|

시장보고서

상품코드

2062269

디스패치 콘솔 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Dispatch Console - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

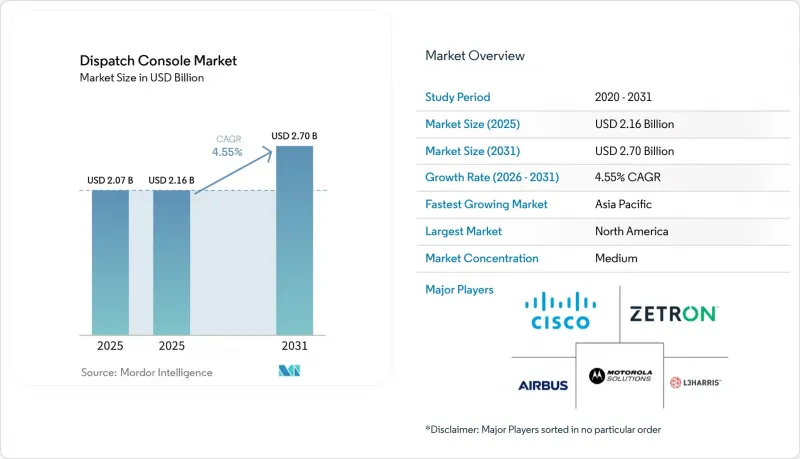

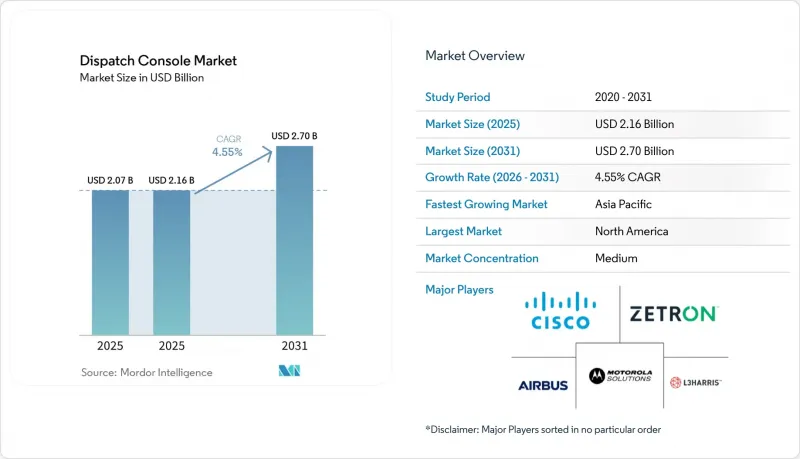

Mordor Intelligence에 의하면, 디스패치 콘솔 시장 규모는 2025년 20억 7,000만 달러로 평가되었고, 2026년 21억 6,000만 달러로 추정되고, 2031년까지 27억 달러로 확대될 전망이며, 2026-2031년 CAGR 4.55%를 나타낼 것으로 예측됩니다.

본 보고서는 구성 요소별(하드웨어 및 소프트웨어), 유형별(IP 기반 디스패치 콘솔 및 TDM 기반 디스패치 콘솔), 기능별(음성 디스패치, 텍스트 디스패치, 위치 정보 서비스, 실시간 모니터링 등), 최종 사용자 산업별(공공 안전 기관, 정부 및 국방, 운송 및 물류 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 디스패치 콘솔 시장 동향 및 인사이트

NG9-1-1 도입이 콘솔 업그레이드를 가속화

연방 및 주 정부의 규정에 따라 콜센터는 음성, 텍스트, 이미지, 동영상을 처리할 의무가 있으며, 이로 인해 공공 안전 기관은 멀티미디어 세션 시작 프로토콜(SIP) 피드를 지원하지 못하는 콘솔을 폐기해야 하는 상황에 처해 있습니다. 캔자스주, 오클라호마주 및 기타 선도 지역들은 2026년에 응급 서비스 IP 네트워크를 가동함으로써, 중앙 정부가 자금을 지원하는 프로그램이라면 2026년 연방 목표를 달성할 수 있음을 입증했습니다. 이미 지출이 4억 5,000만 달러를 넘어선 캘리포니아주의 비용 초과 사태는 조달이 분산되어 있을 때 발생할 수 있는 예산 위험을 여실히 드러내고 있습니다. 하드웨어 업데이트 외에도 각 기관은 녹음 시스템과 교육 과정의 현대화도 추진해야 하므로, 이로 인해 수년에 걸친 종합적인 설비 투자 주기가 형성되고 있습니다. 기기 인증을 신속하게 진행하고 단계적인 전환을 지원하는 벤더는 선점 우위를 확보하게 됩니다.

물류 분야에서의 클라우드 네이티브 CAD 및 디스패치 도입

차량 운영 사업자들은 온프레미스 서버를 없애고, 감독자가 어떤 기기에서든 업무를 관리할 수 있는 클라우드 기반 디스패치 스위트를 도입하는 경향이 강해지고 있습니다. 조지아주와 위스콘신주의 제안 요청서(RFP)에서는 가동 중단 시간을 거의 제로로 줄일 것, 브라우저 기반 인터페이스, 그리고 분석 대시보드를 명시적으로 요구하고 있습니다. 월정액 요금제를 통해 설비 투자가 운영비로 전환되고, 사내 승인 절차가 단축되므로 중소규모의 차량 운영 사업자에게도 매력적인 솔루션이 되고 있습니다. 다운타임의 위험은 로컬 하드웨어에서 광역 네트워크 연결로 전환됨에 따라 발생하므로, 공급업체는 안전성이 극히 중요한 이용 사례에 대응하기 위해 이중화된 통신 환경과 엄격한 서비스 수준 계약(SLA)을 함께 제공해야 합니다.

지연되는 공공 조달과 예산상의 장애물

공공 안전 기관은 다단계 승인 절차, 공청회, 입찰 이의 제기 가능성 등에 직면해 있어, 계약 체결까지 18-36개월이 소요될 수 있습니다. 일리노이주의 추가 수입은 운영비의 절반을 간신히 충당할 정도에 불과하여, 각 부서는 주정부의 보조금이 확보될 때까지 콘솔 교체를 미룰 수밖에 없습니다. 아르헨티나에서도 유사한 지연 현상이 나타나고 있으며, 230억 아르헨티나 페소(2,300만 달러) 규모의 911 시스템 업데이트 자금이 두 개의 예산 주기로 분할된 사례는 거시경제의 변동이 이미 승인된 프로젝트조차 좌초시킬 수 있음을 보여줍니다. 공급업체는 경쟁력을 유지하기 위해 브리지 보증과 유연한 지불 일정을 제공해야 합니다.

부문별 분석

각 기관이 콘솔, 무선 게이트웨이, 조절 가능한 가구의 감가상각을 7-10년에 걸쳐 지속함에 따라, 2025년 매출의 55.55%를 하드웨어가 차지했습니다. 오클라호마주의 주 전체 계약과 캔자스주의 카운티 차원 승인은 전용으로 설계된 인체공학 기반 책상이 범용 사무용 가구보다 여전히 높은 가격대를 유지하고 있음을 뒷받침하고 있습니다. 소프트웨어 매출 증가율은 연평균 4.63%로 하드웨어를 상회하고 있습니다. 이는 클라우드 구독, 매핑 확장 기능, 분석 모듈이 일회성 라이선스를 예측 가능한 월정액 요금제로 전환하고 있기 때문입니다. 예전에는 서버를 설치할 때 지게차가 필요했지만, 새로운 시스템을 도입한 후에는 몇 분 만에 가상 머신을 가동할 수 있으며, 업데이트는 심야에 자동으로 이루어집니다. 이러한 변화는 총 소유 비용을 절감해 주지만, 한편으로는 정부 기관을 공급업체의 로드맵에 얽매이게 하여 타사로의 전환에 많은 비용이 들게 만듭니다. 인공지능(AI) 워크로드가 증가함에 따라, 하드웨어 업데이트에는 추가적인 그래픽 처리 능력, 고해상도 모니터, 10기가비트 네트워크 업링크가 필요하게 되며, SaaS가 주류를 이루는 세상에서도 하드웨어 매출 증가를 뒷받침하게 될 것입니다.

