|

시장보고서

상품코드

2044250

영국의 접착제 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United Kingdom Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

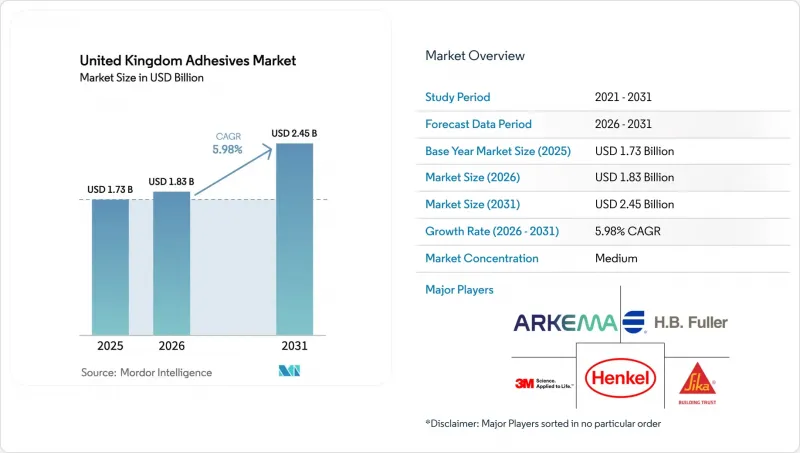

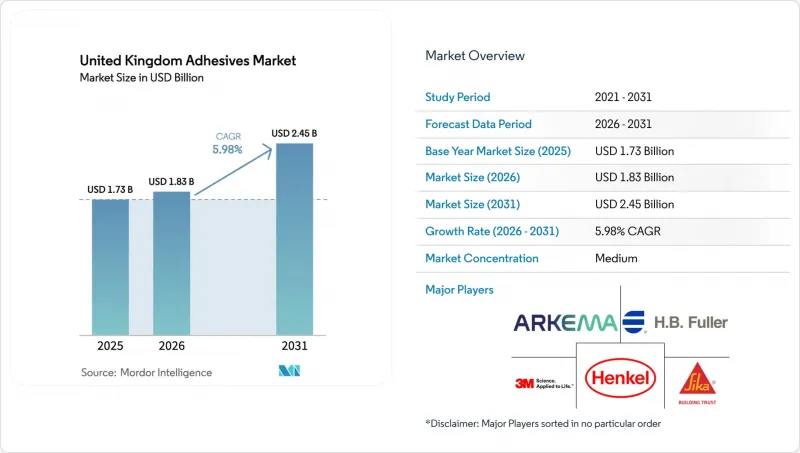

영국의 접착제 시장 규모는 2025년에 17억 3,000만 달러, 2026년에 18억 3,000만 달러가 되어, 2031년까지 24억 5,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 5.98%로 성장할 전망입니다.

EU의 SVHC(고위험물질) 규제 업데이트에 따른 대응, 수성 화학물질의 급속한 보급, 그리고 모빌리티, 건설, 포장 분야에서의 경량 기판의 다용도로 인해 접착제는 단순한 범용 소재에서 성능을 향상시키는 소재로 그 역할을 계속 재정의하고 있습니다. 규제에 영향을 받기 쉬운 용도는 이미 수성 등급이 주류를 이루고 있는 반면, 핫멜트 제품은 60초 미만의 경화 시간을 필요로 하는 전자상거래용 포장 시장을 장악하고 있습니다. 각 공급업체들은 필러의 배합률을 높이는 한편, 원료 가격 변동과 VOC 규제에 대응하기 위해 반응성 시스템이나 바이오 시스템으로 전환을 추진하고 있습니다. 인수 대상 기업이 현지 생산 기지, 기술 서비스 팀, 지역 유통망을 제공함에 따라 세계 대기업 간의 통합이 가속화되고 있습니다.

영국 접착제 시장 동향 및 인사이트

영국 자동차 제조업계의 경량 복합소재 채택 확대

재규어 랜드로버의 630만 파운드(831만 달러) 규모의 'SCALE-UP' 프로그램에서는 복합재 도어와 재생 탄소섬유 휠의 대량 생산이 진행되고 있으며, 서로 다른 기판을 접착하고 배터리 전기자동차의 열 부하를 견딜 수 있는 접착제에 대한 수요가 발생하고 있습니다. 헨켈이 2026년에 체결한 ATP Adhesive Systems 인수 계약으로 Euro 7의 재활용성 목표에 부합하는 저VOC 특수 테이프가 추가되었습니다. SCALE-UP의 디지털 모델링을 통해 접착 라인의 성능 예측이 가능해져 공급업체의 개발 주기가 단축되고 있습니다. 구조용 접합부에는 여전히 폴리우레탄과 에폭시계 화학물질이 주류를 이루고 있지만, 60초 미만의 택트 타임이 요구되는 분야에서는 시아노아크릴레이트와 실란 말단 폴리머의 선택이 점유율을 높이고 있습니다. 복합소재의 채택으로 차량 중량이 35kg 감소할 것으로 예상되며, 기계식 체결구를 대체하는 구조용 접착제에 대한 장기적인 수요는 더욱 증가할 것으로 예측됩니다.

모듈 식 오프 사이트 건설 기술 증가로 접착제 수요가 증가할 것입니다.

Sika의 영국 네트워크는 SikaTack Panel 및 Sikaflex-545와 같은 폴리우레탄 및 하이브리드 시스템을 판매하며, 이를 통해 오프사이트 시공업체에게 기계적 고정 장치를 사용하지 않고도 기밀성이 높고 진동에 강한 접합부를 제공합니다. 공장에서의 관리를 통해 경화시간의 편차를 줄이고, 더 넓은 폭의 롤 형태가 가능하여 폐기물을 약 30% 절감할 수 있습니다. 현재 여러 공급업체에 설치된 전담 MMC 부서는 생산 라인에 대한 통합 지원과 운영자 교육을 제공합니다. SikaForce 시스템으로 리벳을 교체하면 샌드위치 패널의 생산 속도가 30% 향상되는 것으로 보고되고 있습니다. 하이브리드 접착제의 ±25% 변위 허용 능력은 모듈 운송 중 균열을 최소화합니다. 이는 주택 건설업체들이 인력난을 완화하기 위해 조립식화를 추진하고 있는 상황에서 중요한 이점이 될 수 있습니다.

석유화학제품 공급망 혼란에 따른 원자재 가격의 변동

헨켈은 2026년 이소시아네이트, 에폭시, 아크릴 모노머의 원가 상승률을 한 자릿수 초반으로 예상하고 있지만, 일부 원료의 경우 분기별로 15-25%의 현물 가격 변동이 여전히 일반적입니다. 지역 공급의 대부분을 차지하는 중소 배합업체들은 헤지 능력이 부족하여 수익률 하락을 흡수하거나 생산능력 증설을 늦추는 경우가 많습니다. 영국의 REACH 롤링 실행 계획에서 PFAS 및 난연제에 대한 감시가 강화되면서 불확실성이 더욱 커지고 있습니다. 대기업들은 광물성 필러의 배합률을 높이는 방식으로 대응하고 있지만, 점도와 용도의 제약으로 인해 이 전략은 한계가 있습니다. 비용 변동은 결국 선물 구매 레버리지와 세계 공급망을 갖춘 통합형 다국적 기업에게 유리하게 작용합니다.

부문 분석

2025년 기준 영국 접착제 시장 점유율의 43.44%를 수성 제품이 차지하고 있으며, 이러한 우위는 영국의 VOC 규제 강화와 수출업체가 EU의 PPWR 재활용 기준을 충족해야 할 필요성에 의해 더욱 강화될 것으로 예측됩니다. 핫멜트 제품은 시장 규모는 작지만, 자동화된 소포 처리 라인과 종이 완충재 채택이 확대되면서 전자상거래 관련 영국 접착제 시장이 성장함에 따라 CAGR 6.26%를 나타낼 것으로 예측됩니다.

솔벤트 기반 제품들은 컴플라이언스 비용의 상승과 틈새 시장의 축소에도 불구하고, 기질에 깊숙이 침투해야 하는 특정 바닥재와 외장재에 대한 수요는 여전히 존재합니다. 반응성 폴리우레탄 및 에폭시 시스템은 복합재료 및 모듈식 건축물의 구조적 접착에 여전히 필수적인 요소입니다. BASF와 Sika의 경화제 'Baxxodur EC 151'은 VOC 배출량을 90% 감소시켜 저배출형 반응성 등급으로의 전환을 상징하는 제품입니다. UV 경화 제품은 시장 점유율은 작지만, 순간 경화 및 무공해 공장 환경을 실현하기 위해 의료기기 및 전자기기 조립 분야로 확대되고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.11The United Kingdom Adhesives Market size is projected to be USD 1.73 billion in 2025, USD 1.83 billion in 2026, and reach USD 2.45 billion by 2031, growing at a CAGR of 5.98% from 2026 to 2031. Regulatory realignment with EU SVHC updates, rapid uptake of water-borne chemistries, and heavier use of lightweight substrates in mobility, construction, and packaging continue to redefine adhesives from commodity inputs to performance-enabling materials. Water-borne grades already dominate regulatory-sensitive applications, while hot-melt lines capture e-commerce packaging runs that demand sub-60-second set times. Suppliers are improving filler loading and shifting to reactive or bio-based systems to balance raw-material volatility and VOC compliance. Consolidation among global majors is intensifying as acquisition targets supply local production footprints, technical service teams, and regional distribution depth.

United Kingdom Adhesives Market Trends and Insights

Growing Adoption of Lightweight Composites in UK Automotive Manufacturing

Jaguar Land Rover's GBP 6.3 million (USD 8.31 million) SCALE-UP program is scaling composite doors and recycled carbon-fiber wheels, creating demand for adhesives that bond mixed substrates and survive battery-electric vehicle thermal loads. Henkel's 2026 agreement to acquire ATP Adhesive Systems adds low-VOC specialty tapes that align with Euro 7 recyclability goals. Digital modelling within SCALE-UP now predicts bond-line performance, shrinking development cycles for suppliers. Polyurethane and epoxy chemistries still dominate structural joints, but cyanoacrylate and silane-terminated polymer options are gaining share where sub-60-second takt times matter. Composite adoption is forecast to trim vehicle mass by 35 kg, reinforcing long-term pull for structural adhesives over mechanical fasteners.

Increase in Modular Off-Site Construction Techniques Boosting Adhesive Demand

Sika's UK network sells polyurethane and hybrid systems such as SikaTack Panel and Sikaflex-545 that give off-site builders airtight, vibration-tolerant joints without mechanical fixings. Factory controls cut cure-time variance and allow wider roll formats, reducing waste by roughly 30%. Dedicated MMC divisions at several suppliers now offer line-integration support and operator training. Sandwich-panel production speeds reportedly rise 30% when SikaForce systems replace rivets. Hybrid adhesives' +-25% movement capability minimizes cracking during module transport, a key benefit as housebuilders boost prefabrication to ease labor shortages.

Volatility in Raw-Material Prices Linked to Petrochemical Supply-Chain Disruptions

Henkel projects low single-digit cost inflation for isocyanates, epoxies, and acrylic monomers in 2026, yet 15-25% quarterly spot swings remain common for some feedstocks. SME formulators, which dominate local supply, lack hedging power and often absorb margin hits or delay capacity upgrades. PFAS and flame-retardant scrutiny within the UK REACH Rolling Action Plan adds further uncertainty. Larger players are countering by boosting mineral-filler loading, but viscosity and application limits cap this tactic. Cost turbulence ultimately favors integrated multinationals with forward-buying leverage and global supply webs.

Other drivers and restraints analyzed in the detailed report include:

- Rising Use of Bio-Based Adhesive Formulations Driven by UK Sustainability Mandates

- Expansion of E-Commerce Packaging Volumes Requiring High-Performance Adhesives

- Stringent VOC-Emission Limits Under UK REACH Regulations Increasing Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Water-borne chemistries accounted for 43.44% of the United Kingdom adhesives market share in 2025, a lead reinforced by the UK's tighter VOC trajectory and by exporters' need to satisfy EU PPWR recyclability criteria. Hot-melt products, while smaller in base, are on track for a 6.26% CAGR as the UK adhesives market size tied to e-commerce grows in step with automated parcel lines and paper-based void-fill adoption.

Solvent-borne products confront rising compliance costs and shrinking target niches, though they still win select flooring and exterior joinery work that demands deep substrate wetting. Reactive polyurethane and epoxy systems remain indispensable for structural bonding in composites and modular construction; BASF and Sika's Baxxodur EC 151 hardener, with 90% lower VOC release, exemplifies the pivot toward low-emission reactive grades. UV-cure lines, though a small slice, are expanding in medical and electronics assembly for instant curing and zero-emission factory floors.

The United Kingdom Adhesives Market Report is Segmented by Technology (Water-Borne, Solvent-Borne, Reactive, Hot Melt, and UV Cured Adhesives), Resin (Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, Silicone, and Other Resins), and End-User Industry (Building and Construction, Packaging, Automotive, Aerospace, Woodworking and Joinery, Footwear, Healthcare, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- Arkema

- Avery Dennison Corporation

- BASF

- Beardow Adams

- Dow

- Dymax Corporation

- Follmann Chemie GmbH

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Jowat SE

- Momentive Performance Materials

- PARKER HANNIFIN CORP

- Scapa

- Sika AG

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing adoption of lightweight composites in UK automotive manufacturing

- 4.2.2 Increase in modular off-site construction techniques boosting adhesive demand

- 4.2.3 Rising use of bio-based adhesive formulations driven by UK sustainability mandates

- 4.2.4 Expansion of e-commerce packaging volumes requiring high-performance adhesives

- 4.2.5 Surge in niche aerospace MRO activities around UK regional airports

- 4.3 Market Restraints

- 4.3.1 Volatility in raw-material prices linked to petrochemical supply-chain disruptions

- 4.3.2 Stringent VOC-emission limits under UK REACH regulations increasing compliance costs

- 4.3.3 Skills shortage in advanced adhesive-application technicians

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Water-borne

- 5.1.2 Solvent-borne

- 5.1.3 Reactive

- 5.1.4 Hot Melt

- 5.1.5 UV Cured Adhesives

- 5.2 By Resin

- 5.2.1 Polyurethane

- 5.2.2 Epoxy

- 5.2.3 Acrylic

- 5.2.4 Cyanoacrylate

- 5.2.5 VAE/EVA

- 5.2.6 Silicone

- 5.2.7 Other Resins

- 5.3 By End-user Industry

- 5.3.1 Building and Construction

- 5.3.2 Packaging

- 5.3.3 Automotive

- 5.3.4 Aerospace

- 5.3.5 Woodworking and Joinery

- 5.3.6 Footwear

- 5.3.7 Healthcare

- 5.3.8 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Avery Dennison Corporation

- 6.4.4 BASF

- 6.4.5 Beardow Adams

- 6.4.6 Dow

- 6.4.7 Dymax Corporation

- 6.4.8 Follmann Chemie GmbH

- 6.4.9 H.B. Fuller Company

- 6.4.10 Henkel AG & Co. KGaA

- 6.4.11 Huntsman International LLC

- 6.4.12 Jowat SE

- 6.4.13 Momentive Performance Materials

- 6.4.14 PARKER HANNIFIN CORP

- 6.4.15 Scapa

- 6.4.16 Sika AG

- 6.4.17 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment