|

시장보고서

상품코드

2062341

이소프렌 고무 라텍스 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Isoprene Rubber Latex - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

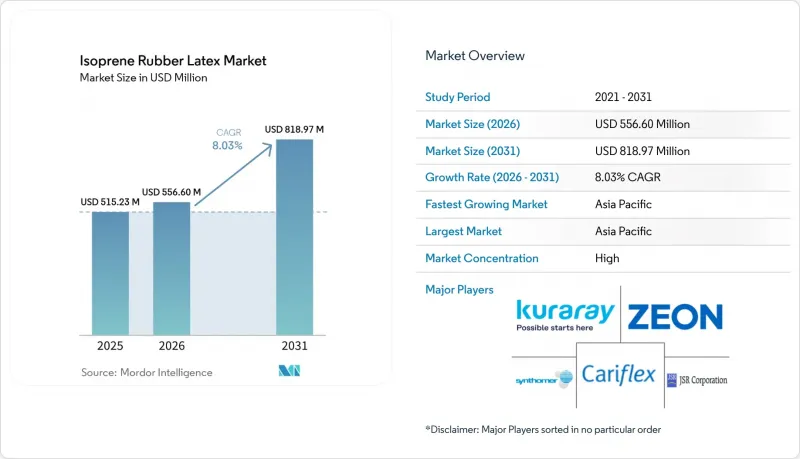

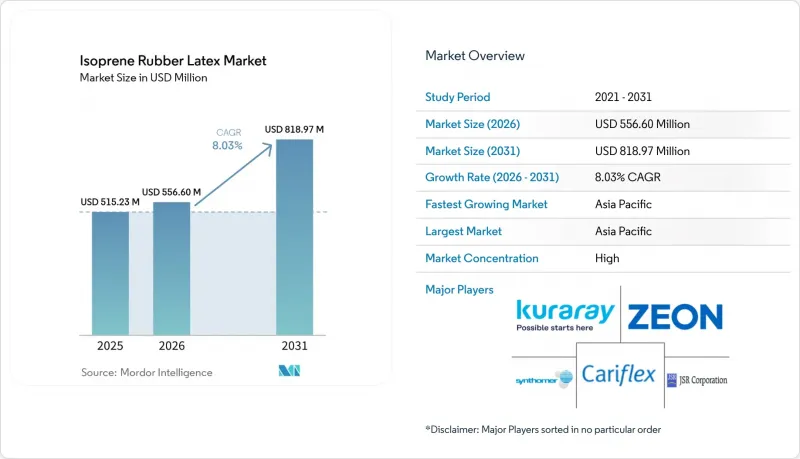

이소프렌 고무 라텍스 시장 규모는 2025년에 5억 1,523만 달러로 평가되었습니다. 2026년 5억 5,660만 달러에서 2031년까지 8억 1,897만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 8.03%를 나타낼 전망입니다.

본 보고서는 등급(의료용, 산업용, 식품용, 고암모니아), 형태(고고형분 및 저고형분/예비 가황), 용도(의료용 장갑, 카테터, 콘돔, 접착제, 섬유, 기타), 최종 사용자(헬스케어, 퍼스널케어, 산업, 소비재, 기타), 지역(아시아태평양, 유럽, 북미, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

세계의 이소프렌 고무 라텍스 시장 동향 및 분석

파우더 프리 의료용 장갑에 대한 수요 급증

2017년, 미국은 라텍스 알레르겐을 확산시키는 것으로 알려진 옥수수 전분을 운반체로 사용하는 제품을 특히 대상으로 하여, 파우더가 묻은 검사용 장갑의 사용을 금지했습니다. 이러한 규제 변경으로 인해 병원들은 저알레르기성 합성 대체품으로 전환할 수밖에 없게 되었습니다. 2026년부터 2031년까지의 예측 기간 동안, 말레이시아는 수술용 장갑의 주요 수출국으로 부상하며 이소프렌 라텍스 수요를 견인하고 있습니다. 중국의 제조업체인 Intco Medical은 생산 능력을 확대하고 인건비를 합리화함으로써 경쟁 구도를 더욱 격화시키고 있습니다. 1그램당 50마이크로그램 미만의 낮은 단백질 함량을 자랑하는 이소프렌 등급은 제1형 과민반응을 완화하는 능력이 높이 평가되어, 병원에서의 조달 시장에서 우위를 점하고 있습니다. 이러한 추세를 반영하여, 파우더 프리 장갑의 의무화 범위가 산업 분야와 외식 산업으로 확대되면서, 이소프렌 고무 라텍스 시장 잠재력이 더욱 높아지고 있습니다.

알레르기 우려에 따른 천연 고무 라텍스의 대체재

천연 라텍스 알레르기는 의료 종사자의 상당 부분에 영향을 미치고 있으며, 산업안전보건 당국은 이를 작업장의 위험 요인으로 분류하고 있습니다. 유럽 약전 3.2.9항에서는 의약품의 1차 포장에 천연 고무 라텍스의 사용이 금지됨에 따라, 합성 이소프렌으로 만든 캡에 대한 관심이 높아지고 있습니다. 과유르 고무나 바이오 이소프렌은 알레르기 사례가 적다고 보고되고 있지만, 여전히 대규모 검증 결과가 기다려지고 있습니다. 북미 및 유럽의 병원에서는 니트릴 또는 합성 이소프렌 장갑이 사용되고 있으며, 니트릴 장갑의 매출은 계속해서 증가하고 있습니다. 합성 등급은 시스-1,4-폴리이소프렌의 골격이 천연 고무와 동일하기 때문에 천연 고무와 같은 탄력성을 재현하고 있습니다. 또한, 작물 유래 단백질을 포함하지 않기 때문에 클래스 II/III 의료기기에 적합한 일관된 로트가 확보됩니다.

천연고무(NRL)의 높은 생산 비용

2026년부터 2031년까지의 예측 기간 동안, 합성 이소프렌 라텍스 가격은 천연 라텍스 가격을 상회할 것으로 전망됩니다. 이는 C4/C5 원유 스트림보다 폴리머 등급의 모노머가 더 높은 가격에 거래되고 있기 때문입니다. 천연 고무 가격은 안정적인 반면, 이소프렌 단량체 시장은 꾸준히 성장하고 있습니다. 가정용 장갑이나 산업용 디핑 제품 등 가격에 민감한 분야에서는 여전히 천연 라텍스에 의존하고 있습니다. 반면, 의료용 및 식품용 등급 분야에서는 저알레르기성이라는 특징을 살려 고가 대에서 거래가 이루어지고 있습니다.

부문별 분석

2025년에는 장갑용 FDA 21 CFR 880 규격 및 밀폐부용 USP 381 규격을 준수하는 의료용 라텍스가 매출의 41.94%를 차지했습니다. FDA 21 CFR 177.2600을 준수하는 배합을 목표로 하는 콘돔 제조업체들의 주도 하에, 식품 등급 이소프렌 고무 라텍스 시장은 2026년부터 2031년까지 연평균 성장률(CAGR) 8.52%를 나타낼 전망입니다. 산업용 라텍스는 접착제나 실런트에 사용되며, 액상 폴리이소프렌 등급은 점착제 역할을 합니다. 보존 기간 연장으로 잘 알려진 고암모니아 등급은 EU의 VOC 규제에 대한 적합성 심사를 받고 있으나, 업계에서는 저암모니아 안정제로의 전환이 두드러지게 나타나고 있습니다. 단백질 농도가 50µg/g 미만인 초저단백질 라텍스는 클래스 III 수술용 장갑 및 특수 의료기기용으로 설계되었습니다.

의료용 라텍스의 가격은 ISO 13485에 기반한 추적 가능성과 천연 라텍스 알레르겐에 대한 병원 규제의 강화에 힘입어 계속해서 견조한 추세를 보이고 있습니다. 식품용 라텍스는 젖꼭지, 젖병 젖꼭지, 저알레르기성 콘돔 등에 널리 사용되고 있으며, 이것이 꾸준한 수요 증가를 이끌고 있습니다. 산업용 부문도 성장세를 보이고 있는데, 특히 전기차 제조업체들이 경량화를 위해 기존의 기계식 패스너에서 엘라스토머 접착 방식으로 전환하고 있는 것이 그 요인입니다.

2025년에는 고형분 함량이 50%를 초과하는 고형분 라텍스가 매출의 63.91%를 차지했습니다. 이처럼 높은 고형분 함량은 운송 비용 절감뿐만 아니라 기계적 안정성 향상에도 기여했습니다. 한편, 이소프렌 고무 분야의 저고형분 예비 가황 라텍스 시장 점유율은 2026년부터 2031년에 걸쳐 연평균 성장률(CAGR) 8.63%로 확대되고 있습니다. 이러한 성장은 방사선·과산화물 가황법을 통해 이루어졌으며, 수술용 장갑의 기준이 되는 ASTM D3577 규격을 상회하는 인장 강도를 달성한 것이 그 요인입니다. 또한, 상온 예비 가황 기술의 발전으로 인해 얇은 두께의 카테터 필름 제조가 가능해졌으며, 이로 인해 후경화 오븐이 더 이상 필요하지 않게 되었습니다.

고고형분 제품이 여전히 주류를 이루고 있지만, 무황 프리가황 등급에 대한 수요가 증가하고 있습니다. 그 매력은 니트로소아민 위험 감소와 생산 주기 단축에 있습니다. 아시아태평양(말레이시아 및 태국)의 장갑 생산 거점도 발전하고 있습니다. 이러한 거점에서는 방사선 가교와 과산화물 가황을 결합한 하이브리드 제조 모델의 도입이 시작되고 있습니다. 물류 측면에서 공급망 참여 기업 중 특히 2-8℃라는 엄격한 콜드체인 조건 하에서 안정화된 저고형분 라텍스를 운송할 수 있는 능력을 갖춘 기업들은 2026년부터 2031년까지의 예측 기간 동안 전문 의료용 주문을 확보하는 데 있어 전략적 우위를 점하고 있습니다.

지역별 분석

2025년 매출의 53.37%를 차지한 아시아태평양은 2026년부터 2031년까지의 예측 기간 동안 연평균 성장률(CAGR) 8.99%를 기록하며 그 우위를 더욱 공고히할 것으로 전망됩니다. 말레이시아는 수술용 장갑 수출에서 중요한 역할을 해왔습니다. 중국은 장갑 수출에 더해 합성고무의 생산 능력을 확대되고 있습니다. 태국과 베트남은 중국산 장갑에 영향을 미치는 관세 변경에 대응하여 생산을 확대되고 있습니다. 2026년 2월, ARLANXEO는 창저우에 HNBR 생산 설비를 가동했으며, 제온의 요네자와 공장은 2034년까지 바이오이소프렌의 상용화를 목표로 하고 있습니다. 또한, 인도와 인도네시아에서 중산층의 부상이 의료비 증가를 주도하고 있어, 해당 지역의 성장 잠재력을 부각시키고 있습니다.

북미와 유럽은 2025년 매출에서 상당한 점유율을 차지했습니다. 2026년에 도입된 FDA의 QMSR(품질 관리 시스템 규정)에 더해, 주 차원의 프탈레이트 사용 금지 조치가 카테터 및 스토퍼의 혁신을 촉진하고 있으며, 이는 합성 이소프렌의 채택 확대로 이어지고 있습니다. 동시에, 유럽 내 스팀 크래커의 가동 중단으로 인해 현지 원료 공급이 제한되고 있어, 해당 지역은 수입에 의존할 수밖에 없게 되었고, 이로 인해 라텍스 가격이 급등하고 있습니다. 북미에서는 특히 mRNA 제제의 충전 및 마무리 라인 확장에 따라 백신용 스토퍼에 대한 수요가 계속해서 견조한 양상을 보이고 있습니다.

남미, 중동 및 아프리카 등 3개 지역을 합쳐도 2025년 매출에서 차지하는 비중은 미미했습니다. 2℃에서 8℃ 사이의 온도에서 보관해야 하는 가황 전 라텍스의 유통은 콜드체인의 미비로 인해 어려움을 겪고 있습니다. ARLANXEO는 라틴아메리카 내 현지 공급을 강화하기 위해 2027년까지 트리운포 공장의 확장을 완료하는 것을 목표로 하고 있습니다. 한편, 중동은 풍부한 석유화학 원료를 보유하고 있는 반면, 하류 부문인 라텍스 생산 능력은 제한적이기 때문에 장갑 및 카테터 분야의 투자자들에게 매력적인 합작 투자 기회가 생겨나고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the isoprene rubber latex market size was valued at USD 515.23 million in 2025 and is estimated to grow from USD 556.60 million in 2026 to reach USD 818.97 million by 2031, at a CAGR of 8.03% during the forecast period (2026-2031).

This report is Segmented by Grade (Medical, Industrial, Food, and High-Ammonia), Form (High-Solids and Low-Solids/Prevulcanized), Application (Medical Gloves, Catheters, Condoms, Adhesives, Textiles, and Others), End-User (Healthcare, Personal Care, Industrial, Consumer Goods, and Others), and Geography (Asia-Pacific, Europe, North America, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Isoprene Rubber Latex Market Trends and Insights

Surging Demand for Powder-Free Medical Gloves

In 2017, the U.S. imposed a ban on powdered examination gloves, specifically targeting cornstarch carriers known to disseminate latex allergens. This regulatory shift prompted hospitals to pivot towards hypoallergenic synthetic alternatives. By the forecast period 2026-2031, Malaysia has emerged as a key exporter of surgical gloves, bolstering the demand for isoprene latex. Chinese manufacturer Intco Medical has increased its production capacity and streamlined labor costs, heightening the competitive landscape. Low-protein isoprene grades, containing less than 50 micrograms per gram, are now favored for their ability to reduce type I hypersensitivity, securing a premium position in hospital purchases. Reflecting this trend, mandates for powder-free gloves have expanded to encompass industrial and food-service sectors, amplifying the market potential for isoprene rubber latex.

Substitution of Natural Rubber Latex Amid Allergy Concerns

Natural-latex allergies affect a significant portion of healthcare workers, prompting occupational safety organizations to classify them as a workplace hazard. The European Pharmacopeia 3.2.9 has banned natural rubber latex in pharmaceutical primary packaging, shifting the focus to synthetic isoprene closures. Although guayule rubber and bio-based isoprene report fewer allergy incidents, they still await large-scale validation. Hospitals across North America and Europe have adopted nitrile or synthetic isoprene gloves, with nitrile glove revenues continuing to grow. Due to their identical cis-1,4 polyisoprene backbones, synthetic grades replicate the elasticity of natural rubber. Furthermore, being free from crop-derived proteins, they ensure consistent batches suitable for Class II/III devices.

High Production Cost Versus NRL

By the forecast period 2026-2031, synthetic isoprene latex prices outpace those of natural latex, fueled by the premium trading of polymer-grade monomers over crude C4/C5 streams. While natural rubber prices remain stable, the isoprene monomer market continues to grow steadily. Price-sensitive sectors, including household gloves and industrial dipped goods, still rely on natural latex. In contrast, medical and food-grade segments, benefiting from their hypoallergenic compliance, command premium prices.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Minimally Invasive Catheter and Balloon Procedures

- DEHP-Free Device Regulation Favors IRL Catheter Balloons

- Volatile Isoprene-Monomer Feedstock Pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, medical-grade latex, adhering to FDA 21 CFR 880 standards for gloves and USP 381 standards for closures, commanded 41.94% of the revenue. The market for food-grade isoprene rubber latex, driven by condom manufacturers targeting FDA 21 CFR 177.2600 compliant formulations, is set to expand at a CAGR of 8.52% from 2026 to 2031. Industrial-grade latex finds its application in adhesives and sealants, with liquid polyisoprene grades acting as tackifiers. While high-ammonia grades, known for enhancing shelf life, face scrutiny for EU VOC compliance, there is a noticeable industry shift towards low-ammonia stabilizers. Ultra-low-protein latex, with concentrations below 50 µg/g, is tailored for Class III surgical gloves and specialized medical devices.

Pricing for medical-grade latex remains strong, supported by ISO 13485 traceability and tightening hospital regulations on natural-latex allergens. Food-grade latex is commonly used in pacifiers, baby-bottle nipples, and hypoallergenic condoms, which drives a consistent volume increase. The industrial-grade segment is witnessing growth, especially as electric-vehicle manufacturers lean towards elastomeric bonding, moving away from traditional mechanical fasteners for weight reduction.

In 2025, high-solids latex, boasting over 50% solids content, commanded 63.91% of the revenue. This high-solids content not only reduced freight costs but also enhanced mechanical stability. Meanwhile, the market share of low-solids prevulcanized latex in the isoprene rubber sector is growing at 8.63% CAGR, from 2026 to 2031. This growth is attributed to radiation-peroxide vulcanization, which has achieved tensile strengths exceeding the ASTM D3577 standard, a benchmark for surgical gloves. Additionally, advancements in room-temperature pre-vulcanization have enabled the production of thin-wall catheter films, eliminating the need for post-cure ovens.

Although high-solids variants continue to dominate, sulfur-free prevulcanized grades are gaining traction. Their appeal lies in a reduced nitrosamine risk and faster production cycles. Glove manufacturing hubs in the Asia-Pacific (Malaysia and Thailand) region are also evolving. They have started integrating hybrid manufacturing models, combining radiation crosslinking with peroxide curing. On the logistics front, players in the supply chain, particularly those proficient in shipping stabilized low-solids latex under stringent cold-chain conditions of 2 to 8 °C, are strategically positioned to capture specialized medical orders during the forecast period of 2026-2031.

Geography Analysis

Asia-Pacific, which accounted for 53.37% of the revenue in 2025, is set to reinforce its lead with a projected 8.99% CAGR during the forecast period of 2026-2031. Malaysia has played a significant role in exporting surgical gloves. China, in addition to exporting gloves, is expanding its synthetic-rubber capacity. Both Thailand and Vietnam are increasing production in response to tariff changes affecting Chinese gloves. In February 2026, ARLANXEO launched an HNBR unit in Changzhou, while Zeon's Yonezawa facility is targeting bio-isoprene commercialization by 2034. Additionally, a rising middle class in India and Indonesia is driving increased healthcare spending, highlighting the region's growth potential.

North America and Europe are set to capture a substantial share of 2025's sales. The FDA's QMSR, introduced in 2026, along with state-level bans on phthalates, is driving reforms in catheters and stoppers, leading to increased adoption of synthetic isoprene. At the same time, European steam-cracker shutdowns are limiting local feedstock availability, pushing the region towards imports and driving up latex prices. In North America, the demand for vaccine stoppers remains strong, particularly with the expansion of mRNA fill-finish lines.

South America, the Middle-East, and Africa together make up a smaller portion of the 2025 revenue. The distribution of pre-vulcanized latex, which requires storage between 2°C and 8°C, faces challenges due to cold-chain deficiencies. ARLANXEO aims to complete its Triunfo expansion by 2027 to bolster local supply in Latin America. Meanwhile, the Middle-East's abundant petrochemical feedstock contrasts with its limited downstream latex production capacity, presenting attractive joint-venture opportunities for investors in gloves and catheters.

- ARLANXEO

- Cariflex

- Daelim Co., Ltd.

- Eni S.p.A

- Exxon Mobil Corporation

- Fushun Yikesi New Materials Co., Ltd.

- JSR Corporation

- Kent Elastomers Products, Inc.

- Kraton Corporation

- Kumho Petrochemical

- Kuraray Co., Ltd.

- LG Chem

- Lion Elastomers

- PetroChina Yanshan Petrochemical

- PJSC SIBUR Holding

- Shandong Yuhuang Chemical Co., Ltd.

- Sumitomo Rubber Industries

- Synthomer plc

- Top Glove Corporation Bhd

- Zeon Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for powder-free medical gloves

- 4.2.2 Substitution of natural rubber latex (NRL) amid allergy concerns

- 4.2.3 Growth in minimally-invasive catheter and balloon procedures

- 4.2.4 DEHP-free device regulation favouring IRL catheter balloons

- 4.2.5 Ultra-clean IRL required for mRNA-vaccine vial stoppers

- 4.2.6 Microfluidic-chip elastomer layers needing ultra-pure IRL

- 4.3 Market Restraints

- 4.3.1 High production cost versus NRL

- 4.3.2 Volatile isoprene-monomer feedstock pricing

- 4.3.3 Steam-cracker outages limiting polymer-grade isoprene

- 4.3.4 Cold-chain logistics limitations in emerging markets

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Grade

- 5.1.1 Medical Grade

- 5.1.2 Industrial Grade

- 5.1.3 Food Grade

- 5.1.4 High-Ammonia IRL

- 5.2 By Form

- 5.2.1 Personal Care and Hygiene

- 5.2.2 Low-Solids/Prevulcanized Latex

- 5.3 By Application

- 5.3.1 Medical Gloves

- 5.3.2 Catheters and Balloon Devices

- 5.3.3 Condoms

- 5.3.4 Adhesives and Sealants

- 5.3.5 Elastic Threads and Textiles

- 5.3.6 Other Applications (Coatings, Baby Products)

- 5.4 By End-user Industry

- 5.4.1 Healthcare and Medical

- 5.4.2 Personal Care and Hygiene

- 5.4.3 Industrial Manufacturing

- 5.4.4 Consumer Goods

- 5.4.5 Other Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 North America

- 5.5.3.1 United States

- 5.5.3.2 Canada

- 5.5.3.3 Mexico

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 South Africa

- 5.5.5.5 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 ARLANXEO

- 6.4.2 Cariflex

- 6.4.3 Daelim Co., Ltd.

- 6.4.4 Eni S.p.A

- 6.4.5 Exxon Mobil Corporation

- 6.4.6 Fushun Yikesi New Materials Co., Ltd.

- 6.4.7 JSR Corporation

- 6.4.8 Kent Elastomers Products, Inc.

- 6.4.9 Kraton Corporation

- 6.4.10 Kumho Petrochemical

- 6.4.11 Kuraray Co., Ltd.

- 6.4.12 LG Chem

- 6.4.13 Lion Elastomers

- 6.4.14 PetroChina Yanshan Petrochemical

- 6.4.15 PJSC SIBUR Holding

- 6.4.16 Shandong Yuhuang Chemical Co., Ltd.

- 6.4.17 Sumitomo Rubber Industries

- 6.4.18 Synthomer plc

- 6.4.19 Top Glove Corporation Bhd

- 6.4.20 Zeon Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Bio-based Isoprene Latex