|

시장보고서

상품코드

2061639

만성 림프구성 백혈병 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Chronic Lymphocytic Leukemia - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

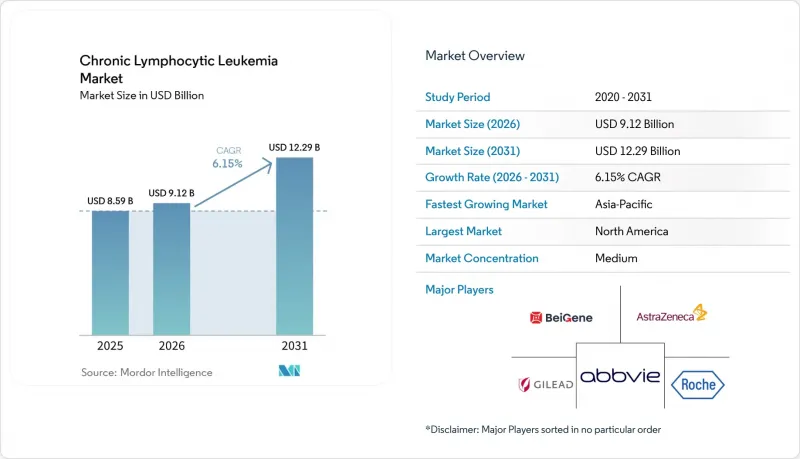

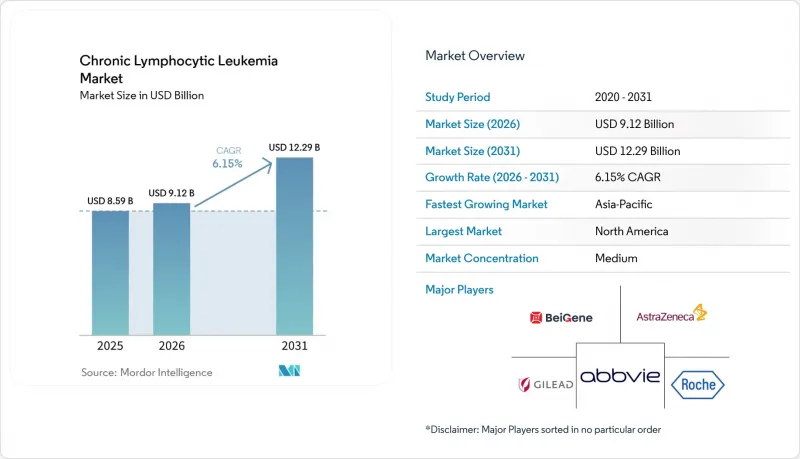

Mordor Intelligence에 의하면, 만성 림프구성 백혈병 시장 규모는 2025년 85억 9,000만 달러로 평가되었고, 2026년에는 91억 2,000만 달러로 추정되고, 2031년까지 122억 9,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 6.15%로 성장할 전망입니다.

본 보고서는 치료법별(화학요법, 표적요법 등), 진단 기술별(유세포 분석법, 분자유전학적 검사 등), 투여 경로별(경구, 정맥 내, 피하 및 근육 내), 치료 단계별(1차 치료법 등), 최종 사용자별(병원, 전문 클리닉, 검사실, 약국), 지역별(북미, 유럽 등)로 분류되어 있습니다. 시장 전망치는 금액(달러) 단위로 제시되어 있습니다.

세계의 만성 림프구성 백혈병 시장 동향 및 분석

BTK 및 BCL-2 억제제가 화학면역요법을 능가

BTK 및 BCL-2 억제제는 5년 무재발 생존율에서 우월성을 보이며, 경구 투여로 인한 편의성 및 독성 감소 덕분에 기존의 화학면역요법을 대체하여 1차 치료제로 선호되게 되었습니다. 아카라부티닙과 베네토클락스의 병용 요법은 미치료 환자에서 88%의 5년 무재발 생존율을 보였으며, 오비누츠주맙과 클로람부실 요법을 크게 상회했습니다. 공유 결합형 억제제에 대한 내성을 해결하기 위해 승인된 필트브루티닙은 1세대 약물에 의한 선택압으로 인해 연간 8-12%의 환자에서 C481S 돌연변이가 증가하고 있다는 점에서 주목을 받고 있습니다. 1차 치료법의 강력한 효능과 효과적인 구제 요법 옵션이 결합되면서, 만성 림프구성 백혈병 시장에서 화학요법 부문의 비중이 점차 줄어들고 있습니다.

고령화에 따라 CLL 환자가 급증하고 있습니다.

진단 시 중앙값이 72세인 만성 림프구성 백혈병(CLL)의 환자 수는 선진국의 인구 고령화에 따라 증가하고 있습니다. 미국에서는 2026년에 2만 2,760건의 신규 사례가 발생할 것으로 예상되며, 이는 2024년 대비 4% 증가한 수치입니다. 유럽에서는 독일, 이탈리아, 스페인 등 여러 국가에서 평균 수명이 연장된 것을 배경으로, 2025년에는 2만 4,500건의 신규 진단 사례가 기록되었습니다. 중국에서는 2선 도시에서 정기적인 혈액 검사 실시가 확대됨에 따라, 2020-2025년 CLL 발병률이 18% 증가했습니다. 그러나 유럽에서는 75세 이상 신규 진단 환자의 43%가 베네토클락스 투여에 있어 신장 또는 심혈관계 관련 금기 사항을 가지고 있어, 진단 건수 증가와 치료 적격성 사이에 격차가 있다는 사실이 드러났습니다. 이러한 격차를 해소하고 치료 중단을 줄이기 위해, 만 나이가 아닌 환자의 허약도를 바탕으로 투여량과 투여 일정을 조정하는 임상 프로토콜이 도입되기 시작했습니다.

미국 내 치료비 급등과 지불자 측의 장벽

베네토클락스나 자누부르티닙 등의 약물에 대한 연간 치료비가 18만 달러까지 급등하면서, 엄격한 사용 관리 방침이 도입되고 있습니다. 2025년까지 미국의 민간 보험사들은 BTK 억제제 청구 건의 78%에 대해 사전 승인을 의무화했으며, FDA의 광범위한 승인에도 불구하고 del(17p)이나 TP53 돌연변이의 증거를 요구하는 경우가 늘어났습니다. 브라질에서는 민간 보험 플랜에 따라 아카라부티닙 승인 전에 환자가 2차 화학요법을 완료해야 하는 것이 의무화되어 있으며, 이로 인해 표적 치료에 대한 접근이 평균 11개월 지연되어 리히터 전이의 위험이 높아지고 있습니다. 인도에서는 국민건강보험 제도가 BTK 억제제를 완전히 제외하고 있어, 환자의 92%가 제네릭 항암제에 의존할 수밖에 없으며, 그 결과 3년 전체 생존율은 표적 치료 요법의 89%에 비해 61%로 떨어졌습니다. 단계적 가격 책정이나 수량 기준의 정부 입찰이 부분적인 해결책을 제시하고는 있지만, 접근 격차를 완전히 해소하기에는 미치지 못하고 있습니다.

부문별 분석

면역요법 및 세포요법은 2031년까지 연평균 성장률(CAGR) 8.10%를 나타낼 것으로 예측되지만, 2025년에는 표적 치료제가 매출의 46.35%를 차지했습니다. 만성 림프구성 백혈병 치료 시장에서 BTK 및 BCL-2 억제제는 2025년에 72억 달러의 매출을 기록했습니다. 그러나 이중 특이성 항체와 동종 CAR-T 제품이 후기 임상시험 단계로 진입함에 따라, 이들 시장 점유율은 감소하고 있습니다. 미국에서는 화학요법을 대체 치료법으로 규정하는 지침 개정으로 인해, 2023-2025년 벤담스틴·리툭시맙의 사용량이 34% 감소했습니다. 2026년 2월에 승인된 아카라부티닙-베네토클락스 병용 요법은 12개월 후 환자의 67%에서 MRD가 검출되지 않는 결과를 달성함으로써, 화학요법을 동반하지 않는 치료로의 전환을 부각시켰을 뿐만 아니라, 향후 출시될 경쟁 제품에 대해 높은 유효성 기준을 제시했습니다.

신속한 4시간 내 결과 보고와 보험 환급상의 이점으로 높이 평가받고 있는 유세포분석법은 2025년 진단 시장 매출의 44.23%를 차지했습니다. 그러나 차세대 염기서열 분석(NGS)이 세를 넓혀가고 있으며, 연평균 성장률(CAGR) 7.60%로 확대되면서 만성 림프구성 백혈병 진단 시장의 성장을 주도하고 있습니다. 300-648개의 유전자를 분석하는 NGS 패널은 TP53, NOTCH1, SF3B1 및 ATM의 변이를 규명함으로써, 치료 방침 결정 및 임상시험 참여 적격성에 영향을 미쳐 치료 전략을 재구축하고 있습니다. 2025년에는 TP53 돌연변이 검출률이 22%에 달하고, 기존 방법의 2배가 될 것으로 예상되며, 이는 보다 광범위한 패널의 임상적 중요성을 뒷받침합니다. 세포유전학은 대규모 염색체 결손을 검출하는 데 여전히 틈새적인 역할을 하고 있지만, 시퀀싱 비용의 하락과 보험 적용 범위의 확대에 따라 경제적 균형은 NGS 쪽으로 유리하게 기울고 있습니다.

지역별 분석

2025년, 매출의 39.67%를 차지한 북미는 단계적 치료 요건을 우회하는 메디케어 정책의 혜택을 받고 있으며, FDA 승인을 받은 새로운 치료법을 신속하게 도입할 수 있는 견고한 종양학 네트워크를 보유하고 있습니다. 미국은 이 지역을 주도하며, 매출의 88%를 차지했습니다. 2025년에는 1만 8,400건의 신규 사례가 보고되었으며, 진단 당시의 중앙값 연령은 72세였습니다. 캐나다의 공적 의료보험 제도에서는 승인 후 6개월 이내에 표적 치료제의 보험 적용이 보장되지만, 멕시코에서는 보험 적용 범위가 제한적이어서 환자의 76%가 제네릭 항암제를 선택할 수밖에 없는 상황입니다.

2025년 매출의 32%를 차지한 유럽은 해당 지역 매출의 71%를 창출하는 주요 5개국에 의해 주도되고 있습니다. 독일은 1인당 BTK 억제제 사용량에서 1위를 차지했지만, 이탈리아와 스페인에서는 BTK 억제제에 대한 연간 지출 상한선이 설정되어 있어, 2027년에 제네릭 이부르티닙이 출시될 때까지 고위험 유전체 하위군에 대한 접근이 제한되고 있습니다. 영국에서는 1차 치료에 사용되는 아카라부티닙에 대해 35%의 비공개 할인이 적용됨에 따라, 연간 3,200명의 환자가 추가로 치료를 받을 수 있게 되어 도입이 가속화되었습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 8.50%를 기록하며 성장할 것으로 전망됩니다. 중국은 자누부르티닙을 연간 비용 2만 8,000달러로 국가 보험 적용 의약품 목록에 추가하여, 처방 건수의 대폭적인 증가를 이끌었습니다. 2026년 1분기에는 신규 BTK 치료 시작 건수의 28%를 이 치료법이 차지할 것으로 예측됩니다. 또한, 인구 고령화로 인해 2020년 이후 신규 환자 수가 18% 증가하여, 2025년에는 1만 2,500건에 달할 것으로 예측됩니다. 인도 및 동남아시아에서는 신생 헬스케어 네트워크들이 유전체 검사와 내원형 수액 센터를 도입하며, 인프라 측면의 과제를 점차 해결해 나가고 있습니다. 중동 및 아프리카 및 남미는 각각 전 세계 매출의 약 7%를 차지하고 있습니다. 부유한 걸프 연안 국가들은 자국민을 위해 BTK 억제제 비용을 지원하고 있지만, 이 지역의 다른 국가들은 바이오시밀러 가격이 하락하기를 기다리는 동안 화학요법에 의존하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the chronic lymphocytic leukemia market size is expected to increase from USD 8.59 billion in 2025 to USD 9.12 billion in 2026 and reach USD 12.29 billion by 2031, growing at a CAGR of 6.15% over 2026-2031.

This report is Segmented by Therapy Class (Chemotherapy, Targeted Therapy, and More), Diagnostics Technology (Flow Cytometry, Molecular Genetic Tests, and More), Route (Oral, IV, SC/IM), Line of Therapy (First-Line, and More), End User (Hospitals, Specialty Clinics, Labs, Pharmacies), and Geography (North America, Europe, and More). Market Forecasts are Provided in Value (USD).

Global Chronic Lymphocytic Leukemia Market Trends and Insights

BTK and BCL-2 Inhibitors Surge Ahead of Chemoimmunotherapy

BTK and BCL-2 inhibitors have become the preferred frontline treatments, replacing traditional chemoimmunotherapy due to their superior five-year progression-free survival rates, simplified oral dosing, and reduced toxicity. The acalabrutinib-venetoclax combination demonstrated an 88% five-year progression-free rate in treatment-naive patients, significantly outperforming the obinutuzumab-chlorambucil regimen. Pirtobrutinib, approved for addressing covalent-inhibitor resistance, is gaining traction as first-generation agents increasingly select for C481S mutations in 8-12% of patients annually. The strong efficacy of first-line treatments, combined with effective salvage options, is driving a decline in the chemotherapy segment within the chronic lymphocytic leukemia market.

CLL Cases Surge as Populations Age

With a median diagnosis age of 72, chronic lymphocytic leukemia (CLL) cases are increasing alongside aging populations in industrialized nations. The United States is projected to see 22,760 new cases in 2026, reflecting a 4% rise from 2024. In Europe, 2025 recorded 24,500 new diagnoses, driven by rising life expectancies in countries such as Germany, Italy, and Spain. In China, the incidence of CLL rose by 18% between 2020 and 2025, supported by expanded routine hematology testing in second-tier cities. However, 43% of newly diagnosed Europeans over 75 faced renal or cardiovascular contraindications for venetoclax, underscoring a gap between increasing diagnoses and treatment eligibility. This disparity has prompted the adoption of clinical protocols that adjust doses and schedules based on patient frailty rather than chronological age, aiming to reduce treatment discontinuations.

Escalating Therapy Costs and Payer Hurdles in the U.S.

Annual treatment costs for drugs like venetoclax and zanubrutinib have surged to USD 180,000, leading to the implementation of stringent utilization-management policies. By 2025, U.S. commercial insurers required prior authorization for 78% of BTK inhibitor claims, often demanding evidence of del(17p) or TP53 mutations despite broad FDA approvals. In Brazil, private insurance plans mandate patients to complete two lines of chemotherapy before approving acalabrutinib, delaying access to targeted therapy by an average of 11 months and increasing the risk of Richter transformation. In India, the national health scheme excludes BTK inhibitors entirely, forcing 92% of patients to rely on generic chemotherapy, which reduces three-year overall survival rates to 61% compared to 89% for targeted regimens. While tiered pricing and volume-based government tenders provide partial solutions, they have not fully addressed the access disparity.

Other drivers and restraints analyzed in the detailed report include:

- Next-Gen Oral Regimens Gain Wider Reimbursement

- Companion Diagnostics and Precision Medicine on the Rise

- Resistance Mutations Emerge in First-Generation BTK Inhibitors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Immunotherapy and cell therapy are projected to grow at an 8.10% CAGR through 2031, while targeted agents accounted for 46.35% of sales in 2025. In the chronic lymphocytic leukemia therapy market, BTK and BCL-2 inhibitors generated USD 7.2 billion in 2025. However, their market share is declining as bispecific antibodies and allogeneic CAR-T products progress to late-stage trials. The use of bendamustine-rituximab in the U.S. decreased by 34% from 2023 to 2025 due to updated guidelines that relegated chemotherapy to an alternative option. The approval of the acalabrutinib-venetoclax combination in February 2026, which achieved a 67% undetectable MRD rate in patients after 12 months, highlights the shift towards chemotherapy-free treatments and sets a high efficacy standard for future competitors.

Flow cytometry, valued for its quick four-hour turnaround and reimbursement advantages, accounted for 44.23% of diagnostics revenue in 2025. However, next-generation sequencing (NGS) is gaining traction, expanding at a 7.60% CAGR and driving growth in the chronic lymphocytic leukemia diagnostics market. NGS panels, which analyze 300-648 genes, identify mutations in TP53, NOTCH1, SF3B1, and ATM, influencing therapy decisions and trial eligibility, thereby reshaping treatment strategies. A 22% detection rate for TP53 mutations in 2025, double that of traditional methods, underscores the clinical importance of broader panels. While cytogenetics continues to play a niche role in detecting large chromosomal deletions, declining sequencing costs and increased payer coverage are shifting the economic balance in favor of NGS.

Geography Analysis

In 2025, North America, accounting for 39.67% of sales, benefits from Medicare policies that bypass step-therapy requirements and features robust oncology networks that quickly adopt new FDA-approved treatments. The United States led the region, contributing 88% of its revenue, with 18,400 new cases reported in 2025 and a median diagnosis age of 72 years. While Canada's public healthcare system ensures reimbursement for targeted therapies within six months of approval, Mexico's limited coverage drives 76% of its patients toward generic chemotherapy.

Europe, representing 32% of 2025's revenue, is driven by its five largest economies, which generate 71% of the region's turnover. Germany leads in per-capita BTK usage, while Italy and Spain impose annual spending caps on BTK therapies, restricting access to high-risk genomic subsets until the expected availability of generic ibrutinib in 2027. The United Kingdom experienced accelerated adoption after a confidential 35% discount on acalabrutinib for first-line treatment expanded access to an additional 3,200 patients annually.

Asia-Pacific is projected to grow at a CAGR of 8.50% through 2031. China included zanubrutinib in its National Reimbursement Drug List at an annual cost of USD 28,000, driving a significant increase in prescriptions, with the therapy accounting for 28% of all new BTK initiations in Q1 2026. Additionally, population aging contributed to an 18% rise in new cases since 2020, resulting in 12,500 new cases in 2025. In India and Southeast Asia, emerging healthcare networks are introducing genomic testing and day-care infusion centers, gradually addressing infrastructure challenges. The Middle East and Africa, along with South America, each account for approximately 7% of global revenue. Wealthy Gulf states provide funding for BTK inhibitors for their citizens, while other countries in these regions rely on chemotherapy, awaiting reductions in biosimilar prices.

- Abbvie

- Adaptive Biotechnologies

- Amgen

- AstraZeneca

- BeiGene Ltd.

- Bristol-Myers Squibb

- Celgene Corporation (BMS)

- Cyclacel Pharmaceuticals

- Roche

- Gilead Sciences

- Infinity Pharmaceuticals

- Johnson & Johnson

- Merck

- MorphoSys AG

- Novartis

- Ono Pharmaceutical

- Pfizer

- Sanofi

- Secura Bio, Inc.

- Teva Pharmaceutical Industries

- TG Therapeutics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Uptake of Targeted BTK & BCL-2 Inhibitors

- 4.2.2 Rising CLL Prevalence in Ageing Populations

- 4.2.3 Broader Reimbursement for Next-Gen Oral Regimens

- 4.2.4 Expansion of Companion Diagnostics & Precision Medicine

- 4.2.5 Emergence of Off-The-Shelf Allogeneic CAR-T Platforms

- 4.2.6 AI-Enabled Minimal-Residual-Disease (MRD) Monitoring Tools

- 4.3 Market Restraints

- 4.3.1 Therapy Cost Escalation & Payer Step-Therapy Hurdles

- 4.3.2 Resistance Mutations to First-Gen BTK Inhibitors

- 4.3.3 Limited Specialized Oncology Capacity in Emerging Markets

- 4.3.4 Data-Privacy Concerns in Cloud-Based Genomic Diagnostics

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Therapy Class

- 5.1.1 Chemotherapy

- 5.1.2 Targeted Therapy (BTK, BCL-2, PI3K, others)

- 5.1.3 Immunotherapy & Cell Therapy (mAbs, CAR-T, bispecifics)

- 5.1.4 Combination Regimens

- 5.2 By Diagnostics Technology

- 5.2.1 Flow Cytometry

- 5.2.2 Molecular Genetic Tests (NGS, PCR panels)

- 5.2.3 FISH & Cytogenetics

- 5.2.4 Immunohistochemistry & Others

- 5.3 By Route of Administration

- 5.3.1 Oral

- 5.3.2 Intravenous

- 5.3.3 Subcutaneous / Intramuscular

- 5.4 By Line of Therapy

- 5.4.1 First-Line / Treatment-Naive

- 5.4.2 Second-Line

- 5.4.3 Relapsed / Refractory

- 5.5 By End User

- 5.5.1 Hospitals & Academic Medical Centers

- 5.5.2 Specialty Oncology Clinics

- 5.5.3 Diagnostic Laboratories

- 5.5.4 Retail & Online Pharmacies

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Adaptive Biotechnologies

- 6.3.3 Amgen Inc.

- 6.3.4 AstraZeneca PLC

- 6.3.5 BeiGene Ltd.

- 6.3.6 Bristol Myers Squibb

- 6.3.7 Celgene Corporation (BMS)

- 6.3.8 Cyclacel Pharmaceuticals

- 6.3.9 F. Hoffmann-La Roche AG

- 6.3.10 Gilead Sciences Inc.

- 6.3.11 Infinity Pharmaceuticals

- 6.3.12 Johnson & Johnson (Janssen)

- 6.3.13 Merck & Co., Inc.

- 6.3.14 MorphoSys AG

- 6.3.15 Novartis AG

- 6.3.16 Ono Pharmaceutical Co., Ltd.

- 6.3.17 Pfizer Inc.

- 6.3.18 Sanofi S.A.

- 6.3.19 Secura Bio, Inc.

- 6.3.20 Teva Pharmaceutical Industries Ltd.

- 6.3.21 TG Therapeutics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment