|

시장보고서

상품코드

2062125

특수강 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Special Steel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

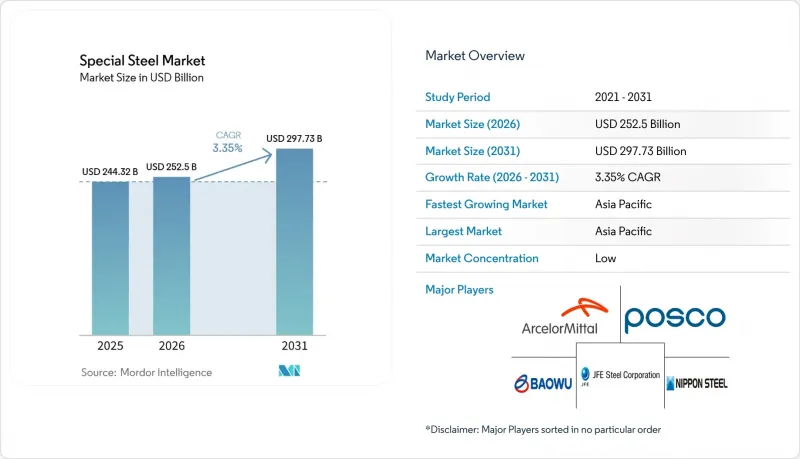

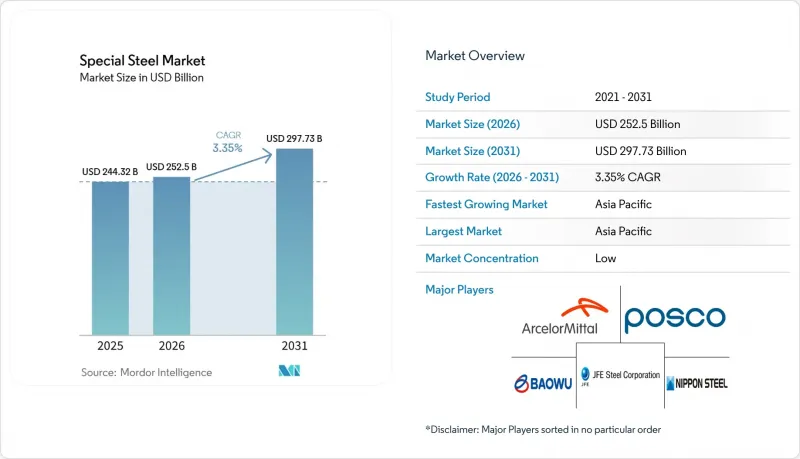

Mordor Intelligence에 의하면, 특수강 시장 규모는 2025년 2,443억 2,000만 달러에서 2026년에는 2,525억 달러로 확대되어 2026년부터 2031년까지 CAGR 3.35%로 성장을 지속하여, 2031년까지 2,977억 3,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형(스테인리스 스틸, 공구강, 합금강 등), 형태(시트·플레이트, 바, 로드, 코일 등), 용도(자동차 부품, 항공우주 구조물·엔진, 기계·공구 등) 및 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 특수강 시장 동향과 인사이트

탈탄소화를 배경으로 한 전기로(EAF) 및 수소 직접 환원(H2-DRI)으로의 전환

전기로(EAF) 및 수소 DRI(H2-DRI) 프로젝트는 고로와 비교하여 현장 수준의 CO2 배출량을 최대 70%까지 줄입니다. SSAB는 2026년까지 옥셀순드에서 화석 연료 없는 생산을 달성할 것으로 예상하고 있으며, H2 Green Steel은 2030년까지 스웨덴에서 500만 톤의 친환경 강판을 생산하는 것을 목표로 하고 있습니다. 자본 집약도는 연간 생산 능력 1톤당 1,200-1,500달러로 여전히 높은 수준이지만, 유럽연합(EU)의 탄소 가격이 톤당 90유로를 상회함에 따라 투자 회수 기간이 단축되고 있습니다. 알고마 스틸의 7억 캐나다 달러 규모 프로그램 등 북미의 이러한 변화는 자동차 제조업체들의 저탄소 조달 요건과 부합합니다. 티센크루프의 뒤스부르크 사업에서 전환이 지연된 사례에서 볼 수 있듯이, 수소 공급이나 재생에너지 확보가 프로젝트 일정을 따라가지 못할 경우 실행 위험은 여전히 남아 있습니다.

재생에너지 관련 설비의 확충

해상 풍력, 전해조, 수소 파이프라인 등 각 프로젝트는 특수강 시장의 등급별 최종 용도 다각화를 촉진하고 있습니다. 미국은 해상 풍력 인프라에 420억 달러를 배정하고 2030년까지 30GW를 도입하는 것을 목표로 하고 있으며, 이는 연간 150만-200만 톤의 강판 수요에 해당합니다. EU의 ‘REPowerEU’는 2050년까지 300GW 규모의 해상 풍력 발전을 목표로 하고 있으며, 이에 따라 1,500만-2,000만 톤의 모노파일 및 타워용 강재가 필요하게 됩니다. 전해조의 설치 용량은 2026년에 8GW에 달할 가능성이 있으며, 1기가와트당 약 4,000톤의 특수 스테인리스 스틸이 소비될 것으로 예측됩니다. 수소 수송 인프라에서는 API 5L X70/X80 규격의 파이프가 주류를 이루고 있으며, 유럽 수소 백본 계획에 따르면 2040년까지 8만 1,000km의 인프라가 구축될 것으로 예측됩니다.

에너지 집약적 공정과 탄소 가격 책정

고로 제강에서는 조강 1톤당 18-22기가줄의 에너지를 소비하고 있으며, 탄소 가격 메커니즘으로 인해 제철소가 고객에게 전가할 수 있는 속도를 웃도는 속도로 가동 비용이 상승하고 있습니다. 유럽연합(EU)의 배출권 가격이 90유로(103달러)를 넘어서면, 통합 비용에 톤당 약 18-20유로(20-23달러)가 추가되는 한편, CBAM으로 인해 2026년까지 저비용 수입 경로가 차단될 것입니다. 중국의 확대되는 탄소 시장과 인도의 국경 조정 조치에 대한 우려로 인해 초기 비용은 높아지겠지만, 국내 생산자들은 전기 아크로(EAF)에 대한 투자를 서두르고 있습니다.

부문별 분석

2025년에 스테인리스 스틸이 35.22%의 점유율을 차지한 것은 전해조 스택이나 해상 구조물에서 부식 방지 대책이 지극히 중요하다는 사실을 뒷받침하고 있습니다. 인도네시아의 니켈 선철 생산량 급증과 인도의 생산 능력 확대가 2031년까지 연평균 성장률(CAGR) 3.67%를 뒷받침하고 있습니다. 공구강 수요는 정체세를 보이고 있으며, 2023년 공구 생산에서 적층 가공의 점유율이 11%에 달하면서 기존 공급처에 압박이 가해지고 있습니다.

합금강은 여전히 구동계나 중장비 부품에 있어 중요한 역할을 하고 있지만, 전기차로의 전환에 따라 더 가벼운 금속이 선호되고 있습니다. NSK의 고속 전기차용 액슬 유닛 등 베어링용 강재의 혁신에 힘입어, 일렉트로슬래그 재용해 공법을 통한 화학 성분이 자동차 공급망의 주류로 자리 잡고 있습니다. 로스아톰의 BR-1200 등급으로 대표되는 원자력 프로그램을 통해 오스테나이트계 합금이 고온 용도로 진출하고 있습니다.

지역별 분석

2025년 아시아태평양의 43.35% 점유율은 중국의 규모, 인도의 경기 부양책, 그리고 인도네시아의 니켈 통합에 기인합니다. 중국의 바오우강철은 2024년에 조강 1억 3,185만 톤을 생산할 예정이며, 수소 제련을 통해 2050년까지 탄소 중립을 달성하는 것을 목표로 하고 있습니다. 인도는 2030-2031년까지 3억 톤의 생산 능력을 목표로 하고 있으며, 특수강 유형의 수입 의존도를 낮추기 위한 생산 연계형 인센티브에 힘입어 이를 추진하고 있습니다. 아세안의 제철소 건설은 확대되고 있지만, 부지 확보와 자금 조달의 지연으로 인해 그 실현 속도는 더뎌지고 있습니다.

북미에서는 풍부한 스크랩 자원과 생산의 국내 복귀(리쇼어링)라는 호재를 활용하고 있습니다. 뉴코어사의 31억 달러 규모 강판 공장과 아르셀로미탈사의 10억 달러 규모 배수관 공장 개보수 사업은 OEM(주문자 상표 부착 생산) 업체들의 경량화 프로그램과 발을 맞추고 있습니다. 일본제철과 US 스틸의 제휴가 성사된다면 태평양을 횡단하는 특수강 플랫폼이 구축될 전망이지만, 한편 게르다우의 EBITDA는 현재 62%가 미국 네트워크에 집중되어 있습니다.

유럽은 가장 높은 탈탄소화 비용에 직면해 있습니다. SSAB는 2026년까지 화석 연료가 아닌 원료로 만든 강재를 공급할 예정이며, 아우트쿰프의 페로크롬 통합은 크롬 가격 변동 위험을 완화할 것입니다. 티센크루프는 ETS 가격이 제철소의 수익성을 압박하는 가운데 파트너를 모색하고 있으며, 영국 포트 탈보트의 전환 사례는 고용 감축을 배경으로 한 정치적 지원을 보여주고 있습니다.

남미의 운명은 브라질의 무역 방어 조치와 지속 가능한 광업의 개선에 달려 있습니다. 2026년에 예정된 반덤핑 판정으로 인해 국내 가격이 안정될 가능성이 있습니다. 아르헨티나의 긴축 재정 정책은 수요를 억제하고 있지만, 지역별 수출 경로는 국지적인 기회를 창출하고 있습니다.

중동 및 아프리카에서는 사우디아라비아의 건설 수요와 남아프리카공화국의 페로크롬 공급에서의 우위가 결합되어 있습니다. 에너지 비용이 제련소의 생산량을 위협하고 있지만, ‘비전 2030’의 메가 프로젝트가 장형 제품 수요를 뒷받침하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the special steel market size is expected to grow from USD 244.32 billion in 2025 to USD 252.5 billion in 2026 and is forecast to reach USD 297.73 billion by 2031 at 3.35% CAGR over 2026-2031.

This report is Segmented by Product Type (Stainless Steel, Tool Steel, Alloy Steel, and More), Form (Sheets and Plates, Bars, Rods, Coils, and Others), Application (Automotive Components, Aerospace Structures and Engines, Machinery and Tools, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Special Steel Market Trends and Insights

Decarbonization Driven Switch To EAF And H2-DRI Routes

EAF and H2-DRI projects trim as much as 70% of site-level CO2 emissions compared with blast furnaces. SSAB expects fossil-free output from Oxelosund by 2026, while H2 Green Steel targets 5 million tons of green steel in Sweden by 2030. Capital intensity remains high at USD 1,200-1,500 per tonne of annual capacity, yet European Union (EU) carbon prices above EUR 90 per ton are accelerating payback periods. North American conversions, such as Algoma Steel's CAD 700 million program, align with automaker low-carbon sourcing mandates. Execution risk persists when hydrogen supply and renewable power lag project timelines, evidenced by Thyssenkrupp's delayed Duisburg transition.

Expansion Of Renewable-Energy Hardware

Offshore-wind, electrolyzer, and hydrogen-pipeline projects are widening end-use diversity for special steel market grades. The United States earmarked USD 42 billion for offshore-wind infrastructure, aiming for 30 GW by 2030, equating to 1.5-2.0 million tons of plate demand per year. EU's REPowerEU targets 300 GW of offshore wind by 2050, pulling 15-20 million tons of monopile and tower steel. Electrolyzer installations could reach 8 GW in 2026, with each gigawatt consuming around 4,000 tons of specialty stainless. API 5L X70/X80 pipe grades dominate hydrogen-transmission frameworks, and the European Hydrogen Backbone foresees 81,000 km of infrastructure by 2040.

Energy-Intensive Processes and Carbon Pricing

Blast-furnace steelmaking consumes 18-22 gigajoules per tonne of crude steel, and carbon-pricing mechanisms are escalating operating costs faster than mills can pass through to customers. European Union (EU) allowance prices over EUR 90 (USD 103) add around EUR 18-20 (USD 20-23) per tonne to integrated costs, while CBAM removes the low-cost import avenue by 2026. China's expanding carbon market and India's fear of border adjustments are pushing domestic producers toward EAF (Electric Arc Furnace) investment despite higher initial costs.

Other drivers and restraints analyzed in the detailed report include:

- Digitally Enabled Alloy-Design Platforms Shortening Grade-Development Cycles

- Infrastructure Stimulus In Emerging Economies

- Competition From Additive-Manufactured Lightweight Metals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Stainless steel's 35.22% share in 2025 underscores its corrosion-critical role in electrolyzer stacks and offshore structures. Indonesia's nickel-pig-iron surge and India's capacity expansion underpin a 3.67% CAGR to 2031. Tool steel demand is flattening as the additive share in tooling production hit 11% in 2023, pressuring traditional supplies.

Alloy steel maintains relevance for drivetrain and heavy-equipment parts, but electric-vehicle shifts favor lighter metals. Bearing steel innovation, such as NSK's high-speed EV axle unit, is pushing electroslag-remelted chemistries into mainstream auto supply. Nuclear programs, exemplified by Rosatom's BR-1200 grade, pull austenitic alloys into high-temperature service.

Geography Analysis

Asia-Pacific's 43.35% 2025 share stems from Chinese scale, Indian stimulus, and Indonesian nickel integration. China Baowu produced 131.85 million tons of crude steel in 2024 and pursues carbon-neutrality by 2050 through hydrogen metallurgy. India targets 300 million tons of capacity by 2030-31, supported by production-linked incentives that lower specialty-grade import reliance. ASEAN mills expand, though land and financing delays temper realization.

North America leverages scrap abundance and reshoring tailwinds. Nucor's USD 3.1 billion sheet mill and ArcelorMittal's USD 1 billion Calvert upgrade align with OEM (original equipment manufacturer) light-weighting programs. A pending Nippon Steel-US Steel tie-up would create a trans-Pacific specialty platform, while Gerdau's EBITDA now skews 62% to its U.S. network.

Europe faces the steepest decarbonization costs. SSAB will deliver fossil-free steel by 2026, and Outokumpu's ferrochrome integration buffers chromium volatility. Thyssenkrupp seeks partners as ETS prices pressure blast-furnace economics, and the UK's Port Talbot conversion demonstrates political support framed by job cuts.

South America hinges on Brazilian trade defenses and sustainable mining improvements. Anti-dumping rulings due 2026 may stabilize domestic pricing. Argentina's austerity curbs demand, though regional export channels open pockets of opportunity.

Middle East and Africa combine Saudi construction demand with South African ferrochrome supply dominance. Energy costs threaten smelter output, yet Vision 2030 megaprojects anchor long-product demand.

- Aperam S.A.

- ArcelorMittal

- China BaoWu Steel Group Corporation Limited

- CRS Holdings, LLC.

- Daido Steel Co., Ltd.

- Gerdau S/A

- JFE Steel Corporation

- JSW

- Nippon Steel Corporation

- Nucor Corporation

- Outokumpu

- POSCO

- Sandvik AB

- SSAB

- Tata Steel

- Thyssenkrupp Steel Europe

- United States Steel Corporation

- Vardhman Special Steels Limited

- Voestalpine Stahl GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Decarbonisation-driven switch to EAF and H2-DRI routes

- 4.2.2 Expansion of renewable-energy hardware (off-shore wind, electrolyser frames, and hydrogen pipelines)

- 4.2.3 Digitally enabled alloy-design platforms shortening grade-development cycles

- 4.2.4 Infrastructure stimulus in emerging economies

- 4.2.5 Surge in green-hydrogen-ready steels for electrolyser and pipeline build-out

- 4.3 Market Restraints

- 4.3.1 Energy-intensive processes and tightening carbon-pricing regimes

- 4.3.2 Competition from additive-manufactured light-weight metals

- 4.3.3 Supply-chain volatility in critical minerals (nickel and chromium)

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Stainless Steel

- 5.1.2 Tool Steel

- 5.1.3 Alloy Steel

- 5.1.4 Bearing Steel

- 5.1.5 Carbon Steel (Special Grades)

- 5.2 By Form

- 5.2.1 Sheets and Plates

- 5.2.2 Bars

- 5.2.3 Rods

- 5.2.4 Coils

- 5.2.5 Others (Forgings, Wires, and Billets)

- 5.3 By Application

- 5.3.1 Automotive Components

- 5.3.2 Aerospace Structures and Engines

- 5.3.3 Oil and Gas Equipment

- 5.3.4 Machinery and Tools

- 5.3.5 Construction and Infrastructure

- 5.3.6 Energy and Power (Turbines, Nuclear, and Renewables)

- 5.3.7 Other Applications (Railways, Medical Devices, and Defense)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Aperam S.A.

- 6.4.2 ArcelorMittal

- 6.4.3 China BaoWu Steel Group Corporation Limited

- 6.4.4 CRS Holdings, LLC.

- 6.4.5 Daido Steel Co., Ltd.

- 6.4.6 Gerdau S/A

- 6.4.7 JFE Steel Corporation

- 6.4.8 JSW

- 6.4.9 Nippon Steel Corporation

- 6.4.10 Nucor Corporation

- 6.4.11 Outokumpu

- 6.4.12 POSCO

- 6.4.13 Sandvik AB

- 6.4.14 SSAB

- 6.4.15 Tata Steel

- 6.4.16 Thyssenkrupp Steel Europe

- 6.4.17 United States Steel Corporation

- 6.4.18 Vardhman Special Steels Limited

- 6.4.19 Voestalpine Stahl GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment