 프로그램이 라이선스 제도에 공격적인 테스트를 도입하면서 유력한 시장으로 부상하고 있습니다. 따라서 전반적인 지리적 확장 속도는 각 관할권에서 법령이 '지침'에서 '시행'으로 전환되는 속도에 따라 달라질 수 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The penetration testing market size is projected to expand from USD 2.36 billion in 2025 and USD 2.72 billion in 2026 to USD 5.54 billion by 2031, registering a CAGR of 15.29% between 2026 to 2031.

Rapid adoption of cloud workloads, a sharp rise in generative-AI driven exploits, and compressed regulatory deadlines are moving penetration testing from ad-hoc audits to an always-on control. Enterprises now treat proactive validation as essential insurance against publicly disclosed vulnerabilities that adversaries weaponize within hours. Mandatory annual tests under HIPAA and PCI DSS version 4.0, along with the European Union's Digital Operational Resilience Act and NIS2, have shortened internal decision cycles and lifted multi-year contract values. Vendors are responding with autonomous red-team agents that cut test duration from weeks to days, while integration with CI/CD pipelines enables developers to trigger tests at every commit. Competitive dynamics, therefore, favor platforms that combine continuous coverage, regulatory mapping, and granular reporting.

Global Penetration Testing Market Trends and Insights

Rising Cybersecurity Risks Across Sectors

Public exploit kits now appear within hours of vulnerability disclosure, shrinking defenders' reaction windows and forcing more frequent penetration tests. Dragos counted 26 threat groups actively probing operational technology in 2026, showing that industrial environments no longer enjoy obscurity or safety. After a coordinated attack on Poland's energy grid, CISA urged quarterly testing for critical infrastructure operators, signaling regulatory impatience with annual testing cycles. A Pentera survey of 500 security leaders found 67% suffered at least one breach in the prior year and raised testing budgets to a median of USD 187,000, confirming that executives now treat proactive validation as insurance rather than an audit luxury. Together, these data points illustrate how escalating threat velocity directly expands demand for continuous penetration testing.

Increasing Demand for Security Assessments and Compliance Audits

Layered industry frameworks are stacking mandatory penetration-testing clauses, compelling organizations to synchronize multiple audits into one program. PCI DSS version 4.0, effective March 2025, requires annual testing for all merchants, plus segmentation and wireless assessments that were previously optional. FDA pre-market guidance obliges medical-device makers to include test results in every submission and maintain post-market evidence, widening the scope beyond hospitals to their suppliers. FedRAMP 3.0 requires quarterly scanning and annual testing for federal cloud providers, with a draft 4.0 proposal to double the cadence for high-impact systems. New York's amended 23 NYCRR 500 rule requires boards to review penetration-testing findings within 30 days, elevating tests from technical exercises to governance artifacts. These overlapping audits drive enterprises toward managed service providers that can map a single engagement to multiple rulebooks.

Shortage and High Cost of Skilled Testers

Global demand for certified penetration testers far exceeds supply, driving up engagement fees and lengthening project queues. ISC2 found that 95% of organizations report cybersecurity staffing gaps, ranking offensive testing among the three hardest roles to fill. The United Kingdom still needed 11,200 additional cybersecurity workers in 2024, with offensive roles taking the longest to hire. Pass rates for advanced OSCP credentials remain below 50%, underscoring steep learning curves and slow growth in the talent pipeline. Enterprises, therefore, turn to automation for routine tasks, yet scoping, social engineering, and post-exploitation analysis still require human expertise. The persistent talent deficit caps service capacity and tempers market growth despite strong demand.

Other drivers and restraints analyzed in the detailed report include:

- Government Mandates and Industry-Specific Regulations

- DevSecOps Pipelines Require Continuous Pen-Testing Integration

- Lack of Awareness Among SMEs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Network assessments held a 38.23% market share in penetration testing in 2025, underscoring the continued priority of perimeter and lateral-movement defenses. Yet cloud penetration testing, propelled by multi-cloud adoption, is projected to advance at a 16.63% CAGR through 2031, making it the fastest-growing modality. The shift reflects container orchestration, serverless functions, and API-centric architectures that fall outside traditional network scopes. Bishop Fox expanded its CloudFox toolkit to Google Cloud Platform in 2026, signaling maturity in cloud-native testing methods. Mobile and web application tests are converging because adversaries frequently reuse API and credential-stuffing tactics across channels. Social-engineering exercises now simulate deepfake voice and video attacks, a trend made possible by generative AI. Wireless testing widens to cover Wi-Fi 6E and 5G private networks in factories and logistics hubs. IoT and operational technology assessments grow as industrial asset owners replicate production environments in sandboxes to avoid downtime.

The penetration testing market size for hybrid engagements that bundle network, cloud, and application scopes is growing, as buyers prefer a single contract that spans multiple frameworks. Vendors that offer unified dashboards and automated retesting win deals as compliance cycles tighten. Continuous validation expectations are rising quickly; Bishop Fox's Cosmos AI claims a 40% reduction in assessment time, while HackerOne's agentic service delivers findings within hours rather than days. These efficiency gains let security teams schedule more frequent tests without escalating budgets. As threat actors weaponize disclosed flaws in hours, enterprises gravitate toward modalities that confirm exploitability, not just vulnerability presence. Consequently, demand migrates from point-in-time network sweeps to always-on cloud and application probes that integrate directly into CI/CD pipelines.

On-premises deployments commanded 59.21% of the penetration testing market share in 2025, as many regulated sectors still favor on-premises control. However, cloud-delivered platforms are set to grow at a 15.61% CAGR to 2031, fueled by elastic scaling and rapid feature updates that align with DevSecOps cycles. Aikido Infinite lets developers trigger penetration tests on every commit without provisioning servers, illustrating the operational ease of SaaS delivery. PCI DSS 4.0 clarified that cloud-based tests satisfy cardholder data rules, removing a lingering barrier. Hybrid environments now dominate enterprise architectures, so visibility into both cloud workloads and on-premise assets becomes essential.

The penetration testing market for on-prem tools remains resilient in air-gapped government and defense networks, where sovereignty rules block external connectivity. Even there, vendors ship virtual appliances that synchronize anonymized findings once links are available. For the broader market, subscription pricing moves expenditure from capital to operating budgets, simplifying approvals. Managed service providers increasingly bundle cloud testing dashboards with verbal readouts that satisfy board-level reporting. Buyers also cite quicker patch validation when test results are fed directly into ticketing systems via REST APIs. As continuous deployment normalizes, organizations view cloud delivery not as an option but as the default unless a statute forbids it.

The Penetration Testing Market Report is Segmented by Testing Type (Cloud Penetration Testing, and More), Deployment Model (On-Premise, and More), Organization Size (Large Enterprises, and Small and Medium Enterprises), Service Delivery Mode (In-House Testing Teams, and Third-Party Managed Services), End-User Industry (IT and Telecom, Manufacturing, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 38.27% penetration testing market share in 2025, anchored by mature regulatory frameworks such as HIPAA, PCI DSS 4.0, and FedRAMP that formalize annual or semiannual testing cadences. U.S. financial institutions bundle threat-led testing into operational resilience programs, while Canadian health-privacy statutes drive hospitals to adopt continuous validation. Mexico's fast-growing fintech ecosystem also embeds penetration testing into cross-border payment licenses, widening regional demand. Venture funding is concentrated in Silicon Valley and Boston, allowing local platform vendors to iterate on AI agents that shorten test cycles for domestic clients. As a result, North America remains the reference market for new tooling and service models.

Asia-Pacific is forecast to expand its penetration testing market size at a 16.26% CAGR through 2031, the fastest regional trajectory. India's 30% to 50% cyber-talent gap encourages enterprises to adopt automated platforms, while data-localization rules in China compel in-country testing of all systems that handle personal information. Japan's revised Act on the Protection of Personal Information and South Korea's critical infrastructure mandates further hardwire annual testing into corporate governance. Rapid digital-payment adoption in Indonesia and the Philippines underscores the need for validation for small merchants connecting to regional gateways. Together, these factors create a demand surge that helps global vendors justify in-region cloud PoPs and local language reporting.

Europe benefits from a compliance floor established by the Digital Operational Resilience Act, NIS2, and the forthcoming Cyber Resilience Act, which collectively elevate penetration testing from best practice to a legal duty. Germany's BSI released sector playbooks for critical infrastructure in 2025, and France expanded its SecNumCloud framework to include mandatory testing for service providers. The United Kingdom's National Cyber Security Centre recommends annual tests for any firm handling sensitive data, to keep post-Brexit standards aligned with continental norms. South America, the Middle East, and Africa are emerging as strong markets as Brazil's data-protection law and Gulf national cyber programs embed offensive testing into licensing regimes. Overall geographic expansion is therefore paced by how quickly statutes migrate from guidance to enforcement across each jurisdiction.

- IBM Corporation

- Rapid7 Inc.

- Synopsys Inc.

- Checkmarx Ltd.

- Acunetix Ltd.

- Broadcom Inc.

- FireEye Inc.

- Veracode Inc.

- Qualys Inc.

- Tenable Holdings Inc.

- Palo Alto Networks Inc.

- Offensive Security LLC

- Core Security Technologies Inc.

- Pentera Security Ltd.

- HackerOne Inc.

- Trustwave Holdings Inc.

- IOActive Inc.

- NCC Group plc

- Cofense Inc.

- Bishop Fox Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Cybersecurity Risks Across Sectors

- 4.2.2 Increasing Demand for Security Assessments and Compliance Audits

- 4.2.3 Government Mandates and Industry-Specific Regulations

- 4.2.4 DevSecOps Pipelines Require Continuous Pen-Testing Integration

- 4.2.5 AI-Driven Autonomous Red Teaming Enables Continuous Validation

- 4.2.6 Software Bill of Materials Mandates Expand Supply-Chain Pentest Scope

- 4.3 Market Restraints

- 4.3.1 Lack of Awareness Among SMEs

- 4.3.2 Shortage and High Cost of Skilled Testers

- 4.3.3 Ethical Constraints on Live Exploitation of Critical OT Environments

- 4.3.4 Unclear Legal Liability in Multi-Jurisdiction Cloud Environments

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Testing Type

- 5.1.1 Network Penetration Testing

- 5.1.2 Web Application Penetration Testing

- 5.1.3 Mobile Application Penetration Testing

- 5.1.4 Social Engineering Penetration Testing

- 5.1.5 Wireless Network Penetration Testing

- 5.1.6 Cloud Penetration Testing

- 5.1.7 Other Testing Types

- 5.2 By Deployment Model

- 5.2.1 On-Premise

- 5.2.2 Cloud-Based

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Service Delivery Mode

- 5.4.1 In-House Testing Teams

- 5.4.2 Third-Party Managed Services

- 5.5 By End-User Industry

- 5.5.1 Government and Defense

- 5.5.2 Banking, Financial Services and Insurance

- 5.5.3 IT and Telecom

- 5.5.4 Healthcare and Life Sciences

- 5.5.5 Retail and E-Commerce

- 5.5.6 Manufacturing

- 5.5.7 Energy and Utilities

- 5.5.8 Other End-User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Funding

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Rapid7 Inc.

- 6.4.3 Synopsys Inc.

- 6.4.4 Checkmarx Ltd.

- 6.4.5 Acunetix Ltd.

- 6.4.6 Broadcom Inc.

- 6.4.7 FireEye Inc.

- 6.4.8 Veracode Inc.

- 6.4.9 Qualys Inc.

- 6.4.10 Tenable Holdings Inc.

- 6.4.11 Palo Alto Networks Inc.

- 6.4.12 Offensive Security LLC

- 6.4.13 Core Security Technologies Inc.

- 6.4.14 Pentera Security Ltd.

- 6.4.15 HackerOne Inc.

- 6.4.16 Trustwave Holdings Inc.

- 6.4.17 IOActive Inc.

- 6.4.18 NCC Group plc

- 6.4.19 Cofense Inc.

- 6.4.20 Bishop Fox Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment