|

시장보고서

상품코드

2061718

치과용 밀링 머신 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Dental Milling Machine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

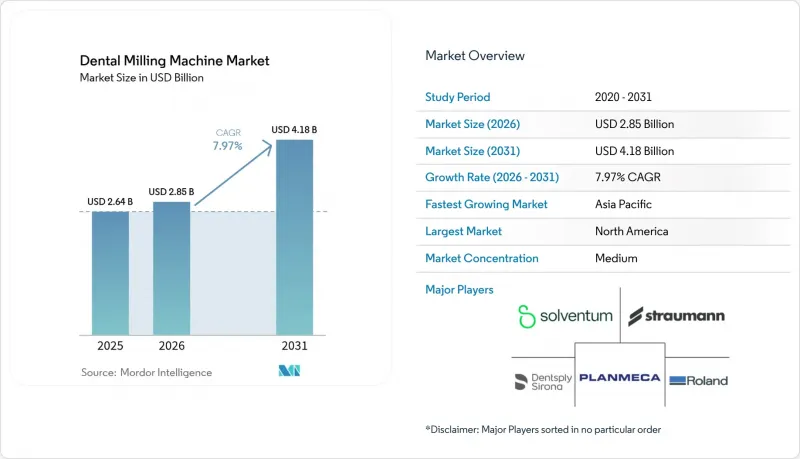

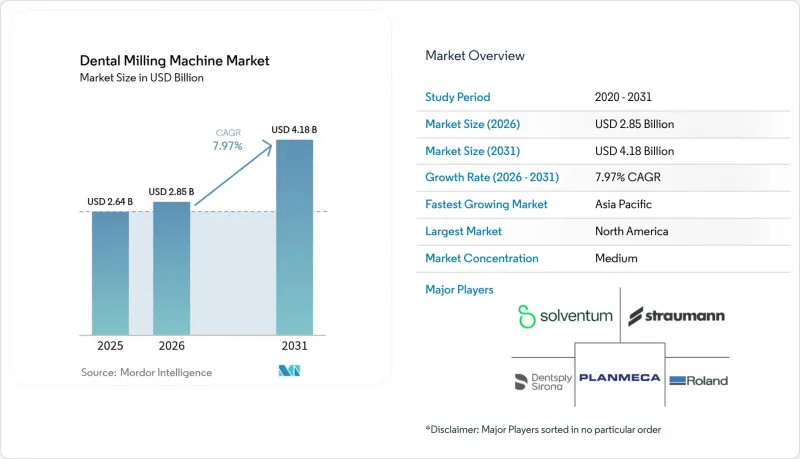

Mordor Intelligence에 의하면, 2026년 치과용 밀링 머신 시장 규모는 28억 5,000만 달러에 달할 것으로 추정됩니다. 2025년 26억 4,000만 달러에서 성장하여 2031년에는 41억 8,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지의 연평균 성장률(CAGR)은 7.97%를 나타낼 것으로 전망됩니다.

본 보고서는 기계 유형(실험실용 밀링 머신 및 진료실용 밀링 머신), 크기(탁상형, 벤치탑형, 스탠드얼론형), 축 구성(4축 머신 및 5축 머신), 기술(카피 밀링 및 CAD/CAM 밀링), 최종 사용자(치과 기공소 등), 지역(북미, 유럽 등)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 치과용 밀링 머신 시장 동향 및 분석

치료되지 않은 충치 및 치아 상실로 인한 전 세계적 부담 증가

추정 23억 명이 치료받지 않은 충치를 안고 생활하고 있으며, 치과의사는 단 한 번의 내원만으로 치료를 제공할 수 있고 지르코니아 크라운의 장기 생존율이 95%를 넘기 때문에 밀링 방식으로 제작된 보철물을 점점 더 많이 선택하고 있습니다. 증례 수가 증가하는 가운데, 워크플로우의 효율화는 매우 중요하며, 기존의 실험실 작업을 밀링으로 대체함으로써 진료 시간이 최대 60% 단축되었다고 보고하는 치과도 있습니다. 신흥국에서는 중산층의 확대에 따라 발치 대신 심미성이 뛰어난 보철물을 원하는 환자가 증가하고 있어, 그 영향이 가장 두드러집니다. 당일 치료 솔루션을 도입한 치과에서는 환자들의 확실한 지지를 얻고 있으며, 고액의 치료비에 대한 지불 의향도 확인되어, 이를 통해 의료기관의 수익 증대 가능성이 높아지고 있습니다.

치과 업무 프로세스의 급속한 디지털화

스캐너와 밀링 장치의 연동은 설계 파일 전송을 몇 분이 아닌 몇 초 만에 가능하게 하는 클라우드 플랫폼을 통해 가속화되고 있으며, 환자가 의자에 앉은 채로 원격지의 디자이너가 크라운이나 브릿지의 최종 조정을 수행할 수 있게 되었습니다. 자동화된 설계 도구를 통해 크라운 제안에 대한 승인률은 94%에 달하며, CAD 습득 기간을 대폭 단축하고 비전문 팀의 활용 범위를 넓히고 있습니다. 밀링 장치에 내장된 품질 관리 루틴 덕분에 재가공 횟수가 줄어들고, 시간이 지남에 따라 준비 작업을 최적화하는 데이터 피드백 루프가 형성됩니다. 그 결과, 치과 병원들은 디지털 전환을 단순한 선택적 업그레이드가 아닌, 경쟁력을 유지하기 위한 필수 요건으로 인식하게 되었습니다.

다축 밀링 장비의 높은 초기 비용과 유지비

엔트리 레벨의 체어사이드 패키지는 소프트웨어, 교육, 시설 업그레이드 비용을 포함하기 전 단계에서 약 10만 달러부터 시작됩니다. 다이아몬드 버 교체 비용은 연간 운영비의 20%에 달하기도 하여, 진료 건수가 적은 클리닉의 경우 투자 회수율 계산에 큰 부담이 되고 있습니다. 리스나 수리 비용에 따른 지불 방식이 점차 보편화되고 있지만, 잔존 가치의 불확실성과 서비스 계약상의 의무로 인해 여전히 일부 구매자들은 망설이고 있습니다. 신흥 시장에서는 자금 부족이 더욱 심각하며, 대출 금리는 여전히 높은 수준이고, 환율 변동으로 인해 수입 비용도 상승하고 있습니다. 이에 대응하여 각 벤더사는 진료소가 시간이 지남에 따라 스핀들이나 툴 매거진을 추가할 수 있는 모듈식 설계를 채택하여, 증가하는 진료 건수에 맞추어 현금 흐름을 조정할 수 있도록 하고 있습니다.

부문별 분석

내부 플랫폼은 2025년 매출의 64.40%를 차지하며, 여러 클리닉에 제품을 공급하는 고생산성 실험실의 핵심적인 역할을 부각시켰습니다. 일반적인 설치 환경에서는 다중 재료 대응 캐러셀, 연속 스핀들 운전, 자동 디스크 관리가 지원되어, 체어사이드 유닛을 훨씬 능가하는 일일 생산량을 실현합니다. 이 연구소는 이러한 규모를 바탕으로 폭넓은 환자층에게 일관성 있는 보철물을 제공하고 있으며, 치과용 밀링 머신 시장은 집중 생산 체제에 기반을 둔 상태를 유지하고 있습니다.

‘병원 내’ 카테고리는 연평균 성장률(CAGR) 10.36%로 성장하고 있습니다. 이는 당일 진료가 예약 관리를 개선하고 진료 수락률을 높이기 위함입니다. 최신 소형 밀링 머신은 단일 크라운뿐만 아니라 지르코니아 브릿지도 가공할 수 있게 되어, 실험실 시스템과의 격차를 좁히고 있습니다. 치과 병원의 보고에 따르면, 팀이 디지털 공정에 자신감을 갖게 되면 도입 후 4개월 이내에 월간 생산량이 두 배로 증가합니다. 이러한 생산성의 급격한 상승은 장비 소유의 경제적 이점을 강화하여 견조한 수요를 지속시키고 있습니다.

4축 장비는 합리적인 가격과 사용 편의성 덕분에 표준 크라운 및 인레이에 충분한 가공 범위를 제공하여, 2025년에는 치과용 밀링 머신 시장의 55.30% 점유율을 차지했습니다. 사용자들은 간결한 공구 경로와 설정 시간 단축을 높이 평가하고 있으며, 이는 효율적인 실험실 운영을 뒷받침하고 있습니다.

한편, 5축 솔루션은 위치를 재조정할 필요 없이 언더컷, 스크류 접근 채널, 풀 아치 프레임워크를 가공할 수 있어 연평균 성장률(CAGR) 11.55%로 성장하고 있습니다. 자유도가 높아짐에 따라 치경부의 밀착감과 마진의 완성도가 향상되어, 인도 후 진료석에서의 수정이 줄어듭니다. 5축 스테이션을 도입한 치과 진료소는 임플란트 및 심미 치과 관련 케이스를 더 많이 수주하고 있으며, 이러한 수익성이 높은 틈새 시장이 치과용 밀링 머신 업계 전반의 장비 업그레이드를 촉진하고 있습니다.

지역별 분석

북미는 정교한 보험 환급 제도와 CAD/CAM의 조기 도입에 힘입어 2025년 전 세계 매출의 37.60%를 차지했습니다. 약 15%의 치과에서 원내 밀링을 실시하고 있으며, 서비스 업체들은 지원 계약의 효율성을 높이기 위해 장비 조달을 표준화하고 있습니다. 또한, 5년마다 하드웨어를 교체할 수 있도록 예측 가능한 유리한 리스 조건 역시 설비 투자를 촉진하고 있습니다.

유럽은 두 번째로 큰 시장이며, 규제 조화가 진행됨에 따라 제품 출시가 가속화되고 있습니다. 독일과 스칸디나비아의 제조업체들은 지속가능성을 중시하는 치과 기공소를 유치하기 위해 다층 지르코니아와 에너지 절약형 스핀들 개발을 주도하고 있습니다. 엄격한 데이터 개인정보 보호 규제로 인해 공급업체들은 안전한 클라우드 커넥터 구축을 촉진하고 있으며, 국경을 넘어 설계 데이터를 교환하는 의료 기관 네트워크에서 도입이 확대되고 있습니다. 이 지역의 치과용 밀링 머신 시장은 장인 정신이 깃든 품질을 중시하는 독립 실험실들에 의해 형성되어 있으며, 단순한 생산 능력 확대보다는 정밀도 향상을 위한 업그레이드에 대한 수요가 발생하고 있습니다.

아시아태평양은 가처분 소득 증가와 태국 및 인도에서 활기를 띠고 있는 치과 관광의 호조에 힘입어, 세계 최고 수준인 연평균 성장률(CAGR) 12.95%로 성장을 지속하고, 있습니다. 중국은 국내 생산을 급속히 확대하며 서유럽 기존 기업들과의 기술 격차를 좁혀가고 있는 반면, 일본은 정밀 공학 분야의 전문 지식을 활용해 도시 지역의 소규모 클리닉에 최적화된 소형 5축 밀링 머신을 개발하고 있습니다. 현재 일부 국가에서는 공적 의료보험 제도를 통해 CAD/CAM 크라운 비용이 보장됨에 따라, 치과에서 밀링 머신을 도입하는 움직임이 활발해지고 있습니다. 중동 및 아프리카 및 남미에서는 완만한 성장이 예상됩니다. 남미에서는 확립된 치과 제조 클러스터를 바탕으로 브라질이 주도적인 역할을 수행하는 반면, 걸프협력회의(GCC) 회원국에서는 의료 관광객을 대상으로 한 현대적인 클리닉에 대한 투자가 활발해지고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the dental milling machine market size in 2026 is estimated at USD 2.85 billion, growing from 2025 value of USD 2.64 billion with 2031 projections showing USD 4.18 billion, growing at 7.97% CAGR over 2026-2031.

This report is Segmented by Machine Type (In Lab Milling Machines and In-Office Milling Machines), Size (Tabletop, Bench-Top, and Stand-Alone), Axis Configuration (4-Axis Machines and 5-Axis Machines), Technology (Copying Milling and CAD/CAM Milling), End-User (Dental Laboratories, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Dental Milling Machine Market Trends and Insights

Rising Global Burden of Untreated Dental Caries & Tooth Loss

An estimated 2.3 billion people live with untreated caries, and clinicians increasingly choose milled restorations because they can be delivered in a single visit and achieve long-term survival rates above 95% for zirconia crowns. The workflow efficiency is critical as case volumes grow, with practices reporting up to 60% chair-time reduction when milling replaces conventional lab work. Developing economies feel the greatest impact because a growing middle class now seeks aesthetic prosthetics rather than extractions. Clinics that adopted same-day solutions report measurable patient preference and willingness to pay premium fees, reinforcing revenue potential for providers.

Rapid Digitization of Dental Workflows

Scanner-to-mill connectivity has accelerated due to cloud platforms that move design files in seconds instead of minutes, allowing remote designers to finalize crowns and bridges while patients remain in the chair. Automated design tools now achieve a 94% acceptance rate for crown proposals, slashing the CAD learning curve and widening access among non-specialist teams. Integrated quality-control routines inside the mill reduce remakes and create a data feedback loop that refines preparations over time. Consequently, clinics view digital transformation less as a discretionary upgrade and more as a requirement for competitive parity.

High Up-Front & Maintenance Costs of Multi-Axis Mills

Entry-level chairside packages start near USD 100,000 before software, training, and facility upgrades are added. Diamond bur replacements can equal 20% of running costs each year, pressuring return-on-investment calculations for low-volume clinics. Leasing and pay-per-restoration schemes are gaining traction, but residual value uncertainties and service commitments still deter some buyers. Capital shortages are more acute in emerging markets, where financing rates remain higher and currency volatility raises import costs. Vendors respond with modular designs that let practices add spindles or tool magazines over time, aligning cash flow with growing case loads.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Dental Service Organizations & Centralized Milling Hubs

- Escalating Demand for High-Aesthetic Materials Requiring Precision Milling

- Digital Workflow Integration & Training Barriers for Small Clinics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In-Lab platforms generated 64.40% of 2025 revenue, underscoring their central role in high-capacity laboratories that supply multiple clinics. The typical installation supports multi-material carousels, continuous spindle operation, and automatic disc management, enabling daily output far above chairside units. Laboratories leverage this scale to deliver consistent restorations for broad patient groups, keeping the dental milling machine market anchored in centralized production.

The In-Office category expands at 10.36% CAGR because same-day dentistry improves scheduling and increases case acceptance. Modern compact mills now handle zirconia bridges alongside single crowns, closing the gap with laboratory systems. Practices report that monthly production doubles within four months of adoption as teams gain confidence in digital steps. This productivity spike strengthens the economic case for ownership, sustaining robust demand.

Four-axis equipment held 55.30% of the dental milling machine market share in 2025 due to affordability and ease of use, offering sufficient articulation for standard crowns and inlays. Users appreciate straightforward toolpaths and shorter setup times that support lean laboratory operations.

Five-axis solutions, however, expand at 11.55% CAGR because they cut undercuts, screw-access channels, and full-arch frameworks without repositioning. The extra degrees of freedom improve cervical fit and margin integrity, reducing chairside adjustments after delivery. Laboratories that incorporate five-axis stations secure more implant and aesthetic work, a profitable niche that propels equipment upgrades across the dental milling machine industry.

Geography Analysis

North America contributed 37.60% of global revenue in 2025, supported by sophisticated insurance reimbursement and early CAD/CAM rollout. Approximately 15% of clinics perform in-office milling, and service organizations have standardized equipment procurement to streamline support contracts. Capital spending also benefits from favorable leasing conditions that make hardware renewal predictable every five years.

Europe stands as the second-largest region, with regulatory harmonization accelerating product launches. German and Scandinavian manufacturers pioneer multi-layer zirconia and energy-efficient spindles that appeal to laboratories focused on sustainability. Strict data-privacy rules encourage vendors to build secure cloud connectors, improving adoption among practice networks that exchange designs across borders. The dental milling machine market here is shaped by independent labs that stress craft quality, creating demand for precision upgrades rather than outright capacity expansion.

Asia-Pacific records a 12.95% CAGR, the fastest worldwide, fueled by rising disposable income and vibrant dental tourism in Thailand and India. China quickly scales domestic production, narrowing the technology gap with Western incumbents, while Japan applies its expertise in precision engineering to develop compact five-axis mills tailored for small urban clinics. Public health initiatives in several countries now reimburse CAD/CAM crowns, spurring clinics to add mills. Middle East and Africa and South America show moderate growth; Brazil leads South America due to its established dental manufacturing cluster, whereas Gulf Cooperation Council nations invest heavily in modern clinics aimed at medical tourists.

- Solventum Corporation

- Dentsply Sirona

- Amann Girrbach

- Planmeca

- Roland DG Corp. (DGSHAPE)

- Zirkonzahn GmbH

- vhf camfacture AG

- Datron

- imes-icore GmbH

- Straumann Group

- Renishaw plc

- Pritidenta GmbH

- Axsys Dental Solutions

- Yenadent Ltd.

- B&D Dental Technologies

- Ivoclar Vivadent

- Zimmer Biomet

- KaVo Kerr (Envista)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Burden of Untreated Dental Caries & Tooth Loss

- 4.2.2 Rapid Digitization of Dental Workflows (Scanner-CAD-Mill-Sinter)

- 4.2.3 Expansion of Dental Service Organizations & Centralized Milling Hubs

- 4.2.4 Escalating Demand for High-Aesthetic Materials (Zirconia, Li-disilicate) Requiring Precision Milling

- 4.2.5 Government-Backed Insurance Expansion for Prosthetic Restorations

- 4.3 Market Restraints

- 4.3.1 High Up-Front & Maintenance Costs of Multi-Axis Mills

- 4.3.2 Digital Workflow Integration & Training Barriers for Small Clinics

- 4.3.3 Competition from Additive Manufacturing and Outsourced Labs

- 4.4 Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Machine Type

- 5.1.1 In-Lab Milling Machines

- 5.1.2 In-Office Milling Machines

- 5.2 By Axis Configuration

- 5.2.1 4-Axis Machines

- 5.2.2 5-Axis Machines

- 5.3 By Size

- 5.3.1 Table-top

- 5.3.2 Bench-top

- 5.3.3 Stand-alone

- 5.4 By Technology

- 5.4.1 CAD/CAM Milling

- 5.4.2 Copying Milling

- 5.5 By End-User

- 5.5.1 Dental Laboratories

- 5.5.2 Dental Clinics (Chair-side)

- 5.5.3 Academic & Research Institutes

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Solventum Corporation

- 6.3.2 Dentsply Sirona

- 6.3.3 Amann Girrbach AG

- 6.3.4 Planmeca Oy

- 6.3.5 Roland DG Corp. (DGSHAPE)

- 6.3.6 Zirkonzahn GmbH

- 6.3.7 vhf camfacture AG

- 6.3.8 Datron AG

- 6.3.9 imes-icore GmbH

- 6.3.10 Institut Straumann AG

- 6.3.11 Renishaw plc

- 6.3.12 Pritidenta GmbH

- 6.3.13 Axsys Dental Solutions

- 6.3.14 Yenadent Ltd.

- 6.3.15 B&D Dental Technologies

- 6.3.16 Ivoclar Vivadent AG

- 6.3.17 Zimmer Biomet Holdings Inc.

- 6.3.18 KaVo Kerr (Envista)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment