|

시장보고서

상품코드

2062119

재생 건설용 자재 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Recycled Construction Aggregates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

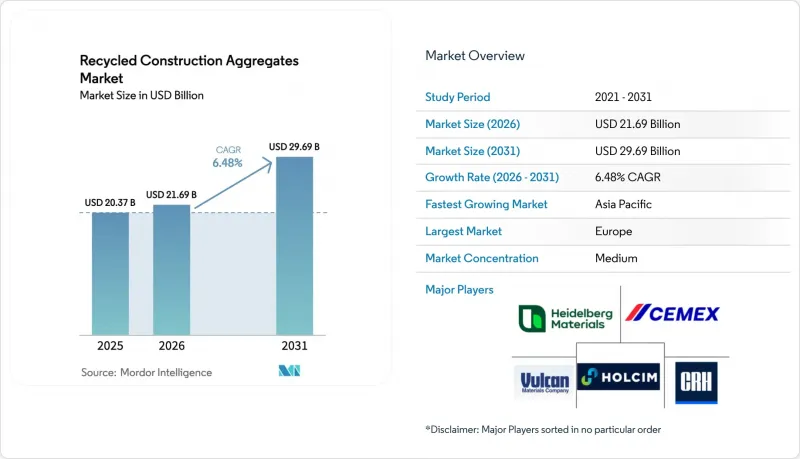

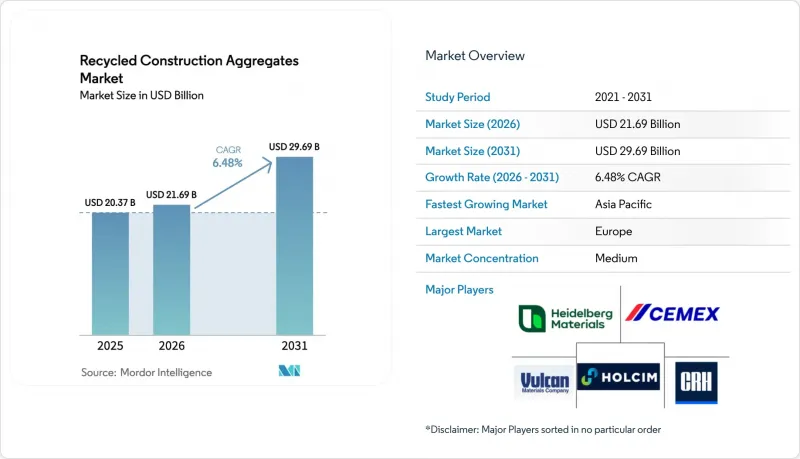

Mordor Intelligence에 의하면, 재생 건설용 자재 시장 규모는 2025년에 203억 7,000만 달러로 평가되었고 2026년 216억 9,000만 달러에서 2031년까지 296억 9,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 6.48%를 나타낼 전망입니다.

본 보고서는 유형(쇄석, 자갈, 모래, 콘크리트 자재, 기타), 용도(주택, 상업, 인프라, 산업), 원료(건설·해체 폐기물, 재생 아스팔트 포장, 기타) 및 지역(아시아태평양, 북미, 유럽, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 재생 건설용 자재 시장 동향 및 인사이트

건설·철거 폐기물의 디지털 추적 의무화

위성 추적 및 전자 운송장은 비공식적인 불법 투기를 효과적으로 억제하고, 폐기물을 인가된 재활용 업체로 유도하고 있습니다. 2026년 5월부터 운영되고 있는 유럽연합(EU)의 ‘디지털 폐기물 운송 시스템’은 세관 직원이 규정을 준수하지 않는 국경 간 운송을 차단할 수 있도록 하며, 위반 건당 벌금을 부과하고 있습니다. 2026년 1월에 시작된 중국의 ‘고형 폐기물 행동 계획’에서는 5톤 이상의 건설 폐기물을 운반하는 트럭에 대해 북두(BeiDou)를 통한 추적을 의무화하고 있습니다. 동시에, 2026년 4월에 발표된 인도의 ‘건설 및 해체 폐기물 관리 규정’은 확대 생산자 책임(EPR) 목표를 상향 조정하고, 2029년까지의 완전한 준수를 추진하고 있습니다. 이러한 규제는 원자재의 투명성을 높이고, 신규 플랜트의 자금 조달 위험을 줄이며, 특히 그동안 비공식 공급망에 의존해 온 지역에서 재생 건설용 자재 시장 도입을 가속화할 것입니다.

정부의 순환형 경제 목표가 강화되었습니다.

2027년부터 사우디아라비아에서는 유틸리티에서 자재의 일부를 재생 자재로 조달해야 합니다. 멕시코에서는 2026년에 시행될 ‘순환형 경제법’에 따라 건축자재의 보증금 반환 제도와 생산자 책임이 연계됩니다. 스코틀랜드에서는 반경 50km 이내에서 재생 자재를 구할 수 있는 경우, 도로 보수 시 미사용 석재의 사용을 금지하는 규정이 시행되었습니다. 이 규제로 인해 지자체의 아스팔트 수요 상당 부분이 확보되게 되었습니다. 이러한 의무화는 재생 건설용 자재 시장을 확대할 뿐만 아니라, 특히 그동안 소홀히 여겨졌던 지역의 생산 능력에 대한 투자를 촉진하고 있습니다.

천연석과의 구조용 등급 간 성능 격차에 대한 인식

설계 기준에서는 하중을 받는 콘크리트 배합에 재생 자재의 사용이 종종 제한되고 있습니다. 인도에서는 재생 자재의 사용이 M25 콘크리트로 제한되어 있습니다. 한편, 한국에서는 재생 자재가 특정 기준치를 초과할 경우 설계 강도에 제한이 부과됩니다. 장기적인 성능 데이터가 부족하기 때문에 구조 기술자들은 이러한 자재의 품질에 대해 회의적인 시각을 유지하고 있습니다. 이러한 회의적인 시각은 특히 고층 빌딩이나 교량 프로젝트에서 재생 건설용 자재의 광범위한 사용을 저해해 왔습니다.

부문별 분석

2025년, 콘크리트 자재는 재생 건설용 자재 시장에서 40.22%라는 압도적인 점유율을 차지하고 있으며, 2026년부터 2031년까지의 예측 기간 동안 연평균 성장률(CAGR) 6.67%라는 견실한 성장세가 예상됩니다. 이 탄산가스 양생 라인은 28일간의 압축 강도를 향상시키며, EN 206 인증을 받은 구조용 혼합물에서 재생 자재가 미사용 현무암을 효과적으로 대체할 수 있도록 합니다. 쇄석은 허용 오차가 큰 도로 노반에 사용되지만, 투수성 포장에는 재활용 자갈이 주로 채택되어 유럽의 빗물 규제를 준수하고 있습니다. 고미립자 모래는 에어클래스 분류 방식의 고도화로 인해 공급상의 문제에 직면해 있으며, 이는 처리 비용을 상승시킬 뿐만 아니라 시장 침투를 저해하는 요인이 되고 있습니다.

선별 해체, 임팩트 크러셔, 에어 세파레이터는 투자 분야의 주요 관심사로 떠오르고 있습니다. 이러한 개선을 통해, 특히 박편화 및 로스앤젤레스 마모 시험의 임계값과 관련하여 UNI 11531-1:2024 규격 준수가 보장되며, 구조용 콘크리트에 적합한 제품이 됩니다. 하이델베르크 머티리얼즈는 폴란드 공장의 생산 라인에 이산화탄소 처리 시스템을 도입했습니다. 한편, 홀심(Holcim)은 2024년 전략적 인수를 통해 생산 능력을 확대하고, 저탄소 결합재를 위해 설계된 콘크리트 자재에 명확히 주력하고 있습니다. 이러한 설비의 발전은 2026년부터 2031년까지의 예측 기간 동안, 특히 프리캐스트 및 레디믹스트 분야에서 재생 건설용 자재 시장을 견인할 것으로 전망됩니다.

지역별 분석

2025년, 유럽은 전 세계 매출의 36.69%를 차지했습니다. 스코틀랜드에서는 자재에 대한 과세로 인해 재생 자재와 미사용 석재 간의 가격 차이가 확대되고 있습니다. 유럽연합(EU)의 ‘디지털 폐기물 운송 시스템’은 국경을 넘는 폐기물에 대한 실시간 보고를 의무화함으로써, 그동안 지역 재활용 업체들을 불리한 입장에 놓이게 했던 허점을 사실상 차단하고 있습니다. 독일에서는 건축기준법에 따라 비구조 부재에 재생 자재를 사용해야 합니다. 프랑스에서는 해당 지역에서 조달이 가능한 경우, 지방자치단체의 도로 공사 발주 시 재생 자재를 우선적으로 사용하고 있습니다. 영국에서는 현재 표층에 재생 아스팔트 포장재(RAP)를 상당한 비율로 사용하는 것이 허용되고 있습니다. 이러한 조치들은 고부가가치 토목 공사 분야에서 재생 건설용 자재 시장을 전반적으로 강화하고 있습니다.

아시아태평양은 2026년부터 2031년까지의 예측 기간 동안 연평균 성장률(CAGR) 7.12%를 달성할 것으로 전망됩니다. 인도의 확대 생산자 책임(EPR) 목표는 2026년부터 2029년 사이에 크게 증가할 것으로 예측됩니다. 중국에서는 각 성에 2027년까지 자원 이용 목표를 달성할 것을 의무화하고 있으며, 이 지침은 북두(BeiDou)를 통한 모니터링으로 뒷받침되고 있습니다. 인도네시아, 베트남, 말레이시아에서는 연간 인프라 지출에 자원 전용 조항이 포함되어 있습니다. 그러나 내륙 지역 시장에서는 여전히 충분한 파쇄 능력이 부족하여, 재생 건설용 자재 시장의 기반을 주요 도시권을 넘어 확대하려는 투자자들에게는 신규 진입의 호기가 되고 있습니다.

북미에서는 ‘인프라 투자 및 고용법’에 더해, 재생 에너지의 경쟁력을 높이는 탄소 가격 제도의 혜택을 누리고 있습니다. 캐나다에서는 탄소세 인상으로 인해 채석장의 디젤 연료 가격이 상승할 것으로 예측됩니다. 2023년, 미국은 신소재 대신 재생 아스팔트 포장재(RAP)를 활용함으로써 비용을 대폭 절감했습니다. 멕시코의 ‘2026년 순환경제법’은 보증금 반환 제도와 툴라에 위치한 폐기물 가치화 단지를 결합한 것으로, 멕시코를 재생 건설용 자재 시장의 급성장하는 거점으로 자리매김하고 있습니다. 남미와 중동 및 아프리카는 여전히 발전의 초기 단계에 있지만, 브라질과 사우디아라비아에서는 강력한 정책 추진력이 나타나고 있습니다. 이는 자금 조달 문제를 극복하고 미사용 석재의 저가 문제를 해결할 수 있다면, 중기적으로는 성장 가능성이 있음을 시사합니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the recycled construction aggregates market size was valued at USD 20.37 billion in 2025 and is estimated to grow from USD 21.69 billion in 2026 to reach USD 29.69 billion by 2031, at a CAGR of 6.48% during the forecast period (2026-2031).

This report is Segmented by Type (Crushed Stone, Gravel, Sand, Concrete Aggregates, and Others), Application (Residential, Commercial, Infrastructure, and Industrial), Source (Construction and Demolition Waste, Reclaimed Asphalt Pavement, and Others), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Recycled Construction Aggregates Market Trends and Insights

Digital Construction and Demolition-Waste Tracking Mandates

Satellite tracking and electronic manifests are effectively curbing informal dumping, steering debris towards licensed recyclers. The European Union's Digital Waste Shipment System, operational since May 2026, empowers customs officers to intercept non-compliant cross-border shipments, levying fines for each infraction. China's Solid Waste Action Plan, initiated in January 2026, mandates Beidou tracking for trucks hauling over 5 tonnes of construction debris. Simultaneously, India's Construction and Demolition Waste Management Rules, unveiled in April 2026, elevate extended-producer-responsibility targets, pushing for full compliance by 2029. These regulations bolster feedstock transparency, reduce financing risks for new plants, and accelerate the market's adoption of recycled construction aggregates, especially in regions previously reliant on informal supply chains.

Government Circular-Economy Targets Tighten

Starting in 2027, Saudi Arabia will require public projects to source a portion of their aggregates from recycled materials. In Mexico, the Circular Economy Law, effective in 2026, links producer responsibilities to deposit-return schemes for construction materials. Scotland has implemented a rule stating that if recycled materials are available within a 50-kilometer radius, the use of virgin stone for road repairs is prohibited. This regulation has led to a significant reservation of municipal asphalt demand. These mandates not only broaden the market for recycled construction aggregates but also encourage investments in capacity, particularly in previously overlooked regions.

Perceived Structural-Grade Performance Gap vs. Natural Stone

Design codes often restrict the use of recycled aggregates in load-bearing mixes. In India, the use of recycled coarse aggregates is limited to the M25 concrete. South Korea, on the other hand, imposes a design strength limit when the coarse recycled aggregate surpasses a specific threshold. Due to a lack of long-term performance data, structural engineers remain skeptical about the quality of these aggregates. This skepticism has hindered the widespread adoption of recycled construction aggregates, especially in high-rise buildings and bridge projects.

Other drivers and restraints analyzed in the detailed report include:

- Cost Gap Narrows vs. Virgin Aggregates as Diesel Levies Rise

- Carbon-Mineralised Aggregates Earn Negative-Emission Credits

- Sparse Recycling Infrastructure Outside Tier-1 Asia-Pacific Metros

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, concrete aggregates held a dominant 40.22% share of the recycled construction aggregates market, with projections indicating a robust 6.67% CAGR through the forecast period of 2026-2031. Carbonation-curing lines enhance the 28-day compressive strength, enabling recycled materials to effectively replace virgin basalt in EN 206-certified structural mixes. While crushed stone finds its application in road bases with lenient tolerances, recycled gravel is the preferred choice for permeable pavements, ensuring compliance with Europe's stormwater regulations. High-fines sand encounters supply challenges due to air-classification upgrades, which not only inflate processing costs but also hinder its market penetration.

Selective demolition, impact crushers, and air separators have become focal points for investments. These enhancements guarantee adherence to UNI 11531-1:2024 standards, particularly for flakiness and Los-Angeles abrasion thresholds, rendering them suitable for structural-grade concrete. Heidelberg Materials has integrated carbonation into its production line at a Polish facility. On the other hand, Holcim's strategic acquisitions in 2024 have amplified its capacity, with a clear focus on concrete aggregates designed for low-carbon binders. Such advancements in equipment are set to bolster the recycled construction aggregates market, especially within the precast and ready-mix domains, over the forecast period of 2026-2031.

Geography Analysis

In 2025, Europe accounted for 36.69% of global revenue. In Scotland, a levy on aggregates has widened the recycled discount compared to virgin stone. The European Union's Digital Waste Shipment System mandates the real-time reporting of cross-border waste, effectively closing loopholes that have historically disadvantaged local recyclers. Germany mandates the use of recycled content in the non-structural elements of its building code. France prioritizes recycled materials for municipal road orders when they are locally available. The United Kingdom now allows a significant percentage of Reclaimed Asphalt Pavement (RAP) in surface layers. These measures collectively strengthen the market for recycled construction aggregates in high-value civil works.

The Asia-Pacific region is set to achieve a 7.12% compound annual growth rate (CAGR) during the forecast period of 2026-2031. India's extended producer responsibility targets are expected to increase significantly between 2026 and 2029. In China, prefectures are mandated to achieve resource utilization goals by 2027, a directive supported by Beidou monitoring. Indonesia, Vietnam, and Malaysia have integrated diversion clauses into their annual infrastructure spending. However, inland markets still lack sufficient crushing capacity, presenting greenfield opportunities for investors aiming to expand the footprint of the recycled construction aggregates market beyond tier-1 hubs.

North America is benefiting from the Infrastructure Investment and Jobs Act, along with carbon pricing that enhances the competitiveness of recycled materials. Canada's rising carbon tax is projected to increase quarry diesel prices. In 2023, the United States achieved significant savings by utilizing Reclaimed Asphalt Pavement (RAP) instead of virgin materials. Mexico's 2026 Circular Economy Law, which combines deposit-return schemes with a waste-valorization park in Tula, positions the nation as a burgeoning hub for the recycled construction aggregates market. While South America, the Middle-East, and Africa are still in their infancy, Brazil and Saudi Arabia showcase robust policy momentum. This indicates potential growth in the medium term, provided they overcome financing challenges and address the low prices of virgin stone.

- Boral Limited

- Breedon Group plc

- CEMEX S.A.B. de C.V.

- Cherry Companies

- Colas Group

- CRH

- Delta Sand & Gravel

- Eurovia

- GreenRock Recycling

- Heidelberg Materials

- HOLCIM

- Holroyd Company, Inc

- K&B Crushers

- Martin Marietta Materials

- Sibelco

- Veidekke

- Vulcan Materials Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Digital construction and demolition waste tracking mandates

- 4.2.2 Government circular-economy targets tighten

- 4.2.3 Cost gap narrows vs. virgin aggregates as quarry diesel levies rise

- 4.2.4 Carbon-mineralised aggregates earn negative-emission credits

- 4.2.5 AI-optimised mobile crushers cut processing cost/ton >=18%

- 4.3 Market Restraints

- 4.3.1 Perceived structural-grade performance gap vs. natural stone

- 4.3.2 Sparse recycling infrastructure outside Tier-1 Asia-Pacific metros

- 4.3.3 Trace-metal contamination spikes disposal cost for RAP blends

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Crushed Stone

- 5.1.2 Gravel

- 5.1.3 Sand

- 5.1.4 Concrete Aggregates

- 5.1.5 Others

- 5.2 By Application

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Infrastructure (roads, bridges, rail)

- 5.2.4 Industrial

- 5.3 By Source

- 5.3.1 Construction and Demolition Waste

- 5.3.2 Reclaimed Asphalt Pavement

- 5.3.3 Others (slag, foundry sand, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Boral Limited

- 6.4.2 Breedon Group plc

- 6.4.3 CEMEX S.A.B. de C.V.

- 6.4.4 Cherry Companies

- 6.4.5 Colas Group

- 6.4.6 CRH

- 6.4.7 Delta Sand & Gravel

- 6.4.8 Eurovia

- 6.4.9 GreenRock Recycling

- 6.4.10 Heidelberg Materials

- 6.4.11 HOLCIM

- 6.4.12 Holroyd Company, Inc

- 6.4.13 K&B Crushers

- 6.4.14 Martin Marietta Materials

- 6.4.15 Sibelco

- 6.4.16 Veidekke

- 6.4.17 Vulcan Materials Company

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment