|

시장보고서

상품코드

2061621

항공기 엔진 블레이드 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Aircraft Engine Blades - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

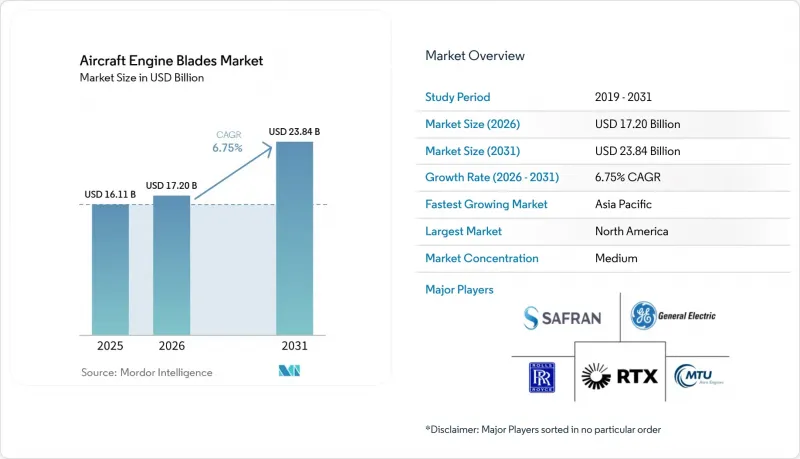

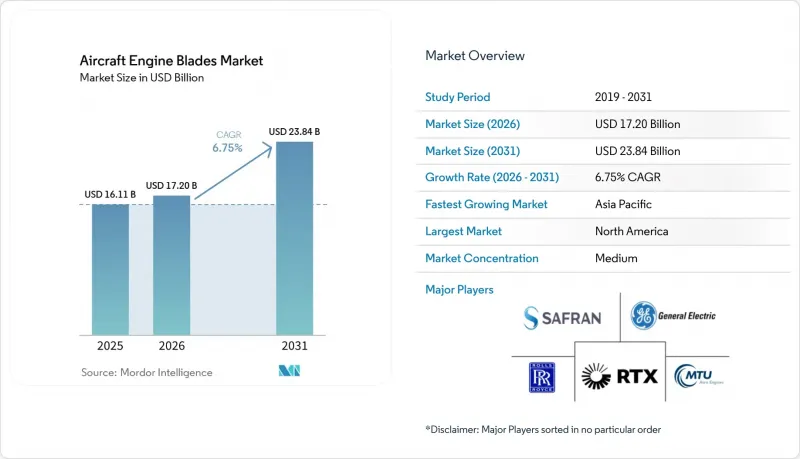

Mordor Intelligence에 의하면, 항공기 엔진 블레이드 시장 규모는 2025년 161억 1,000만 달러로 평가되었습니다. 2026년에는 172억 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR은 6.75%를 나타내, 2031년까지 238억 4,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 소재(티타늄 합금, 니켈 기 초합금, 복합재료, 기타), 블레이드 유형(압축기 블레이드, 터빈 블레이드, 팬 블레이드), 엔진 유형(피스톤, 터보팬, 터보프롭, 터보제트, 터보샤프트), 항공기 유형(민간 항공, 군용 항공 등), 지역(북미, 유럽 등)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

세계의 항공기 엔진 블레이드 시장 동향 및 분석

전 세계 항공기 인도 대수 증가와 기체 수의 확대가 엔진 블레이드 수요를 견인하고 있습니다.

에어버스는 2025년에 793대의 민간 항공기를 인도했으며, 2026년에는 생산량이 증가할 것으로 전망하고 있습니다. 한편, 보잉은 2025년에 600대를 납품했으며, 수주 잔고가 견조한 가운데 생산 일정이 차츰 채워짐에 따라 엔진 조립 라인이 늘어나면서 블레이드 수요도 증가할 것으로 보입니다. 나로우바디 항공기에 대한 집중이 이러한 수요의 조짐을 더욱 뚜렷하게 만들고 있습니다. 왜냐하면, 생산성이 높은 각 엔진 라인에서는 제조 공정 전반에 걸쳐 대량의 압축기 및 터빈용 블레이드가 필요하기 때문입니다. LEAP 엔진 제품군의 엔진 세트에는 각 단계마다 다수의 블레이드가 포함되어 있어, 엔진 생산량의 사소한 월별 변동도 에어포일 수요의 큰 변동으로 이어지며, 이는 항공우주 공급망 내 공급업체의 가동 및 계획에 영향을 미치고 있습니다. 지역적 동향으로 볼 때, 에어버스의 단일 통로기 수주 잔고에서 A321이 주류 기종이 됨에 따라 수요의 중심이 아시아로 이동하고 있습니다. 또한, 인도로부터 수년에 걸쳐 이어진 수주 흐름에 따라 엔진 및 블레이드의 생산 능력이 요구되고 있으며, 이는 현지화되거나 견고한 국경 간 물류 시스템에 의해 뒷받침되어야 합니다. FAA 및 EASA의 내공성 지침 역시 운용 중인 기체군의 교체 주기를 규정하고 있으며, 제안된 FAA AD 2025-0341은 규격에 부합하지 않는 기공률로 제조된 고압 터빈 블레이드를 다루고, 주기 제한 범위 내에서의 구체적인 교체 조치를 정하고 있습니다.

연비 효율이 뛰어난 차세대 터보팬 엔진에 대한 수요 증가

각 항공사가 협폭기 및 광폭기의 연료 소비량을 두 자릿수 수준으로 줄이는 방향으로 나아가고 있는 가운데, 최신 엔진 플랫폼에 대한 확고한 의지로 인해 향후 수십 년에 걸친 블레이드 수요가 점차 확정되고 있습니다. 아메리칸 항공과 페가수스 항공의 최근 결정은 에어버스와 보잉의 전체 협폭기 기단에서 LEAP 엔진의 지속적인 채택을 여실히 보여주고 있으며, 이는 생산 주기와 정비 업무를 통해 압축기 및 터빈 블레이드에 대한 안정적인 수요를 견인하고 있습니다. 가혹한 노선에서의 운용 실적을 바탕으로 블레이드 설계 및 내구성 개선이 중점적으로 추진되고 있으며, CFM사는 LEAP 각 기종의 ‘타임 온 윙(TOW)’ 프로파일을 안정화하기 위해 개량형 고압 터빈 블레이드 형상 및 관련 시스템 개발을 진행하고 있습니다. 또한, 첨단 소재 역시 시험기에서 실기 단계로 넘어가고 있으며, GE9X용으로 검증된 3D 프린팅 세라믹 매트릭스 복합재 부품은 차세대 와이드바디 항공기와 함께 운항할 준비가 완료되었습니다. 이러한 기술적 혁신은 연료 소비량과 배기가스 감축 목표를 뒷받침하고 있습니다. 그러나 한편으로는 이러한 요인들이 수리 및 정밀 점검 시 블레이드의 복잡성을 가중시켜 MRO(정비·수리·정밀 점검) 업체의 폐기율, 부품 조달 가능성 및 비용 구조에 영향을 미치고 있습니다.

초합금 및 세라믹 매트릭스 복합재의 높은 비용과 제조의 복잡성

첨단 합금이나 복합재료는 높은 투입 에너지와 제조 비용이 수반되는데, 이로 인해 블레이드 가격이 높은 수준을 유지하고 있으며, 생산 확대 시 수율 향상을 저해하고 있습니다. 정비의 경제성은 자재 비용에 매우 민감하며, 조사에 따르면 정비 공장에 입고되는 비용의 대부분은 수명 제한이 있는 터빈 부품을 포함한 교체 부품과 관련되어 있어, 이는 대규모 정비 주기에서 예산 부담을 가중시키고 있습니다. 니켈 합금 시장은 관세 조치나 업계 고유 수요 등 정책과 수요의 상호작용에 영향을 받고 있으며, 이는 항공우주 등급 소재의 변동 비용 추이에 영향을 미치고 있습니다. 항공사들도 2025년에는 공급망 제약으로 인해 광범위한 비용 상승 압박에 직면했습니다. 유지보수, 리스, 재고 관리에 드는 비용이 업계 경비에 수십억 달러를 추가로 부담시키고 있으며, 그 결과 블레이드와 같은 중요 부품에 대한 보수적인 조달 및 재고 관리 태도가 간접적으로 강화되고 있습니다. OEM을 통한 생산 능력 및 첨단 공장에 대한 투자는 이러한 압박에 대응하기 위해 마련된 것입니다. 예를 들어, 유럽의 티타늄 압축기 블레이드 생산 라인에서는 높은 처리량을 자랑하는 디지털 생산 기술을 적용하여 대량 생산되는 좁은 동체용 엔진공급을 안정화하고 있습니다.

부문별 분석

2025년, 항공기 엔진 블레이드 시장에서 티타늄 합금은 38.76%를 차지했습니다. 이는 해당 소재의 강도 대 중량 비율, 내식성 및 내열성이 주요 엔진 계열 전반에 걸쳐 압축기 단과 특정 터빈 부위 모두를 뒷받침했기 때문입니다. 복합재료를 활용한 항공기 엔진 블레이드 시장은 터빈 입구 온도의 상승 추세와, 승인된 용도에서 엔진 효율을 높이고 냉각 공기 요구량을 줄이는 세라믹 매트릭스 복합재 설계의 도입에 힘입어 2031년까지 연평균 성장률(CAGR) 9.43%로 확대될 것으로 전망됩니다. 업스트림 공정에서의 스폰지 티타늄 생산 능력 집중과 공급량에 영향을 미치는 각국의 정책 조치로 인해, 티타늄 공급의 안정성은 블레이드 제조업체에게 여전히 중요한 과제로 남아 있습니다. 이에 따라 주요 OEM 및 1차 공급업체들은 장기 계약을 체결하고, 인증상의 제약 범위 내에서 가능한 한 공급처 다각화를 도모하고 있습니다. 기술적인 측면에서 고온부 부품용 적층 가공 공정은 중요한 전환점을 맞이했습니다. GE9X의 인증된 3D 프린팅 CMC 구조체는 기존 제조 방식으로는 구현하기 어려웠던 첨단 설계의 실현 가능성을 입증하고 있습니다. 이러한 변화로 인해, 티타늄이 압축기 블레이드의 대량 생산 기반으로서의 위치를 유지하는 한편, 복합재료는 열적·환경적 차단 요건으로 인해 높은 초기 비용이 정당화되는 특정 역할로 그 적용 범위가 확대되면서, 균형 잡힌 제품 포트폴리오가 형성되고 있습니다.

각 OEM 업체들의 고생산성 티타늄 압축기 블레이드 제조 시설에 대한 투자는 LEAP 및 유사 프로그램의 단기 생산 능력 리스크를 줄이는 것을 목표로 하고 있습니다. 한편, 복합재료의 채택 확대는 가혹한 운용 환경 하에서의 검사 기준 표준화와 수명 주기 검증의 지속적인 발전에 달려 있습니다. 항공기 엔진 블레이드 업계에서는 복합재 구조의 불균일성을 관리하기 위해 디지털 검사 및 수리 계획의 도입이 확대되고 있으며, 이를 통해 현장에서의 성능과 설계 개선 간의 피드백 루프가 강화되고 있습니다. 이 모든 요소를 종합해 보면, 대량 생산되는 압축기 용도에서는 재료 구성의 기반이 여전히 티타늄이 담당하는 한편, 온도, 질량, 냉각 간의 상충 관계에서 승인된 비파괴 검사 및 견고한 수리 체계에 뒷받침된 고부가가치 블레이드 형상이 유리한 분야에서는 복합재료의 성장이 가장 빠르게 진행될 것으로 전망됩니다.

2025년 기준으로, 압축기 블레이드는 항공기 엔진 블레이드 시장의 42.32%를 차지했으며, 이는 다단 코어 전체의 높은 생산량과 현대 축류 설계에서 중량 및 효율성에 중점을 두고 있음을 반영합니다. 터빈 블레이드는 온도 여유폭 확대 및 가혹한 운용 조건에서의 초기 마모에 대응하기 위한 내구성 향상 기술이 항공기 기종에 도입됨에 따라, 2031년까지 연평균 성장률(CAGR) 7.21%라는 가장 높은 성장률을 기록하며 확대될 것으로 전망됩니다. 나로우드바디 항공기의 규모 확대가 압축기 블레이드의 대규모 및 지속적인 수주를 이끌고 있습니다. 한편, 고압 터빈 블레이드는 단결정이나 첨단 합금의 사용, 그리고 MRO 주기 내 수리의 복잡성으로 인해 단위당 가치가 높습니다. 차세대 엔진의 첫 번째 정비 작업이 2020년대 중반에 집중되어 있어, 성능을 저하시키지 않으면서 비행 가능 기간을 연장하기 위한 터빈 블레이드 교체 및 설계 개선에 대한 수요가 높아지고 있습니다. 이미 현장에서 사용되고 있는 OEM 업그레이드 키트는 이러한 추세를 뒷받침하고 있으며, 기체의 정기 및 비정기 정비에 맞추어 개량된 고압 터빈 부품을 도입할 수 있도록 그 규모가 확대되고 있습니다.

팬 블레이드는 구조적 크기와 공기역학적 하중으로 인해 여전히 혁신이 활발히 이루어지는 분야입니다. 그러나 대형 복합재 설계에 대한 검사 및 인증 체계가 여전히 교체 방침과 정비 주기를 좌우하고 있기 때문에 그 성장 궤도는 더욱 안정적입니다. 엔진 프로그램에서는 고압 터빈 단의 초기 수명 연장이 가능함이 입증되었으며, 경우에 따라 비행 시간의 2배 이상을 달성하여 개조 주기 완료 후의 교체 빈도를 줄이고 있습니다. 그 결과, 압축기 블레이드는 수요 피라미드의 기반을 지탱하고, 터빈 블레이드는 성장률과 부가가치 측면에서 주도적인 역할을 수행하며, 팬 블레이드는 대형 복합재 구조물에 대한 비파괴 검사(NDE), 수리 및 인증 체계가 보다 광범위한 표준화를 향해 지속적으로 정비되는 가운데, 다소 완만한 속도로 발전하고 있습니다.

지역별 분석

2025년, 북미는 항공기 엔진 블레이드 시장에서 33.24%라는 최대 점유율을 차지했습니다. 이는 엔진 OEM의 집중, 탄탄한 MRO 인프라, 그리고 신규 생산 및 애프터마켓 채널 전반에 걸쳐 블레이드 수요를 뒷받침하는 강력한 방산 조달을 반영한 것입니다. 2025년에 발표된 미국의 투자는 장기간에 걸쳐 고도의 날개 형상이 필요한 프로그램을 지원하기 위해 제조 능력 확충과 내구성 기술 향상을 목표로 했습니다. 전략적 금속 공급 계약 또한 향후 10년 동안 해당 지역의 협폭기 및 광폭기 블레이드 수요를 충족할 수 있는 기반을 마련해 주었습니다. 업스트림 및 중견 공급업체들은 회전 부품의 기계 가공, 코팅, 검사 분야의 역량 개발을 지속적으로 추진하고 있으며, 이를 통해 고신뢰성 블레이드의 생산 및 수리에 대한 지역 내 회복탄력성을 강화하고 있습니다. 유지보수 측면에서 볼 때, 예측 분석은 미국의 항공사 및 MRO 업체들 사이에서 널리 보급되어 있으며, 데이터 품질과 점검 체계의 성숙도가 엔진 건전성 모니터링 목표와 부합할 경우 블레이드의 수명 연장에 기여하고 있습니다.

아시아태평양은 항공기 엔진 블레이드 시장에서 가장 빠르게 성장하고 있는 지역으로, 2031년까지 연평균 성장률(CAGR)이 8.09%를 나타낼 것으로 전망됩니다. 이는 항공기 대수 증가와, 압축기 및 터빈 에어포일의 생산 능력을 견인하는 장기적인 협폭기 수주 파이프라인에 힘입은 결과입니다. 중국의 제조 생태계는 확대되고 있지만, 여전히 주기적인 부품 부족에 직면하고 있어, 신규 프로그램을 위한 블레이드 공급량을 늘리기 위해서는 여러 국가에 걸친 공급 전략이 중요하다는 점을 여실히 보여주고 있습니다. 인도에서는 항공기 보유 대수와 정비 역량의 장기적인 성장이 신규 블레이드 및 MRO용 예비 부품에 대한 다년간 수요를 뒷받침하고 있으며, 인증 및 금형 기술이 성숙함에 따라 파트너 주도형 현지화가 더욱 가속화될 것으로 예측됩니다. 해당 지역의 생산량 확대는 특수 가스 및 합금 원료 확보, 검사 기술 인증, 그리고 정교한 블레이드 형상에서 안정적인 수율을 확보하기 위한 숙련된 인력 확충에 달려 있습니다. 기체 수가 증가하고 데이터 인프라 및 인증 검사 도구의 보급이 확대됨에 따라, 아시아태평양의 정비 활동도 고부가가치 기종에 대해서는 정기 점검 방식에서 상태 기반 판단 방식으로 전환될 것입니다.

유럽에서는 지속가능성과 효율성 목표를 뒷받침하기 위해 차세대 블레이드 제조 및 소재 연구가 지속적으로 진행되고 있으며, LEAP 생산을 지원할 새로운 고생산성 압축기 블레이드 시설이 2025년에 가동을 시작했습니다. 이 지역의 엔진 및 기체 OEM 업체들은 고온 부위용 열 관리, 코팅, 복합재 구조에 투자하고 있으며, 프로그램이 성숙해짐에 따라 블레이드의 구성 비율에 영향을 미치게 될 것입니다. 중동 및 아프리카에서는 고부가가치 와이드바디 및 나로우바디용 엔진에 대한 수요가 꾸준히 이어지고 있으며, 해당 지역의 피드백을 반영하여 개발된 내구성 기술이 모래먼지나 모래가 유입되는 환경에서의 설계 개선에 활용되고 있습니다. 남미에서는 민간 항공 운항과 지역별 MRO(정비·수리·오버홀) 사업의 성장을 중심으로, 규모는 작지만 안정적인 블레이드 수요가 나타나고 있습니다. 이는 전 세계 공급업체와의 파트너십과 표준화된 정비 프로토콜에 의해 뒷받침되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the aircraft engine blades market size is expected to grow from USD 16.11 billion in 2025 to USD 17.20 billion in 2026 and is forecast to reach USD 23.84 billion by 2031 at a 6.75% CAGR over 2026-2031.

This report is Segmented by Material (Titanium Alloys, Nickel-Based Superalloys, Composites, and Others), Blade Type (Compressor Blades, Turbine Blades, and Fan Blades), Engine Type (Piston, Turbofan, Turboprop, Turbojet, and Turboshaft), Aircraft Type (Commercial Aviation, Military Aviation, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Aircraft Engine Blades Market Trends and Insights

Rising Global Aircraft Deliveries And Fleet Expansion Driving Engine Blade Demand

Airbus reported 793 commercial aircraft deliveries in 2025 and guided higher output in 2026, while Boeing delivered 600 aircraft in 2025, suggesting blade demand will track the upward slope of assembly lines as slots are filled amid strong order backlogs. Narrowbody concentration amplifies this demand signal because each high-rate engine line draws substantial volumes of compressor and turbine airfoils throughout the build process. The LEAP family's shipset, with numerous blades across stages, translates minor monthly changes in engine production into significant variations in airfoil demand, impacting supplier operations and planning in the aerospace supply chain. Regional dynamics are shifting load toward Asia, as the A321 has become the dominant variant in Airbus's single-aisle backlog and India's multi-year order flow demands engine and blade capacity that must be localized or supported via resilient transnational logistics. FAA and EASA airworthiness directives also frame replacement cycles for in-service fleets, with proposed FAA AD 2025-0341 addressing high-pressure turbine blades produced with non-compliant porosity and defining specific replacement actions within cycle limits.

Increasing Demand For Fuel-Efficient Next-Generation Turbofan Engines

Commitments to the newest engine platforms are locking in multi-decade blade demand as airlines move to reduce fuel burn by double digits on narrowbody and widebody missions. Recent selections by American Airlines and Pegasus highlight sustained LEAP engine adoption across Airbus and Boeing narrowbody fleets, driving consistent demand for compressor and turbine blades throughout production cycles and maintenance operations. In-service experience on harsh routes has prompted targeted blade design and durability improvements, with CFM advancing upgraded high-pressure turbine airfoils and associated systems to stabilize time-on-wing profiles for LEAP variants. Advanced materials are also moving from test cells to fleets, with 3D-printed ceramic-matrix composite components validated for the GE9X, poised for entry into service alongside new-generation widebodies. These technological shifts support lower fuel consumption and emissions targets. Still, they also increase blade complexity in repair and overhaul, which influences scrap rates, parts availability, and cost structures at MROs.

High Cost And Manufacturing Complexity Of Superalloys And Ceramic Matrix Composites

Advanced alloys and composites carry high embedded energy and process costs, which keep blade pricing elevated and constrain yield during production ramp-ups. Overhaul economics are highly sensitive to material costs, and research shows that the majority of shop visit expense is tied to replacement parts, including life-limited turbine components, which intensifies budget pressure during heavy maintenance cycles. Nickel alloy markets face intersecting policy and demand effects, including tariff actions and sector-specific needs, which translate into variable cost trajectories for aerospace-grade material. Airlines also faced broader cost headwinds in 2025 due to supply chain constraints, with maintenance, leasing, and inventory burdens adding billions to sector expenses, thereby indirectly reinforcing conservative procurement and stocking stances for critical parts like blades. OEM investments in capacity and advanced factories are designed to counter these pressures, as seen with European titanium compressor blade lines that apply high-throughput digital production techniques to stabilize supply for high-volume narrowbody engines.

Other drivers and restraints analyzed in the detailed report include:

- Military Modernization Programs Accelerating Turbine Blade Procurement

- Shorter Aftermarket MRO Cycles Increasing Blade Replacement Demand

- Lengthy Certification And Quality Assurance Timelines For Advanced Blade Technologies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Titanium alloys accounted for 38.76% of the aircraft engine blades market in 2025, as the material's strength-to-weight ratio, corrosion resistance, and temperature capability supported both compressor stages and selected turbine locations across major engine families. The aircraft engine blades market for composites is projected to expand at a 9.43% CAGR to 2031, driven by the shift toward higher turbine inlet temperatures and the adoption of ceramic-matrix composite designs that improve engine efficiency and reduce cooling air requirements in approved applications. Titanium supply security remains a central theme for blade producers due to concentration in upstream sponge capacity and national policy actions that influence availability, leading OEMs and Tier 1s to secure long-term agreements and, where practical, diversify sources within certification constraints- on the technology front, additive processes for hot-section components reached significant milestones, with certified 3D-printed CMC structures on the GE9X demonstrating the viability of advanced designs that would be difficult to achieve through conventional routes. These shifts are shaping a balanced portfolio in which titanium continues to anchor high-volume compressor blade production. At the same time, composites expand into defined roles where thermal and environmental barrier requirements justify higher initial costs.

OEM investments in high-rate titanium compressor blade facilities are designed to de-risk near-term capacity for LEAP and similar programs. At the same time, composite content growth depends on continued progress in inspection standardization and lifecycle validation in harsh operating environments. The aircraft engine blades industry is also driving digital inspection and repair planning to manage heterogeneity in composite structures, which tightens feedback loops between field performance and design updates. Taken together, the material mix will likely remain anchored by titanium for volume compressor applications, with composites growing fastest where temperature, mass, and cooling tradeoffs favor higher-value airfoils supported by approved non-destructive evaluation and robust repair schemes.

Compressor blades held 42.32% of the aircraft engine blades market in 2025, reflecting their high unit volumes across multi-stage cores and the emphasis on weight and efficiency in modern axial designs. Turbine blades are projected to grow at the fastest 7.21% CAGR through 2031 as temperature margins rise and fleets incorporate durability upgrades to address early-life wear in challenging operating conditions. Narrowbody scale drives large, recurring orders for compressor airfoils. At the same time, high-pressure turbine blades command a higher value per unit due to their single-crystal or advanced-alloy content and the repair complexity they entail during MRO cycles. First restoration visits for new-generation engines are clustering in the middle of the decade, intensifying the need for turbine blade replacements and updated designs that improve time-on-wing without compromising performance. OEM upgrade kits already in the field confirm this trend and have been scaled to bring improved high-pressure turbine parts into service as fleets move through planned and unplanned removals.

Fan blades remain a visible area of innovation due to structural size and aerodynamic loading. Yet, their growth trajectory is steadier because inspection and certification maturity for large composite designs still shape replacement policies and service intervals. Engine programs have demonstrated that early-life durability improvements for high-pressure turbine stages are achievable, with some cases showing more than a doubling of time-on-wing, thereby reducing replacement frequency after retrofit cycles are complete. As a result, compressor blades anchor the base of the volume pyramid, turbine blades lead in growth and value intensity, and fan blades advance more gradually as NDE, repair, and certification frameworks for large composite structures continue to train toward broader standardization.

Geography Analysis

North America held the largest share at 33.24% of the aircraft engine blades market in 2025, reflecting the concentration of engine OEMs, deep MRO infrastructure, and strong defense procurement that sustain blade demand across new-production and aftermarket channels. US investments announced in 2025 targeted additional manufacturing capacity and durability technologies to support programs that will require advanced airfoils over long service lives. Strategic metals supply agreements also underpinned the region's readiness to meet narrowbody and widebody blade needs through the decade. Upstream and midsize suppliers continue to develop capabilities in machining, coating, and inspecting rotating parts, thereby enhancing regional resilience for high-integrity blade production and repair. From a maintenance perspective, predictive analytics are spreading among US operators and MROs, helping extend blade life when data quality and inspection maturity align with engine health-monitoring goals.

Asia-Pacific is the fastest-growing region, with an 8.09% CAGR through 2031, for the aircraft engine blades market, driven by rising fleet counts and long-dated narrowbody order pipelines that pull on both compressor and turbine airfoil capacity. China's manufacturing ecosystem is expanding but still faces periodic component constraints, underscoring the importance of multi-country supply strategies for scaling blade availability for emergent programs. India's long-term growth in aircraft count and maintenance capabilities supports multi-year demand for new blades and MRO spares, with partner-driven localization expected to gain momentum as certifications and tooling mature. The region's path to higher output depends on securing specialty gases and alloy inputs, qualifying inspection technologies, and scaling trained labor to ensure reliable yields on demanding blade geometries. As fleets grow, Asia-Pacific maintenance activity will also shift from interval-based methods to condition-based decisions for high-value airfoils, as data infrastructure and certified inspection tools become more widely available.

Europe continues to advance next-generation blade manufacturing and materials research in support of sustainability and efficiency targets, with new high-rate compressor blade facilities inaugurated in 2025 to support LEAP production. The region's engine and airframe OEMs are investing in thermal management, coatings, and composite structures for hot sections, which will influence blade mix as programs mature. The Middle East and Africa add a stable stream of high-value widebody and narrowbody engine requirements, and durability technologies developed with regional feedback loops are feeding into design refinements for dust- and sand-ingestion environments. South America maintains a smaller but steady profile in blade demand centered on commercial operations and regional MRO growth, which benefits from global supplier partnerships and standardized maintenance protocols.

- General Electric Company

- Rolls-Royce Holdings plc

- RTX Corporation

- Safran SA

- MTU Aero Engines AG

- IHI Corporation

- CFM International

- GKN Aerospace Services Limited

- Chromalloy Gas Turbine LLC

- TURBOCAM, INC.

- Hi-Tek Manufacturing, Inc.

- Moeller Mfg. Company, LLC

- C Blade S.p.A. Forging & Manufacturing

- Precision Castparts Corp.

- Howmet Aerospace Inc.

- Doncasters Group

- AeroEdge Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising global aircraft deliveries and fleet expansion driving engine blade demand

- 4.2.2 Increasing demand for fuel-efficient next-generation turbofan engines

- 4.2.3 Military modernization programs accelerating turbine blade procurement

- 4.2.4 Shorter aftermarket MRO cycles increasing blade replacement demand

- 4.2.5 Integration of smart sensor-enabled blades supporting predictive maintenance

- 4.2.6 Additive manufacturing-enabled circular titanium feedstock improving material sustainability

- 4.3 Market Restraints

- 4.3.1 High cost and manufacturing complexity of superalloys and ceramic matrix composites

- 4.3.2 Lengthy certification and quality assurance timelines for advanced blade technologies

- 4.3.3 Supply chain fragility for argon and helium used in single-crystal casting

- 4.3.4 Limited non-destructive inspection standards for large composite fan blades

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Titanium Alloys

- 5.1.2 Nickel-Based Superalloys

- 5.1.3 Composites

- 5.1.4 Others

- 5.2 By Blade Type

- 5.2.1 Compressor Blades

- 5.2.2 Turbine Blades

- 5.2.3 Fan Blades

- 5.3 By Engine Type

- 5.3.1 Piston

- 5.3.2 Turbofan

- 5.3.3 Turboprop

- 5.3.4 Turbojet

- 5.3.5 Turboshaft

- 5.4 By Aircraft Type

- 5.4.1 Commercial Aviation

- 5.4.1.1 Narrowbody Aircraft

- 5.4.1.2 Widebody Aircraft

- 5.4.1.3 Regional Jets

- 5.4.2 Military Aviation

- 5.4.2.1 Combat Aircraft

- 5.4.2.2 Non-combat Aircraft

- 5.4.3 General Aviation

- 5.4.3.1 Business Jets

- 5.4.3.2 Helicopters

- 5.4.3.3 Turboprop Aircraft

- 5.4.3.4 Piston Engine Aircraft

- 5.4.1 Commercial Aviation

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 General Electric Company

- 6.4.2 Rolls-Royce Holdings plc

- 6.4.3 RTX Corporation

- 6.4.4 Safran SA

- 6.4.5 MTU Aero Engines AG

- 6.4.6 IHI Corporation

- 6.4.7 CFM International

- 6.4.8 GKN Aerospace Services Limited

- 6.4.9 Chromalloy Gas Turbine LLC

- 6.4.10 TURBOCAM, INC.

- 6.4.11 Hi-Tek Manufacturing, Inc.

- 6.4.12 Moeller Mfg. Company, LLC

- 6.4.13 C Blade S.p.A. Forging & Manufacturing

- 6.4.14 Precision Castparts Corp.

- 6.4.15 Howmet Aerospace Inc.

- 6.4.16 Doncasters Group

- 6.4.17 AeroEdge Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment