|

시장보고서

상품코드

2062009

몬탄 왁스 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Montan Wax - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

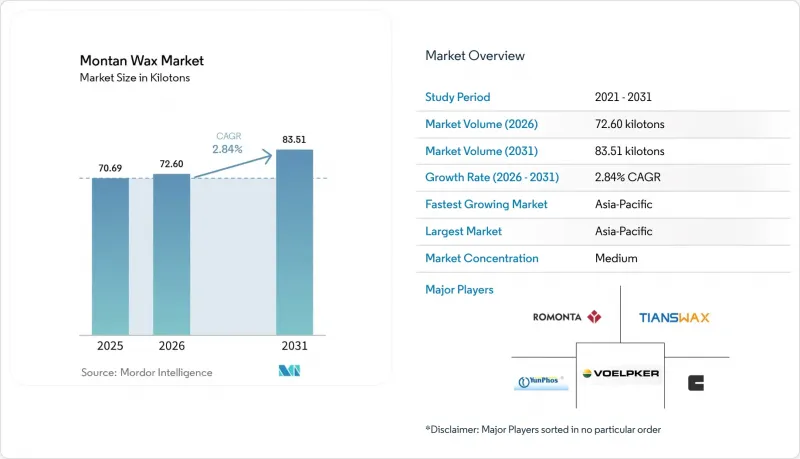

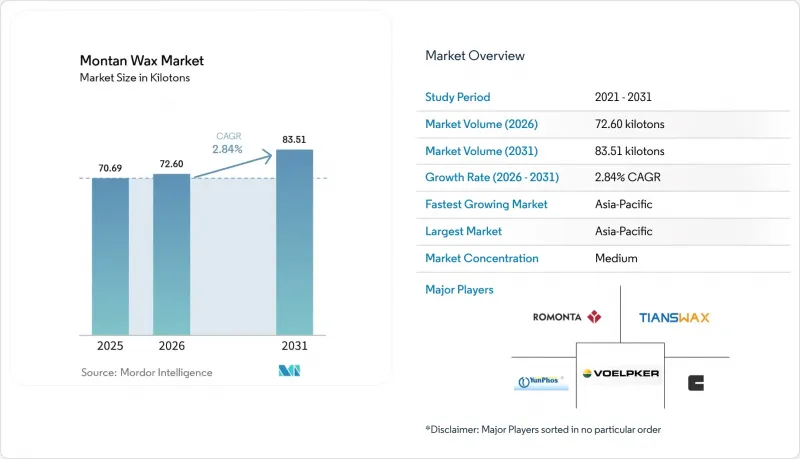

Mordor Intelligence에 의하면, 몬탄 왁스 시장 규모는 2025년 70.69 킬로톤으로 평가되었습니다. 2026년에는 72.60 킬로톤으로 확대되어 2031년까지 83.51 킬로톤에 이를 것으로 예측되며, 2026-2031년 CAGR은 2.84%를 나타낼 전망입니다.

본 보고서는 유형(조제품, 표백·정제, 개질·에스테르화), 용도(연마제, 플라스틱, 종이, 화장품, 전자기기, 기타), 최종 사용자(자동차, 플라스틱, 퍼스널케어, 포장, 전자기기, 산업용), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 수량(톤) 기준으로 제시되어 있습니다.

세계의 몬탄 왁스 시장 동향 및 인사이트

자동차용 광택제 및 디테일링용 배합제에서의 사용 확대

차량의 외관 미관이 중요시됨에 따라, 깊은 광택과 자외선 저항성을 갖추고 신속한 도포가 가능한 프리미엄 왁스 블렌드에 대한 수요가 급증하고 있습니다. 이러한 상황에서 배합 개발자들은 고융점 몽탕 등급에 대한 관심을 높이고 있습니다. 이러한 등급은 세제에 의한 부식을 견딜 뿐만 아니라, 자동 세차 시에도 보호막을 유지하기 때문에 정비 주기를 연장하고 고객 가치를 높이는 데 기여합니다. 몽탕 왁스 시장은 광택을 손상시키지 않으면서도 저VOC 기준을 충족하는 수성 분산 기술의 혜택을 누리고 있습니다. 이는 규제가 엄격한 북미 및 유럽의 소매업체들에게 특히 중요합니다. 한편, 중국과 인도에서는 확대되는 중산층이 전문적인 디테일링 수요를 주도하고 있으며, 이 지역의 블렌딩 센터에서 소비량이 두 자릿수 성장세를 기록하는 데 기여하고 있습니다. 또한, 연마 페이스트 제조업체들은 몬탄 왁스와 실리카, 알루미나, 고분자계 미세 연마제의 시너지 효과를 활용하고 있습니다. 이를 통해 도장면을 보정할 뿐만 아니라 보호 기능도 갖춘 원스텝 컴파운드를 제조할 수 있게 되었으며, 왁스의 단위당 배합량이 증가하고 있습니다.

열가소성 플라스틱 분야에서 윤활제·이형제로서 수요 증가

대량 생산을 하는 플라스틱 가공 업체들은 안정적인 용융 유동성과 신속한 사이클 타임을 최우선으로 여깁니다. 0.5%에서 3%의 몬탄 왁스를 첨가함으로써 이러한 목표를 달성할 수 있으며, 특히 폴리염화비닐(PVC)이나 폴리에틸렌테레프탈레이트(PET) 프로파일과 같은 고전단 응용 분야에서 플레이트아웃을 현저히 줄일 수 있습니다. 아시아태평양에서는 포장 및 전자기기 분야의 급증하는 수요에 대응하기 위해 압출 성형 및 사출 성형 시설이 풀가동되고 있습니다. 이러한 시설에서는 표백 및 산화 몬탄 왁스의 사용이 점점 더 늘어나고 있습니다. 이러한 왁스는 투명성이나 기계적 강도를 저해하지 않으면서 내부 윤활 효과를 제공합니다. 개질 등급, 특히 칼슘 몬타네이트는 안료의 분산을 용이하게 할 뿐만 아니라, 몬탄 왁스 시장을 활성화하고 컬러 마스터배치 제조업체에 설계상의 유연성을 제공합니다. 폴리젖산 등의 바이오 폴리머가 널리 보급되는 가운데, 에스테르화된 몬탄 왁스는 극성 소재와의 용해성 면에서 두드러진 장점을 보이며, 가공 업체가 기존 설비를 활용해 생산성을 유지할 수 있도록 보장합니다.

갈탄 매장량의 한계와 채굴 규제

조제 몬탄 왁스의 생산지로 알려진 독일의 갈탄 지대는 자원 고갈과 환경 규제 강화에 직면해 있습니다. 이러한 과제는 하류 수요가 다양화되고 있는 시기에 발생하고 있습니다. ROMONTA는 통합적인 접근 방식을 통해 사업을 전개하고 있지만, 이러한 수직 통합형 구조는 채굴 가능한 광석의 유한성이라는 한계에 직면해 있습니다. 또한, EU의 탄소 가격 규제는 2025년까지 CO2 1톤당 45유로에서 55유로로 인상될 예정입니다. 이러한 생산 비용 상승은 현물 가격을 끌어올리고 있으며, 수입 원료에 의존하는 북미 및 아시아의 가공업체들 사이에서 우려가 확산되고 있습니다. 그 결과, 몬탄 왁스 시장에서는 리드타임이 길어지고 있으며, 유통망 전반에 걸쳐 재고 비축과 선물 매수가 활발해지고 있습니다.

부문별 분석

2025년, 원료는 몬탄 왁스 시장 점유율의 60.24%를 차지했으며, 그 높은 비용 효율성을 바탕으로 아스팔트 개질제, 석고보드 발수 처리, 주조용 이형제 등의 분야에서 계약을 수주했습니다. 그러나 시장은 에스테르화 및 산화 유도체 쪽으로 점차 전환되고 있습니다. 이러한 유도체들은 더 밝은 색상, 낮은 냄새, 특정 융점 범위와 같은 특성을 중시하는 화장품, 바이오폴리머 및 전자 분야에서 점점 더 많은 지지를 얻고 있습니다. 연평균 성장률(CAGR) 3.45%를 기록하며 성장하고 있는 개질 등급 제품 역시 3D 프린팅 및 고온 섬유 방적 기술의 발전을 주도하고 있으며, 이는 몬탄 왁스 시장 전체를 견인하고 있습니다. 산가 조정이나 부분적인 비누화 같은 화학적 조정을 통해, 배합 설계자는 원료 왁스만으로는 달성할 수 없는 특수한 유변학적 특성을 구현할 수 있으며, 이를 통해 프리미엄 가격 책정을 정당화할 수 있고, 경우에 따라서는 장기 공급 계약을 확보할 수도 있습니다.

비용 차이가 30%를 초과하는 경우에도, 규정 준수나 브랜드 포지셔닝을 우선시하는 최종 소비자들은 그 추가 비용을 기꺼이 부담하고 있습니다. 이는 대체안으로서, 서로 다른 유변학 조절제에 맞추어 전체 배합을 재검토해야 하는 경우에 특히 해당됩니다. 그 결과, 개질 몬탄 왁스는 판매량에 따른 기여도를 상회하는 이익률을 기록하고 있으며, 이는 공급업체를 원자재 비용 변동으로부터 보호하고, 몬탄 왁스 시장에서 지속적인 연구개발 투자의 정당성을 입증하고 있습니다.

지역별 분석

2025년, 아시아태평양은 총 판매량의 42.20%를 차지했습니다. 이는 중국과 일본의 견고한 자동차 공급망에 더해, 인도 및 아세안(ASEAN) 국가들의 급성장 중인 퍼스널케어 제조 부문이 주도한 결과입니다. 이 지역에서는 자동차 디테일링 소모품이 프리미엄 스프레이 왁스나 세라믹 성분이 함유된 폴리시로 전환되고 있으며, 이들 제품은 모두 피막의 강도를 유지하기 위해 몬탄 왁스에 의존하고 있습니다. 한국의 K-뷰티 브랜드는 몬탄 왁스와 쌀겨 왁스를 혼합하여 지속가능성과 성능의 균형을 맞추고 있으며, 완전한 대체가 아닌 공존이라는 추세를 보이고 있습니다.

북미에서는 확립된 유통 채널과 뿌리 깊은 DIY 자동차 관리 문화를 배경으로, 세라믹 코팅의 부상이 있음에도 불구하고 여전히 견조한 수요가 이어지고 있습니다. 엄격한 VOC(휘발성 유기 화합물) 및 PFAS(퍼플루오로알킬 물질) 규제를 준수하기 위해, 배합 개발자들은 수성 몬탄 분산액으로 전환하고 있으며, 용제를 사용하지 않고도 동등한 광택을 구현함으로써 해당 지역의 몬탄 왁스 시장을 견인하고 있습니다. 또한, 멕시코에서는 플라스틱 가공 부문이 확대되고 있으며, 사출 성형된 소비재를 위해 정제 등급 원료를 수입하고 있어, 이로 인해 해당 대륙에서의 소비가 정착되어 가고 있습니다.

유럽은 몬탄왁스 시장의 발상지일 뿐만 아니라, 그 실증의 장이기도 합니다. ROMONTA나 Volpker와 같은 독일 생산자들은 품질과 전문 지식 면에서 세계적 기준을 확립하고 있지만, 탄소 가격 제도나 갈탄 고갈과 같은 과제들이 사업 확장을 가로막고 있습니다. 동시에, EU의 규제 관련 과제가 저PAH 식품 접촉 적합 등급 제품 생산을 목표로 하는 연구 개발(R&D) 노력을 뒷받침하고 있습니다. 이 시점에서 성공적으로 방향을 전환한다면, 새로운 성장 기회를 열어갈 수 있을 것입니다. 앞으로 대체품의 위협이 커짐에 따라, 유럽 기업들은 원자재 제약이 비교적 적은 아시아에서 합작 사업을 전개하게 될 가능성이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the montan wax market size is expected to increase from 70.69 kilotons in 2025 to 72.60 kilotons in 2026 and reach 83.51 kilotons by 2031, growing at a CAGR of 2.84% over 2026-2031.

This report is Segmented by Type (Crude, Bleached/Refined, Modified/Esterified), Application (Polishes, Plastics, Paper, Cosmetics, Electronics, Other), End-User (Automotive, Plastics, Personal Care, Packaging, Electronics, Industrial), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (tons).

Global Montan Wax Market Trends and Insights

Growing Use in Automotive Polishes and Detailing Formulations

As vehicle aesthetics gain prominence, the demand for premium wax blends that offer deep gloss, UV resistance, and quick application has surged. In this landscape, formulators are increasingly gravitating toward high-melting montan grades. These grades not only resist detergent attacks but also uphold protective films during automated washes, leading to extended service intervals and heightened perceived value. The montan wax market is reaping the benefits of water-borne dispersion technology, which adheres to low-VOC standards without compromising on shine. This is particularly important for retailers in North America and Europe, where regulatory oversight is strict. Meanwhile, in China and India, a growing middle class is fueling a professional detailing surge, bolstering double-digit consumption growth in regional blending centers. Additionally, manufacturers of polishing pastes are capitalizing on montan wax's synergy with silica, alumina, and polymer micro-abrasives. This allows them to craft single-step compounds that not only correct but also safeguard paint surfaces, resulting in increased per-unit wax loadings.

Expanding Demand as Lubricant/Release Agent in Thermoplastics

High-volume plastics processors prioritize consistent melt flow and rapid cycle times. By adding 0.5% to 3% montan wax, they achieve these objectives and notably reduce plate-out, especially in high-shear applications like polyvinyl chloride and polyethylene terephthalate profiles. In the Asia-Pacific region, extrusion and injection-molding facilities are running at full capacity to meet the surging demands of packaging and electronics. These facilities are increasingly turning to bleached and oxidized montan waxes. These waxes offer internal lubrication benefits without sacrificing clarity or mechanical strength. Modified grades, especially calcium montanate, not only facilitate easy pigment dispersion but also bolster the montan wax market, granting color-masterbatch producers greater design flexibility. As biopolymers like polylactic acid gain popularity, esterified montan wax stands out for its polar compatibility, ensuring processors can maintain productivity on their current equipment.

Limited Lignite Reserves and Mining Restrictions

Germany's lignite belts, known for their crude montan wax production, are facing resource depletion and tighter environmental regulations. These challenges come at a time when downstream demand is diversifying. While ROMONTA operates with an integrated approach, its vertically aligned structure struggles against the finite limits of accessible ore. Furthermore, EU carbon-pricing regulations are set to rise from EUR 45 to EUR 55 per tonne of CO2 by 2025. This increase in production costs is pushing spot prices higher, causing concern among converters in North America and Asia who depend on imported feedstock. As a result, the montan wax market is experiencing extended lead times, leading to inventory hoarding and forward-buying across distributor networks.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption in Cosmetics and Personal-Care Emulsions

- Rapid Uptake in 3-D-Printing Filament Surface Modifiers

- Substitution Threat from Synthetic and Bio-Based Waxes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, crude material clinched 60.24% of the montan wax market share, leveraging its cost-effectiveness to secure contracts in asphalt modifiers, gypsum-board hydrophobization, and foundry release agents. However, the market is shifting toward esterified and oxidized derivatives. These derivatives are increasingly favored by the cosmetic, biopolymer, and electronics sectors, which prioritize attributes like lighter color, reduced odor, and specific melting-point ranges. Modified grades, growing at a 3.45% CAGR, are also driving advancements in 3-D printing and high-temperature fiber-spinning, bolstering the overall montan wax market. Through chemical tailoring such as acid-number adjustment and partial saponification, formulators can achieve niche rheological targets unattainable by crude wax, justifying premium pricing and, in certain instances, securing long-term offtake agreements.

Even when the cost difference can surpass 30%, end users, prioritizing regulatory compliance and brand positioning, willingly absorb the extra expense. This is particularly true when the alternative involves overhauling an entire formulation to fit a different rheology modifier. As a result, modified montan wax enjoys a profit margin that exceeds its volume contribution, shielding suppliers from fluctuations in raw material costs and underscoring the rationale for sustained R&D investments in the montan wax market.

Geography Analysis

In 2025, Asia-Pacific accounted for 42.20% of the volume, driven by a robust automotive supply chain in China and Japan, coupled with a burgeoning personal-care manufacturing sector in India and ASEAN. In the region, automotive detailing consumables are gravitating toward premium spray waxes and ceramic-infused polishes, both of which depend on montan wax for their film integrity. South Korean K-beauty brands are blending montan wax with rice-bran wax, striking a balance between sustainability and performance, indicating a trend of coexistence over outright substitution.

North America, with its established distribution channels and a strong DIY car care culture, continues to see robust demand, even with the rise of ceramic coatings. In response to stringent VOC and PFAS regulations, formulators are pivoting to water-borne montan dispersions, achieving similar gloss without solvents, bolstering the regional montan wax market. Additionally, Mexico's expanding plastics processing sector is importing refined grades for its injection-molded consumer goods, solidifying the continent's consumption.

Europe stands as both the birthplace and a testing ground for the montan wax market. While German producers like ROMONTA and Volpker set global standards for quality and expertise, challenges like carbon-pricing schemes and lignite depletion hinder their expansion. Concurrently, EU regulatory challenges are spurring R&D initiatives aimed at producing low-PAH, food-contact-compliant grades. A successful pivot here could pave the way for new growth opportunities. Looking ahead, potential substitution threats might drive European firms to forge joint ventures in Asia, where feedstock limitations are less pronounced.

- AmeriLubes LLC

- Blended Waxes Inc.

- Brother ( Japan )

- Carmel Industries

- Clariant

- Deurex AG

- Dhariwal Corp Ltd.

- Excel International

- Huber Engineered Materials

- Koster Keunen

- Paraffinwaxco Inc.

- Poth Hille

- Pramelt B.V.

- ROMONTA Group

- Strahl & Pitsch Inc.

- Ter Hell & Co. GmbH

- TianshiWax

- Volpker Spezialprodukte GmbH

- Volwax (Yunnan Shangcheng)

- Yunphos

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing use in automotive polishes and detailing formulations

- 4.2.2 Expanding demand as lubricant/release agent in thermoplastics

- 4.2.3 Rising adoption in cosmetics and personal-care emulsions

- 4.2.4 Rapid uptake in 3-D-printing filament surface modifiers

- 4.2.5 Utilisation in encapsulating hazardous-waste barriers

- 4.3 Market Restraints

- 4.3.1 Limited lignite reserves and mining restrictions

- 4.3.2 Substitution threat from synthetic and bio-based waxes

- 4.3.3 Tightening EU-REACH limits on PAH traces in waxes

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Crude Montan Wax

- 5.1.2 Bleached / Refined Montan Wax

- 5.1.3 Modified / Esterified Montan Wax

- 5.2 By Application

- 5.2.1 Polishes and Coatings

- 5.2.2 Plastic Processing

- 5.2.3 Paper Coatings

- 5.2.4 Cosmetics and Personal Care

- 5.2.5 Electronics Wire-Enamelling and Solder-Mask

- 5.2.6 Other Applications (Rubber, Electrical Insulation, 3-D Printing)

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Plastics and Polymers

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Packaging and Paper

- 5.3.5 Electrical and Electronics

- 5.3.6 Industrial and Construction

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 AmeriLubes LLC

- 6.4.2 Blended Waxes Inc.

- 6.4.3 Brother ( Japan )

- 6.4.4 Carmel Industries

- 6.4.5 Clariant

- 6.4.6 Deurex AG

- 6.4.7 Dhariwal Corp Ltd.

- 6.4.8 Excel International

- 6.4.9 Huber Engineered Materials

- 6.4.10 Koster Keunen

- 6.4.11 Paraffinwaxco Inc.

- 6.4.12 Poth Hille

- 6.4.13 Pramelt B.V.

- 6.4.14 ROMONTA Group

- 6.4.15 Strahl & Pitsch Inc.

- 6.4.16 Ter Hell & Co. GmbH

- 6.4.17 TianshiWax

- 6.4.18 Volpker Spezialprodukte GmbH

- 6.4.19 Volwax (Yunnan Shangcheng)

- 6.4.20 Yunphos

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Smart functional coatings for recyclable paper-based packaging