|

시장보고서

상품코드

2062157

잉크젯 착색제 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Inkjet Colorants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

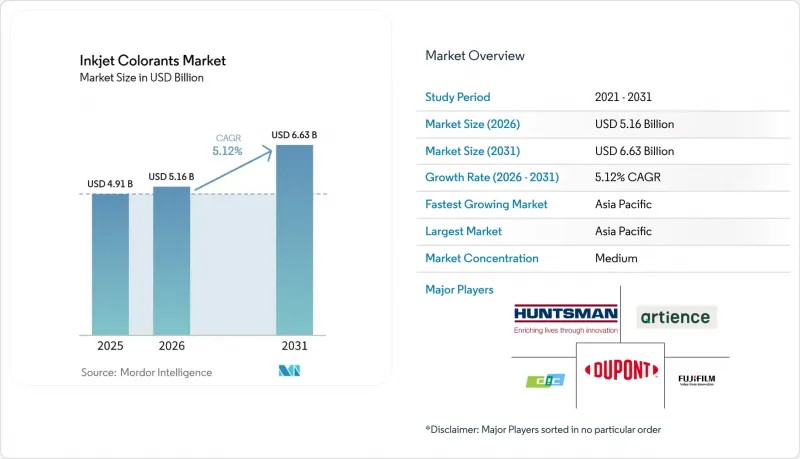

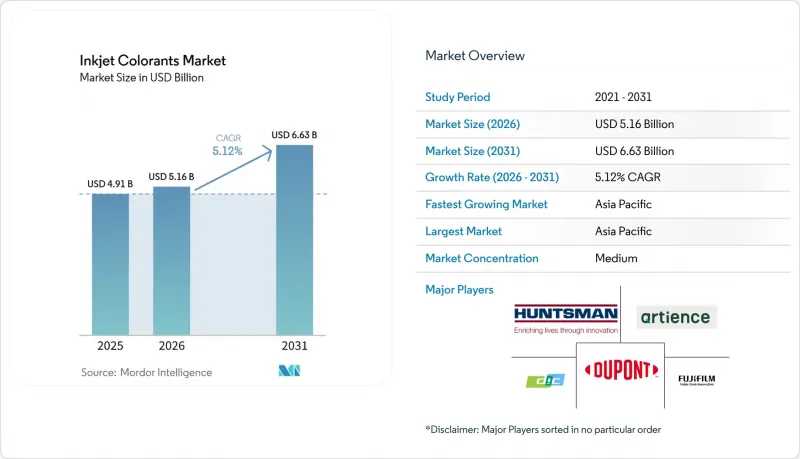

Mordor Intelligence에 의하면, 잉크젯 착색제 시장 규모는 2025년 49억 1,000만 달러로 평가되었습니다. 2026년에는 51억 6,000만 달러로 확대되어 2031년까지 66억 3,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 5.12%를 나타낼 전망입니다.

본 보고서는 착색제의 유형(염료, 안료 등), 제형(수성, 용제계 등), 용도(상업 인쇄, 산업 인쇄 등), 최종 사용자 산업(섬유 및 의류, 포장 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 잉크젯 착색제 시장 동향 및 인사이트

디지털 텍스타일 인쇄 및 포장 분야의 확대

섬유 제조업체들은 기존의 스크린 인쇄 라인에서 잉크젯 시스템으로 전환하고 있으며, 수익성이 확보되는 생산량을 수천 미터에서 불과 수백 미터로 낮추고 있습니다. 이러한 변화로 인해 브랜드는 생산량을 실제 수요에 맞추어 조정할 수 있게 됩니다. 2025년, Monster Digital은 Kornit Apollo 10대를 도입하여 사업을 확장하고, 의류 사전 주문에 대한 당일 발송을 실현했습니다. Errea Sport는 Mimaki Tiger-1800B MkIII 프린터 7대를 도입하여 생산 효율을 높였으며, 폴리에스터 혼방 원단에서 시간당 150제곱미터의 생산 속도를 달성했습니다. 골판지 및 유연 소재 가공 업체에서는 코로나 처리가 필요 없이 폴리올레핀 필름에 직접 인쇄할 수 있는 후지필름의 ‘Jet Press FP790’과 같은 수성 잉크젯 프레스가 도입되고 있습니다. 아시아태평양은 여전히 중요한 시장이며, 2025년에는 중국의 섬유용 디지털 잉크 지출이 44억 1,700만 위안으로 증가해 전 세계 지출의 약 20%를 차지했습니다.

고해상도 잉크젯 기술의 발전

의약품의 일련번호 부여 및 보안 라벨의 경우, 나노 안료를 채택함으로써 1,200 dpi라는 놀라운 해상도로 출력하는 것이 가능해졌습니다. 코닥의 ‘KODACOLOR’ 플랫폼은 평균 입자 직경 11 nm를 자랑하며, 1차 통과 수율 99%라는 놀라운 수치를 달성했습니다. 이러한 효율성 덕분에, 특히 분당 100미터를 초과하는 생산 라인에서 폐기물 감축으로 이어집니다. 주목할 만한 진전으로, 고베 대학은 은 나노입자를 이용한 구조색 인쇄 기술을 선보였습니다. 이러한 나노 입자는 시야각에 따라 색상이 변하여 위조 방지 기능을 강화합니다. 엡손과 만츠 아시아는 공동으로 반도체 포토레지스트 패터닝에 특화된 잉크젯 적층 기술을 선도적으로 개발하고 있습니다. 이러한 혁신은 인쇄 전자 분야의 새로운 가능성을 열어줄 것입니다. 또한, 에보닉의 ‘TEGO Dispers 695’와 같은 하이퍼 분산제는 안료 함유율을 25 wt% 이상으로 안정적으로 유지하면서, 점도를 최적의 분사 매개변수 범위 내에 유지하는 중요한 역할을 수행하고 있습니다.

VOC 및 폐수 규제의 강화

EU의 새로운 인쇄 설비 VOC 배출 상한치(50 mg/m³) 및 미국의 유사한 규제로 인해, 배합 변경에 따른 비용이 증가하고 있습니다. 2027년 1월까지 독일의 식품 접촉용 잉크 규정에 따라 광물유 수지의 사용이 금지되므로, 기술적인 조정이 필요합니다. 미네소타주의 배수 규정은 구리 및 크롬의 농도를 1ppm 미만으로 제한하고 있으며, 이로 인해 여과 비용이 증가하고 있습니다. 위반 시 최대 100만 위안의 벌금이 부과되는 중국의 수질오염방지법 개정에 따라, 중금속계 건조제의 대체가 진행되고 있습니다. 대규모 다국적 기업은 시험 비용을 전 세계 생산량에 분산시킬 수 있지만, 지역 공급업체들은 이익률 압박에 직면해 있습니다.

부문별 분석

2025년, 안료는 총 매출의 55.11%를 차지했으며, 이는 염료에 비해 내광성이 높음을 보여줍니다. 가장 빠르게 성장하고 있는 하위 부문인 나노 안료는 연평균 성장률(CAGR) 5.57%를 나타낼 것으로 전망됩니다. 15 nm 미만으로 억제된 입자 크기는 노즐 막힘 위험을 줄이고 색 영역을 확대합니다. 코닥의 11 nm 분산액은 광택이 있는 기판 위에서 1,200 dpi의 인쇄 품질을 구현합니다. 2025년 11월, 산케미칼은 블루 울 7의 내광성이 요구되는 포장용 잉크에 주력하여 페릴렌 안료의 생산량을 200톤 늘렸습니다. 원가 효율을 중시하는 섬유 분야에서는 분산염료가 여전히 시장 점유율을 유지하고 있지만, 각 브랜드 기업들은 오코텍스 기준을 준수하기 위해 안료로의 전환을 추진하고 있습니다.

보안 인쇄 분야에서는 카본블랙과 TiO₂ 안료가 NIR 광?下에서 1.5 : 1을 초과하는 바코드 명암비 기준을 충족하고 있습니다. 일본과 독일은 식품 접촉 적합성 분야에서 나노 안료를 주로 채택하고 있는 국가들입니다. 200°C를 초과하는 온도에서도 안정성이 필수적인 승화 전사 및 세라믹 장식용으로 특수한 제품이 개발되었습니다.

2025년에는 수성 시스템이 수요의 60.33%를 차지했으나, UV 경화형 잉크는 연평균 성장률(CAGR) 5.89%로 더 높은 성장률을 보였습니다. INX International사의 MDLM 잉크는 분당 2,000캔의 속도로 0.5초 만에 경화되어, 오븐 없이도 금속 캔에 장식을 할 수 있게 해줍니다. Toyo Ink Europe의 GIO 시리즈는 2027년 규제에 대비하여 광물유 제거 기능을 갖추고 있습니다. UV-LED 어레이는 에너지 소비를 70% 절감하고 표면 온도를 50℃ 이하로 유지하므로, 발포체나 필름 기판에 적합합니다.

실외 간판의 경우, 특히 가소제의 이주로 인해 강력한 캐리어 잉크가 필요한 경우, 용제형 잉크가 여전히 사용되고 있습니다. 롤랜드의 ‘ECO-SOL MAX’는 글리콜 에테르를 사용하여 악취를 줄이고 있습니다. 라텍스 잉크와 에코솔벤트 잉크는 성능과 규제 준수의 균형을 제공합니다. 고점도 수성 잉크와 함께 근적외선 건조기를 사용하면 에너지 소비량을 40% 절감할 수 있습니다.

지역별 분석

2025년 매출의 46.23%를 차지한 아시아태평양은 2031년까지 연평균 성장률(CAGR) 5.90%를 나타낼 것으로 전망됩니다. 중국에서는 광둥성과 절강성의 섬유 제조업체들이 Kornit 및 Mimaki 시스템을 도입함에 따라, 섬유용 디지털 잉크 지출액이 44억 1,700만 위안으로 증가했습니다. 2026년 지크웍이 하이테크 잉크스를 인수함에 따라, 인도 연포장 시장의 20%를 확보하고 구자라트주 및 타밀나두주의 클러스터를 강화할 것으로 예측됩니다. 일본에서는 OEM 각사가 50kHz를 초과하는 동작 주파수를 가진 1,200dpi 프린트 헤드의 개발을 추진하고 있습니다. 한국에서는 음료 라벨 생산 라인을 UV 잉크로 전환하고 있습니다. 아세안 국가 전체적으로 보면, 생산 거점의 이전에 따라 규제를 준수하는 수성 및 UV 경화형 솔루션에 대한 수요가 증가하고 있습니다.

북미와 유럽에서는 시장이 신규 개발보다 갱신에 중점을 두고 있어 성장이 둔화되고 있습니다. 미국의 NESHAP(대기오염방지법) 및 독일의 광물유 사용 금지 조치로 인해, 친환경 배합의 도입이 가속화되고 있습니다. Flint Group의 인도 공장 설립은 유럽 공급업체들이 아시아 시장에 주력하고 있음을 여실히 보여주고 있습니다. 캐나다와 멕시코에서는 니어쇼어링의 추세에 따라, 특히 온타리오주와 할리스코주에서 디지털 인쇄기 도입이 증가하고 있습니다.

남미, 중동 및 아프리카에서는 브라질의 스포츠웨어 인쇄 업체들이 잉크젯 기술로 전환하고 있습니다. 사우디아라비아에서는 ‘비전 2030’ 이니셔티브에 따라 포장 분야 확장을 위한 자금이 투입되고 있으며, UV 잉크와 수성 잉크가 선호되고 있습니다. 남아프리카에서는 상업용 건물에서 악취가 심한 용제계 잉크라인이 대체되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the inkjet colorants market size is expected to increase from USD 4.91 billion in 2025 to USD 5.16 billion in 2026 and reach USD 6.63 billion by 2031, growing at a CAGR of 5.12% over 2026-2031.

This report is Segmented by Colorant Type (Dyes, Pigments, and More), Formulation Type (Water-Based, Solvent-Based, and More), Application (Commercial Printing, Industrial Printing, and More), End-User Industry (Textile and Apparel, Packaging, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Inkjet Colorants Market Trends and Insights

Expansion of Digital Textile Printing and Packaging

Textile mills are shifting from traditional screen lines to inkjet systems, reducing break-even volumes from thousands of meters to just hundreds. This change allows brands to align production with actual demand. In 2025, Monster Digital expanded its operations with ten Kornit Apollo units, enabling same-day fulfillment for apparel pre-orders. Errea Sport increased its production efficiency by incorporating seven Mimaki Tiger-1800B MkIII printers, achieving a production rate of 150 m2 per hour on polyester blends. Corrugated and flexible converters are adopting water-based presses, such as Fujifilm's Jet Press FP790, which bonds to polyolefin films without requiring corona treatment. Asia-Pacific remains a key region, with China's digital ink expenditure in textiles reaching CNY 4.417 billion in 2025, representing approximately 20% of the global total.

Advancements in High-Resolution Inkjet Technology

Pharmaceutical serialization and security labels now benefit from nano-pigments, achieving an impressive 1,200 dpi output. Kodak's KODACOLOR platform boasts an 11 nm mean particle size, achieving a remarkable 99% first-pass yield. This efficiency translates to reduced waste, especially on production lines exceeding 100 m/min. In a notable advancement, Kobe University showcased structural-color printing using silver nanoparticles. These nanoparticles shift hue based on the viewing angle, bolstering anti-counterfeiting measures. In a collaborative effort, Epson and Manz Asia are pioneering inkjet deposition techniques tailored for semiconductor photoresist patterning. This innovation paves the way for expanded opportunities in printed electronics. Additionally, hyperdispersants like Evonik's TEGO Dispers 695 play a crucial role, stabilizing pigment loads exceeding 25 wt% while ensuring viscosity remains within optimal jetting parameters.

Stricter VOC and Wastewater Regulations

New EU caps of 50 mg/m3 VOC for printing installations, along with similar U.S. limits, are increasing reformulation costs. By January 2027, Germany's food-contact ink regulations will require the removal of mineral-oil resins, necessitating technological adjustments. Minnesota's wastewater directives, which limit copper and chromium to under 1 ppm, are contributing to higher filtration expenses. China's updated Water Pollution Control Law, with fines up to CNY 1 million for violations, is encouraging the replacement of heavy-metal driers. While large multinationals can allocate testing costs across global volumes, regional suppliers are experiencing pressure on their margins.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Water-Based and Eco-Friendly Formulations

- Rise of On-Demand Additive-Manufacturing Inks

- Nozzle Clogging and Dispersion-Stability Issues

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, pigments accounted for 55.11% of total revenue, indicating their higher lightfastness compared to dyes. Nano-pigments, the fastest-growing sub-segment, are projected to grow at a 5.57% CAGR. Their particle sizes, kept below 15 nm, reduce nozzle clogging risks and improve the color gamut. Kodak's 11 nm dispersions enhance print quality to 1,200 dpi on glossy substrates. In November 2025, Sun Chemical increased its perylene pigment production by 200 tons, focusing on packaging inks that require Blue Wool 7 lightfastness. Disperse dyes continue to hold a share in cost-sensitive textiles, although brands are shifting to pigments to comply with Oeko-Tex standards.

In security printing, carbon black and TiO2 pigments meet barcode contrast standards above 1.5:1 under NIR light. Japan and Germany are key adopters of nano-pigments for food-contact compliance. Specialty variants are being developed for sublimation and ceramic decoration, where stability beyond 200 °C is critical.

In 2025, water-based systems represented 60.33% of the demand, while UV-curable inks exhibited a higher growth rate with a 5.89% CAGR. INX International's MDLM inks cure in 0.5 seconds at a rate of 2,000 cans per minute, supporting metal-can decoration without requiring ovens. Toyo Ink Europe's GIO series has addressed the removal of mineral oil in preparation for the 2027 regulations. UV-LED arrays reduce energy consumption by 70% and maintain surface temperatures below 50 °C, making them suitable for foam and film substrates.

Solvent lines continue to be used in outdoor signage, particularly where plasticizer migration necessitates strong carriers. Roland's ECO-SOL MAX reduces odor through the use of glycol ethers. Latex and eco-solvent inks provide a balance between performance and regulatory compliance. Near-infrared dryers, when used with high-viscosity water inks, achieve a 40% reduction in energy consumption.

Geography Analysis

Asia-Pacific, which accounted for 46.23% of 2025 revenue, is projected to grow at a 5.90% CAGR through 2031. In China, textile digital-ink expenditure reached CNY 4.417 billion, driven by mills in Guangdong and Zhejiang adopting Kornit and Mimaki systems. Siegwerk's acquisition of Hi-Tech Inks in 2026 is expected to secure 20% of India's flexible-packaging market, strengthening clusters in Gujarat and Tamil Nadu. In Japan, OEMs are advancing 1,200 dpi heads operating beyond 50 kHz. South Korea is transitioning its beverage-label lines to UV inks. Across ASEAN nations, relocations are increasing the demand for compliant water-based and UV-curable solutions.

In North America and Europe, growth is moderating as markets focus on replacements rather than new developments. The U.S. NESHAP and Germany's mineral-oil ban are driving faster adoption of eco-formulations. Flint Group's establishment of a plant in India highlights the Asian focus of European suppliers. In Canada and Mexico, near-shoring trends are increasing digital press installations, particularly in Ontario and Jalisco.

In South America and the Middle East & Africa, Brazil's sportswear printers are shifting to inkjet technology. In Saudi Arabia, the Vision 2030 initiative is directing funds toward packaging expansions, with a preference for UV and water-based inks. In South Africa, high-odor solvent lines in commercial buildings are being replaced.

- BASF

- CLARIANT

- DIC CORPORATION

- DuPont

- Flint Group

- FUJIFILM Corporation

- Huntsman International Inc.

- Nazdar

- Nippon Kayaku Co., Ltd.

- Sensient Technologies Corporation

- Siegwerk Druckfarben AG & Co. KGaA

- Sun Chemical Corporation

- Toyo Ink Co., Ltd. (artience Co., Ltd.)

- Trust Chem Co., Ltd.

- Zhejiang Xinkai Technology Group Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of digital textile printing and packaging

- 4.2.2 Advancements in high-resolution inkjet technology

- 4.2.3 Shift toward water-based and eco-friendly formulations

- 4.2.4 Rise of on-demand additive-manufacturing inks

- 4.2.5 Integration of colorants for printed electronics

- 4.3 Market Restraints

- 4.3.1 Stricter VOC and wastewater regulations

- 4.3.2 Competition from laser, UV-offset and hybrid presses

- 4.3.3 Nozzle clogging and dispersion-stability issues

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Colorant Type

- 5.1.1 Dyes

- 5.1.2 Pigments

- 5.1.3 Nano-pigments

- 5.1.4 Disperse dyes and others

- 5.2 By Formulation Type

- 5.2.1 Water-based

- 5.2.2 Solvent-based

- 5.2.3 UV-curable

- 5.2.4 Eco-solvent and latex

- 5.3 By Application

- 5.3.1 Commercial printing

- 5.3.2 Industrial printing

- 5.3.3 Office and desktop printing

- 5.3.4 Advertising and signage

- 5.3.5 Other Applications (coding, security, etc.)

- 5.4 By End-user Industry

- 5.4.1 Textile and apparel

- 5.4.2 Packaging (labels, corrugated, flexible)

- 5.4.3 Advertising and media

- 5.4.4 Consumer electronics

- 5.4.5 Education and corporate

- 5.4.6 Other End-user Industries (healthcare, automotive, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 BASF

- 6.4.2 CLARIANT

- 6.4.3 DIC CORPORATION

- 6.4.4 DuPont

- 6.4.5 Flint Group

- 6.4.6 FUJIFILM Corporation

- 6.4.7 Huntsman International Inc.

- 6.4.8 Nazdar

- 6.4.9 Nippon Kayaku Co., Ltd.

- 6.4.10 Sensient Technologies Corporation

- 6.4.11 Siegwerk Druckfarben AG & Co. KGaA

- 6.4.12 Sun Chemical Corporation

- 6.4.13 Toyo Ink Co., Ltd. (artience Co., Ltd.)

- 6.4.14 Trust Chem Co., Ltd.

- 6.4.15 Zhejiang Xinkai Technology Group Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment