|

시장보고서

상품코드

2062031

TPM(Trusted Platform Module) : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Trusted Platform Module (TPM) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

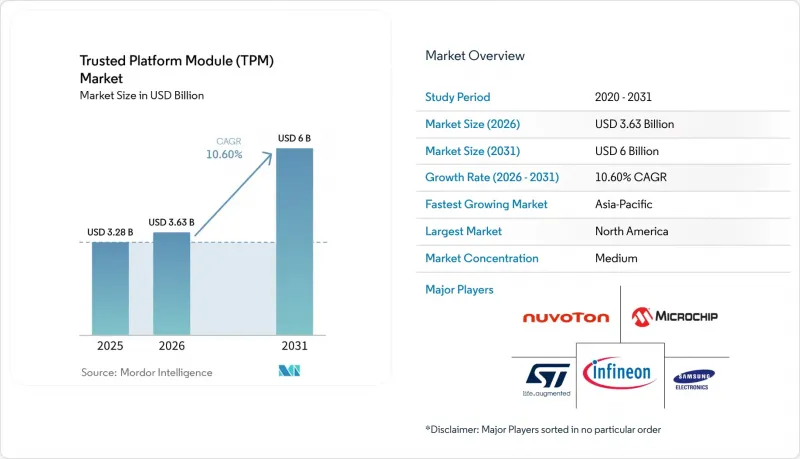

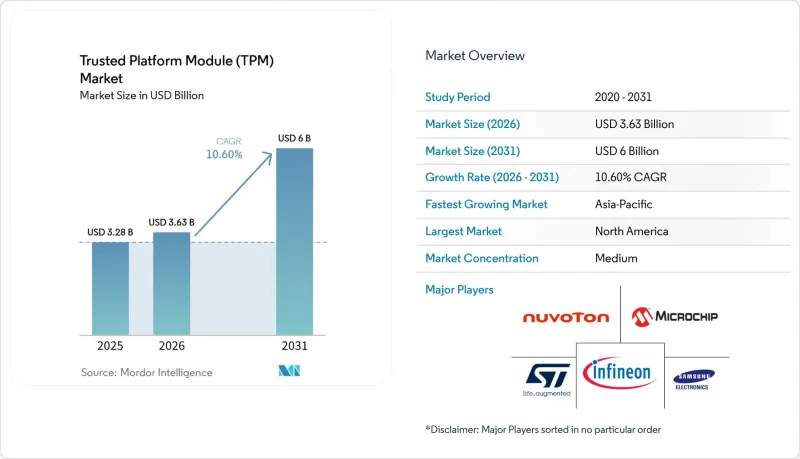

Mordor Intelligence에 의하면, TPM(Trusted Platform Module) 시장 규모는 2025년에 32억 8,000만 달러로 평가되었습니다. 2026년 36억 3,000만 달러에서 2031년까지 60억 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 10.60%를 나타낼 전망입니다.

본 보고서는 TPM의 유형(디스크리트 TPM(dTPM) 등), 호스트 인터페이스(SPI/ESPI, I2C/I3C, LPC 등), 최종 용도 기기(데스크톱·노트북, 서버·데이터센터 플랫폼, IoT·임베디드 시스템, 자동차용 전자기기 등), 산업별(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 의료 및 생명과학 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

세계의 TPM(Trusted Platform Module) 시장 동향 및 인사이트

데스크톱 및 서버에서 하드웨어 기반 ‘Root of Trust’의 도입 확대

하드웨어 기반 신뢰의 근간이 선택적 업그레이드에서 필수적인 보안 계층으로 전환됨에 따라, TPM(Trusted Platform Module) 시장 수요가 증가하고 있습니다. 마이크로소프트는 BitLocker, Windows Hello for Business, 가상화 기반 보안 등 Windows 11의 보안 기능의 핵심으로 TPM 2.0을 자리매김하고 있습니다. 이러한 신뢰의 기반은 현재 Microsoft Pluton을 최신 프로세서 제품군에 통합한 새로운 클라이언트 플랫폼으로까지 확대되고 있으며, 하드웨어 기반의 신원 인증 기능이 표준 디바이스 아키텍처의 더 깊은 부분까지 통합되고 있습니다. 네트워크 인프라에서도 유사한 경향이 나타나고 있으며, IETF RFC 9683에 따라 TPM이 탑재된 라우터, 스위치, 방화벽을 위한 원격 무결성 검증 워크플로가 공식적으로 규정되었습니다. 이에 따라 시장의 서비스 제공 대상은 기존의 PC에 그치지 않고 서버, 네트워크 장비, 클라우드 인프라로 확대되고 있습니다.

Windows 11 업그레이드 주기에서 TPM 2.0의 필수 요건

Windows 10 지원 종료 시한에 따라 TPM 시장은 OS 전환으로 인한 직접적인 혜택을 받게 되었습니다. 마이크로소프트는 Windows 11에서도 TPM 2.0을 필수 보안 요건으로 계속 지정하고 있습니다. 이 기준에 따라 기업들은 계획보다 일찍 도입된 기기들을 평가할 수밖에 없게 되었습니다. 왜냐하면, 이 요건을 충족하지 못하는 기기는 장기적인 서비스 주기 동안 운영을 지속하기 어려워지기 때문입니다. 이 요구 사항은 TPM 2.0을 보안 부팅, UEFI, 장치 ID, 측정된 부팅 프로세스와 연계하여 보다 광범위한 엔드포인트 보안 스택을 강화하는 것입니다. 그 결과, 소프트웨어 전환은 시장 전체에서 하드웨어 조달과 유사한 성격을 띠게 되었습니다.

45nm 및 그 이전의 트러스트드 파운드리 노드에서 나타나는 공급망의 불안정성

성숙한 노드에서공급 부족은 여전히 TPM 시장에 직접적인 걸림돌이 되고 있습니다. 디스크리트 TPM의 설계는 40-90nm 공정에 의존하며, 이 공정에서는 밀도 향상보다 변조 방지, 차폐, 사이드 채널 보호가 더 중요하게 여겨집니다. 이 카테고리의 제품군은 대개 긴 수명과 가혹한 작동 조건을 가정하여 설계되었기 때문에 공급업체가 인증이나 수명 주기 약속에 영향을 미치지 않으면서 새로운 제조 공정으로 전환할 수 있는 속도에는 한계가 있습니다. 보안 인증 및 플랫폼 수준의 검증 역시 공급처 변경을 지연시키는 요인이 되며, 제조 및 규정 준수 분야에서 풍부한 경험을 보유한 기존 공급업체에 유리하게 작용합니다. 그 결과, 수요가 견조하더라도 인증된 노드에서공급 차질이 단기적인 시장 확대를 제한할 가능성이 있습니다.

부문별 분석

2025년, 디스크리트 TPM은 TPM(Trusted Platform Module) 시장 점유율의 48.8%를 차지했으며, 이는 기업 및 정부 구매자들이 키 저장 및 신뢰성 검증에 있어 여전히 물리적 분리를 중요하게 여기고 있음을 보여줍니다. 그 위상은 변조 방지 패키지, 독립된 전원 도메인, 인증의 깊이가 조달 결정에 직접적인 영향을 미치는 시스템에서 여전히 가장 견고합니다. 통합형 TPM 및 펌웨어 TPM 솔루션은 별도의 구성 요소가 필요 없이 보안 기능을 추가할 수 있기 때문에 PC 및 모바일 플랫폼에서 그 입지를 넓혀가고 있습니다. 이로 인해 디스크리트 부품 공급업체들은 기본적인 공급 능력보다는 인증 실적, 공급망 추적성, 장기적인 라이프사이클 지원 측면에서 경쟁을 벌여야 하는 상황에 놓여 있습니다.

가상 TPM(vTPM)은 2026년부터 2031년까지 연평균 성장률(CAGR) 12.8%를 나타낼 것으로 예측되며, TPM 시장에서 가장 빠르게 성장하는 포맷이 될 전망입니다. 또한, 업계에서는 클라우드 환경이나 엣지 AI 시스템에서 vTPM 및 fTPM이 점차 보급되고 있습니다. 이러한 환경에서는 소프트웨어를 통한 신뢰 관리가 새로운 이산형 하드웨어보다 더 신속하게 확장될 수 있기 때문입니다. ARM 기반 임베디드 아키텍처에 대한 조사 결과, 이미 펌웨어 주도형 신뢰 모델 내에서 구현 가능한 포스트 양자 인증 경로가 제시되었습니다. wolfSSL이 2026년 5월에 출시한, ML-DSA 및 ML-KEM을 지원하는 펌웨어 TPM은 네이티브 PQC 실리콘이 널리 보급되기 전에 공급업체들이 이러한 요구에 어떻게 대응하고 있는지를 보여줍니다.

SPI/eSPI는 2025년에도 시장 점유율 46.7%를 유지했으며, 이는 상용 PC 및 산업용 임베디드 시스템 분야에서 폭넓게 도입된 실적을 반영한 것입니다. 이러한 보급 현황으로 인해 새로운 플랫폼 설계에서는 더 높은 처리량을 제공하는 연결 방식이 선호되더라도, 이 인터페이스는 여전히 중요한 위치를 차지하고 있습니다. LPC 역시 여전히 중요한 레거시 인프라를 지원하고 있지만, 서버와 데이터센터 아키텍처가 구식 버스 설계에서 점차 벗어나면서 그 역할은 축소되고 있습니다. Trusted Platform Module(TPM) 시장에서는 호스트 인터페이스의 선택이 순수한 보안 기능과 마찬가지로 공급업체 선정, 인증 작업, 업데이트 시기에 영향을 미치고 있습니다.

PCIe/USB 시장은 2026년부터 2031년까지 연평균 성장률(CAGR) 13.7%를 나타낼 것으로 예측되며, 이는 현대 서버 인프라 설계에서 광범위한 플랫폼 전환이 이루어지고 있음을 시사합니다. 이러한 변화는 중요한 의미를 지닙니다. 왜냐하면 인터페이스 전환에는 시스템 수준의 재인증이 필요한 경우가 많으며, 새로운 아키텍처에 대응하는 공급업체에게는 조달 기회가 생기기 때문입니다. 또한, 핀 수 감축이 중요한 자동차 및 IoT 이용 사례에서도 I2C와 I3C의 점유율이 확대되고 있으며, I3C는 차세대 제어 및 인증 워크로드를 위해 높은 처리량을 제공합니다. STMicroelectronics는 SPI 또는 I2C 옵션, FIPS 140-3 및 Common Criteria EAL4+ 인증을 지원하며, -40°C에서 105°C의 작동 온도 범위와 20년의 제품 수명을 갖춘 산업용 모델을 포함한 ST33KTPM 제품군을 통해 이러한 요구 사항을 충족하고 있습니다.

지역별 분석

2025년, 북미는 TPM(Trusted Platform Module) 시장 점유율의 38.2%를 차지하며, 지역별로는 가장 큰 기여도를 보였습니다. 미국은 여전히 핵심적인 위치를 차지하고 있으며, 연방 정부의 조달 요건, 클라우드 보증에 대한 요구, 기업의 보안 기준 덕분에 인증된 실리콘에 대한 안정적인 수요가 유지되고 있습니다. 또한, 하이퍼스케일 데이터센터의 밀집된 집적도 TPM 시장 전체에서 서버 측 도입 확대를 뒷받침하고 있습니다. 캐나다는 디지털 정부 프로그램과 금융 부문의 보안 요건을 통해 규모는 작지만 중요한 역할을 수행하고 있습니다. 북미 시장에서 신뢰할 수 있는 공급업체를 선호하는 경향은 인증받은 개별 TPM 공급업체의 가격 결정력을 유지하는 데 도움이 되고 있습니다.

아시아태평양은 2026년부터 2031년까지 연평균 성장률(CAGR) 12.4%를 나타낼 것으로 예측되며, TPM(Trusted Platform Module) 시장에서 가장 빠르게 성장하는 지역 부문이 될 전망입니다. 일본, 한국, 중국, 인도는 모두 자동차, 반도체, 커넥티드 기기 분야의 활발한 활동을 통해 이러한 성장 가속화에 기여하고 있습니다. 중국에서 GB 44495가 도입됨에 따라, 해당 지역 전체에서 보안이 강화된 차량용 전자기기에 대한 규정 준수 수요가 확대되고 있습니다. 한국에서는 삼성의 5nm 공정으로 제조된 BOS Semiconductors사의 자동차용 AI 가속기 ‘Eagle-N’에, 인증된 부팅 및 보호된 무선 업데이트(OTA)를 구현하는 램버스(Rambus)사의 보안 IP가 통합되어 있어, 이러한 추세가 확산되고 있음을 보여주고 있습니다. 또한, Trusted Computing Group(TCG)의 일본 지역 포럼을 통해서도 아시아태평양의 표준화 노력이 생태계 전반에 걸쳐 보다 광범위한 확산을 뒷받침할 만큼 성숙해졌음이 드러났습니다.

유럽은 두 번째로 큰 지역 시장이며, 독일, 영국, 프랑스가 주요 수요 거점입니다. Windows 11로의 전환 요건과 EU 사이버 복원력 법에 따라, 기업 및 제품 보안의 전반적인 이용 사례 전반에 걸쳐 인증된 하드웨어 루트 오브 트러스트의 도입이 더욱 확대되고 있습니다. 남미, 중동 및 아프리카는 여전히 도입 초기 단계에 있는 지역으로, 도입은 일반 기업의 대규모 교체 주기보다는 정부, 국방, 통신 프로젝트에 집중되어 있습니다. 이 지역들은 현재로서는 규모가 작지만, 인프라의 디지털화와 국가 차원의 사이버 보안 투자에 힘입어 향후 TPM(Trusted Platform Module) 시장의 역할이 확대될 것으로 전망됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the trusted platform module (TPM) market size was valued at USD 3.28 billion in 2025 and estimated to grow from USD 3.63 billion in 2026 to reach USD 6.00 billion by 2031, at a CAGR of 10.60% during the forecast period (2026-2031).

This report is Segmented by TPM Type (Discrete TPM (dTPM), and More), Host-Interface (SPI/ESPI, I2C/I3C, LPC, and More), End-Use Device (PCs and Laptops, Servers and Data-Center Platforms, Iot and Embedded Systems, Automotive Electronics, and More), Industry Vertical (IT and Telecom, BFSI, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Trusted Platform Module (TPM) Market Trends and Insights

Growing Adoption of Hardware-Based Root of Trust in PCs and Servers

Demand in the Trusted Platform Module (TPM) market has strengthened as the hardware root of trust has shifted from an optional upgrade to a required security layer. Microsoft places TPM 2.0 at the center of Windows 11's protections, including BitLocker, Windows Hello for Business, and virtualization-based security.That same trust anchor now extends to newer client platforms that integrate Microsoft Pluton into modern processor families, moving hardware-backed identity deeper into standard device architecture. Network infrastructure is also adopting this pattern, as IETF RFC 9683 formalized remote integrity verification workflows for routers, switches, and firewalls that contain TPMs.This expands the market's serviceable base beyond traditional PCs into servers, networking equipment, and cloud infrastructure.

Mandatory TPM 2.0 Requirement for Windows 11 Upgrade Cycle

The Windows 10 support deadline turned the TPM market into a direct beneficiary of operating system migration. Microsoft continues to treat TPM 2.0 as a non-negotiable security requirement in Windows 11. That baseline forces enterprises to assess their installed fleets earlier than planned, because devices that cannot meet the requirement become harder to keep in place over long service cycles. The same expectation reinforces a broader endpoint security stack that links TPM 2.0 with secure boot, UEFI, device identity, and measured startup processes. The result is that a software transition now behaves like a hardware procurement event across the market.

Supply Chain Volatility for 45 Nm and Older Trusted Foundry Nodes

Supply tightness at mature nodes remains a direct brake on the TPM market. Discrete TPM designs depend on 40-90nm processes where tamper resistance, shielding, and side-channel protection matter more than density gains. Product families in this category are often designed for long life and harsh operating conditions, which limits how quickly vendors can move to new manufacturing paths without affecting qualification and lifecycle commitments. Security certification and platform-level validation also slow down sourcing changes, which favors incumbents with deep manufacturing and compliance experience. As a result, supply disruptions at qualified nodes can limit near-term market expansion even when demand remains firm.

Other drivers and restraints analyzed in the detailed report include:

- Rising Cyber-Insurance Premiums Driving Demand for Certified Secure Elements

- Automotive UNECE R155/R156 Compliance Accelerating Secure ECU Rollouts

- Cost-Sensitive IoT Nodes Opting for Lightweight Crypto Alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Discrete TPM held 48.8% of the trusted platform module (TPM) market share in 2025, which shows that enterprise and government buyers still place a premium on physical separation for key storage and trust validation. Its position remains strongest in systems where tamper-resistant packaging, independent power domains, and certification depth directly shape procurement decisions. Integrated TPM and firmware TPM solutions continue to gain presence in PCs and mobile platforms because they add security functions without requiring a separate component. This is pushing discrete suppliers to compete less on basic availability and more on certification history, supply-chain provenance, and long-term lifecycle support.

Virtual TPM is projected to grow at a 12.8% CAGR from 2026 to 2031, making it the fastest-growing format in the TPM market. The industry is also seeing vTPM and fTPM gain traction in cloud environments and edge AI systems, where software-managed trust can scale faster than new discrete hardware. Research on ARM-based embedded architectures already points to post-quantum attestation paths that can be implemented within firmware-led trust models. wolfSSL's May 2026 firmware TPM release with ML-DSA and ML-KEM support shows how vendors are responding to that need before native PQC silicon becomes widely available.

SPI/eSPI retained 46.7% of the market in 2025, reflecting its broad installed base across commercial PCs and embedded industrial systems. That footprint keeps the interface relevant even as newer platform designs favor higher-throughput connections. LPC still supports a meaningful legacy base, but its role is narrowing as server and data-center architectures move away from older bus designs. In the Trusted Platform Module (TPM) market, host-interface selection now affects supplier choice, qualification work, and upgrade timing as much as raw security capability.

PCIe/USB is forecast to grow at a 13.7% CAGR from 2026 to 2031, indicating a broader platform shift in modern server and infrastructure designs. This change matters because interface migration often requires system-level requalification and opens procurement windows for vendors aligned with the new architecture. I2C and I3C are also gaining share in automotive and IoT use cases where lower pin counts matter, and I3C offers higher throughput for next-generation control and attestation workloads. STMicroelectronics addresses these needs through its ST33KTPM family with SPI or I2C options, FIPS 140-3 and Common Criteria EAL4+ certification, and industrial variants rated from -40°C to 105°C with a 20-year product lifetime.

Geography Analysis

North America held 38.2% of the trusted platform module (TPM) market share in 2025, which made it the largest regional contributor. The United States remains the anchor because federal procurement expectations, cloud assurance needs, and enterprise security baselines keep certified silicon in steady demand. A dense concentration of hyperscale data centers also supports stronger server-side deployment across the Trusted Platform Module (TPM) market. Canada adds a smaller but meaningful layer through digital government programs and financial-sector security requirements. North America's preference for trusted sourcing helps preserve pricing power for qualified discrete TPM suppliers.

Asia-Pacific is projected to grow at a 12.4% CAGR from 2026 to 2031, making it the fastest-growing regional segment of the trusted platform module (TPM) market. Japan, South Korea, China, and India are all contributing to this acceleration through stronger automotive, semiconductor, and connected-device activity. China's GB 44495 rollout is widening the compliance pull for secure vehicle electronics across the region. South Korea shows the depth of this movement, with Rambus security IP integrated into BOS Semiconductors' Eagle-N automotive AI accelerator on Samsung's 5nm process for authenticated startup and protected over-the-air updates. The Trusted Computing Group's Japan Regional Forum also shows that standards engagement in Asia-Pacific is mature enough to support broader deployment across the ecosystem.

Europe is the second-largest regional market, with Germany, the United Kingdom, and France as principal demand centers. Windows 11 migration requirements and the EU Cyber Resilience Act are reinforcing the case for certified hardware roots of trust across enterprise and product-security use cases. South America, the Middle East, and Africa remain earlier-stage regions where adoption is concentrated in government, defense, and telecom projects rather than mass enterprise refresh cycles. These regions are still smaller today, but infrastructure digitization and sovereign cybersecurity investment should support a broader role for the Trusted Platform Module (TPM) market over time.

- Infineon Technologies AG

- Nuvoton Technology Corp.

- STMicroelectronics N.V.

- Microchip Technology Inc.

- Samsung Electronics Co. Ltd.

- Renesas Electronics Corp.

- Texas Instruments Inc.

- Intel Corp.

- Advanced Micro Devices Inc.

- Marvell Technology Inc.

- Broadcom Inc.

- Winbond Electronics Corp.

- IBM Corp.

- Cisco Systems Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Co.

- Lenovo Group Ltd.

- Google LLC

- Microsoft Corp.

- Huawei Technologies Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of Hardware-Based Root of Trust in PCs and Servers

- 4.2.2 Mandatory TPM 2.0 Requirement for Windows 11 Upgrade Cycle

- 4.2.3 Rising Cyber-Insurance Premiums Driving Demand for Certified Secure Elements

- 4.2.4 Automotive UNECE R155/R156 Compliance Accelerating Secure ECU Rollouts

- 4.2.5 Edge AI Inference Platforms Requiring Hardware Security for Model IP Protection

- 4.2.6 Quantum-Resistant Firmware Initiatives Boosting Next-Gen TPM Refresh

- 4.3 Market Restraints

- 4.3.1 Supply Chain Volatility for 45 nm and Older Trusted Foundry Nodes

- 4.3.2 Cost-Sensitive IoT Nodes Opting for Lightweight Crypto Alternatives

- 4.3.3 Fragmented Attestation Standards Across Cloud, Edge, and Automotive Domains

- 4.3.4 Emerging Zero-Trust Architectures Reducing Reliance on Local TPMs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Degree of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By TPM Type

- 5.1.1 Discrete TPM (dTPM)

- 5.1.2 Integrated TPM (iTPM/Platform Trust Tech)

- 5.1.3 Firmware TPM (fTPM)

- 5.1.4 Virtual TPM (vTPM/Software)

- 5.2 By Host-Interface

- 5.2.1 SPI/eSPI

- 5.2.2 I2C/I3C

- 5.2.3 LPC

- 5.2.4 PCIe/USB

- 5.3 By End-Use Device Category

- 5.3.1 PCs and Laptops

- 5.3.2 Servers and Data-Center Platforms

- 5.3.3 IoT and Embedded Systems

- 5.3.4 Automotive Electronics

- 5.3.5 Industrial Control and Automation

- 5.3.6 Mobile and Consumer Devices

- 5.3.7 Other End-Use Device Categories

- 5.4 By Industry Vertical

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Government and Defense

- 5.4.5 Retail and Commerce

- 5.4.6 Other Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Infineon Technologies AG

- 6.4.2 Nuvoton Technology Corp.

- 6.4.3 STMicroelectronics N.V.

- 6.4.4 Microchip Technology Inc.

- 6.4.5 Samsung Electronics Co. Ltd.

- 6.4.6 Renesas Electronics Corp.

- 6.4.7 Texas Instruments Inc.

- 6.4.8 Intel Corp.

- 6.4.9 Advanced Micro Devices Inc.

- 6.4.10 Marvell Technology Inc.

- 6.4.11 Broadcom Inc.

- 6.4.12 Winbond Electronics Corp.

- 6.4.13 IBM Corp.

- 6.4.14 Cisco Systems Inc.

- 6.4.15 Dell Technologies Inc.

- 6.4.16 Hewlett Packard Enterprise Co.

- 6.4.17 Lenovo Group Ltd.

- 6.4.18 Google LLC

- 6.4.19 Microsoft Corp.

- 6.4.20 Huawei Technologies Co. Ltd.

7 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment