|

시장보고서

상품코드

2062337

군용 조명 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Military Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

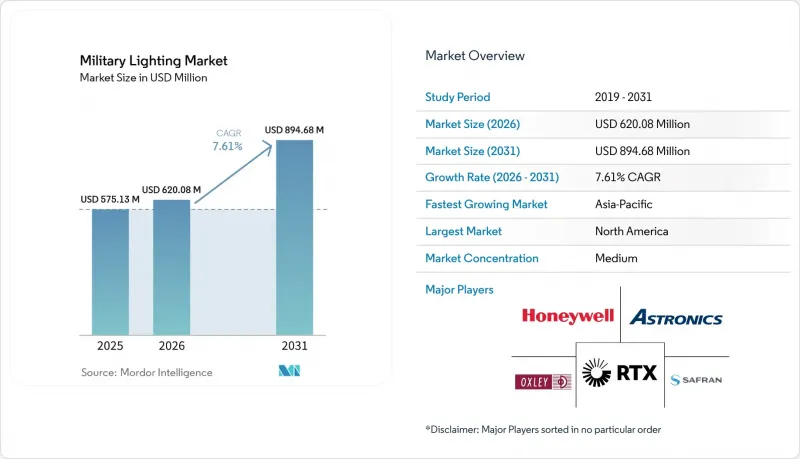

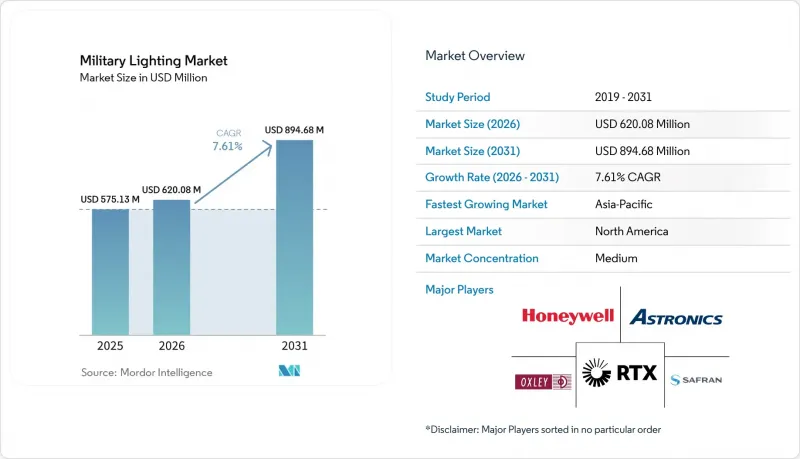

Mordor Intelligence에 의하면, 군용 조명 시장 규모는 2025년 5억 7,513만 달러, 2026년 6억 2,008만 달러에서 2031년까지 8억 9,468만 달러로 확대되어 2026년부터 2031년까지 CAGR 7.61%를 나타낼 것으로 예측됩니다.

본 보고서는 플랫폼(항공, 육상, 해상), 기술(LED, 백열등/할로겐, OLED 및 마이크로 LED, 트리튬 및 베타라이트), 솔루션(하드웨어, 소프트웨어, 서비스), 용도(실내 및 실외), 최종 사용자(육군, 해군, 공군), 지역(북미, 유럽, 아시아태평양, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 군용 조명 시장 동향 및 분석

LED로 개조함으로써 전력 소비를 줄이고 플랫폼의 적외선 시그니처를 감소시켰습니다.

LED로의 전환은 군용 조명 시장에서의 점유율 확대에 따라, 단순한 권장 옵션에서 프로그램 요건으로 자리 잡고 있습니다. 하네웰의 CH-47용 LED 적색/IR 듀얼 모드 충돌 방지등은 기존의 크세논 ACL을 대체하여 전력 소비를 최대 52% 절감하고, 무게를 65% 줄였으며, 광수명은 최대 40,000시간에 달할 전망입니다. 이러한 이점들은 정기 유지보수 요건을 줄이고, 항공기 가동률을 높이며, 플래시 튜브나 커패시터 뱅크의 정기적인 교체 필요성을 없애줌으로써, 견고한 유지보수 계획 수립에 기여합니다. 그 가치는 효율성에 그치지 않고, 솔리드 스테이트 시스템은 구형 조명 어셈블리가 적대적인 열 센서에 쉽게 감지되는 원인이 되는 불필요한 열과 광대역 복사를 억제하는 데에도 도움이 됩니다. 실제로, 군용 조명 시장은 LED로의 전환으로 인해 혜택을 보고 있습니다. 이를 통해 유지보수 횟수가 줄어들고 신뢰성이 향상되며, 전력 효율을 중시하는 플랫폼 설계로 향하는 광범위한 추세와 부합합니다. 이러한 요인들은 일반적인 프로그램 예산 범위 내에서 투자 회수 기간을 단축시켜 주며, 조달 팀이 중요도가 낮은 하위 시스템의 도입을 미루라는 압력을 받고 있는 상황에서도 개조 수요를 유지하는 데 도움이 됩니다.

규정에 따라 의무화된 NVIS 업그레이드로 인해 전 기체 규모의 조종석 교체가 불가피해졌습니다.

MIL-STD-3009는 야간 투시 영상 시스템과 연동하여 작동하는 항공기 시스템에 적용되며, 조명이 장착된 조종실 부품의 방사 휘도, 색도 및 휘도 성능을 규정하고 있기 때문에 군용 조명 시장에서 가장 명확한 구조적 촉진요인 중 하나로 자리 잡고 있습니다. 이 규격은 현재도 유효하며, DLA(국방물자국)는 ‘통지 2-검증’에서 문서 날짜를 2024년 4월로 명시하고 있으며, 다음 검토는 2029년 4월로 예정되어 있습니다. 이를 통해 조종실, 디스플레이 및 조명 제어 장치의 업데이트 프로그램에 관여하는 항공기 운영사, 조명 공급업체 및 개조 팀에게 지속적인 규정 준수의 중요성이 보장됩니다. 따라서 디스플레이, 패널, 표시등, 키보드 또는 푸시 버튼 스위치와 관련된 모든 항공 전자 시스템은 비록 초기 프로그램 목표가 조명 프로젝트로 설정되지 않았더라도, 더 광범위한 조명 교체 요구 사항을 초래할 가능성이 있습니다. 옥슬리 그룹의 MIL-STD-3009 준수 NVIS 조종실 구성품 및 C-130 업그레이드 프로젝트는 NATO의 승인을 받은 C-130 조명 개조가 국제적인 C-130 운용사들에게 얼마나 높은 적응성을 제공하는지를 보여줍니다. 이러한 접근 방식은 조종실 조명에 그치지 않고 외부 조명, 화물실 조명 및 적재 램프 조명 솔루션까지 확대되어 항공기의 수명 연장에 기여합니다. 그 결과, 군용 조명 시장은 단순히 새로운 플랫폼의 생산뿐만 아니라, 주로 규격에 따른 업데이트 덕분에 혜택을 보고 있습니다.

고신뢰성 GaN LED공급 제약으로 인해 부품 리드타임 관련 리스크가 증가

고신뢰성 GaN 소자는 드라이버 서브시스템의 가혹한 열, 스위칭 및 전력 조건에 대응할 수 있어, 첨단 군용 조명 시장 용도에서 성능의 한계에 근접한 수준에 도달했습니다. 이러한 제약 요인으로는 공급망이 여전히 원자재의 집중 공급이나 반도체 병목 현상에 직면해 있다는 점을 들 수 있습니다. 방위사업위원회(Defense Business Board)는 희토류 및 갈륨 생산 분야에서 중국의 지배적인 역할을 지적하고 있습니다. 미국 주도로 신뢰성 높은 공급 체계를 구축하기 위한 노력이 진행되고 있습니다. EPC Space는 GaN HEMT의 JANS MIL-PRF-19500 인증을 획득했다고 발표했으며, 2025년 5월 QPL 갱신을 통해 자사 최초의 인증 완료된 파워 GaN JANS 소자를 도입했습니다. 이 회사는 또한 향후 12개월 동안 16종의 GaN JANS 디바이스를 추가로 인증할 계획이라고 밝혔습니다. 하지만, 인증된 공급량은 여전히 제한적이기 때문에 높은 신뢰성을 요구하는 GaN 기반 전자 기기에 의존하는 군용 조명 시장 프로그램의 경우, 여전히 긴 리드타임과 불안정한 공급 상황에 직면할 가능성이 있습니다. 이는 부품 인증을 단기간 내에 대체할 수 없는 항공기 탑재용이나 고사양 지상 프로그램에서 매우 중요한 문제입니다. 웨이퍼 생산 능력이 인증될 때까지는 조달 팀이 첨단 조명 계약에 대해 계속해서 일정상의 여유를 두게 될 것입니다.

부문별 분석

2025년에는 항공기용이 매출의 42.45%를 차지하며, 플랫폼당 조명 탑재량이 여전히 가장 많기 때문에 이 부문은 군용 조명 시장에서 가장 큰 점유율을 차지하고 있습니다. 고정익기 및 회전익기 플랫폼에는 조종실, 항법, 충돌 방지, 착륙, 점검 및 스텔스 조명 시스템이 밀집된 배열이 필요하며, 이로 인해 항공기용 프로그램은 업데이트 수요와 신규 생산 수요 모두에서 계속해서 핵심적인 위치를 차지하고 있습니다. NVIS(비가시광선) 규격 준수는 다른 플랫폼군에 비해 항공기 분야에서 더욱 중요하게 여겨지며, 이 부문은 MIL-STD-3009의 업데이트 주기와 조종실 현대화 예산과 밀접하게 연관되어 있습니다. 항공기 외부 조명은 장기간 운용되는 동안 진동과 기상 조건에 노출되며 엄격한 인증 기준을 충족해야 하므로, 단가가 높은 임베디드니다. 따라서 방위 조달 시장 전체가 해마다 들쑥날쑥한 움직임을 보일지라도, 항공기용 조명은 여전히 군사 조명 시장의 핵심을 차지하고 있습니다.

해군 분야 수요는 안정적이지만, 함내 및 갑판 조명의 교체 주기가 길고, 연간 조달 피크보다는 플랫폼 개조 기간에 따라 좌우되기 때문에 그 흐름은 비교적 완만합니다. 육상 플랫폼 부문은 가장 빠르게 성장하고 있으며, 2031년까지 연평균 성장률(CAGR)이 8.75%를 나타낼 것으로 전망되어, 군용 조명 시장에서 다음 대규모 전환의 물결이 어디에서 형성되고 있는지를 보여주고 있습니다. 장갑차, 전술 차량 및 쉘터에서의 조명 수요는 LED 기반이며, NVG(야간 투시경) 및 IR(적외선)에 대응하고 유지보수가 간편한 솔루션으로 전환되고 있습니다. 예산 배분에서는 전술 차량의 현대화, JLTV(차세대 경전차) 개조, 쉘터 통합, 전력 분배, 지휘통제(C2) 시스템 업그레이드, 그리고 노후화 문제 대응이 우선시되고 있습니다. 공급업체의 데이터에 따르면, 군용 차량과 대피소에서 LED 기술이 널리 채택되고 있습니다. 하네웰사가 MV-75 FLRAA LED 착륙 및 탐색등을 채택한 것은 차세대 군용 항공 플랫폼 및 기타 가혹한 군사 용도 분야에서 LED를 우선시하는 설계 요건에 대한 중요성이 커지고 있음을 보여줍니다.

2025년에는 매출의 56.80%를 LED가 차지하며, 군용 조명 시장에서 가장 확고히 자리 잡은 기술이 되었습니다. 이 위상은 외장 어셈블리, 조종석용 유틸리티 조명, 차량 시스템 및 군사 시설에서의 사용 현황을 반영한 것으로, 이러한 분야에서는 긴 수명, 낮은 유지보수 비용, 낮은 전력 소비가 이전보다 조달 결정에 있어 더 중요한 요소가 되고 있습니다. 또한, 미국 국방부(DoD)의 조달 규정이 효율적인 솔리드 스테이트 시스템을 점점 더 우선시하고 있다는 점과, 국내 조달 요건으로 인해 향후 계약에서 승인된 공급업체의 범위가 좁아지고 있다는 점도 이 기술의 보급을 뒷받침하고 있습니다. 백열등이나 할로겐 시스템은 호환성, 열 성능, 혹은 기존 설계상의 제약으로 인해 대체가 어려운 분야에서 여전히 일정한 수요가 남아 있습니다. 그럼에도 불구하고, 새로운 플랫폼 주기가 반복될 때마다 그 점유율은 계속 줄어들고 있습니다. 따라서 군용 조명 시장에서 LED는 신규 조달 시 기본적인 선택지일 뿐만 아니라, 구형 기체 개조 시에도 여전히 주요한 선택지로 자리 잡고 있습니다.

OLED와 마이크로 LED는 2031년까지 연평균 성장률(CAGR)이 8.95%로 가장 빠르게 성장하고 있는 기술입니다. 이는 첨단 조종석 디스플레이나 HUD(헤드업 디스플레이)와 같은 용도에서는 표준 조명 모듈이 제공하는 수준을 뛰어넘는 높은 휘도, 더욱 정밀한 명암비 제어, 그리고 뛰어난 전력 대비 성능이 요구되기 때문입니다. 이러한 변화는 조종석 경계와 가장 가까운 영역에서 일어나고 있으며, 항공기 현대화 작업 과정에서 디스플레이 시스템과 조명 요건의 경계가 점점 더 모호해지고 있습니다. 따라서 군용 조명 시장은 램프나 조명 기구뿐만 아니라, 주야를 가리지 않고 조종사의 시인성을 높여주는 디스플레이 연동형 광학 시스템을 통해 확대되고 있습니다. 트리튬 및 베타라이트 용액은 배터리, 배선, 외부 전원이 필요 없는 자체 발광 기능이 요구되는 군사 용도, 예를 들어 조준기, 나침반, 계기, 마커, 안전 장치 등에 적합합니다. 그러나 10 CFR 32.22 및 10 CFR 32.53과 같은 규정에 따라 라이선스, 안전성, 표시, 취급 및 이전에 관한 요건이 부과되어 있어, 기존의 전기 조명에 비해 확장성이 제한됩니다. LED 기술은 여전히 대부분의 군용 조명 분야에서 주요 선택지이지만, OLED와 마이크로 LED는 조종석 디스플레이, HUD, 헤드마운트 시스템, 그리고 병사용 비전 인터페이스를 위한 새로운 대안으로 부상하고 있습니다.

지역별 분석

2025년, 북미는 매출의 36.60%를 차지하며 군용 조명 시장에서 가장 큰 비중을 차지하는 지역이 되었습니다. 해당 지역은 미국의 방위 조달 규모, 장기적인 항공기 업그레이드 계획, 그리고 향후 계약에서 LED 채택 및 국내 조달 요건 준수를 뒷받침하는 규제 체계의 혜택을 누리고 있습니다. 2026년 1월 하네웰사가 MV-75 FLRAA용 LED 착륙 탐조등 공급업체로 선정된 점과, 아스트로닉스사의 군용기용 판매가 확대되고 있는 점은 고부가가치 군용기 조명 및 안전 시스템 분야에서 북미가 차지하는 역할에 대해 차세대 미국 항공 프로그램이 미치는 영향이 확대되고 있음을 여실히 보여주고 있습니다. 그러나 이는 광범위한 군사 조명 시장에서 북미의 우위를 결정적으로 입증하는 것은 아니며, 오히려 미국 프로그램의 성장세가 견고함을 보여주는 증거라고 할 수 있습니다.

유럽은 여전히 2위 지역으로, 인증된 군용 조명 시장에서 중요한 수요처로 자리 잡고 있습니다. 이는 NATO 회원국의 항공기 및 방위 자율화 프로그램이 현지 공급 체계를 지속적으로 뒷받침하고 있기 때문입니다. 영국, 프랑스, 독일은 NVIS(비가시광선) 및 외부 조명 인증 실적을 보유한 검증된 공급업체를 우선적으로 선정하는 국가 및 다자간 플랫폼 프로그램을 운영하고 있습니다. 옥슬리 그룹이 영국 및 동맹국의 항공기 함대에 대한 NVIS 항공기 업그레이드 과정에서 쌓은 풍부한 경험은 국내 공급업체의 장기적인 참여를 유지하는 데 있어 인증, 기존 플랫폼에 대한 전문 지식, 그리고 국가의 지원이 얼마나 중요한지를 여실히 보여주고 있습니다. 콜린스 에어로스페이스가 유로파이터, A400M, 토네이도, 그리펜 등 각 플랫폼에 조명 장비를 탑재한 것은 유럽의 다국적 항공기 부대를 지원하는 이 회사의 역할을 여실히 보여주고 있습니다. 이러한 존재감은 단일 국가의 항공기 부대에 국한되지 않고, 다양한 운용자와 국가들 사이에서 지속적인 수요를 이끌고 있습니다. 이는 해당 항공기의 연장된 수명 기간 동안 필요한 플랫폼 유지보수, 개조, 예비 부품 및 NVIS/LED 업그레이드에 있어 특히 중요합니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 8.05%를 나타낼 것으로 예측되며, 군용 조명 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 주요 요인으로는 사상 최고 수준에 달한 국방 예산, 활발한 플랫폼 조달, 그리고 일본, 인도 및 기타 지역 동맹 프로그램에서 야간 투시 능력 및 상호 운용성 요건에 대한 대응이 진전되고 있다는 점을 들 수 있습니다. 일본은 2026년도 국방 예산으로 9조 400억 엔(578억 7,000만 달러)을 승인했습니다. 여기에는 JS 이즈모 및 JS 카가호 항공모함 개조 공사에 필요한 자금이 포함되어 있으며, 갑판 조명 및 관련 착륙 지원 시스템이 대상입니다. 인도의 2026-2027년도 국방 예산은 78.5조 루피(902억 달러)에 달하며, 이러한 지출로 인해 광범위한 현대화 과정을 통해 조종석, 차량 및 항공기 등급 조명 시스템에 대한 수요가 증가할 것으로 예측됩니다. 일본 항공자위대(JASDF)의 조달 기록에 따르면, LED 기반 조명의 구매가 반복되고 있으며, 납품은 2026년 초로 예정되어 있습니다. 이는 주요 국방 예산과 일상적인 조달 모두에서 지역적으로 LED 조명으로의 전환이 진행되고 있음을 보여줍니다. 한국이 SWIR(단파장 적외선) 기반의 아군·적군 식별 장비를 도입한 것은 첨단 저가시성 조명에 대한 관심을 뒷받침하고 있습니다. 중동 및 아프리카에서는 조명 시장 규모가 작지만, 사우디아라비아나 UAE 등 국가들의 함대 현대화, 방위 시설 업그레이드, 그리고 현지 방위 산업화 노력이 수요를 견인하고 있습니다. 남미의 경우 여전히 기회는 제한적이지만, 일부 시장에서는 재정적 압박으로 인해 조달 속도가 둔화되고 있는 반면, 노후화된 함대의 현대화 수요가 시장을 지탱하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the military lighting market size is projected to expand from USD 575.13 million in 2025 and USD 620.08 million in 2026 to USD 894.68 million by 2031, registering a CAGR of 7.61% between 2026 and 2031.

This report is Segmented by Platform (Airborne, Land, and Naval), Technology (LED, Incandescent/Halogen, OLED and Micro-LED, and Tritium and Betalights), Solution (Hardware, Software, and Services), Application (Interior and Exterior), End-User (Army, Navy, and Air Force), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Military Lighting Market Trends and Insights

LED Retrofitting Cuts Power Consumption and Reduces Platform IR Signatures

LED retrofitting has moved from a preferred option to a program requirement across a growing share of the military lighting market. Honeywell's CH-47 LED red/IR dual-mode anti-collision light replaces the traditional xenon ACL, providing up to 52% lower power consumption, a 65% weight reduction, and a photometric life of up to 40,000 hours. These benefits contribute to a robust sustainment case by reducing scheduled maintenance requirements, enhancing aircraft availability, and eliminating the need for routine flashtube and capacitor-bank replacements. The value extends beyond efficiency because solid-state systems also help limit unwanted heat and broad-spectrum emission that can make older lighting assemblies more visible to hostile thermal sensors. In practice, the military lighting market benefits from LED conversions, which reduce maintenance events, improve reliability, and align with the broader move toward more power-conscious platform design. These factors also shorten payback periods within normal program funding windows, which helps sustain retrofit demand even when procurement teams face pressure to delay less critical subsystems.

Standard-Mandated NVIS Upgrades Force Fleet-Wide Cockpit Replacements

MIL-STD-3009 remains one of the clearest structural drivers in the military lighting market because it applies to aircraft systems that operate with night vision imaging systems and governs radiance, chromaticity, and luminance performance for illuminated cockpit components. The standard remains active, with the DLA listing a document date of April 2024 in Notice 2 - Validation, and the next review is scheduled for April 2029, ensuring ongoing compliance relevance for aircraft operators, lighting suppliers, and retrofit teams involved in cockpit, display, and illuminated-control refresh programs. Every avionics system that touches displays, panels, indicators, keyboards, or push-button switches can, therefore, trigger a broader lighting replacement requirement, even when the original program objective is not framed as a lighting project. Oxley Group's MIL-STD-3009-compliant NVIS cockpit components and C-130 upgrade projects illustrate the adaptability of a NATO-approved C-130 lighting modification for international C-130 operators. This approach extends beyond cockpit lighting to include external, cargo cabin, and loading ramp lighting solutions, thereby supporting the aircraft's extended service life. As a result, the military lighting market benefits primarily from standards-driven replacements rather than solely from the production of new platforms.

High-Reliability GaN LED Supply Constraints Add Component Lead-Time Risk

High-reliability GaN devices sit close to the performance ceiling for advanced military lighting market applications because they support demanding thermal, switching, and power conditions in driver subsystems. The constraint is that their supply chain remains exposed to material concentration and semiconductor chokepoints, with the Defense Business Board noting China's dominant role in rare earths and gallium production. US-linked high-reliability supply response is in progress. EPC Space has announced JANS MIL-PRF-19500 certification for GaN HEMTs and, in its May 2025 QPL update, introduced its first qualified Power GaN JANS devices. The company also stated its intention to qualify 16 additional GaN JANS devices over the next 12 months. Even so, certified volume remains limited, meaning military lighting market programs that depend on high-reliability GaN-based electronics can still face long lead times and uneven supply availability, which is vital in airborne and high-specification ground programs where component qualification cannot be substituted at short notice. Until wafer capacity is certified, procurement teams will continue to build schedule buffers into advanced lighting contracts.

Other drivers and restraints analyzed in the detailed report include:

- Dual-Mode Visible/IR Beacons Enable Multinational Coalition IFF Operations

- DoD Zero-Maintenance Policy Systematically Displaces Incandescent Technology

- EM/EMC Certification Thresholds Create Non-Trivial Program Schedule Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Airborne accounted for 42.45% of revenue in 2025, giving this segment the largest footprint in the military lighting market as aircraft continue to carry the highest lighting content per platform. Fixed-wing and rotary platforms require dense arrays of cockpit, navigation, anti-collision, landing, inspection, and covert lights, which keep airborne programs central to both replacement and new-production demand. NVIS compliance also weighs more heavily in aircraft than in other platform groups, which ties the segment closely to MIL-STD-3009 refresh cycles and cockpit modernization budgets. Exterior lighting on aircraft tends to command higher unit values because assemblies must withstand vibration, weather exposure, and strict certification standards over long service periods, keeping airborne at the core of the military lighting market even when broader defense procurement moves unevenly from year to year.

Naval demand remains stable but less dynamic because shipboard and deck-light replacement cycles are longer and more tied to platform refit windows than to annual procurement spikes. Land is the fastest-growing platform segment, with a 8.75% CAGR through 2031, indicating where the next broad conversion wave is taking shape in the military lighting market. The demand for lighting in armored vehicles, tactical vehicles, and shelters is transitioning toward LED-based, NVG/IR-compatible, and low-maintenance solutions. Budget allocations prioritize tactical vehicle modernization, JLTV modifications, shelter integration, power distribution, command and control (C2) upgrades, and addressing obsolescence issues. Supplier data indicates widespread adoption of LED technology across military vehicles and shelters. Honeywell's selection of the MV-75 FLRAA LED Landing Search Light highlights the growing emphasis on LED-first design requirements in next-generation military aviation platforms and other rugged military applications.

LED accounted for 56.80% of revenue in 2025, making it the most established technology in the military lighting market. That position reflects its use across exterior assemblies, cockpit utility lights, vehicle systems, and military facilities, where long life, lower maintenance, and lower power draw now carry more weight in procurement decisions than before. The technology is also helped by the fact that DoD procurement rules increasingly favor efficient solid-state systems, while domestic content requirements narrow the approved supplier base for future contracts. Incandescent and halogen systems still retain some demand, where compatibility, thermal performance, or legacy design lock-in make substitution more difficult. Still, their footprint continues to shrink with each new platform cycle. In the military lighting market, LED therefore remains both the default choice for new procurement and the main retrofit path for older fleets.

OLED and micro-LED are the fastest-growing technologies, with a 8.95% CAGR through 2031, because advanced cockpit displays and HUD applications require higher brightness, deeper contrast control, and better power-to-performance than standard lighting modules provide. This growth sits closest to the cockpit boundary, where display systems increasingly overlap with lighting requirements in aircraft modernization work. The military lighting market is therefore expanding not only through lamps and luminaires but also through display-linked optical systems that enhance pilot visibility during day and night operations. Tritium and betalight solutions are relevant for military applications that require self-luminous functionality without batteries, wiring, or external power, such as weapon sights, compasses, gauges, markers, and safety devices. However, regulations like 10 CFR 32.22 and 10 CFR 32.53 impose licensing, safety, labeling, handling, and transfer requirements, limiting scalability compared to conventional electrical lighting. LED technology remains the primary choice for most military lighting applications, while OLED and micro-LED are emerging options for cockpit displays, HUDs, head-mounted systems, and soldier-vision interfaces.

Geography Analysis

North America accounted for 36.60% of revenue in 2025, making it the largest regional contributor to the military lighting market. The region benefits from the scale of US defense procurement, long aircraft upgrade pipelines, and a regulatory framework that favors LED adoption and compliance with domestic content requirements in future awards. Honeywell's selection in January 2026 for the MV-75 FLRAA LED Landing Search Light and Astronics' increasing military aircraft sales highlight the growing impact of next-generation US aviation programs on North America's role in high-value military aircraft lighting and safety systems. However, this serves as evidence of robust US program momentum rather than conclusive proof of North American dominance in the broader military lighting market.

Europe remains the second-largest region and an important source of demand for the certified military lighting market, as NATO-aligned aircraft and defense autonomy programs continue to support local supply positions. The UK, France, and Germany maintain national and multilateral platform programs that favor proven suppliers with NVIS and exterior-lighting certification histories. Oxley Group's extensive experience in NVIS aircraft upgrades for the UK and allied fleets highlights the importance of certification, expertise in legacy platforms, and sovereign support in maintaining the long-term involvement of domestic suppliers. Collins Aerospace's lighting installations on Eurofighter, A400M, Tornado, and Gripen platforms highlight its role in supporting multinational European aircraft fleets. This presence drives repeat demand across various operators and countries, rather than being limited to a single national fleet. This is particularly significant for platform sustainment, retrofitting, spare parts, and NVIS/LED upgrades, which are required throughout the extended service lives of these aircraft.

Asia-Pacific is projected to grow at an 8.05% CAGR through 2031, making it the fastest-growing regional block in the military lighting market. The main support comes from record defense budgets, active platform procurement, and rising alignment with night-vision and interoperability requirements in Japan, India, and other regional allied programs. Japan approved a FY2026 defense budget of JPY 9.04 trillion (USD 57.87 billion), including funding for carrier conversion work on JS Izumo and JS Kaga, covering deck lighting and associated landing support systems. India's FY2026-27 defense allocation reached INR 7.85 lakh crore (USD 90.20 billion), and that spending is expected to raise demand for cockpit, vehicle, and aircraft-class lighting systems across a broader modernization cycle. Procurement records from Japan's Air Self-Defense Force (JASDF) show repeated LED base-lighting purchases, with deliveries scheduled for early 2026. This highlights a regional shift toward LED lighting in both major defense budgets and routine acquisitions. Korea's adoption of SWIR-based friend-or-foe identification devices underscores interest in advanced low-visibility lighting. In the Middle East and Africa, while lighting markets are smaller, demand is driven by fleet modernization, defense facility upgrades, and local defense-industrialization efforts in countries like Saudi Arabia and the UAE. South America remains a narrower opportunity set, with aging-fleet upgrades supporting the need, even though procurement speed is limited by fiscal pressure in several markets.

- Astronics Corporation

- Honeywell International Inc.

- Collins Aerospace (RTX Corporation)

- Oxley Group

- Luminator Technology Group

- Blue Wolf, Inc.

- Safran SA

- Aveo Engineering Group, s.r.o.

- Betalight Tactical

- EELTEX Inc.

- Marine Electricals (I) Ltd.

- Whelen Engineering, Inc.

- Hoffman Engineering, LLC

- Venta Global Ltd.

- PHT Aerospace LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 LED retrofitting for lower power load and lower IR signature

- 4.2.2 Standard-mandated NVIS cockpit upgrades under MIL-STD-3009

- 4.2.3 Integration of adaptive multi-spectral luminaires for stealth

- 4.2.4 Modular plug-and-play light kits for expeditionary forces

- 4.2.5 Dual-mode (visible/IR) beacon demand for coalition IFF

- 4.2.6 DoD zero-maintenance preference accelerating solid-state adoption

- 4.3 Market Restraints

- 4.3.1 Stricter EM and EMC certification thresholds

- 4.3.2 Supply bottlenecks in high-reliability GaN LED die

- 4.3.3 Tritium regulations raising lifecycle cost

- 4.3.4 Budget diversion toward counter-UAS and autonomy programs

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Platform

- 5.1.1 Airborne

- 5.1.1.1 Fixed-wing

- 5.1.1.2 Rotary-wing

- 5.1.1.3 Unmanned Aerial Vehicle (UAVs)

- 5.1.2 Land

- 5.1.2.1 Tactical Vehicles

- 5.1.2.2 Main Battle Tanks

- 5.1.2.3 Mine Resistant Ambush Protected (MRAP)

- 5.1.2.4 Others

- 5.1.3 Naval

- 5.1.3.1 Surface Combatants

- 5.1.3.2 Sub-surface Vessels

- 5.1.3.3 Carrier Decks

- 5.1.1 Airborne

- 5.2 By Technology

- 5.2.1 LED

- 5.2.2 Incandescent/Halogen

- 5.2.3 OLED and Micro-LED

- 5.2.4 Tritium and Betalights

- 5.3 By Solution

- 5.3.1 Hardware

- 5.3.2 Software

- 5.3.3 Services

- 5.4 By Application

- 5.4.1 Interior

- 5.4.2 Exterior

- 5.5 By End-User

- 5.5.1 Army

- 5.5.2 Navy

- 5.5.3 Air Force

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 France

- 5.6.2.3 Germany

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Israel

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Astronics Corporation

- 6.4.2 Honeywell International Inc.

- 6.4.3 Collins Aerospace (RTX Corporation)

- 6.4.4 Oxley Group

- 6.4.5 Luminator Technology Group

- 6.4.6 Blue Wolf, Inc.

- 6.4.7 Safran SA

- 6.4.8 Aveo Engineering Group, s.r.o.

- 6.4.9 Betalight Tactical

- 6.4.10 EELTEX Inc.

- 6.4.11 Marine Electricals (I) Ltd.

- 6.4.12 Whelen Engineering, Inc.

- 6.4.13 Hoffman Engineering, LLC

- 6.4.14 Venta Global Ltd.

- 6.4.15 PHT Aerospace LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment