|

시장보고서

상품코드

2062256

유기계 마찰 조정제 첨가제 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Organic Friction Modifier Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

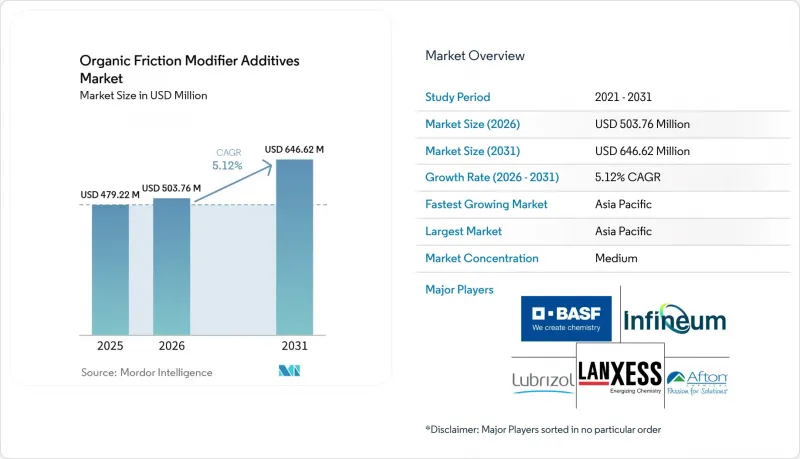

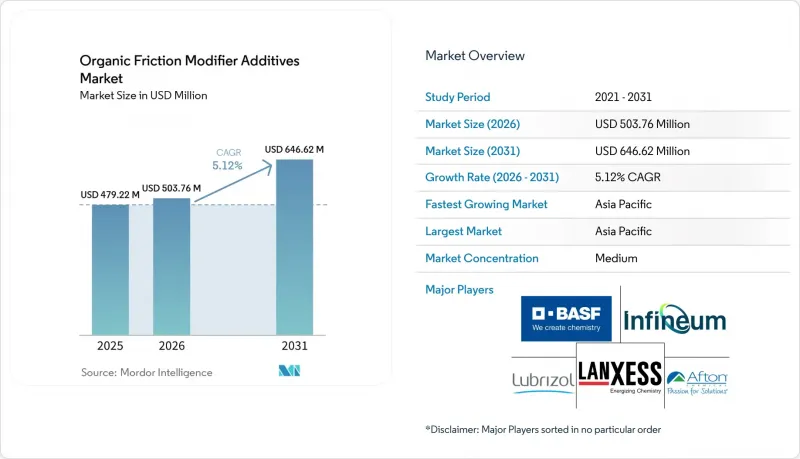

Mordor Intelligence에 의하면, 유기계 마찰 조정제 첨가제 시장 규모는 2025년에 4억 7,922만 달러로 평가되었습니다. 2026년에 5억 376만 달러에서 2031년까지 6억 4,662만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 5.12%를 나타낼 것으로 전망됩니다.

본 보고서는 유형별(에스테르계 마찰 조절제, 아미드계 마찰 조절제 등), 형태별(액체, 고체), 용도별(엔진 오일, 기어 오일, 그리스 등), 최종 사용자 산업별(선박·철도 등), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 유기계 마찰 조정제 첨가제 시장 동향 및 인사이트

엔진 오일 성분에 대한 환경 규제 강화

규제 당국은 인, 황 및 황산 회분 함량을 제한하고 있으며, 이로 인해 블렌딩 업체들은 금속계 마찰 조절제에서 유기계 마찰 조절제로 전환할 수밖에 없는 상황에 처해 있습니다. EU가 2024년 REACH 규정에 따라 단쇄 염소화 파라핀을 재분류함에 따라, 무회분 대체재에 대한 즉각적인 필요성이 대두되었습니다. 미국 환경보호청(EPA)은 2025년에 Tier 4 규정을 최종 확정하고, 배기가스 후처리 장치에 대응하는 디젤 윤활유 사용을 의무화했습니다. 중국의 GB 11121-2024 규격에서는 인 함량을 0.06%로 제한하고 있으며, 이로 인해 글리세롤 모노올레에이트와 PIB-숙시니미드 유도체가 필수적입니다. 이러한 여러 규제가 동시에 시행됨에 따라, 촉매 장치를 손상시키지 않으면서 마찰 계수를 0.08 미만으로 억제할 수 있는 에스테르 및 아미드계 화합물의 도입이 가속화되고 있습니다. 18개월에 걸친 OEM 승인 절차를 앞두고 현장 시험을 완료한 공급업체들은 현재 선구자로서 가격 결정력을 누리고 있습니다.

자동변속기 및 듀얼 클러치 변속기의 보급 확대

2025년 승용차 생산 대수에서 자동변속기 및 듀얼 클러치 변속기가 차지하는 비율은 68%에 달하고, 2023년 대비 7포인트 상승했습니다. 그 증가분의 대부분은 아시아·태평양 지역에서 비롯된 것입니다. 듀얼 클러치 변속기는 -40°C에서 150°C 범위에서 클러치 마찰을 안정적으로 유지하기 위해 0.3%-0.8% 비율로 첨가되는 유기계 개질제에 의존하고 있습니다. BYD와 지리(Geely)가 4.0 L/100 km의 연비 목표를 달성하기 위해 7단 및 8단 변속기 설계로 전환함에 따라, 2025년 중국의 듀얼 클러치 차량 생산 대수는 550만 대에 달했습니다. 무단 변속기(CVT)에는 벨트의 견인력을 안정시키기 위해 내열성이 뛰어난 아미드계 첨가제가 필요합니다. 한편, 북미의 자동차 제조업체들은 8단 및 10단 자동변속기의 보급률을 42%까지 끌어올려 수요를 더욱 높였습니다. 10년이라는 장기 보증 제도의 도입으로 인해, 오일은 10만 km를 초과하더라도 산화 안정성을 유지해야 하며, 이로 인해 첨가제 패키지의 구성이 재편되고 있습니다.

원자재 공급 리스크(유지 화학제품, 에스테르, 아민)

인도네시아의 팜유 과세로 인해 2025년 1분기에 올레산 가격이 34% 상승하면서, 원료를 자체 조달하는 체계를 갖추지 못한 블렌더들의 첨가제 마진이 압박을 받았습니다. 현물 시장의 팜유 중 산가 2mg KOH/g 미만의 규격을 충족하는 제품은 고작 40%에 불과하여, 업스트림 공정에서 정제하거나 고가로 조달할 수밖에 없는 실정입니다. 프로파일렌 옥사이드의 생산 능력은 하류 수요를 따라가지 못하고 있어, 2031년까지 110만 톤공급 부족이 우려되고 있습니다. 이로 인해 아민계 개질제의 비용이 상승하고 있습니다. 페트로나스 케미컬스는 자사 공급을 확보하고 가격 변동을 억제하기 위해 2025년 조호르주에 연간 5만 톤 규모의 오일케미컬 허브를 개설했습니다. 피마자유 및 조류 유래 원료는 여전히 전체 원료의 5% 미만을 차지하지만, 시범 프로젝트에서는 2028년까지 10%를 달성할 계획입니다.

부문별 분석

에스테르계 분자는 GF-6B 및 ACEA C5 오일에 요구되는 뛰어난 열안정성과 저점도 적합성 덕분에, 2025년 유기계 마찰 조정제 첨가제 시장 점유율의 41.11%를 차지했습니다. 글리세롤 모노올레에이트 및 소르비탄 에스테르는 0.5%-1.0%의 첨가량으로 0.07 전후의 마찰 계수를 실현하는 반면, 디(2-에틸헥실)아디핀산은 낮은 전도성으로 인해 e-액슬의 벤치마크로 자리 잡고 있습니다. 에스테르 계열 제품보다 25% 저렴한 아미드 계열 제품이 빠르게 추격하고 있으며, 그 선두에 있는 것이 변속기 오일용 올레아미드로, 예측 기간(2026-2031년) 동안 연평균 성장률(CAGR) 5.63%를 나타낼 것으로 전망됩니다.

아미드의 내구성은 130°C를 초과하면 저하되므로, 고온의 샴프 환경에서는 사용이 제한됩니다. BASF의 2025년 특허에 기반한 에스테르-아민 혼합 하이브리드는 0W-12 오일에서 0.06 미만의 마찰 계수를 실현하기 위해, 에스테르의 열적 안정성과 아민의 극성을 융합하는 것을 목표로 하고 있습니다. 산계 개질제는 그리스나 금속 성형액 분야에서 틈새 시장으로 머물러 있지만, 다기능 고분자 분산제는 첨가제 배합의 간소화가 요구되는 고부하용 디젤유 시장에서 점유율을 확대되고 있습니다.

2025년 기준으로, 유기계 마찰 조정제 첨가제 시장 규모의 83.34%를 액상 제품이 차지했습니다. 이는 자동 주입을 통해 그룹 III 오일이나 폴리아알파올레핀 오일과 쉽게 혼합할 수 있기 때문입니다. 0.3%까지 정밀한 첨가율 제어가 가능하기 때문에 각 OEM 업체들은 정확한 마찰 특성 곡선을 구현할 수 있으며, 이것이 견조한 수요를 뒷받침하고 있습니다.

고체(분말/분산성) 제품은 주로 밀폐형 EV 베어링에 사용되는 이황화 몰리브덴 및 흑연 배합제에 힘입어 2031년까지 연평균 성장률(CAGR) 5.99%를 기록하며 성장할 것으로 전망됩니다. 2025년에 샴록사가 도입할 나노미터 크기의 PTFE는 12개월 동안 침전되지 않으며, 항공우주용 유압 시스템의 서보 밸브에 요구되는 청정도 기준을 충족합니다. 그러나 입자의 잔류성이 새로운 폐기물 규제를 초래할 경우, EU의 미세 플라스틱 정책으로 인해 탄소계 분말의 추가적인 성장이 억제될 가능성이 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 52.22%를 차지하며 1위를 기록했으며, 2031년까지 연평균 성장률(CAGR) 6.26%를 유지할 것으로 전망됩니다. 중국에서는 3,050만 대의 차량이 생산되었으며, 그중 980만 대가 전기차였습니다. 각 차량에는 중국 6b 기준을 충족하기 위해 유기 마찰 조절제에 의존하는 저점도 오일이 필요합니다. 인도에서는 연간 580만 대의 자동차와 2,120만 대의 이륜차 생산에 있어, 미세먼지 배출량을 4.5 mg/km로 제한하는 BS-VI 2단계 규격을 충족하는 오일이 채택되고 있습니다. 아세안 지역에서는 2025년 페트로나스가 조호르에 지역 첨가제 허브를 개설함에 따라 투자가 급증했습니다. 일본과 한국은 이온 액체 하이브리드 기술의 혁신 거점으로서의 위상을 유지하고 있습니다.

북미에서는 미국 내 경차 생산 대수가 1,080만 대로 증가했으며, 클래스 8 트럭은 32만 대에 달했습니다. 이에 따라 후처리 시스템의 내구성을 확보하기 위해, 무회계 개질제를 함유한 API CK-4 규격의 오일이 필요합니다. 캐나다의 겨울용 등급(0W-16 등)에서는 -40°C에서도 펌프의 유체 공급 성능을 확보하기 위해 에스테르계 마찰 개질제가 사용되고 있습니다. 아프턴사는 멕시코로의 수출에 대응하기 위해 2025년에 몬테레이 공장의 생산 능력을 두 배로 늘렸습니다. EPA Tier 4 비도로용 배출 규제 및 캘리포니아주의 LEV 규제로 인해, 금속을 사용하지 않는 제품의 도입이 가속화되고 있습니다.

유럽에서는 독일의 380만 대(이 중 전기차 120만 대) 차량에 대해 초저마찰 e-액슬용 유체가 요구되고 있습니다. 미세 플라스틱 규제 도입을 염두에 두고, BASF와 루브리졸은 2025년에 생분해성 에스테르의 연구 개발에 4,500만 유로를 투자했습니다. 노르웨이에서는 전기차 점유율이 90%에 달하면서, -30°C에서도 사용 가능한 e-액슬용 윤활유에 대한 수요가 증가하고 있습니다. 남미 시장에서는 브라질의 230만 대가 시장 점유율을 주도하고 있으며, 중동 및 아프리카에서는 광업 및 석유화학 산업용 유압 시스템이 수요를 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the organic friction modifier additives market size is projected to be USD 479.22 million in 2025, USD 503.76 million in 2026, and reach USD 646.62 million by 2031, growing at a CAGR of 5.12% from 2026 to 2031.

This report is Segmented by Type (Ester-Based Friction Modifiers, Amide-Based Friction Modifiers, and More), Form (Liquid and Solid), Application (Engine Oils, Gear Oils, Greases and More), End-User Industry (Marine and Rail and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle- East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Organic Friction Modifier Additives Market Trends and Insights

Stricter Environmental Regulations on Engine-Oil Formulations

Regulatory agencies are capping phosphorus, sulfur, and sulfated ash, which forces blenders to shift from metallic to organic friction modifiers. The EU's 2024 REACH reclassification of short-chain chlorinated paraffins created an immediate need for ashless alternatives. The United States Environmental Protection Agency finalized Tier 4 limits in 2025 that require diesel lubricants compatible with after-treatment devices. China's GB 11121-2024 specification restricts phosphorus to 0.06%, making glycerol mono-oleate and PIB-succinimide derivatives indispensable. These simultaneous rules are accelerating the adoption curve for ester and amide molecules that hold friction coefficients below 0.08 without poisoning catalytic hardware. Suppliers that completed field trials ahead of the 18-month OEM approval cycle now enjoy first-mover pricing power.

Growing Penetration of Automatic and Dual-Clutch Transmissions

Automatic and dual-clutch units represented 68% of 2025 passenger-car builds, up seven points from 2023, with Asia-Pacific adding most of the volume. Dual-clutch boxes rely on organic modifiers dosed at 0.3%-0.8% to keep clutch friction steady between -40°C and 150°C. Chinese output reached 5.5 million dual-clutch cars in 2025 as BYD and Geely moved to seven- and eight-speed designs to meet 4.0 L/100 km fuel targets. Continuously variable units need thermally robust amides to stabilize belt traction, while North American OEMs pushed eight- and ten-speed automatics to 42% penetration, further lifting demand. Longer 10-year warranties oblige fluids to hold oxidation stability beyond 100,000 km, which is reshaping additive treat packages.

Raw-Material Supply Risks (Oleochemicals, Esters, Amines)

Palm-oil levies in Indonesia lifted oleic-acid prices by 34% in Q1 2025 and squeezed additive margins for blenders without integrated feedstock positions. Only 40% of spot palm oil meets the less than 2 mg KOH/g acid-value spec, forcing upstream purification or premium sourcing. Propylene-oxide capacity trails downstream needs, creating a looming 1.1-million-ton shortfall by 2031, which is inflating costs for amine modifiers. Petronas Chemicals opened a 50,000-tons/year oleochemical hub in Johor in 2025 to secure a captive supply and cut volatility. Castor oil and algae pathways are still under 5% of feedstock, but pilot projects aim for 10% by 2028.

Other drivers and restraints analyzed in the detailed report include:

- Development of High-Temperature Long-Drain Synthetic Lubricants

- Formulation Synergies with Ionic-Liquid Boosters in Hybrid Powertrains

- Compatibility Issues with Certain Base Oils and Additive Packs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ester-based molecules secured 41.11% of the organic friction modifier additives market share in 2025, owing to excellent thermal stability and low-viscosity compatibility demanded by GF-6B and ACEA C5 oils. Glycerol mono-oleate and sorbitan esters deliver friction coefficients near 0.07 at 0.5%-1.0% dosages, whereas di(2-ethylhexyl) adipate has become the e-axle benchmark because of low conductivity. Amide products priced 25% below esters are catching up fast, led by oleamide in transmission fluids that promise a 5.63% CAGR during the forecast period (2026-2031).

Amide durability tapers above 130°C, which limits usage in high-temperature sump environments. Mixed ester-amine hybrids under BASF's 2025 patent aim to merge ester heat stability with amine polarity for friction below 0.06 in 0W-12 oils. Acid-based modifiers stay niche in greases and metal-forming fluids, while multifunctional polymeric dispersants are gaining share in heavy-duty diesel oils that require simplified additive slates.

Liquid products comprised 83.34% of the organic friction modifier additives market size in 2025 because they blend easily into Group III and polyalphaolefin oils through automated dosing. Precise treat-rate control down to 0.3% lets OEMs target exact friction curves, which secures strong demand.

Solid (powder/dispersible) is set for a 5.99% CAGR to 2031, mainly through molybdenum disulfide and graphite packages used in sealed EV bearings. Nanometer-scale PTFE introduced by Shamrock in 2025 resists sedimentation for 12 months and meets servo-valve cleanliness in aerospace hydraulics. EU micro-plastics policy could, however, cap further carbon-based powder growth if particle persistence triggers new disposal rules.

Geography Analysis

Asia-Pacific led with 52.22% of 2025 revenue and is forecast for a 6.26% CAGR through 2031. China built 30.5 million vehicles, including 9.8 million EVs, each unit demanding low-viscosity oils that depend on organic friction modifiers for compliance with China-6b limits. India's 5.8 million-unit output and 21.2 million two-wheelers also adopt BS-VI Phase 2 oils that cap particulates at 4.5 mg/km. ASEAN investment surged after Petronas opened a regional additive hub in Johor in 2025. Japan and South Korea continue as innovation centers for ionic-liquid hybrids.

In North America, the United States light-vehicle builds climbed to 10.8 million, while Class 8 trucks hit 320,000 units and now need API CK-4 oils containing ashless modifiers for after-treatment durability. Canadian winter grades such as 0W-16 rely on ester friction modifiers for -40°C pumpability. Afton doubled its Monterrey capacity in 2025 to serve Mexican exports. EPA Tier 4 off-road mandates and California LEV rules are prompting faster metal-free adoption.

In Europe, Germany's 3.8 million vehicles, including 1.2 million EVs, require ultra-low-friction e-axle fluids. Pending micro-plastics limits triggered EUR 45 million in research and development for biodegradable esters by BASF and Lubrizol in 2025. Norway's 90% EV share spurred demand for -30°C-capable e-axle lubricants. South America's market share is led by Brazil's 2.3 million vehicles, while the Middle East and Africa share is supported by mining and petrochemical hydraulics.

- ADEKA CORPORATION

- Afton Chemical

- BASF

- Cargil Incorporated

- Infineum International Ltd.

- King Industries, Inc.

- LANXESS

- Lubrizol

- Nouryon

- Petronas Chemicals Group Berhad

- R.T. Vanderbilt Holding Company, Inc.

- Shamrock Technologies

- The W Corporation

- Yasho Industries Limited

- ZSCHIMMER & SCHWARZ, INC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter environmental regulations on engine-oil formulations

- 4.2.2 Growing penetration of automatic and dual-clutch transmissions

- 4.2.3 Development of high-temperature, long-drain synthetic lubricants

- 4.2.4 Formulation synergies with ionic-liquid boosters in hybrid powertrains

- 4.2.5 OEM warranty extensions for ultra-low-friction e-axle lubricants

- 4.3 Market Restraints

- 4.3.1 Raw-material supply risks (oleochemicals, esters, amines)

- 4.3.2 Compatibility issues with certain base oils and additive packs

- 4.3.3 Pending EU micro-plastics legislation on long-chain alkyl esters

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Ester-Based Friction Modifiers

- 5.1.2 Amide-Based Friction Modifiers

- 5.1.3 Acid-Based Friction Modifiers

- 5.1.4 Amine-Based Friction Modifiers

- 5.1.5 Other Organic Friction Modifiers

- 5.2 By Form

- 5.2.1 Liquid

- 5.2.2 Solid (Powder / Dispersible)

- 5.3 By Application

- 5.3.1 Engine Oils

- 5.3.2 Transmission Fluids (ATF, DCTF, CVTF)

- 5.3.3 Gear Oils

- 5.3.4 Hydraulic Fluids

- 5.3.5 Greases

- 5.3.6 Metalworking Fluids

- 5.3.7 Other Specialty Lubricants

- 5.4 By End-user Industry

- 5.4.1 Automotive and Transportation

- 5.4.2 Industrial Manufacturing and Machinery

- 5.4.3 Aerospace and Aviation

- 5.4.4 Energy and Power Generation

- 5.4.5 Marine and Rail

- 5.4.6 Other End-user Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 ADEKA CORPORATION

- 6.4.2 Afton Chemical

- 6.4.3 BASF

- 6.4.4 Cargil Incorporated

- 6.4.5 Infineum International Ltd.

- 6.4.6 King Industries, Inc.

- 6.4.7 LANXESS

- 6.4.8 Lubrizol

- 6.4.9 Nouryon

- 6.4.10 Petronas Chemicals Group Berhad

- 6.4.11 R.T. Vanderbilt Holding Company, Inc.

- 6.4.12 Shamrock Technologies

- 6.4.13 The W Corporation

- 6.4.14 Yasho Industries Limited

- 6.4.15 ZSCHIMMER & SCHWARZ, INC.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment