|

시장보고서

상품코드

2044216

염화알릴 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Allyl Chloride - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

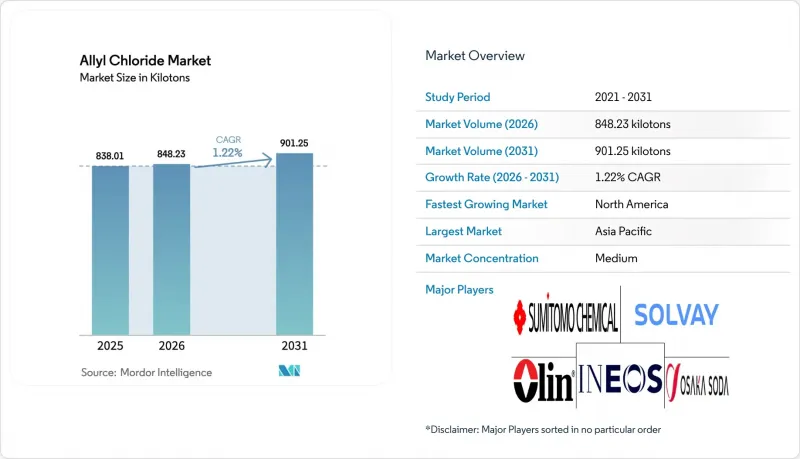

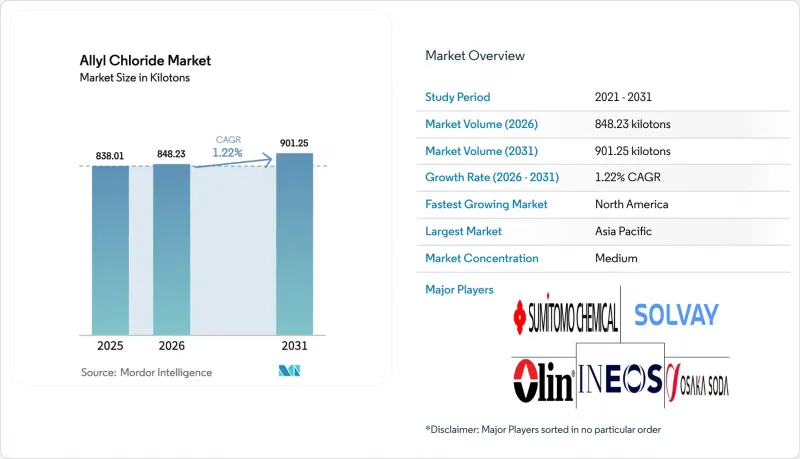

염화알릴 시장 규모는 2025년에 838.01 킬로톤이라고 평가되어 2026년 848.23 킬로톤에서 2031년까지 901.25 킬로톤에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 1.22%를 나타낼 전망입니다.

염화알릴 시장은 여전히 에피클로로히드린 생산을 중심으로 발전하고 있지만, 공정의 발전과 지역별 원료의 장점으로 인해 이러한 의존도는 점차 감소하고 있습니다. 에폭시 수지의 풍력 터빈 블레이드 및 전기자동차 복합소재에 대한 에폭시 수지 적용 확대, 북미의 인프라 투자 재개, 유럽과 미국의 폐수 규제 강화 등이 성장세를 뒷받침하고 있습니다. 또한, 바이오 에피클로로히드린의 생산 능력은 현재 세계 공급량의 6분의 1 이상을 차지하고 있으며, 생산자들은 프로파일렌과 글리세롤 기반 대체품의 경제성을 비교 검토할 수밖에 없는 상황입니다. 디지털 트윈을 활용한 자동화 도입으로 예상치 못한 가동 중단 시간을 줄이고, 수율을 향상시키며, 프로파일렌 및 전력 비용 변동에 따른 영향을 부분적으로 완화하고 있습니다. 한편, 유럽과 미국의 직업적 노출 한계치 강화로 인해 컴플라이언스 비용이 상승하는 한편, 높은 가격대에 거래되는 고순도 제품에 대한 수요도 증가하고 있습니다.