번들화 추세는 계속되고 있으며, 2026년 입찰 프로젝트의 60% 이상에서 단일 통합업체가 하드웨어, 무선 인터페이스, 소프트웨어를 공급해야 합니다. 번들 계약은 거버넌스를 간소화하지만, 수년에 걸친 보증 비용을 감당할 수 없는 소규모 전문 업체에게는 가격 면에서 부담을 주게 됩니다. 베스트 오브 브리드 방식을 채택하는 구매자들은 향후 전환을 가능하게 하기 위해 표준 기반 API나 객체 수준의 데이터 내보내기 기능을 강력히 요구하고 있지만, 이러한 조항이 지자체 RFP 양식에 포함되는 경우는 드물며, 그 결과 벤더 종속 현상이 지속되고 있습니다.

2025년에는 IP 기반 콘솔이 매출의 67.75%를 차지했지만, 디스패치 콘솔 시장에서는 여전히 결정론적 지연과 독립형 신뢰성이 기능보다 우선시되는 광산, 석유 시추 시설, 지방 유틸리티 분야를 대상으로 수천 대의 TDM 단말기가 판매되었습니다. IP 시스템은 광대역 네트워크와 원활하게 통합되어 멀티미디어 통화를 지원하며, 가상화된 재해 복구 거점을 구축할 수 있게 해줍니다. 이 모든 것은 도시 지역의 기관들에게 매력적인 이점입니다. 한편, TDM의 5.05%라는 성장률은 광섬유가 부족한 신흥 시장의 유틸리티자들이 새로운 구리선이나 마이크로파 회선을 설치하고 있음을 반영하고 있습니다. 통신 사업자들이 급격한 전환을 피하는 가운데, 세션 시작 프로토콜(SIP)과 회선 교환 신호 체계 간 변환을 수행하는 상호 운용성 게이트웨이는 여전히 활기를 띠고 있는 하위 부문입니다. 게이트웨이용 디스패치 콘솔 시장 규모는 하이브리드 아키텍처의 보급에 힘입어 2031년까지 2억 7,000만 달러에 달할 것으로 전망됩니다.

벤더의 로드맵에 따르면, 2020년대 후반 통신 사업자들이 협대역 전용선을 폐지할 때 전환점이 올 것으로 예측됩니다. 서비스 제공업체가 올-IP 백본으로 전환하면, 업데이트 수요가 급증하여 10년 치의 업그레이드가 3년 동안 집중될 것입니다. 현장에서 교체 가능한 IP 인터페이스 카드와 이용 규모에 따른 라이선스 체계를 갖춘 공급업체는 이러한 수요 급증을 포착할 수 있는 유리한 위치에 서게 될 것입니다.

지역별 분석

2025년 기준으로 북미는 디스패치 콘솔 시장의 36.67%를 차지했습니다. 워싱턴주의 4,800만 달러 규모의 주 전역에 걸친 긴급 서비스 IP 네트워크 확장 사업과 뉴욕주의 8,500만 달러 규모의 카운티 지원 프로그램 등 여러 주에 걸친 계약을 통해 2031년까지의 확실한 수주 전망이 뒷받침되고 있습니다. 캐나다는 2027년까지 전국에 차세대 911 기능을 도입하도록 의무화하고, 2,500만 캐나다 달러(1,800만 달러) 규모의 자금을 단계적으로 지원함으로써 콘솔 발주를 가속화하고 있습니다. 그렇긴 하지만, 2025년도 미국 예산에서 연방 정부의 매칭 자금이 삭제됨에 따라 재정 부담이 각 주로 전가되면서, 소규모 관할 구역에서의 조달 기간이 길어지고 있습니다. FirstNet과의 통합에는 추가 인증이 필요하며, 도입 계획 기간은 6개월에서 9개월로 늘어납니다만, 완료되면 고대역폭 영상이나 드론 영상을 콘솔에 직접 불러올 수 있게 됩니다.

아시아태평양은 연평균 성장률(CAGR) 4.76%로 가장 높은 성장률을 보이고 있습니다. 인도의 100개 도시를 대상으로 한 스마트시티 구상에서는 14만 2,000대 이상의 카메라를 감시하는 통합 지휘관제센터가 구축되고 있으며, 첨단 영상 분석 기능을 갖춘 IP 카메라의 대규모 발주가 예고되고 있습니다. 중국의 메가시티 지역에서는 이보다 훨씬 더 대규모의 사업이 진행되고 있지만, 국내 조달 정책에 따라 현지 공급업체가 우선적으로 선정되고 있습니다. 두바이의 엔터프라이즈 지휘통제센터는 2만 8,000대의 차량을 관리하며 하루 평균 44억 건의 데이터 포인트를 수집하고 있는데, 이는 중동에서 처리량이 높고 AI를 지원하는 콘솔에 대한 수요가 높음을 보여줍니다. 일본과 한국은 단계적인 업그레이드에 주력하고 있으며, 기존 투자가 5G 및 자율주행차 시범 운영과 연계될 수 있도록 시스템을 전면적으로 교체하지 않고도 대응 방안을 모색하고 있습니다.

유럽에서는 전자통신법(Electronic Communications Code)의 요건을 충족하기 위해 현대화가 진행되고 있습니다. 영국 내 ‘Guardian Hub’ 및 10년간의 모바일 순찰 시스템에 관한 계약은 장기적인 운영 예산을 투입할 의사가 있음을 보여줍니다. 헥사곤(Hexagon)이 유럽의 녹화 솔루션 제공업체를 1,000만 유로(1,130만 달러)에 인수한 것은 EU의 데이터 거주 요건을 충족하는 상호운용성 솔루션을 강화하기 위한 조치입니다. 남미에는 확실한 기회가 있지만, 시장은 세분화되어 있습니다. 아르헨티나와 브라질의 지방 자치단체 구매 담당자들은 대규모 입찰을 공고하고 있지만, 예측 불가능한 환율 변동과 연방 정부의 자금 이체에 대한 제약에 직면해 있습니다. 사우디아라비아의 ‘키디야 스마트 커맨드 센터’와 같은 중동의 메가 프로젝트는 전 세계 공급업체들이 모범 사례로 삼는 사례를 만들어내고 있습니다. 아프리카 시장은 아직 발전 단계에 있지만, 남아프리카공화국, 나이지리아, 이집트의 일부 대도시권에서는 타당성 조사가 시작되었으며, 이는 예측 기간 후반에 그린필드 방식의 IP 콘솔 도입 열풍이 불어올 가능성을 시사하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the dispatch console market size is projected to expand from USD 2.07 billion in 2025, USD 2.16 billion in 2026, to USD 2.70 billion by 2031, registering a 4.55% CAGR over 2026-2031.

This report is Segmented by Component (Hardware and Software), Type (IP-Based Dispatch Console and TDM-Based Dispatch Console), Functionality (Voice Dispatch, Text Dispatch, Geo-Location Services, Real-Time Monitoring, and More), End-User Industry (Public Safety Agencies, Government and Defense, Transportation and Logistics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Dispatch Console Market Trends and Insights

NG9-1-1 Deployments Speeding Up Console Upgrades

Federal and state mandates require call centers to accept voice, text, image, and video, prompting public safety agencies to scrap consoles incapable of multimedia Session Initiation Protocol feeds. Kansas, Oklahoma, and other early movers brought Emergency Services IP Networks online in 2026, validating that centrally funded programs can meet the 2026 federal target. Cost overruns in California, where spending already exceeds USD 450 million, underscore the budget risk when procurement is fragmented. Alongside hardware refreshes, agencies must modernize recording systems and training curricula, creating a bundled multi-year capital cycle. Vendors that certify equipment quickly and support phased cutovers gain an early-mover advantage.

Cloud-Native CAD and Dispatch Adoption in Logistics

Fleet operators increasingly subscribe to cloud dispatch suites that eliminate on-premises servers and allow supervisors to manage operations from any device. Requests for proposals in Georgia and Wisconsin call explicitly for near-zero downtime, browser-based interfaces, and analytics dashboards. Monthly fees convert capital outlays into operating expenses, shortening internal approval cycles and making solutions attractive to small and mid-sized fleets. Downtime risk shifts from local hardware to wide-area connectivity, so suppliers must bundle redundant telecommunications and rigorous Service Level Agreements to satisfy safety-critical use cases.

Slow Public Procurement and Budget Hurdles

Public safety agencies navigate multi-step approval chains, public hearings, and potential bid protests that can stretch contract awards to 18-36 months. Illinois surcharge revenue funds barely cover half of operational costs, forcing departments to defer console refreshes until state grants materialize. Similar delays in Argentina, where funding for a ARS 23 billion (USD 23 million) 911 upgrade is split across two budget cycles, illustrate how macro-economic swings derail even approved projects. Vendors must provide bridge warranties and flexible payment schedules to remain competitive.

Other drivers and restraints analyzed in the detailed report include:

- Grid Modernization Boosting Demand from Utilities

- Roll-Out of Public-Safety Broadband Networks

- High Cost of Cyber-Security Upgrades

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware contributed 55.55% of 2025 sales as agencies continued to amortize consoles, radio gateways, and adjustable furniture over 7-10 years. A statewide contract in Oklahoma and county-level approvals in Kansas affirmed that purpose-built ergonomic desks still command a premium over generic office fixtures. Growth in software revenue outpaces hardware at 4.63% annually because cloud subscriptions, mapping extensions, and analytics modules transform one-time licenses into predictable monthly recurring charges. Where servers once required forklifts, new deployments spin up virtual machines in minutes, and updates push automatically after midnight. This shift cuts total cost of ownership yet locks agencies into vendor roadmaps, making exit switches expensive. As artificial intelligence workloads rise, hardware refreshes will require additional graphics processing, higher-resolution monitors, and 10 gigabit network uplinks, fueling incremental hardware sales even in a SaaS world.

The bundling trend continues: more than 60% of 2026 solicitations require a single integrator to supply furniture, radio interface, and software. Bundled deals simplify governance but put price pressure on smaller specialists that cannot finance multi-year warranties. Best-of-breed buyers insist on standards-based APIs and object-level data export so future migrations remain possible, but those clauses rarely appear in municipal RFP templates, perpetuating supplier lock-in.

IP-based consoles accounted for 67.75% revenue in 2025, yet the dispatch console market still sold thousands of TDM positions to mines, oil rigs, and rural utilities where deterministic latency and standalone reliability trump features. IP systems integrate seamlessly with broadband networks, support multimedia calls, and enable virtualized disaster-recovery positions, all compelling perks for urban agencies. Conversely, a 5.05% growth rate for TDM reflects emerging-market utilities laying new copper or microwave links where fiber is scarce. Interoperability gateways that translate between Session Initiation Protocol and circuit-switched signaling remain a thriving subsegment, as agencies avoid flash-cut migrations. The dispatch console market size for gateways is projected to reach USD 270 million by 2031, rising alongside hybrid architectures.

Vendor roadmaps suggest the inflection point will arrive as carriers sunset narrowband private lines in the late 2020s. Once service providers roll over to all-IP backbones, replacement demand will spike, compressing a decade of upgrades into a three-year window. Suppliers with field-swappable IP interface cards and pay-as-you-grow licensing will be positioned to capture the surge.

Geography Analysis

North America represented 36.67% of the dispatch console market in 2025. Multi-state contracts, such as Washington's USD 48 million statewide Emergency Services IP Network extension and New York's USD 85 million county grant program, underpin a visible pipeline through 2031. Canada mandated Next Generation 911 functionality nation-wide by 2027, releasing CAD 25 million (USD 18 million) funding tranches that accelerate console orders. Nonetheless, the removal of federal matching funds from the 2025 U.S. budget shifted financial burden to states, elongating procurement for smaller jurisdictions. FirstNet integration obliges additional certification, increasing deployment planning from six to nine months but, once complete, enabling high-bandwidth video and drone feeds to flow directly into consoles.

Asia-Pacific offers the fastest 4.76% CAGR. India's 100-city smart-city initiative rolled out Integrated Command and Control Centers that monitor 142,000-plus cameras, evidence of large orders for IP positions with advanced video analytics. China's megacity clusters replicate this at even larger scales, though domestic procurement policies favor local suppliers. Dubai's Enterprise Command and Control Center coordinates 28,000 vehicles and ingests 4.4 billion daily data points, showcasing the Middle Eastern appetite for high-throughput, AI-enabled consoles. Japan and South Korea focus on incremental upgrades, ensuring existing investments interface with 5G and autonomous vehicle trials without wholesale rip-and-replace.

Europe modernizes to meet Electronic Communications Code requirements. Contracts in the United Kingdom for Guardian Hub and 10-year mobile policing suites demonstrate willingness to commit long-term operating budgets. Hexagon's EUR 10 million (USD 11.3 million) acquisition of a European recording solutions provider strengthens interoperability offerings that fit EU data residency mandates. South America's opportunity is real but fragmented; provincial buyers in Argentina and Brazil publish sizable tenders yet face unpredictable foreign-exchange swings and constrained federal transfers. Middle East mega-projects such as Saudi Arabia's Qiddiya Smart Command Center create lighthouse references that vendors cite globally. Africa remains nascent but selected metros in South Africa, Nigeria, and Egypt are starting feasibility studies, hinting at a potential wave of greenfield IP console deployments late in the forecast horizon.

- Motorola Solutions, Inc.

- Hexagon AB

- CentralSquare Technologies, LLC

- Airbus SE

- Hytera Communications Corporation Limited

- L3Harris Technologies, Inc.

- Omnitronics Pty Limited

- Cisco Systems, Inc.

- RapidDeploy, Inc.

- EFJohnson Technologies, Inc.

- Catalyst Communications Technologies, Inc.

- Saab AB

- Telex Radio Dispatch

- Avaya LLC

- InterTalk Critical Information Systems

- Frequentis AG

- Esri, Inc.

- ZETRON Inc.

- Synch Systems, Inc.

- Avtec Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 NG9-1-1 Deployments Speeding Up Console Upgrades

- 4.2.2 Cloud-Native CAD and Dispatch Adoption in Logistics

- 4.2.3 Grid Modernization Boosting Demand from Utilities

- 4.2.4 Roll-Out of Public-Safety Broadband Networks

- 4.2.5 AI-Assisted Dispatch Optimising Response Workflows

- 4.2.6 Private 5G Pilots in Industrial Campuses Enabling IP Dispatch

- 4.3 Market Restraints

- 4.3.1 Slow Public Procurement and Budget Hurdles

- 4.3.2 High Cost of Cyber-Security Upgrades

- 4.3.3 Vendor Lock-In Risks in Integrated Suites

- 4.3.4 Scarcity of Dispatch-Ready Spectrum Bands Below 1 GHz

- 4.4 Industry Ecosystem Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Threat of Substitutes

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Bargaining Power of Buyers

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.2 By Type

- 5.2.1 IP-Based Dispatch Console

- 5.2.2 TDM-Based Dispatch Console

- 5.3 By Functionality

- 5.3.1 Voice Dispatch

- 5.3.2 Text Dispatch

- 5.3.3 Geo-Location Services

- 5.3.4 Real-Time Monitoring

- 5.3.5 Data Analytics and Reporting

- 5.4 By End-User Industry

- 5.4.1 Public Safety Agencies

- 5.4.2 Government and Defense

- 5.4.3 Transportation and Logistics

- 5.4.4 Healthcare

- 5.4.5 Manufacturing

- 5.4.6 Mining, Energy, and Utilities

- 5.4.7 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Kuwait

- 5.5.5.4 Bahrain

- 5.5.5.5 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Motorola Solutions, Inc.

- 6.4.2 Hexagon AB

- 6.4.3 CentralSquare Technologies, LLC

- 6.4.4 Airbus SE

- 6.4.5 Hytera Communications Corporation Limited

- 6.4.6 L3Harris Technologies, Inc.

- 6.4.7 Omnitronics Pty Limited

- 6.4.8 Cisco Systems, Inc.

- 6.4.9 RapidDeploy, Inc.

- 6.4.10 EFJohnson Technologies, Inc.

- 6.4.11 Catalyst Communications Technologies, Inc.

- 6.4.12 Saab AB

- 6.4.13 Telex Radio Dispatch

- 6.4.14 Avaya LLC

- 6.4.15 InterTalk Critical Information Systems

- 6.4.16 Frequentis AG

- 6.4.17 Esri, Inc.

- 6.4.18 ZETRON Inc.

- 6.4.19 Synch Systems, Inc.

- 6.4.20 Avtec Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment