|

시장보고서

상품코드

2062112

염소산칼륨 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Potassium Chlorate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

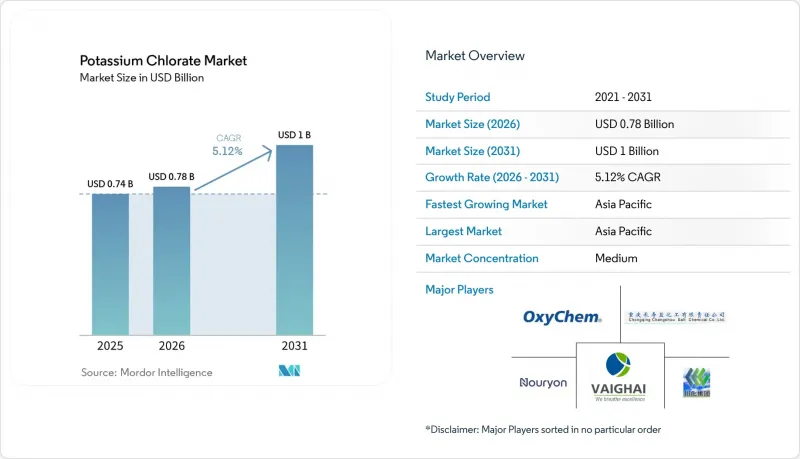

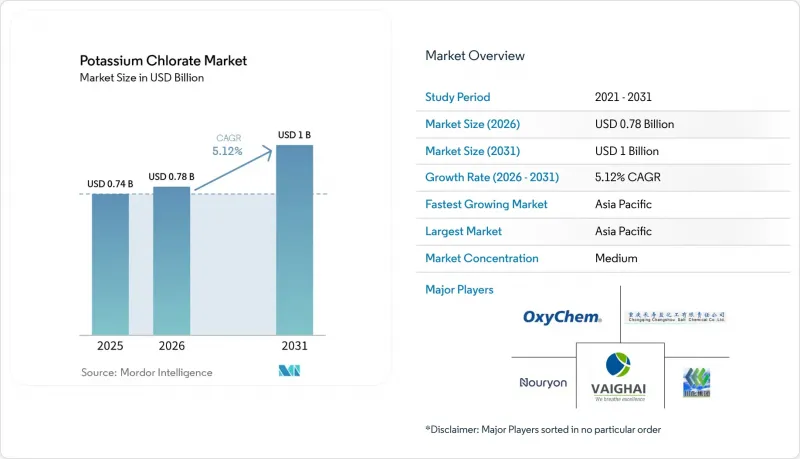

Mordor Intelligence에 의하면, 염소산칼륨 시장 규모는 2025년 7억 4,000만 달러로 평가되었습니다. 2026년 7억 8,000만 달러로 확대되어 2031년까지 10억 달러에 이를 것으로 예상되며 2026-2031년에 걸쳐 CAGR은 5.12%를 나타낼 전망입니다.

본 보고서는 형태(분말, 결정, 플레이크), 순도 등급(산업용 : 99% 이하, 실험용 : 99% 이상), 기술용(99% 이하), 실험용(99% 이상), 용도(안전 성냥, 기타), 최종 사용자 산업(화학, 농업, 기타), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 염소산칼륨 시장 동향 및 분석

농약용 낙엽제 제제의 확대

브라질의 세라두 지역과 인도의 구자라트 지역에서는 면화 재배의 기계화가 진행되고 있어, 나트륨 잔류물을 남기지 않는 즉효성 건조제에 대한 수요가 증가하고 있습니다. 제제 제조업체는 습도가 높은 수확 조건에서도 잎의 낙엽을 촉진하기 위해, 보조제 포장에 염소산칼륨을 배합하고 있습니다. 2023년부터 2024년에 걸쳐 인도는 2만 7,726톤의 염소산을 수출했으며, 이는 케냐와 태국 등 시장에서 면화 재배 면적이 확대되는 상황에 대응할 수 있는 잉여 생산 능력을 보유하고 있음을 보여줍니다. 미국에서는 EPA(환경보호청)의 규제로 인해 수확 전 염소산염 사용이 금지되어 있기 때문에 아시아의 잉여 생산량은 규제가 완화된 시장으로 흘러가고 있습니다. 남아시아의 기계화율은 여전히 15% 미만이지만, 펀자브 주와 신드 주에서 실시된 시범 프로그램을 통해 비용 절감 효과가 입증됨에 따라 향후 도입 가능성이 높아지고 있습니다. 전반적으로 볼 때, 염소산염이 농업에서 차지하는 비중은 유럽 및 미국 시장에서는 감소하는 추세이지만, 신흥 면화 생산 지역에서는 안정적인 수준을 유지하고 있습니다.

재생 섬유 분야의 염소 무첨가 산화 표백으로의 전환

세계 의류 브랜드들이 낮은 염소 배출량을 요구함에 따라, 아시아의 섬유 공장에서는 섬유 강도를 유지할 수 있는 전기화학적 산화제의 도입이 확대되고 있습니다. 염소산칼륨은 실온에서 차아염소산 또는 과산화수소를 즉시 생성할 수 있어, 표백 공정의 소요 시간과 에너지 소비를 줄여줍니다. 누리옹의 ‘Eka HP Puroxide’ 제품 라인은 염소산의 전해와 그린 수소를 통합하여 스코프 3 배출량을 최대 90%까지 줄이고 있습니다. 연간 800만 톤 이상의 섬유를 처리하는 방글라데시와 베트남의 섬유 공장은 EU의 REACH 규정을 준수하기 위한 요건을 충족하기 위해 이 기술을 조기에 도입하고 있습니다. 온사이트 시스템을 통해 불안정한 산화제의 운송이 필요 없어지며, 3회의 생산 주기 이내에 투자 회수가 가능해집니다. 그 결과, 표백용 화학제품 공급업체들은 고순도 염소산염에 대한 수요에서 새로운 성장 기회를 발견하고 있습니다.

제초제 및 성냥 용도에 대한 규제상 금지 조치 및 미립자 제한

미국 환경보호청(EPA)이 2026년까지 허용한 면제 조치는 수확 후 훈증 처리에만 국한되며, 미국의 수확 전 면화 프로그램에서 염소산염의 사용은 제외됩니다. 유럽연합(EU)에서는 사전 동의(PIC) 규정에 따라 수출업체가 구매자의 승인을 얻어야 할 의무가 있으며, 브뤼셀에서 마련 중인 새로운 미세입자 배출 기준으로 인해 성냥 제조 시설의 규정 준수 비용이 증가할 것으로 예측됩니다. 히메지에서 국내 매치 공급량의 80%를 생산하고 있는 일본에서는 당국이 유사한 분진 기준을 검토 중이며, 이로 인해 염소산염의 소비량이 감소할 가능성이 있습니다. 신흥국들이 규제를 조정하고 있는 한편, 이러한 규제 동향을 종합적으로 볼 때, OECD 시장 내 염소산염 사용량이 감소하게 될 것입니다.

부문별 분석

2025년 기준으로, 분말은 염소산칼륨 시장의 57.12%를 차지했으며, 이는 성냥 머리, 농업용 혼합물, 실험용 시약에서의 사용에 힘입은 결과입니다. 누리용의 ISO 인증을 획득한 알비 공장에서는 유럽 성냥 제조업체의 요건을 충족할 수 있도록 분쇄 곡선을 맞춤화하고 있습니다. 결정 등급은 의약품 합성에 사용되고 있지만, 중국의 범용 제품과의 경쟁에 직면해 있습니다. 플레이크 제품의 생산량은 연평균 성장률(CAGR) 5.51%로 증가할 것으로 예측됩니다. 이는 공중 불꽃놀이 제조업체들이 공극을 줄이고 연소의 균일성을 높이기 위해 고밀도 입자를 선호하기 때문입니다. 일본의 불꽃놀이 제조업체들은 다단계의 화려한 폭발 효과를 최적화하기 위해 플레이크의 형태를 지정하는 경우가 늘고 있습니다. 그 결과, 2031년에는 염소산칼륨 플레이크 시장 규모가 전체 시장보다 빠른 속도로 성장할 것으로 전망됩니다.

기술 등급의 염소산칼륨(99% 이하)은 2025년 예상 시장 규모의 73.25%를 차지했으며, 주로 비용을 중시하는 농약 및 매치 산업에 공급되었습니다. 분석 허용 범위에서는 브로메이트 함량이 100ppm 이하, 염화물 함량이 2,000ppm 이하로 규정되어 있으며, 이는 대부분의 산화제 용도에서 충분한 수준입니다. 실험실용 등급의 염소산칼륨(99% 이상)은 보다 엄격한 중금속 관리가 요구되는 의약품 중간체 및 특수 분석 부문 수요에 힘입어 연평균 성장률(CAGR) 5.78%를 나타낼 것으로 예측됩니다. EU의 REACH 등록 자료에 따르면, 이 화합물의 20℃에서의 수용성은 69.9 g/L이며, 이는 결정화 공정을 설계하는 연구실에게 중요한 매개변수입니다.

기술 등급 부문의 성장은 유럽 및 미국 시장에서 제초제 사용이 금지됨에 따라 제한을 받고 있지만, 신흥 면화 생산 지역과 광산용 산소 캔들에 염소산칼륨이 사용됨에 따라 수요는 여전히 견조한 수준을 유지하고 있습니다. 실험실용 칼륨클로라이트는 인도의 수탁 제조 부문 확대와 중국의 특수 염료 합성 기술 발전의 혜택을 받고 있습니다. 듀얼 유스(군민 겸용) 제품에 대한 수출 규제가 점점 더 엄격해지는 가운데, 감사 완료된 생산 이력(체인 오브 커스터디) 문서를 제공할 수 있는 공급업체는 프리미엄 가격을 책정할 수 있게 되어, 염소산칼륨 시장의 고순도 부문에서 가치 확보를 강화하고 있습니다.

지역별 분석

아시아태평양은 인도의 수출 확대와 중국의 원자재 관리 정책에 힘입어, 2025년에는 매출의 47.12%를 차지하고 연평균 성장률(CAGR)은 5.98%를 나타냈습니다. 2024년, 중국의 국내 염화칼륨(KCl) 생산량은 0.56% 감소한 305만 톤을 기록한 반면, 소비량은 15.51% 증가하여 수입 의존도가 50%를 넘어섰습니다. 미국의 중국 클로르산테크사에 대한 제재 조치에 따라 수출 모니터링이 강화되면서, 해당 지역 내에서 비축 움직임이 나타나고 있습니다.

북미에서는 농업용 수요가 감소하는 추세이지만, 방위 및 산소 장치 부문 수요는 견조한 흐름을 보이고 있습니다. NewMarket-AMPAC의 확장 계획은 2026년 말까지 NASA와 미국 국방부(DoD)의 프로그램 요건을 충족할 것으로 예측됩니다. 유럽에서는 알비에 위치한 유일한 염소산염 전용 공장이 비용 효율화를 위해 스웨덴의 수력발전을 활용하고 있습니다.

남미는 주요 진출 기업으로 부상하고 있으며, 누리옹의 마토그로소 두 술 주 프로젝트를 통해 지역 생산량이 20% 증가했고, 전력 비용 절감을 위해 바이오매스 증기를 활용하고 있습니다. 중동 및 아프리카에서는 성장이 케냐와 남아프리카공화국에 집중되어 있으며, 주로 면화와 광업용 원자재로 인도에서 수입되는 물품에 의해 뒷받침되고 있습니다. 전반적으로, 재생에너지 자원을 보유한 지역은 새로운 염소산염 분야에 대한 투자를 유치하고 있는 반면, 화석 연료에 기반한 전력망에 의존하는 지역에서는 이익률이 하락하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the potassium chlorate market size is expected to increase from USD 0.74 billion in 2025 to USD 0.78 billion in 2026 and reach USD 1 billion by 2031, growing at a CAGR of 5.12% over 2026-2031.

This report is Segmented by Form (Powder, Crystals, Flakes), Purity Grade (Technical Less Than or Equal To 99%, Laboratory Greater Than or Equal To 99%), Application (Safety Matches, and More), End-User Industry (Chemicals, Agriculture, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Potassium Chlorate Market Trends and Insights

Expansion of Agro-Chemical Defoliant Formulations

Cotton mechanization is expanding in Brazil's Cerrado region and India's Gujarat belt, increasing demand for fast-acting desiccants that do not leave sodium residues. Formulators are incorporating potassium chlorate into adjuvant packages to promote faster leaf drop under humid harvest conditions. In 2023-24, India exported 27,726 tons of chlorate, indicating surplus production capacity that can cater to growing cotton acreage in markets such as Kenya and Thailand. In the United States, EPA regulations prohibit the use of pre-harvest chlorate, leading to the redirection of surplus Asian production to less-regulated markets. While mechanization rates in South Asia remain below 15%, pilot programs in Punjab and Sindh have demonstrated cost savings, encouraging potential future adoption. Overall, chlorate's agronomic role is declining in Western markets but stabilizing in emerging cotton-producing regions.

Shift Toward Chlorine-Free Oxidative Bleaching in Recycled Textiles

Global apparel brands are requesting low-chlorine discharge scores, leading Asian textile mills to adopt electrochemical oxidants that maintain fiber strength. Potassium chlorate enables the in-situ generation of hypochlorite or hydrogen peroxide at room temperature, reducing bleaching cycle durations and energy consumption. Nouryon's Eka HP Puroxide product line integrates chlorate electrolysis with green hydrogen, achieving up to a 90% reduction in Scope 3 emissions. Textile mills in Bangladesh and Vietnam, which process over 8 million tons of textiles annually, are early adopters to meet EU REACH compliance requirements. On-site systems eliminate the need for transporting unstable oxidants and provide a return on investment within three production cycles. Consequently, suppliers of bleaching chemicals are identifying a new growth opportunity in the demand for high-purity chlorate.

Regulatory Bans and Micro-Particle Limits on Herbicide and Match Uses

The EPA's 2026 tolerance exemption is limited to post-harvest fumigation, excluding chlorate from U.S. pre-harvest cotton programs. In the European Union, Prior Informed Consent regulations mandate exporters to obtain buyer approval, while new micro-particle discharge limits being drafted in Brussels are expected to increase compliance costs for match production facilities. In Japan, which produces 80% of its domestic match supply in Himeji, authorities are considering similar dust standards that may reduce chlorate consumption. These regulatory developments collectively reduce chlorate tons in OECD markets, even as emerging economies adjust restrictions.

Other drivers and restraints analyzed in the detailed report include:

- Growing Use in Low-Temperature Chemical Oxygen Generators

- Cost-Advantaged Renewable-Powered Electrolysis Capacity Additions

- Substitution by Potassium Perchlorate and Sodium Chlorate in Defense and Bleaching

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Powder accounted for 57.12% of the potassium chlorate market share in 2025, driven by its use in match heads, agricultural blends, and laboratory reagents. Nouryon's ISO-certified Alby mill customizes grind curves to meet the requirements of European match manufacturers. Crystal grades are used in pharmaceutical synthesis but face competition from Chinese commodities. Flake volumes are expected to grow at a CAGR of 5.51%, as aerial-shell manufacturers prefer dense particles that reduce void space and enhance burn consistency. Japanese fireworks manufacturers are increasingly specifying flake morphology to optimize multi-stage color bursts. As a result, the market size for potassium chlorate flakes is projected to grow faster than the overall market through 2031.

Technical-grade potassium chlorate (less than or equal to 99%) accounted for 73.25% of the projected 2025 market size, primarily serving cost-sensitive agrochemical and match industries. Assay tolerances permit bromate levels below 100 ppm and chloride levels below 2,000 ppm, which are sufficient for most oxidizer applications. Laboratory-grade potassium chlorate (greater than or equal to 99%) is expected to grow at a CAGR of 5.78%, driven by demand in pharmaceutical intermediates and specialty analytics requiring stricter heavy-metal controls. According to EU REACH dossiers, the compound has a water solubility of 69.9 g/L at 20°C, a critical parameter for laboratories designing crystallization processes.

Growth in the technical-grade segment is limited by herbicide bans in Western markets; however, emerging cotton-growing regions and the use of potassium chlorate in mining oxygen candles maintain baseline demand. Laboratory-grade potassium chlorate benefits from India's expanding contract manufacturing sector and China's advancements in specialty dye synthesis. As dual-use export regulations become increasingly stringent, suppliers providing audited chain-of-custody documentation are able to command premium pricing, enhancing value capture in the high-purity segment of the potassium chlorate market.

Geography Analysis

Asia-Pacific is projected to account for 47.12% of the revenue in 2025, with a compound annual growth rate (CAGR) of 5.98%, supported by India's export growth and China's feedstock control policies. In 2024, China's domestic potassium chloride (KCl) production decreased by 0.56% to 3.05 million tons, while consumption increased by 15.51%, raising import dependency to over 50%. Increased scrutiny on exports, following U.S. sanctions on China Chlorate Tech Co., has led to regional stockpiling efforts.

In North America, agricultural usage is declining, but demand from the defense and oxygen-device sectors remains steady. The NewMarket-AMPAC expansion is expected to meet the requirements of NASA and Department of Defense (DoD) programs by late 2026. In Europe, the only dedicated chlorate plant, located in Alby, benefits from Swedish hydropower for cost efficiency.

South America is emerging as a key player, with Nouryon's Mato Grosso do Sul project increasing regional output by 20% and utilizing biomass steam to reduce power costs. In the Middle East and Africa, growth is concentrated in Kenya and South Africa, primarily supported by Indian exports for cotton and mining applications. Overall, regions with renewable energy resources are attracting new chlorate investments, while areas reliant on fossil fuel grids face reduced margins.

- American Elements

- Barium & Chemicals, Inc.

- Chenzhou Chenxi Metals Co., Ltd

- Chongqing Changshou Salt Chemical Co., Ltd.

- GFS Chemicals Inc.

- Hebei Fiza Technology Co., Ltd

- Merck KGaA

- Nouryon

- Occidental Chemical Corporation

- Pandian Chemicals

- Santa Cruz Biotechnology Inc.

- Sichuan Chemical Works

- Thermo Fisher Scientific Inc.

- Vaighai Agro.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of agro-chemical defoliant formulations

- 4.2.2 Shift toward chlorine-free oxidative bleaching in recycled textiles

- 4.2.3 Growing use in low-temperature chemical oxygen generators

- 4.2.4 Cost-advantaged renewable-powered electrolysis capacity additions

- 4.2.5 Micro-particle engineered oxidizers for mini-rocket & drone propulsion

- 4.3 Market Restraints

- 4.3.1 Regulatory bans on chlorate-based herbicides

- 4.3.2 Substitution by potassium perchlorate & sodium chlorate

- 4.3.3 EU micro-particle discharge limits tightening match formulations

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Form

- 5.1.1 Powder

- 5.1.2 Crystals

- 5.1.3 Flakes

- 5.2 By Purity Grade

- 5.2.1 Technical (Less than equal to 99 %)

- 5.2.2 Laboratory (Greater than equal to 99 %)

- 5.3 By Application

- 5.3.1 Safety Matches

- 5.3.2 Fireworks and Explosives

- 5.3.3 Agrochemicals (Herbicides/Defoliants)

- 5.3.4 Textile Bleaching and Printing

- 5.3.5 Laboratory Reagents and Oxygen Generators

- 5.3.6 Other Applications (Disinfectants, etc.)

- 5.4 By End-User Industry

- 5.4.1 Chemicals

- 5.4.2 Agriculture

- 5.4.3 Paper and Textiles

- 5.4.4 Defense and Pyrotechnics

- 5.4.5 Mining and Safety Equipment

- 5.4.6 Other End-user Industries (Lab, Water Treatment, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 American Elements

- 6.4.2 Barium & Chemicals, Inc.

- 6.4.3 Chenzhou Chenxi Metals Co., Ltd

- 6.4.4 Chongqing Changshou Salt Chemical Co., Ltd.

- 6.4.5 GFS Chemicals Inc.

- 6.4.6 Hebei Fiza Technology Co., Ltd

- 6.4.7 Merck KGaA

- 6.4.8 Nouryon

- 6.4.9 Occidental Chemical Corporation

- 6.4.10 Pandian Chemicals

- 6.4.11 Santa Cruz Biotechnology Inc.

- 6.4.12 Sichuan Chemical Works

- 6.4.13 Thermo Fisher Scientific Inc.

- 6.4.14 Vaighai Agro.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment