|

시장보고서

상품코드

2061641

치과 보철물 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Dental Prosthetics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

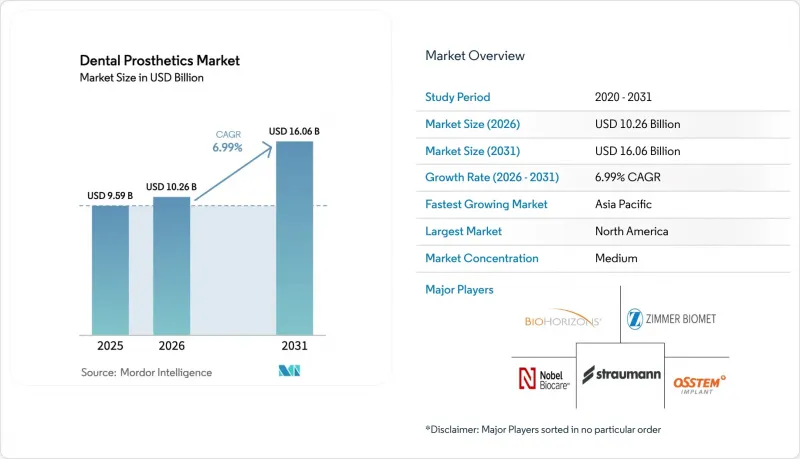

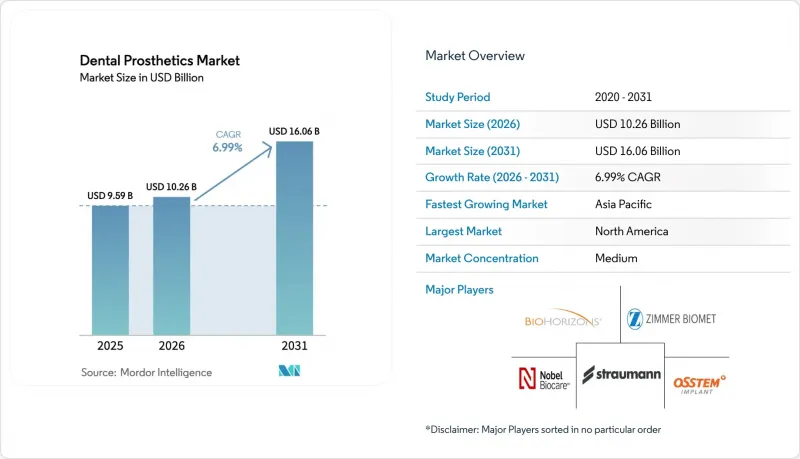

Mordor Intelligence에 의하면, 치과 보철물 시장 규모는 2025년 95억 9,000만 달러로 평가되었습니다. 2026년에는 102억 6,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR은 6.99%를 나타내, 2031년까지 160억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형(크라운, 브릿지, 의치, 어버트먼트, 인레이/온레이/베니어, 기타 보철물), 소재(세라믹/지르코니아 등), 고정 방식(고정식, 가철식, 고정·가철 하이브리드식), 최종 사용자(치과, 치과 기공소 등), 지역(북미, 유럽 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(단위)으로 제시되어 있습니다.

세계의 치과 보철물 시장 동향과 인사이트

고령화와 무치악 환자의 급증

2021년 기준으로 전 세계적으로 3억 4,900만 명이 심각한 치아 상실로 고통받았으며, 일본, 독일, 이탈리아에서는 65세 이상 성인의 유병률이 이미 30%를 넘어섰습니다. 중국의 고령 인구는 2030년까지 4억 명에 달할 것으로 예상되지만, 틀니를 사용하는 비율은 고작 12%에 불과합니다. 일본의 보험사는 임플란트 비용의 70%를 지급하고 있으며, 2025년에는 고령자 치료의 41%가 임플란트 지지 브릿지로 이루어졌습니다. 현재 시장의 성장 속도를 좌우하는 것은 단순한 인구 동향이 아니라 공적 보험 제도입니다. 이는 보조금이 씹는 기능과 영양 섭취를 유지할 수 있는 크라운이나 임플란트 브릿지를 선택하도록 환자를 독려하고 있기 때문입니다.

미용 치과에 대한 수요 증가

미국 내 심미 치과 치료 매출은 2025년에 14% 증가했으며, 그중 68%를 베니어와 올세라믹 크라운이 차지했습니다. 화상 회의의 보급으로 치아 색상에 대한 관심이 높아지면서, 45세 미만의 전문가들은 보철물을 경력의 자산으로 여기게 되었습니다. 아랍에미리트와 사우디아라비아에서는 의료 관광 패키지 상품을 통해 2025년 미용 치과 지출이 22% 증가했습니다. 인도에서는 핀테크 주도의 무이자 상품이 확산되면서, 2024년 도시 지역의 크라우드렌딩 투자액이 19% 증가했습니다. 치과 심미 치료와 고용 가능성 간의 연관성을 보여주는 동료 심사 논문의 발표로 인해, 고액의 치료비를 지불하려는 의지가 더욱 높아지고 있습니다.

고액의 치료비와 장비 비용

2025년, 미국의 임플란트 및 크라운 평균 본인 부담금은 4,200달러에 달하고, 전년 대비 7% 증가했습니다. 독일에서는 메탈 세라믹의 기준 가격의 60%만 보험이 적용되므로, 올 세라믹으로 업그레이드할 경우 환자가 650-975달러를 부담해야 합니다. 브라질에서는 지르코니아 크라운 1개의 비용이 2,800 레알(560 달러)이며, 이는월최저 임금의 60%에 해당합니다. CAD/CAM 설비 투자로 인해 치과 기공소는 가격을 인상할 수밖에 없게 되었고, 그 결과 치료 접근성이 더욱 제한되고 있습니다.

부문별 분석

2025년에는 임시 치아가 필요 없는 1회 치료 CAD/CAM 기술의 확산에 힘입어 크라운이 치과 보철 시장 점유율의 43.12%를 차지하며 시장을 주도했습니다. 한편, 의치 시장은 2031년까지 연평균 6.85%의 성장률을 보일 것으로 전망됩니다. 이는 일본, 독일, 이탈리아에서 고령화가 진행됨에 따라, 골흡수에 대응할 수 있는 탈착식 치료법이 선호되기 때문입니다. 브릿지는 2025년에 약 18%를 차지하며, 임플란트 시술을 피하는 환자층에서 안정적인 수요를 유지했습니다. 2025년 전 세계 임플란트 식립 건수가 11% 증가함에 따라 어버트먼트에 대한 수요도 늘어났습니다.

VITA사는 두께 0.3mm의 리튬 디실리케이트 베니어를 출시했습니다. 이는 법랑질을 보존하면서 파괴 인성을 30% 향상시키는 것입니다. 제품 환경에서는 범용성이 중요시되고 있어, 고정형과 탈착형 워크플로우 모두에 정통한 실험실은 더 폭넓은 환자층을 확보할 수 있는 반면, 단일 제품 라인에 특화된 전문 실험실은 이익률 압박에 직면해 있습니다.

2025년, 치과 보철물 시장 점유율의 48.05%를 세라믹과 지르코니아가 차지했습니다. 이는 에나멜질을 모방한 초고투과성 등급의 보급에 힘입은 결과입니다. 하이브리드 복합재료는 유리섬유 강화 폴리머가 상아질의 탄성을 재현하고 계면에서의 응력을 저감시킴으로써 9.33%의 성장률이 예상됩니다. 금속 세라믹은 후방 치아의 내구성 측면에서 여전히 22%의 점유율을 유지하고 있지만, 심미성 면에서는 역풍을 맞고 있습니다. 순수 금속은 12%를 차지하며, 주로 탈부착식 프레임워크나 어버먼트에 사용됩니다.

폴리머와 아크릴이 10%를 차지했으나, 프린트 수지의 등장으로 시장이 변화하고 있습니다. 도쿄대학 연구진은 강도 구배가 있는 지르코니아를 단일 크라운에 배합하여 파절 위험을 40% 줄였습니다. 이보클라르의 IPS e.max ZirCAD Prime은 49%의 투과율과 850 MPa의 굽힘 강도를 자랑하며, 단일 재료로 전체 치열의 치료에 대응할 수 있습니다.

지역별 분석

북미는 2025년 매출의 35.08%를 차지하며, 메디케어 어드밴티지(Medicare Advantage)의 보험금 지급 및 USMCA(미국·멕시코·캐나다 협정)에 따른 니어쇼어링에 힘입고 있습니다. 그러나 연구소의 68%가 CAD 담당자 채용에 어려움을 겪고 있으며, FDA 510(k) 및 ISO 13485 준수 요건으로 인해 20만-50만 달러의 간접비가 추가로 발생함에 따라 업계 재편이 진행되고 있습니다. 멕시코에서는 연구소에 대한 투자액이 1억 8,000만 달러에 달했으며, 캐나다에서는 1,200개의 일자리가 창출되었습니다.

아시아태평양은 연평균 성장률(CAGR) 8.93%를 나타낼 것으로 전망됩니다. 이는 중국에서 본인 부담금 상한선이 설정됨에 따라 시범 도시에서 크라우드펀딩을 통한 치료 건수가 31% 급증한 데 기인합니다. 일본에서는 고령자용 임플란트 비용의 70%가 보험 적용 대상이므로, 고정 브릿지 시술 비율이 41%에 달할 전망입니다. 인도에서는 핀테크를 활용한 할부 결제 방식이 선택적 치료 수요를 끌어올리고 있는 반면, 서울과 시드니의 대학에서는 AI를 활용한 크라운 설계가 선도적으로 이루어지고 있습니다. 인프라 격차는 여전히 존재하며, 동남아시아 지방의 치과 중 구강 스캐너를 보유하고 있는 곳은 30% 미만입니다.

독일의 환자들은 올세라믹으로 업그레이드하는 데 650-975달러의 추가 비용을 지불하고 있습니다. 영국 국민보건서비스(NHS)의 210만 건에 달하는 예약 적체로 인해, 영국 환자들은 1,000-1,500달러 상당의 민간 임플란트 치료를 받고 있습니다. 남유럽의 치과 관광 비용은 북유럽보다 40% 저렴하여, 스페인에는 34만 명의 외국인 환자가 방문하고 있습니다. GCC 국가들에서는 심미 치과 시장이 22% 성장했으며, 브라질에서 의치에 대한 보험 적용이 의무화되면서 남미 시장의 성장세가 더욱 가속화되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the dental prosthetics market size is expected to grow from USD 9.59 billion in 2025 to USD 10.26 billion in 2026 and is forecast to reach USD 16.06 billion by 2031 at 6.99% CAGR over 2026-2031.

This report is Segmented by Product Type (Crowns, Bridges, Dentures, Abutments, Inlays/Onlays/Veneers, Other Prosthetics), Material (Ceramic/Zirconia, and More), Fixation Type (Fixed, Removable, Fixed-Removable Hybrid), End User (Dental Clinics, Dental Laboratories, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Global Dental Prosthetics Market Trends and Insights

Aging Population & Edentulism Surge

Severe tooth loss affected 349 million people worldwide in 2021; prevalence already exceeds 30% among adults 65+ in Japan, Germany, and Italy. China's seniors will reach 400 million by 2030, yet only 12% use any prosthetics. Japan's insurer reimburses 70% of implant costs, raising implant-supported bridges to 41% of senior placements in 2025. National payers, rather than raw demographics, now dictate velocity as subsidies nudge patients toward crowns and implant bridges that preserve mastication and nutrition.

Rising Demand for Aesthetic Dentistry

Aesthetic-procedure revenue in the United States climbed 14 % in 2025, with veneers and all-ceramic crowns making up 68 % of electives. Video-conferencing culture increased scrutiny of tooth color, pushing professionals under 45 to treat restorations as career assets. The UAE and Saudi Arabia increased cosmetic spend by 22% in 2025 through bundled medical tourism packages. India's urban crowdlending placements rose 19% in 2024 as fintech-driven zero-interest plans spread. Peer-reviewed links between dental aesthetics and employability are reinforcing willingness to pay premiums.

High Procedure & Device Costs

The average U.S. implant-and-crown out-of-pocket cost reached USD 4,200 in 2025, up 7% year over year. Germany reimburses only 60% of metal-ceramic reference prices, leaving patients with USD 650-975 for an all-ceramic upgrade. In Brazil, a single zirconia crown costs BRL 2,800 (USD 560), 60 % of the monthly minimum wage. Capital spending on CAD/CAM forces labs to raise prices, further limiting access.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of CAD/CAM & 3D Printing

- Expanding Dental Insurance Coverage

- Shortage of Digitally Skilled Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Crowns dominated 2025 with a 43.12% share of the dental prosthetics market, lifted by single-visit CAD/CAM, which eliminates the need for temporaries. Dentures, however, are forecast to grow at 6.85% through 2031, as aging populations in Japan, Germany, and Italy favor removable options that accommodate bone resorption. Bridges accounted for roughly 18% in 2025, stable among patients who forgo implant surgery. Abutments rose in line with an 11% global increase in implant placement in 2025.

VITA introduced a lithium-disilicate veneer with a 0.3 mm thickness, preserving enamel while increasing fracture toughness by 30 %. The product landscape rewards versatility; labs fluent in both fixed and removable workflows capture a wider patient base, while single-line specialists face margin compression.

Ceramic and zirconia accounted for 48.05% of the dental prosthetics market share in 2025, propelled by ultra-translucent grades that mimic enamel. Hybrid composites are poised to grow at 9.33% as glass-fiber polymers replicate dentin's elasticity, reducing stress at interfaces. Metal-ceramic still held 22 % for posterior durability, yet faces cosmetic headwinds. Pure metals accounted for 12%, mainly in removable frameworks and abutments.

Polymers and acrylics accounted for 10% but are being disrupted by printed resins. University of Tokyo researchers blended graded-strength zirconia into single crowns, reducing chipping risk by 40%. Ivoclar's IPS e.max ZirCAD Prime delivers 850 MPa flexural strength at 49% translucency, covering full-arch cases with a single material.

Geography Analysis

North America accounted for 35.08% of 2025 revenue, buoyed by Medicare Advantage reimbursement and USMCA-driven near-shoring. Yet 68% of labs struggle to fill CAD vacancies, and FDA 510(k) and ISO 13485 compliance add USD 200,000-500,000 in overhead, reinforcing consolidation. Mexico attracted USD 180 million in lab investment, while Canada added 1,200 jobs.

Asia-Pacific is set to grow at an 8.93% CAGR as China's copay cap sparked a 31% surge in crowdfunded placements in pilot cities. Japan reimburses 70% of senior implant costs, pushing fixed bridges to 41% of placements. India's fintech-enabled installment plans raise elective demand, while Seoul and Sydney universities pioneer AI crown design. Infrastructure gaps persist: fewer than 30 % of rural Southeast Asian clinics own intraoral scanners.

German patients pay an extra USD 650-975 for all-ceramic upgrades. NHS England's 2.1 million-appointment backlog funnels U.K. patients to private implants at USD 1,000-1,500. Southern European dental tourism undercuts northern prices by 40 %, drawing 340,000 inbound patients to Spain. The GCC posted 22% cosmetic dentistry growth, and Brazil's mandatory denture coverage lifts South American momentum.

- 3M

- Align Technology

- BioHorizons

- Coltene Holding

- Dentium Co. Ltd.

- Dentsply Sirona

- Envista Holdings (Nobel Biocare)

- GC Corporation

- Glidewell Dental

- Henry Schein

- Straumann Group

- Ivoclar Vivadent

- Kuraray Noritake Dental

- Nobel Biocare Services

- Osstem Implant Co. Ltd.

- Planmeca

- Straumann Group

- VITA Zahnfabrik

- Zimmer Biomet

- ZimVie

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Population & Edentulism Surge

- 4.2.2 Rising Demand for Aesthetic Dentistry

- 4.2.3 Rapid Adoption of CAD/CAM & 3-D Printing

- 4.2.4 Expanding Dental Insurance Coverage

- 4.2.5 AI-Driven Automated Design Workflows

- 4.2.6 Near-Shoring Spurred by Tariff Barriers

- 4.3 Market Restraints

- 4.3.1 High Procedure & Device Costs

- 4.3.2 Shortage of Digitally Skilled Technicians

- 4.3.3 Volatile Zirconia & Noble-Metal Prices

- 4.3.4 Fragmented Global Data-Protection Rules

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value & Volume)

- 5.1 By Product Type

- 5.1.1 Crowns

- 5.1.2 Bridges

- 5.1.3 Dentures

- 5.1.4 Abutments

- 5.1.5 Inlays / Onlays / Veneers

- 5.1.6 Other Prosthetics

- 5.2 By Material

- 5.2.1 Ceramic / Zirconia

- 5.2.2 Metal-Ceramic (PFM)

- 5.2.3 Metals

- 5.2.4 Polymers & Acrylics

- 5.2.5 Hybrid / Composite Materials

- 5.3 By Fixation Type

- 5.3.1 Fixed

- 5.3.2 Removable

- 5.3.3 Fixed-Removable Hybrid

- 5.4 By End User

- 5.4.1 Dental Clinics

- 5.4.2 Dental Laboratories

- 5.4.3 Hospitals & Surgical Centers

- 5.4.4 Academic & Research Institutes

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 3M

- 6.3.2 Align Technology Inc.

- 6.3.3 BioHorizons Inc

- 6.3.4 COLTENE Holding AG

- 6.3.5 Dentium Co. Ltd.

- 6.3.6 Dentsply Sirona Inc.

- 6.3.7 Envista Holdings (Nobel Biocare)

- 6.3.8 GC Corporation

- 6.3.9 Glidewell Dental

- 6.3.10 Henry Schein Inc.

- 6.3.11 Institut Straumann AG

- 6.3.12 Ivoclar Vivadent AG

- 6.3.13 Kuraray Noritake Dental

- 6.3.14 Nobel Biocare Services

- 6.3.15 Osstem Implant Co. Ltd.

- 6.3.16 Planmeca Oy

- 6.3.17 Straumann AG

- 6.3.18 VITA Zahnfabrik

- 6.3.19 Zimmer Biomet Holdings

- 6.3.20 ZimVie Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment