|

시장보고서

상품코드

2062218

마이크로파이버 합성 가죽 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Microfiber Synthetic Leather - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

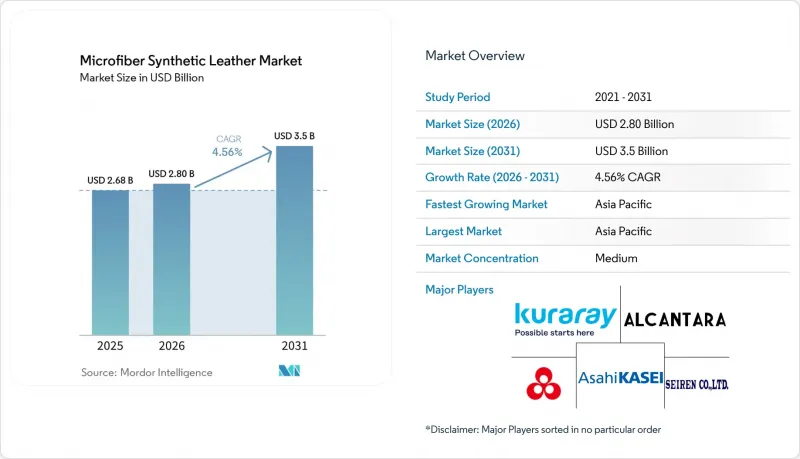

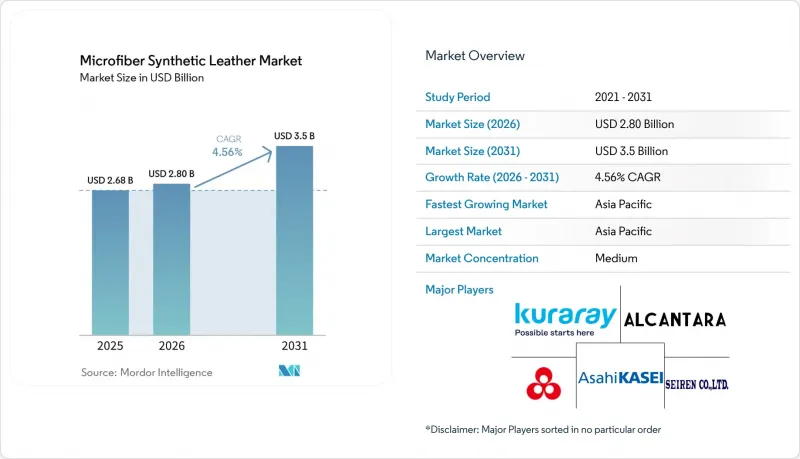

Mordor Intelligence에 의하면, 마이크로파이버 합성 가죽 시장 규모는 2025년에 26억 8,000만 달러로 평가되었고 2026년 28억 달러에서 2031년까지 35억 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 4.56%를 나타낼 전망입니다.

본 보고서는 소재 유형(폴리우레탄 계열 등), 질감 및 표면 가공 유형(스웨이드, 나파, 스플릿 등), 최종 사용자 산업(패션 및 의류, 자동차 및 운송, 가구 및 인테리어 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 마이크로파이버 합성 가죽 시장 동향 및 분석

지역을 아우르는 비건 및 지속 가능한 패션의 성장

H&M과 스텔라 매카트니 등 주요 브랜드들은 차세대 합성 소재 개발을 가속화하기 위해 2026년 봄에 공동 인사이트 위원회를 설립하고, 마이크로파이버의 새로운 브랜딩 역량을 강조했습니다. 휴고 보스를 비롯한 럭셔리 브랜드들은 2030년까지 버진 폴리에스터 및 폴리아미드를 단계적으로 폐지하겠다고 약속했으며, 화학적 탈중합을 위해 설계된 마이크로파이버 배합에 대한 관심을 높이고 있습니다. 도레이의 ‘울트라 스웨이드 BX’는 30%의 식물 유래 폴리에스테르를 함유하고 있어, 고급 전기차 모델에 널리 채택되고 있습니다. 이는 바이오 소재의 함유율이 가격 프리미엄을 창출한다는 사실을 입증하고 있습니다. 캘리포니아주 SB 707에 따른 용제 규제 및 EU의 PFAS 금지 조치로 인해, 변환업체들은 수성 폴리우레탄으로의 전환을 강요받고 있으며, 이는 이미 전 세계 마이크로파이버 생산량의 약 4분의 1을 차지하고 있습니다. 한편, 환경 NGO들은 세탁 시 68.5 mg/kg으로 측정된 마이크로파이버의 탈락을 문제 삼고 있으며, 생분해성은 정책 과제로서 계속해서 주목받고 있습니다.

PU/PVC 합성 소재에 비해 뛰어난 성능(내마모성 및 통기성)

실험실 테스트 결과, 마이크로파이버 합성 가죽은 파열 강도 374 N, 인열 강도 139 N을 기록하여 천연 가죽을 크게 웃돌고 있습니다. 이를 통해 마모가 심한 시트에 적용하는 것이 타당해집니다. 2026년 3월에 도입된 닛산의 ‘TailorFit’ 시트 커버는 10만 회 이상의 마모 주기를 견디며, 천연 가죽에 비해 40-60%의 비용 경쟁력을 자랑합니다. SEIREN은 마이크로파이버 기판과 Viscotec사의 디지털 인쇄 기술을 결합한 제품입니다. 이 소량 생산 모델은 재고 리스크를 증가시키지 않으면서도 맞춤형 인테리어를 원하는 자동차 제조업체의 요구를 충족시킵니다. 다만, 극한의 추위나 무더위 같은 기후 조건에서는 여전히 해결해야 할 과제가 남아 있어, 천연 가죽의 열안정성이 여전히 활용되고 있습니다. Spiber사의 ‘Brewed Protein’ 섬유와 같은 획기적인 기술은 폴리우레탄을 사용하지 않고 콜라겐의 구조를 재현한 발효 유래 소재를 통해, 향후 경쟁 구도를 예고하고 있습니다.

생분해성의 한계와 천연 가죽의 비교

폴리우레탄 및 폴리아미드 구조는 효소에 의한 분해에 저항하기 때문에 마이크로파이버 폐기물은 매립지에 장기간 잔류하지만, 천연 가죽은 40년 이내에 분해됩니다. 2026년 7월부터 시행되는 EU의 ESPR(지속 가능한 제품을 위한 에코디자인 규정)에 따른 미판매 섬유 제품의 폐기 금지는 분해를 전제로 한 설계를 의무화하고 있지만, 복합재료의 박리 과정으로 인해 PET 재활용에 비해 처리 비용이 2배로 증가합니다. BASF의 Haptex 4.0은 폴리아미드 층을 제거함으로써 폐쇄형 PET 회수를 가능하게 하지만, 상업적 적용은 한 곳의 전기차 OEM 제조업체에 국한되어 있습니다. 생산자책임확대제도(EPR)의 비용이 증가하면, 브랜드는 현재 가죽에 대해 부담하고 있는 40-60%의 비용 차이를 메울 수 있을 가능성이 있습니다.

부문별 분석

폴리우레탄계 제품은 10만 회 이상의 내마모 사이클과 기존 가죽 가공 설비와의 높은 호환성 덕분에, 2025년에는 매출 점유율 68.12%를 기록하며 마이크로파이버 합성 가죽 시장을 주도했습니다. 그 밖의 소재 유형(블렌드 마이크로파이버 기재)은 고급차 제조업체들이 순환형 소재를 추구하는 가운데, 예측 기간(2026-2031년) 동안 가장 높은 연평균 성장률(CAGR) 4.96%를 나타낼 것으로 전망됩니다. 폴리아미드 마이크로파이버는 비용보다 인열 강도를 중시하는 틈새 스포츠 용품 시장과 내구성이 뛰어난 시트 시장을 선점하고 있습니다. DMF 사용 규제가 강화된 결과, 수성 폴리우레탄은 이미 전 세계 생산량의 약 4분의 1을 차지하고 있으며, 바이오 폴리우레탄의 생산 능력은 2024년에 52만 톤에 달했습니다.

투자의 초점은 물리적 성능을 저해하지 않으면서 바이오 함유율을 높이는 연구 개발에 있습니다. 페라리의 ‘풀로산게’에 적용된 알칸타라의 68% 재활용 폴리에스터 배합은 프리미엄 친환경 스웨이드에 대한 소비자의 높은 수요를 보여줍니다. 아사히카세이와 아쿠아파일의 셀룰로오스 강화 PA6는 폐쇄형 루프(closed-loop)화를 목표로 하고 있는 반면, ECOLORICA의 드럼 염색 풀그레인 마이크로파이버는 대중 시장용 PVC와의 가격 격차를 좁히지 않으면서도 고급 액세서리 시장에서 수익성을 확보하고 있습니다. 캘리포니아주 프로포지션 65 및 REACH 기준을 모두 충족하는 복합 소재 디자인은 OEM 승인 절차가 더 신속하게 진행됩니다.

지역별 분석

아시아태평양은 2025년에 매출 점유율 54.44%를 차지하며 주도적인 위치를 차지할 것으로 보이며, 2031년까지 연평균 성장률(CAGR) 5.32%를 나타낼 것으로 전망됩니다. 중국은 전 세계 폴리우레탄 공급량의 36%를 단독으로 차지하고 있으며, 2026년에 가동을 시작한 만화화학(万華化学)의 연간 150만 톤 규모 MDI 생산 시설이 이를 뒷받침하고 있습니다. 화펑(Huafeng)이 2026년에 36억 위안 규모의 설비 확장을 단행함에 따라 스판덱스와 액상 폴리우레탄 생산량이 20만 톤 증가할 전망이며, 이는 그동안 일본이 독점해 온 고급 스웨이드 시장에 중국이 진출할 것임을 시사합니다. 인도에서 합성피혁 원자재에 대한 관세 면제에 더해, SEIREN의 현지 마감 공장이 가동되면서 남아시아 지역 수요 증가에 박차를 가하고 있습니다.

유럽과 북미는 순환형 경제로의 전환을 추진하고 있습니다. NIO가 BASF의 Haptex 4.0을 채택한 것은 용제를 사용하지 않는다는 특징을 입증하는 것이며, 한편 2026년 7월부터 시행되는 ESPR(유럽 지속가능한 소비 및 생산 규정)에 따른 미판매 재고 폐기 금지는 재활용을 고려한 설계를 의무화하게 됩니다. 에너지 비용과 인건비 급등으로 인해 유럽의 가스 요금이 2019년 대비 120% 높은 수준임에도 불구하고, 아시아와의 가격 차이는 유지되고 있으며, 이에 따라 코베스트로는 2026년 2월 MDI 계약 가격을 톤당 200달러 인상했습니다. 이탈리아의 에콜로리카는 추적성에 대한 추가 비용을 지불할 의사가 있는 고급 제품 구매자들로부터 혜택을 보고 있습니다.

라틴아메리카 및 중동 및 아프리카(MEA) 지역은 여전히 발전 단계에 있습니다. 브라질의 신발 제조업체들은 마이크로파이버 소재의 갑피를 시범 도입하고 있으며, 산팡(San Fang)이 2025년에 계획하고 있는 3억 대만 달러(945만 달러) 규모의 확장 계획은 이러한 중산층 시장을 겨냥하고 있습니다. 그러나 지역 내 이소시아네이트 생산 공장의 부족과 해상 운송비 변동으로 인해, 공급 기반이 현지화될 때까지는 이익 확대가 저해될 것입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the microfiber synthetic leather market size was valued at USD 2.68 billion in 2025 and is estimated to grow from USD 2.80 billion in 2026 to reach USD 3.5 billion by 2031, at a CAGR of 4.56% during the forecast period (2026-2031).

This report is Segmented by Material Type (Polyurethane-Based, and More), Texture/Grain Type (Suede, Nappa, Split, and More), End-User Industry (Fashion and Apparel, Automotive and Transportation, Furniture and Home Decor, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Microfiber Synthetic Leather Market Trends and Insights

Growth of Vegan and Sustainable Fashion Across Regions

Mainstream labels such as H&M and Stella McCartney formed a joint Insight Board in spring 2026 to fast-track next-generation synthetics, underscoring microfiber's new branding power. Luxury houses, including Hugo Boss, are committed to phasing out virgin polyester and polyamide by 2030, spurring interest in microfiber formulas engineered for chemical depolymerization. Toray's Ultrasuede BX, built on 30% plant-based polyester, has been adopted across premium EV models, proving bio-content can command pricing premiums. Solvent regulations from California SB 707 and EU PFAS prohibitions are pushing converters toward waterborne polyurethane, which already accounts for roughly a quarter of global microfiber output. Meanwhile, environmental NGOs spotlight microfiber shedding, measured at 68.5 mg kg during washing, keeping biodegradability on the policy agenda.

Performance Advantages Versus PU/PVC Synthetics (Abrasion and Breathability)

Laboratory tests show microfiber synthetic leather achieves burst force of 374 N and tear strength of 139 N, sharply higher than natural hides, justifying its use in high-wear seating. Nissan's TailorFit seat coverings introduced in March 2026 boast more than 100,000 abrasion cycles and a 40-60% cost edge over genuine leather. SEIREN couples microfiber substrates with Viscotec's digital printing; this small-lot model satisfies automakers seeking bespoke interiors without raising inventory risk. Limitations persist in very cold or hot climates, where natural leather's thermal stability still wins adoption. Breakthroughs such as Spiber's Brewed Protein fiber point to future competition from fermentation-derived materials that replicate collagen architecture without polyurethane.

Limited Biodegradability Versus Natural Hides

Polyurethane-polyamide architecture resists enzymatic breakdown, leaving microfiber waste persistent in landfills, whereas natural hides degrade within four decades. The EU ESPR (Ecodesign for Sustainable Products Regulation) prohibition on destroying unsold textiles from July 2026 compels design for disassembly, yet composite delamination adds double the processing cost relative to PET recycling. BASF's Haptex 4.0 removes polyamide layers to allow closed-loop PET recovery, but commercial roll-out remains limited to one Electric Vehicle Original Equipment Manufacturer. If extended-producer-responsibility fees expand, brands could lose the current 40-60% cost gap over leather.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Use in Automotive Interiors and Luxury Upholstery

- Government Bans/Restrictions on Genuine-Leather Imports

- Supply-Chain Concentration in East Asia Creating Dependency Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyurethane grades led the microfiber synthetic leather market with 68.12% revenue share in 2025, owing to 100,000+ abrasion-cycle durability and ready compatibility with existing tannery equipment. Other material types (blended microfiber bases) are forecast to post the fastest 4.96% CAGR during the forecast period (2026-2031) as luxury OEMs chase circular content. Polyamide microfiber captures niche athletic and heavy-duty seating that values tear strength over cost. Waterborne polyurethane already comprises about one-quarter of global output after regulations clamped down on DMF usage, and bio-based polyurethane capacity reached 520,000 tons in 2024.

Investment centers on research and development that elevates bio-content without compromising physical performance. Alcantara's 68% recycled-polyester formulation in Ferrari's Purosangue demonstrates consumer appetite for premium green suede. Asahi Kasei and Aquafil's cellulose-reinforced PA6 targets closed-loop ambitions, while ECOLORICA's drum-dyed full-grain microfiber commands luxury accessory margins without price convergence to mass-market PVC. Composite designs able to meet both California Prop 65 and REACH standards enjoy quicker OEM approval cycles.

Geography Analysis

Asia-Pacific dominated with a 54.44% revenue share in 2025 and is projected to log a 5.32% CAGR through 2031. China alone supplies 36% of global polyurethane, backed by Wanhua Chemical's 1.5 million tpa MDI facility that came online in 2026. Huafeng's CNY 3.6 billion 2026 upgrade will add 200,000 tons of spandex and polyurethane liquids, signaling China's push into premium suede previously cornered by Japan. India's duty waivers on synthetic footwear inputs plus SEIREN's localized finishing plant are catalyzing demand growth in South Asia.

Europe and North America pivot on circularity. BASF's Haptex 4.0 approval by NIO underscores solvent-free credentials, while the ESPR ban on destroying unsold stock from July 2026 forces design-for-recycling. High energy and labor costs sustain an Asia price gap even as European gas tariffs remain 120% above 2019 levels, prompting Covestro to lift MDI contract prices by USD 200 per ton in February 2026. Italy's ECOLORICA benefits from luxury buyers willing to pay traceability premiums.

Latin America and MEA remain embryonic. Brazilian footwear OEMs trial microfiber uppers, and San Fang's NTD300 million (USD 9.45 million) 2025 expansion targets these mid-income markets. Lack of regional isocyanate plants and ocean-freight volatility, however, inhibit profit pools until supply bases localize.

- Alcantara S.p.A.

- Asahi Kasei Corporation

- Dongguan Kaiyue

- ECOLORICA MICROFIBER S.r.l.

- FUJIAN POLYTECH TECHNOLOGY CO., LTD.

- Kuraray Co., Ltd.

- San Fang Chemical Industry Co., Ltd.

- SEIREN CO., LTD.

- Wanhua

- ZHEJIANG HEXIN HOLDINGS LTD.

- Filwel Co., Ltd.

- HUAFENG GROUP

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth of vegan and sustainable fashion across regions

- 4.2.2 Performance advantages vs PU/PVC synthetics (abrasion and breathability)

- 4.2.3 Expanding use in automotive interiors and luxury upholstery

- 4.2.4 Government bans/restrictions on genuine-leather imports

- 4.2.5 Adoption in high-end consumer electronics casings

- 4.3 Market Restraints

- 4.3.1 Limited biodegradability vs natural hides

- 4.3.2 Supply-chain concentration in East Asia creating dependency risks

- 4.3.3 Lack of drop-in recycling streams for microfiber composites

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Polyurethane-based Microfiber Synthetic Leather

- 5.1.2 Polyamide-based Microfiber Synthetic Leather

- 5.1.3 Other Material Types (Blended Microfiber Bases)

- 5.2 By Texture/Grain Type

- 5.2.1 Suede Microfiber Leather

- 5.2.2 Nappa Microfiber Leather

- 5.2.3 Split Microfiber Leather

- 5.2.4 Embossed/Printed Microfiber Leather

- 5.3 By End-user Industry

- 5.3.1 Fashion and Apparel

- 5.3.2 Automotive and Transportation

- 5.3.3 Furniture and Home Decor

- 5.3.4 Commercial Interiors (Retail, Offices, and Hospitality)

- 5.3.5 Sporting Goods and Equipment

- 5.3.6 Other End-user Industries (Industrial, Defense, and Marine)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Alcantara S.p.A.

- 6.4.2 Asahi Kasei Corporation

- 6.4.3 Dongguan Kaiyue

- 6.4.4 ECOLORICA MICROFIBER S.r.l.

- 6.4.5 FUJIAN POLYTECH TECHNOLOGY CO., LTD.

- 6.4.6 Kuraray Co., Ltd.

- 6.4.7 San Fang Chemical Industry Co., Ltd.

- 6.4.8 SEIREN CO., LTD.

- 6.4.9 Wanhua

- 6.4.10 ZHEJIANG HEXIN HOLDINGS LTD.

- 6.4.11 Filwel Co., Ltd.

- 6.4.12 HUAFENG GROUP

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment