|

시장보고서

상품코드

2044270

자가치유 코팅 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Self-Healing Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

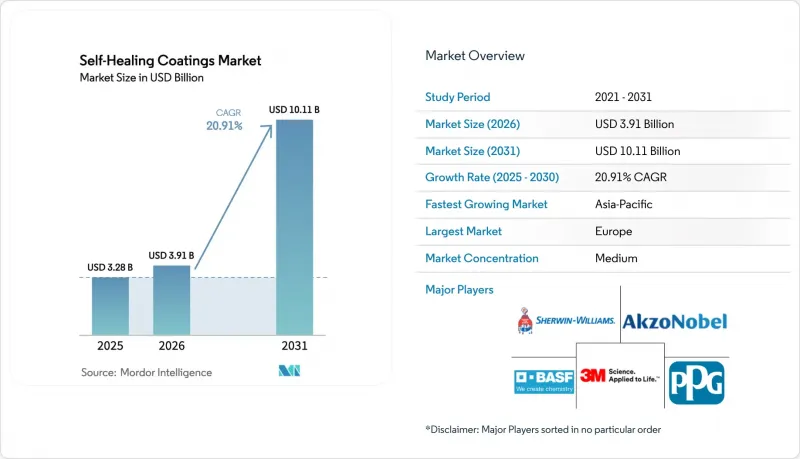

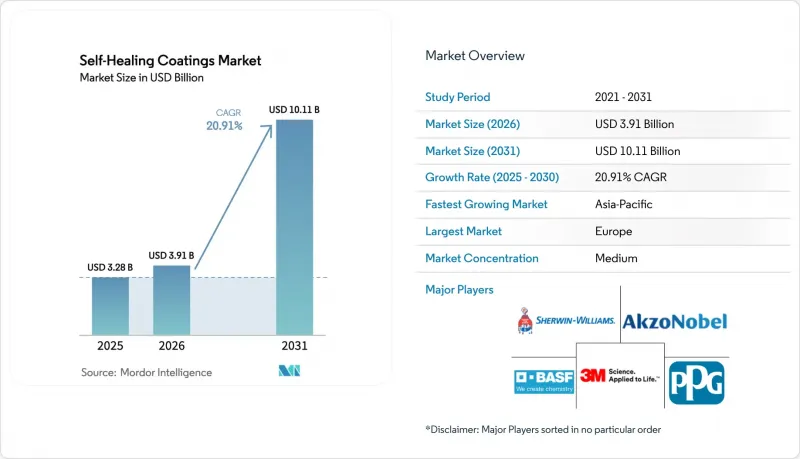

자가치유 코팅 시장 규모는 2025년 32억 8,000만 달러에서 2026년에는 39억 1,000만 달러로 확대되어 2031년까지 101억 1,000만 달러에 이를 것으로 예상되고 있으며 2026-2031년까지 CAGR 20.91%로 성장할 전망입니다.

OEM과 인프라 소유주들은 현재 잦은 재도장 주기보다 장기적인 내구성을 갖춘 재료를 선호하고 있습니다. 이러한 전략적 전환으로 프로젝트 범위가 확대되고 평균 수주액도 증가했습니다. 약간의 공정 조정으로 기존 폴리우레탄 및 에폭시 화학 성분에 원활하게 통합할 수 있는 외재성 캡슐 기술이 매출 점유율을 주도하고 있습니다. 한편, 내재성 가역 결합 시스템은 합성 비용의 감소에 따라 파일럿 규모에서 상업적 생산으로 전환하고 있습니다. 현재 유럽, 북미, 아시아태평양의 건설 기관은 자체 수리 사양에 중점을 둔 입찰을 발행하고 있습니다. 이러한 움직임은 과거 틈새 시장이었던 항공우주 및 전자제품 부문을 넘어 물량 성장의 폭을 넓히고 있습니다. 이와 병행하여, 코팅제 배합 제조업체는 IoT 센서를 내장하여 수리 진행 상황을 실시간으로 모니터링하고 있습니다. 이러한 발전은 새로운 데이터 스트림을 생성할 뿐만 아니라, 조달 주기를 단축하고 프리미엄 가격 책정을 정당화할 수 있도록 돕고 있습니다.

세계 자가치유 코팅 시장 동향 및 인사이트

마이크로 캡슐 기술 스케일업 프로젝트 급증

2025년에는 수 톤 규모의 캡슐 반응 장비가 가동되기 시작하여 단위 비용이 크게 감소하여 자기 수리 코팅의 가격이 프리미엄 에폭시 수지 가격대에 가까워졌습니다. 현재, 평균 직경이 10 마이크로미터 이하인 캡슐을 사용하는 배합 제조업체들은 필름의 헤이즈(김서림) 없이 높은 충진 밀도를 달성하여 자동차 클리어 코트에서 큰 진전을 이루었습니다. 이중 쉘 구조를 채택한 해상풍력발전 타워는 엄격한 염수분무 검사를 통과하여 현장에서의 내구성을 확인했습니다. 표준 스프레이 장치를 사용하여 캡슐을 공동 압출할 수 있어 시공업체는 많은 설비투자를 피할 수 있어 검사 도입으로의 전환이 순조롭게 진행되었습니다. 이러한 발전에 따라 주요 수지 공급업체들은 기존 혼합 라인에 원활하게 통합할 수 있는 캡슐 마스터배치 제품을 도입하여 세계 보급을 더욱 가속화하고 있습니다.

아시아 및 유럽의 노후화된 인프라에 대한 리노베이션 수요 증가

1960년대에 건설된 교량 상판, 터널, 철도 고가교 등 노후화된 인프라를 다루는 공공기관은 현재 자본을 절약하기 위해 전면적인 개보수보다 개보수를 우선시하고 있습니다. 2025년, 호라이즌 유럽은 복원력 프로젝트에 많은 자금을 할당하고, 재도장 간격을 연장하기 위해 자기복구 코팅에 중점을 두었습니다. 중국 교통운수부는 광활한 고속도로 네트워크 전체의 수명주기 비용을 절감하기 위해 미세한 균열을 자율적으로 봉쇄하는 폴리머 오버레이를 도입하고 있습니다. 동시에 인도의 국가 인프라 계획(National Infrastructure Pipeline)은 철도 교량 보수에 많은 자금을 할당하고, 점검 간격을 연장하는 코팅을 채택하고 있습니다. 이상기후로 인한 동결-융해 사이클이 심화됨에 따라 자산 소유주들은 예기치 못한 폐쇄를 방지하기 위한 안전책으로 자가복구 기술을 점점 더 중요하게 여기고 있습니다.

항공우주 공급망에서 인증의 장애물

소규모 혁신 기업들은 새로운 프라이머 프로그램마다 Nadcap 인증 및 MIL-PRF-85285 준수에 따른 추가 비용을 충당하는 데 어려움을 겪고 있습니다. 규제 당국은 아직 수리능력 측정 기준을 표준화하지 않아 용도별로 개별적으로 심사하고 있어 승인까지 시간이 오래 걸리고 있습니다. 배합을 변경하려면 다운스트림 조립품의 재인증이 필요하며, 이미 승인된 코팅이라 하더라도 도입이 지연될 수 있습니다. 산업 단체가 통일된 검사 기준을 마련하기 전까지는 항공우주 분야에서의 채택은 지상 설비나 내장 패널 등 중요도가 낮은 부품에 국한될 것으로 보입니다.

부문 분석

2025년에는 캡슐의 크기와 벽의 무결성을 대규모로 유지하는 엄격한 품질 관리 조치에 힘입어 외재성 시스템이 매출의 68.45%를 차지했습니다. 자가치유 코팅 시장에서 외래성 제품 시장 점유율은 100마이크로미터 이하의 결함에서 80% 이상의 균열을 봉쇄할 수 있는 것으로 입증된 것에 힘입어 성장세를 보이고 있습니다. 내재성 제품은 2026-2031년의 예측 기간 동안 21.17%의 견고한 CAGR을 나타낼 것으로 예측됩니다. 이는 딜스 알더 결합과 수소결합 네트워크가 실험실 환경에서 실용화 단계로 빠르게 전환되고 있는 것이 원동력이 되고 있습니다.

외재성 캡슐은 주로 선박이나 교량 구조물에서 활용되고 있으며, 충격은 빈도는 낮지만 심각한 결과를 초래할 수 있습니다. 반면, 본질적인 화학 반응은 끊임없는 미세한 마모를 견디는 전자기기 케이스에서 우수한 성능을 발휘합니다. 현재 공급망은 두 가지 접근 방식을 통합하여 캡슐을 먼저 터뜨려 밀봉한 후 가역적 결합을 이용하는 하이브리드 배합을 제공합니다. ISO 위원회가 자가복구 검사 방법을 수립하고 있기 때문에 사양 개발자는 보다 명확한 기준의 혜택을 받을 것으로 예상되며, 이로 인해 자가복구 코팅 시장은 다주기 대응의 본질적인 시스템으로 나아갈 가능성이 있습니다.

지역별 분석

유럽에서는 '그린딜'의 자금 지원과 '호라이즌 유럽'의 시범 사업에 힘입어 2025년 매출의 48.91%를 차지해, 유지보수 주기를 20년으로 연장하는 페인트에 대한 수요 증가가 두드러졌습니다. 2024년, 독일은 아우토반 교량 보수에 자금을 할당하고, 자가 수리 프라이머 사용을 의무화했습니다. 영국의 네트워크 레일은 콘크리트 오버레이를 채택하여 선로 폐쇄 시간을 단축하는 데 성공했습니다. 한편, 프랑스는 고속철도 가선 기둥에 폴리우레탄 탑코트를 권장하여 18개월 만에 유지보수 비용을 크게 절감했습니다. 현재 북유럽 국가에서는 동결-해동 사이클 동안 억제제를 방출하는 캡슐 시스템이 사용되고 있습니다. 지중해 연안의 항구에서는 크레인 구조물을 자가 수리 실리콘으로 전환하고 있습니다. 이러한 노력은 이 지역 수요를 지속적으로 견인하고 있습니다.

중국의 일대일로 이니셔티브에 힘입어 아태지역은 2026-2031년의 예측 기간 동안 CAGR 24.64%를 달성할 것으로 예측됩니다. 2025년, 중국은 수천 킬로미터에 달하는 고속도로 입찰에 자가 수리 조항을 포함시켰습니다. 인도 철도 교량 기금은 점검 간격을 연장하는 도료의 도입을 추진하고 있습니다. 일본 국토교통성은 지진이 잦은 교각에 대한 자가복구 보호를 제안하고 있습니다. 한국에서는 스마트시티의 교통 허브에 센서가 부착된 코팅을 내장하고, 유지보수 데이터를 지자체 대시보드에 통합하여 관리하고 있습니다. 이 지역공급업체들은 캡슐 생산 확대, 가격 격차 해소, 현지 도입 가속화를 위해 노력하고 있습니다. 이러한 모멘텀은 아시아 신흥국의 자기복원 코팅 시장을 더욱 확대시킬 것으로 예측됩니다.

북미에서는 미국의 교량 법안이 자기복구 코팅을 적격비용으로 인정하는 것을 배경으로 도입이 급증하고 있습니다. 캐나다에서는 추운 지역용 규격으로 인해 극한의 환경에서도 유연성을 확보할 수 있는 저Tg 폴리우레탄 클리어 코트에 대한 관심이 높아지고 있습니다. 동시에 멕시코의 자동차 산업은 E-코팅 탱크에서 캡슐 프라이머로의 전환이 진행되고 있습니다. 브라질에서는 다운타임 단축을 위해 프리솔트층 해양 시추 시설에서 실리콘계 선체 시스템 검사가 이루어지고 있습니다. 중동에서는 NEOM과 같은 대형 프로젝트에서 모래 폭풍에 의한 마모에 강한 코팅이 선택되고 있습니다. 남아공의 광업에서는 광석 슈트에 자기 경화형 에폭시 수지의 검사가 이루어지고 있습니다. 이러한 다양한 프로젝트로 인해 자가치유 코팅 시장의 지리적 수익 기반이 확대되고 있습니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The Self-Healing Coatings Market size is expected to increase from USD 3.28 billion in 2025 to USD 3.91 billion in 2026 and reach USD 10.11 billion by 2031, growing at a CAGR of 20.91% over 2026-2031. OEMs and infrastructure owners are now prioritizing materials with long-lasting durability over frequent repaint cycles. This strategic pivot has expanded project scopes and boosted average order values. Extrinsic capsule technology, with its seamless integration into existing polyurethane and epoxy chemistries through a minor process tweak, leads in revenue share. Meanwhile, intrinsic reversible-bond systems, as synthesis costs have decreased, have transitioned from pilot scales to commercial production. Construction agencies in Europe, North America, and the Asia-Pacific are now issuing tenders emphasizing self-healing specifications. This push is expanding volume growth beyond the once-niche markets of aerospace and electronics. In tandem, coating formulators are embedding IoT sensors to monitor healing events in real-time. This advancement not only creates new data streams but also quickens procurement cycles and justifies premium pricing.

Global Self-Healing Coatings Market Trends and Insights

Surge in Micro-Capsule Technology Scale-Up Projects

In 2025, operations began for multi-ton capsule reactors, significantly reducing unit costs and bringing healing coatings closer to the price range of premium epoxies. Formulators, now utilizing capsule diameters averaging under 10 µm, achieved a significant advancement in automotive clearcoats by attaining high packing density without any film haze. Offshore wind towers, featuring dual-shell architectures, successfully passed rigorous salt-spray tests, confirming their durability in the field. The ability to co-extrude capsules using standard spray equipment enabled contractors to avoid substantial capital expenditures, smoothing the transition to trial adoption. In response to these advancements, tier-one resin suppliers introduced capsule masterbatch offerings that seamlessly integrate into current mixing lines, further accelerating global adoption.

Increasing Refurbishment Demand from Aging Infrastructure in Asia and Europe

Public agencies, addressing aging infrastructure from the 1960s, such as bridge decks, tunnels, and rail viaducts, are now prioritizing rehabilitation over complete overhauls to conserve capital. In 2025, Horizon Europe allocated a significant amount of funding to resilience projects, emphasizing self-healing coatings to extend recoating intervals. China's transport ministry is implementing polymer overlays that autonomously seal minor cracks, aiming to reduce lifecycle costs across its extensive expressway network. Concurrently, India's National Infrastructure Pipeline has allocated substantial funds for retrofitting railway bridges, incorporating coatings that extend inspection intervals. As extreme weather intensifies freeze-thaw cycles, asset owners increasingly view self-healing technology as a safeguard against unexpected closures.

Qualification Hurdles in Aerospace Supply Chain

Small innovators face challenges in funding the additional costs associated with Nadcap accreditation and MIL-PRF-85285 compliance for each new primer program. Regulators have not yet standardized healing metrics, resulting in tailored reviews for each application and extended approval timelines. A change in formulation requires the recertification of downstream assemblies, delaying the rollout of even previously approved coatings. Until industry consortia establish unified test standards, aerospace adoption will remain limited to non-critical components, such as ground equipment and interior panels.

Other drivers and restraints analyzed in the detailed report include:

- OEM Push for Lifetime Corrosion Warranty in EV Platforms

- Mandatory Anti-Fouling Norms Driving Marine Adoption

- Nanocapsule Raw-Material Toxicity Debates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, extrinsic systems accounted for 68.45% of the revenue, supported by rigorous quality-control measures that maintain capsule size and wall integrity on a large scale. The market share of extrinsic products in the self-healing coatings market is bolstered by their proven ability to seal over 80% of cracks in defects smaller than 100 micrometers. Intrinsic variants are experiencing a robust growth rate of 21.17% CAGR during the forecast period of 2026-2031, driven by the rapid transition of Diels-Alder linkages and hydrogen-bond networks from laboratory settings to practical applications.

Extrinsic capsules are predominantly utilized in marine and bridge structures, where impacts, though infrequent, carry significant consequences. In contrast, intrinsic chemistries excel in electronic housings, which endure constant micro-abrasion. Supply chains are now integrating both approaches, offering hybrid formulations that first seal through capsule rupture and subsequently utilize reversible bonds. With ISO committees developing healing test methods, specifiers are expected to benefit from clearer benchmarks, potentially steering the self-healing coatings market towards multi-cycle intrinsic systems.

The Self-Healing Coatings Market Report is Segmented by Form (Extrinsic and Intrinsic), Material Type (Polymers, Metals and Alloys, Concrete and Cementitious, and Others), End-User Industry (Building and Construction, Automotive, Aerospace, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe, buoyed by Green Deal funding and Horizon Europe pilots, commanded 48.91% of 2025 revenue, underscoring a push for coatings that extend maintenance intervals to 20 years. In 2024, Germany allocated funds for retrofitting Autobahn bridges, mandating self-healing primers. The United Kingdom's Network Rail adopted concrete overlays, successfully reducing track-closure hours. France, meanwhile, endorsed polyurethane topcoats for high-speed catenary masts, slashing maintenance costs within 18 months. Nordic nations are now utilizing capsule systems that release inhibitors during freeze-thaw cycles. Mediterranean ports are transitioning crane structures to self-repairing silicone. These initiatives are consistently driving demand in the region.

Asia-Pacific, led by China's Belt and Road Initiative, is on track for a 24.64% CAGR through the forecast period of 2026-2031. In 2025, China integrated self-healing clauses into expressway tenders covering thousands of kilometers. India's railway-bridge fund is pushing for coatings that prolong inspection intervals. Japan's transport ministry is advocating self-healing protection for quake-prone piers. South Korea is embedding sensor-equipped coatings in smart-city transit hubs, funneling maintenance data into municipal dashboards. Suppliers across the region are boosting capsule production, addressing price disparities, and accelerating local adoption. This momentum is set to elevate the self-healing coatings market in emerging Asian nations.

North America is witnessing a surge in adoption, driven by the United States bridge bill, which recognizes self-healing coatings as an eligible expense. In Canada, cold-weather standards are sparking interest in low-Tg polyurethane clears, ensuring flexibility in frigid conditions. Concurrently, Mexico's automotive sector is shifting from e-coat tanks to capsule primers. Brazil is trialing silicone-based hull systems on pre-salt offshore rigs, targeting reduced downtime. In the Middle-East, mega-projects like NEOM are selecting coatings resistant to sandstorm abrasion. South Africa's mining industry is testing intrinsic epoxies on ore chutes. These varied projects are expanding the geographic revenue landscape of the self-healing coatings market.

List of Companies Covered in this Report:

- 3M

- Akzo Nobel N.V.

- Autonomic Materials

- Axalta Coating Systems, LLC

- BASF

- Covestro AG

- Denso

- FEYNLAB INC.

- GVD Corporation

- NEI Corporation

- PPG Industries Inc.

- Revivify Coatings of America

- spotLESS Materials Inc.

- The Sherwin-Williams Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Micro-Capsule Technology Scale-Up Projects

- 4.2.2 Increasing Refurbishment Demand from Aging Infrastructure in Asia and Europe

- 4.2.3 OEM Push for Lifetime Corrosion Warranty in EV Platforms

- 4.2.4 Mandatory Anti-Fouling Norms Driving Marine Adoption

- 4.2.5 AI-Enabled In-Situ Coating Health Monitoring: Unlocking Service Models

- 4.3 Market Restraints

- 4.3.1 High price premium vs. legacy coatings

- 4.3.2 Qualification hurdles in aerospace supply chain

- 4.3.3 Nanocapsule raw-material toxicity debates

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Form

- 5.1.1 Extrinsic

- 5.1.2 Intrinsic

- 5.2 By Material Type

- 5.2.1 Polymers

- 5.2.2 Metals and Alloys

- 5.2.3 Concrete and Cementitious

- 5.2.4 Ceramics and Glass

- 5.3 By End-user Industry

- 5.3.1 Building and Construction

- 5.3.2 Automotive

- 5.3.3 Aerospace

- 5.3.4 Electrical and Electronics

- 5.3.5 Other End-user Industries (Marine, Medical Devices, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 Indonesia

- 5.4.1.6 Vietnam

- 5.4.1.7 Malaysia

- 5.4.1.8 Thailand

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordic Countries

- 5.4.3.7 Russia

- 5.4.3.8 Turkey

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 Egypt

- 5.4.5.5 South Africa

- 5.4.5.6 Nigeria

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 Autonomic Materials

- 6.4.4 Axalta Coating Systems, LLC

- 6.4.5 BASF

- 6.4.6 Covestro AG

- 6.4.7 Denso

- 6.4.8 FEYNLAB INC.

- 6.4.9 GVD Corporation

- 6.4.10 NEI Corporation

- 6.4.11 PPG Industries Inc.

- 6.4.12 Revivify Coatings of America

- 6.4.13 spotLESS Materials Inc.

- 6.4.14 The Sherwin-Williams Company

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 AI-enabled in-situ coating health monitoring