세계 염화알릴 시장 동향 및 인사이트

풍력 터빈 블레이드 및 전기자동차 복합재에 대한 에폭시 수지 수요 급증 추세

2024년 전 세계 풍력 발전 설비 설치에 12만 톤 이상의 에폭시 수지가 사용되며, 증설 용량 1기가와트당 약 1,700톤의 수지가 필요하며, 이는 에피클로로히드린 수요를 직접적으로 견인하고 있습니다. 2024년 배터리 전기자동차(BEV)의 복합재료 부품 사용량은 전년 대비 15% 증가하여 염화알릴 시장을 고부가가치 수지 등급으로 전환하고 있습니다. 2024년 중국은 70GW, 유럽은 18GW, 미국은 12GW의 풍력발전 설비를 증설할 것이며, 이 세 대륙이 성장의 원동력이 될 것입니다. 에폭시 수지 배합 제조업체는 추적 가능한 공급망에 대한 관심이 높아지고 있으며, 이에 따라 염화알릴 생산 제조업체는 배치 인증 프로세스를 더욱 엄격하게 적용하고 있습니다. 배터리 전기자동차 생산량은 2026년까지 2,500만 대에 달할 것으로 예상되며, 바이오 생산 방식이 확산되고 있는 가운데 고순도 에피클로로히드린에 대한 수요는 유지될 것으로 보입니다.

전 세계 공업용 수처리 규제 확대

2024년 최종 결정된 유럽연합(EU) 개정 도시 폐수처리 지침에 따라 2045년까지 대규모 도시권에서 4차 처리를 의무화하고, 제약-화장품 기업에 미량 오염물질 제거 비용의 80%를 부담하도록 의무화했습니다. 이를 통해 신규 처리 시설에 36억 유로의 자금이 확보되었습니다. 2026년에는 퍼플루오로알킬 물질 및 폴리플루오로알킬 물질에 대한 모니터링이 의무화되면서 염화알릴 유래 4급 암모늄 화합물에 대한 수요가 확대되었습니다. 미국에서는 이들 물질에 대한 최대 오염물질 농도(MCL) 제안에 2029년 준수 기한이 포함되어 있으며, 이로 인해 유틸리티 사업자들은 알릴 전구체에 의존하는 이온 교환 수지를 채택해야 하는 상황에 처해 있습니다. 일본에서는 2024년 1,4-디옥산의 배출기준이 강화되고, 인도에서는 섬유산업 거점의 ZLD(Zero Liquid Dicharge) 규제가 확대되면서 특수 응집제에 대한 수요가 증가했습니다. 이러한 규제 동향으로 인해 염화알릴 시장은 경기 순환에 따른 원자재 가격 변동보다는 인프라 투자에 연동된 움직임을 유지하고 있습니다.

엄격한 직업적 노출 및 배출 기준(미국/EU/일본)

미국 산업안전보건국(OSHA)은 8시간 평균 1ppm이라는 기준을 적용하고 있으며, 폐루프 이송 시스템 도입을 의무화하고 있습니다. 이로 인해 중형 플랜트 비용에 약 1,000만 달러가 추가될 수 있습니다. 유럽의 REACH 규정에서는 근로자에 대한 1ppm 기준과 유사한 1ppm 기준 외에 일반인 노출에 대해서는 더 엄격한 0.1ppm 기준을 적용하고 있으며, 증기 회수 장치를 설치해야 합니다. 이로 인해 신규 프로젝트 비용이 약 20% 증가하게 됩니다. 일본 경제산업성은 유사한 노출 기준을 적용하고 연례 건강진단을 의무화하고 있으며, 이로 인해 연간 최대 70만 달러의 운영비가 추가될 수 있습니다. 2024년 개정된 EU의 산업 배출 규제는 반응로에서 VOC 배출량을 5mg/m3로 제한하고 있으며, 이는 열산화 장비에 대한 투자를 촉진하고 있습니다. 이미 규제 위반으로 인해 장쑤성과 구자라트주에서 연간 약 12kg의 생산이 중단된 바 있어, 규제 준수에 대한 리스크가 부각되고 있습니다.

부문 분석

에피클로로히드린은 2025년 생산량의 89.08%를 차지했습니다. 바이오 유래 대체품이 보급되기 시작했음에도 불구하고, 풍력발전, 전기자동차, 전자제품이 이들 생산량의 대부분을 소비했습니다. 그러나 가장 빠르게 성장한 분야는 또 다른 분야였습니다. 수처리 화학물질은 2031년까지 연평균 3.59%의 연평균 복합 성장률(CAGR)로 확대될 것으로 예상되며, 유틸리티 업체들의 엄격한 미량 오염물질 규제 준수에 힘입어 성장세를 보일 것으로 예측됩니다. 의약품용 알릴아민은 제네릭 항진균제에 대한 수요의 수혜를 입었습니다. 가격이 높은 글리시딜 에테르와 알릴 설포네이트는 범용 제품과 특수 제품 생산을 전환할 수 있는 공장에게 여전히 매력적인 선택지였습니다.

생산업체들은 대규모 에피클로로히드린 생산 후 특수용도 생산으로 스케줄을 재편하여 대규모 설비투자 없이 가동률을 극대화했습니다. 디지털 트윈 시스템을 통해 염화물 농도 50ppm 미만의 기준을 충족하는 의약품 등급의 염화알릴으로 36시간 만에 전환할 수 있게 되었습니다. 이러한 유연성으로 인해 프로파일렌 가격이 급등하는 시기에도 고순도 염화알릴 시장 점유율을 확대하여 수익률 하락을 완화할 수 있었습니다. 바이오 에피클로르히드린의 점유율이 확대되는 가운데, 자산의 지속가능성을 확보하기 위해서는 균형 잡힌 포트폴리오 전략이 점점 더 중요해지고 있습니다.

'알릴 클로라이드 시장 보고서'는 용도별(에피클로로히드린, 알릴아민, 알릴설포네이트, 글리시딜에테르, 수처리제, 기타), 지역별(아시아태평양, 북미, 유럽, 남미, 중동/아프리카)로 분류되어 있습니다. 시장 예측은 수량(톤) 기준으로 제공됩니다.

지역별 분석

2025년 아시아태평양은 세계 총 생산량의 52.32%를 차지했습니다. 이 지역의 염화알릴 시장 규모는 대규모 풍력 발전 및 전자 산업에 의해 뒷받침되었지만, 수입된 바이오 유래 에피클로로히드린(bio-ECH) 시장 침투로 인해 대체 압력이 높아졌습니다. 인도는 2025년까지 수성 페인트 수요를 지원하기 위해 구자라트 주에서 연간 12kg의 생산량을 확대할 예정이며, 일본에서는 엄격한 품질 관리 시스템 덕분에 의약품 등급 제품의 수출이 계속해서 지배적인 지위를 유지했습니다. 한국은 프로파일렌 잉여분을 활용하여 동남아시아 고객사에 공급했습니다.

북미는 2031년까지 연평균 복합 성장률(CAGR) 1.36%로 가장 높은 성장률을 보였습니다. 이는 미국 멕시코만 연안의 풍부한 셰일 유래 프로파일렌 및 통합형 염소 생산 능력을 반영한 것입니다. 중서부 및 대서양 연안의 풍력 발전소의 급속한 증가로 에피클로로히드린공급과 수요는 견조한 반면, Dow Chemical의 앨버타 주에 위치한 신규 바이오 플랜트는 구매자에게 탄소 배출량을 줄일 수 있는 선택권을 제공했습니다. 멕시코는 플라스틱 제조를 동아시아에서 북미로 전환하는 니어쇼어링(near-shoring) 추세의 수혜를 입었습니다.

유럽에서는 엄격한 배출 규제로 인해 운영비용이 상승하여 규모가 큰 통합형 대기업이 유리하게 되었습니다. 독일은 여전히 가장 큰 소비국이었지만, 인증된 바이오 소재로의 전환으로 인해 전통적인 수요는 연간 약 3% 감소했습니다. 폴란드와 체코를 중심으로 한 동유럽에서는 인프라 정비의 진전으로 수지 수요가 증가하여 서유럽의 위축을 일부 상쇄하였습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.11The Allyl Chloride Market size was valued at 838.01 kilotons in 2025 and is estimated to grow from 848.23 kilotons in 2026 to reach 901.25 kilotons by 2031, at a CAGR of 1.22% during the forecast period (2026-2031).

The allyl chloride market remains centered on epichlorohydrin production, though advancements in processes and regional feedstock benefits are gradually reducing this reliance. Growth is supported by increasing epoxy resin applications in wind turbine blades and electric vehicle composites, renewed infrastructure investments in North America, and stricter wastewater regulations in Europe and the United States. Additionally, bio-epichlorohydrin capacity now accounts for over one-sixth of global supply, compelling producers to weigh the economics of propylene against glycerol-based alternatives. The adoption of digital-twin automation is reducing unplanned downtime and improving yields, partially mitigating the impact of fluctuating propylene and electricity costs. Meanwhile, stricter occupational exposure limits in both Europe and the United States are driving up compliance costs but also fostering demand for higher-purity products that command premium prices.

Global Allyl Chloride Market Trends and Insights

Surging Epoxy-Resin Demand in Wind-Turbine Blades and Electric-Vehicle Composites

Global wind installations utilized more than 120,000 metric tons of epoxy resin in 2024, with each gigawatt of added capacity requiring approximately 1,700 metric tons of resin, directly driving epichlorohydrin demand. Composite components in battery-electric vehicles increased by 15% year-on-year in 2024, shifting the allyl chloride market toward higher-value resin grades. China added 70 GW of wind power in 2024, Europe contributed 18 GW, and the United States added 12 GW, forming a growth engine across three continents. Epoxy formulators are increasingly focusing on traceable supply chains, leading allyl-chloride producers to tighten batch certification processes. Battery-electric vehicle production is expected to reach 25 million units by 2026, maintaining demand for high-purity epichlorohydrin even as bio-based production methods gain traction.

Expansion of Industrial Water-Treatment Regulations Worldwide

The European Union's revised Urban Wastewater Treatment Directive, finalized in 2024, requires quaternary treatment for large agglomerations by 2045 and mandates pharmaceutical and cosmetic companies to cover 80% of micropollutant removal costs, unlocking EUR 3.6 billion for new treatment facilities. Monitoring of per- and polyfluoroalkyl substances became mandatory in 2026, boosting demand for quaternary-ammonium compounds derived from allyl chloride. In the United States, proposed maximum contaminant levels for these substances include compliance deadlines in 2029, prompting utilities to adopt ion-exchange resins that rely on allyl precursors. Japan tightened discharge limits on 1,4-dioxane in 2024, while India extended zero-liquid-discharge rules for textile hubs, increasing specialty-coagulant volumes. These regulatory developments keep the allyl chloride market aligned with infrastructure investments rather than cyclical commodity fluctuations.

Stringent Occupational-Exposure and Emission Limits (US/EU/JP)

The US Occupational Safety and Health Administration enforces an 8-hour limit of 1 ppm, requiring closed-loop transfer systems that can add approximately USD 10 million to the costs of a mid-size unit. Europe's REACH framework enforces the same 1 ppm worker limit and a stricter 0.1 ppm limit for public exposure, necessitating vapor-recovery units that increase greenfield project costs by about 20%. Japan's Ministry of Economy, Trade and Industry applies similar exposure limits and mandates annual health checks, which can add up to USD 700,000 annually to operating expenses. Revised EU Industrial Emissions rules in 2024 now cap reactor VOC emissions at 5 mg/m3, prompting investments in thermal oxidizers. Non-compliance has already resulted in temporary shutdowns of approximately 12 kilotons per year in Jiangsu and Gujarat, highlighting enforcement risks.

Other drivers and restraints analyzed in the detailed report include:

- Pharma and Agrochemical Pipeline Requiring High-Purity Allyl Intermediates

- Digital-Twin Automation Boosting Plant Uptime and Capacity Utilization

- Volatile Propylene and Electricity Prices Squeezing Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Epichlorohydrin captured 89.08% of the 2025 volume. Wind energy, electric vehicles, and electronics consumed the bulk of these volumes even as bio-alternatives began to gain traction. Yet the fastest expansion lay elsewhere: water-treatment chemicals advanced at a 3.59% CAGR through 2031 as utilities complied with stricter micropollutant rules. Pharma-focused allyl amines benefited from the demand for generic antifungal products. Glycidyl ethers and allyl sulfonates with higher pricing remained attractive for plants that could switch between commodity and specialty batches.

Producers reconfigured scheduling so that specialty campaigns followed large epichlorohydrin runs, maximizing uptime without major capital additions. Digital-twin systems allowed a 36-hour changeover to pharmaceutical-grade allyl chloride that met sub-50 ppm chloride limits. This flexibility raised the allyl chloride market share of high-purity output during periods of propylene price spikes, cushioning margins. As bio-epichlorohydrin gained a footprint, the balanced portfolio approach became more critical for asset sustainability.

The Allyl Chloride Market Report is Segmented by Application (Epichlorohydrin, Allyl Amines, Allyl Sulfonates, Glycidyl Ethers, Water Treatment Chemicals, and Other Applications) and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific anchored 52.32% of global volume in 2025, with the region's allyl chloride market size buffered by large wind and electronics sectors, yet substitution pressure rose as imported bio-ECH made inroads. India expanded Gujarat output by 12 kilotons per year in 2025 to back water-borne coatings, and Japan's pharmaceutical-grade exports remained dominant thanks to tight quality systems. South Korea leveraged its propylene surplus to feed Southeast Asian customers.

North America posted the quickest 1.36% CAGR through 2031, reflecting ample shale-based propylene and integrated chlorine capacity on the U.S. Gulf Coast. Rapid wind-farm additions in the Midwest and offshore Atlantic kept epichlorohydrin flows healthy, while Dow's new Alberta bio unit gave buyers the option to lower embodied carbon. Mexico gained from near-shoring dynamics that redirected plastics manufacturing from East Asia into North America.

In Europe, strict emission limits raised operating costs, favoring integrated majors with scale. Germany stayed the largest consumer, but a shift toward certified bio-materials trimmed conventional demand by roughly 3% annually. Eastern Europe, led by Poland and Czechia on infrastructure upgrades that raised resin needs, partially offset Western European contraction.

- AccuStandard

- Aditya Birla Chemicals

- Arkema S.A.

- Befar Group Co., Ltd.

- Dow Inc.

- Gelest Inc.

- INEOS

- Kashima Chemical Co., Ltd.

- Olin Corporation

- OSAKA SODA

- Shandong Jinling Chemical Co.

- SINOPEC Baling Petrochemical Co., Ltd.

- Solvay

- Sumitomo Chemical Co., Ltd.

- Thermo Fisher Scientific Inc.

- Vizag Chemical

- WEGO CHEMICAL GROUP

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging epoxy-resin demand in wind-turbine blades and Electronic Vehicle composites

- 4.2.2 Expansion of industrial water-treatment regulations worldwide

- 4.2.3 Pharma and agrochemical pipeline requiring high-purity allyl intermediates

- 4.2.4 Digital-twin automation boosting plant uptime and capacity utilization

- 4.2.5 On-purpose chlorination revamps enabling small-scale, low-CAPEX plants

- 4.3 Market Restraints

- 4.3.1 Stringent occupational-exposure and emission limits (US/EU/JP)

- 4.3.2 Volatile propylene and electricity prices squeezing margins

- 4.3.3 Bio-ECH scale-up eroding allyl-chloride demand share

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Application

- 5.1.1 Epichlorohydrin

- 5.1.2 Allyl Amines

- 5.1.3 Allyl Sulfonates

- 5.1.4 Glycidyl Ethers

- 5.1.5 Water Treatment Chemicals

- 5.1.6 Other Applications (Adhesives, Perfumes, Pharmaceuticals, etc.)

- 5.2 By Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 France

- 5.2.3.4 Italy

- 5.2.3.5 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle-East and Africa

- 5.2.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 AccuStandard

- 6.4.2 Aditya Birla Chemicals

- 6.4.3 Arkema S.A.

- 6.4.4 Befar Group Co., Ltd.

- 6.4.5 Dow Inc.

- 6.4.6 Gelest Inc.

- 6.4.7 INEOS

- 6.4.8 Kashima Chemical Co., Ltd.

- 6.4.9 Olin Corporation

- 6.4.10 OSAKA SODA

- 6.4.11 Shandong Jinling Chemical Co.

- 6.4.12 SINOPEC Baling Petrochemical Co., Ltd.

- 6.4.13 Solvay

- 6.4.14 Sumitomo Chemical Co., Ltd.

- 6.4.15 Thermo Fisher Scientific Inc.

- 6.4.16 Vizag Chemical

- 6.4.17 WEGO CHEMICAL GROUP

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment