|

시장보고서

상품코드

2062361

군용 웨어러블 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Military Wearables - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

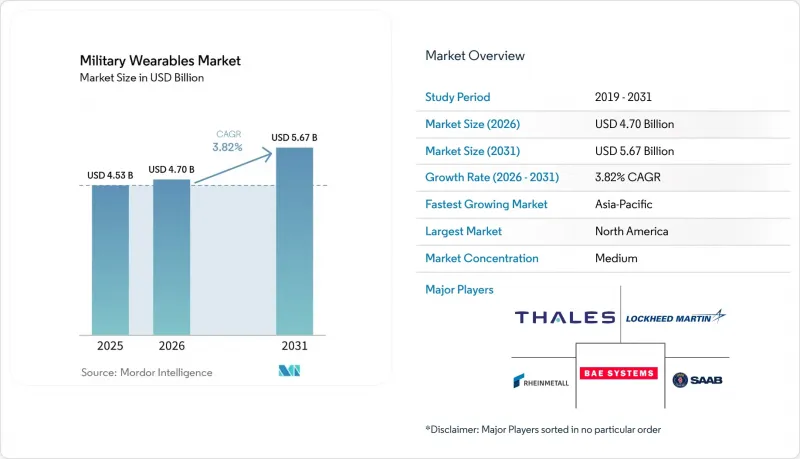

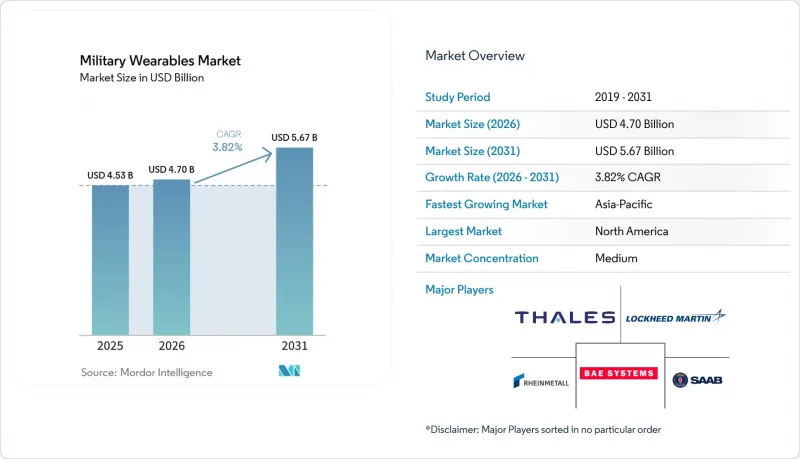

Mordor Intelligence에 의하면, 군용 웨어러블 시장 규모는 2025년 45억 3,000만 달러로 평가되었고, 2026년 47억 달러로 추정되고, 2031년까지 56억 7,000만 달러로 확대될 전망이며, 2026-2031년 연평균 복합 성장률(CAGR)은 3.82%를 나타낼 것으로 예측됩니다.

본 보고서는 웨어러블 유형별(헤드웨어, 아이웨어, 리스트웨어, 바디웨어, 히어러블, 엑소스켈레톤), 용도별(통신 및 컴퓨팅, 시각 및 감시, 기타), 최종 사용자별(육군, 공군, 해군), 핵심 기술별(스마트 텍스타일, 기타), 지역별(북미, 유럽, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 군용 웨어러블 시장 동향 및 인사이트

차세대 병사 현대화 프로그램에 대한 전 세계적 투자 증가

국방 현대화를 위한 지출은 군용 웨어러블 시장에 있어 가장 확실한 수요의 주축이 되고 있습니다. 이는 몇몇 대규모 군인 대상 프로그램이 구상 단계에서 실용 단계로 넘어가고 있기 때문입니다. 독일에서는 2025년 2월, 라인메탈사가 IdZ-ES 병사 시스템과 관련하여 31억 유로(32억 1,000만 달러) 규모의 기본 계약을 수주함으로써, 2030년까지 최대 368개의 소대급 장비 세트를 공급하게 되어 그 속도를 더욱 가속화했습니다. 이 프로그램은 2026년 4월, 추가로 8,600명의 병사를 대상으로 10억 유로(12억 1,000만 달러) 규모의 추가 발주를 받아, 네트워크 기반 방호 장비, 야간 투시 장비, 전술 컴퓨팅에 대한 단기 수요 전망이 더욱 명확해졌습니다. 캐나다는 2025년 5월, 국방부가 Logistik Unicorp사와 1,970만 캐나다 달러(1,419만 달러) 규모의 계약을 체결하고, 경부대 현대화의 일환으로 3,000명의 병사를 위한 현대화된 장비를 납품함으로써, 더욱 명확한 조달 신호를 보냈습니다. 이러한 수주 건들은 매출액이라는 측면을 넘어 중요한 의미를 지닙니다. 왜냐하면, 군용 시스템에 대한 각 발주는 군용 웨어러블 시장 전체에서 보호 캐리어, 임베디드 전자기기, 섬유, 전원 모듈 및 견고한 인터페이스에 대한 수요를 견인하기 때문입니다. 그 결과, 대규모 국가 계약을 통해 주요 도급업체가 중심적인 지위를 유지하는 조달 환경이 조성되고 있습니다. 그럼에도 불구하고, 이러한 계약들은 군사 규격을 충족할 수 있는 서브시스템 공급업체들에게 더 큰 하류 사업 기회를 창출하고 있습니다.

실시간 생체 인증 및 건강 모니터링에 대한 운영상 수요 증가

실시간 생리학적 모니터링은 단순한 시범적 개념에 그치지 않고, 군용 웨어러블 시장에서 실용적인 기능으로 자리 잡고 있습니다. 미 육군은 ‘웨어러블 올해저드 원격 모니터링 프로그램(Wearable All-Hazard Remote Monitoring Program)’이 2025년 말에 선정된 특수작전부대에 배치될 예정이며, 2026 회계연도에는 더 광범위한 통합 부대에 배치될 예정이라고 발표했습니다. 이러한 변화는 웨어러블 시스템이 동일한 하드웨어 환경 내에서 훈련, 안전, 위험 인식 및 임무 수행 태세 지원을 수행할 것으로 기대되고 있음을 보여주며, 중요한 의미를 지닙니다. RTI 인터내셔널의 ‘AlphaWear’ 프로그램은 열 스트레스 및 감염증 위험 모니터링 기능을 국방 분야에 특화된 정밀 헬스케어 플랫폼에 통합하고 있습니다. 2025년 10월에 시작된 AlphaWear는 미군 요원을 위한 웨어러블 데이터 플랫폼으로, 피트니스 기기를 활용해 열 스트레스, 감염병 위험 및 정신 건강을 실시간으로 추적할 수 있게 해줍니다. 이 기술은 군사적 즉각 대응 능력과 작전 효율성 향상 측면에서 웨어러블 기기가 수행하는 역할이 확대되고 있음을 여실히 보여주고 있습니다. 이 기능의 확대에 따라, 군용 웨어러블 시장은 민간용 형식과 점점 더 멀어지고 있습니다. 군용 설계에서는 편의성을 중시한 일상적인 사용이 아니라, 방탄 보호, 통신 장비, 가혹한 전장 환경에 대한 대응이 요구되기 때문입니다. 이로 인해 센서 성능과 마찬가지로 방위 분야 특유의 통합이 중요시되는 보호된 틈새 시장이 강화되고 있습니다. 또한, 병사 한 명당 하드웨어 부담을 늘리지 않으면서 생체 인증 데이터를 유용한 경보로 변환할 수 있는 소프트웨어 계층의 가치도 높아지고 있습니다.

동맹군 전체에 걸친 표준화된 상호운용성 프레임워크의 부재

상호운용성은 여전히 군용 웨어러블 시장에 있어 구조적인 걸림돌로 작용하고 있습니다. 왜냐하면 연합군 작전은 여전히 단일한 공유 하드웨어 및 데이터 표준에 기반하여 운영되지 않고 있기 때문입니다. 미 육군의 ‘미션 파트너 키트’는 상황 인식 공유, 보안 채팅, 음성 통신 및 협업 도구를 제공함으로써 ‘세이버 스트라이크 24’와 ‘세이버 정션 24’ 등의 훈련에서 다국적 지휘통제 연결성을 강화했습니다. 그러나 특히 호환성이 없는 통신 네트워크, 데이터 공유 프로토콜, 기밀 분류 규정, 그리고 연합군 부대 전체에 걸친 표준화된 소프트웨어 기반 프레임워크의 도입과 관련하여, 더 광범위한 연합군 간의 상호 운용성을 실현하기 위해서는 여전히 큰 과제가 남아 있습니다. 유럽에서는 2027년까지 여러 회원국에 걸쳐 차세대 보병 시스템을 통합하는 것을 목표로 하는 ‘ACHILE’ 이니셔티브와 같은 체계적인 프로그램을 통해 이러한 격차를 해소하기 위해 노력하고 있습니다. 이와 유사한 움직임은 더 광범위한 유럽의 방위 기반에서도 관찰되며, ARMETISS 프로그램에서는 다국적 컨소시엄을 통해 공통 스마트웨어 모듈을 개발하고 있습니다. 이러한 노력들이 조달 단계에서의 인터페이스 통합으로 이어지기 전까지는 각국의 웨어러블 스택이 공동 전개 시 상호 연동할 때, 각국 군은 계속해서 높은 통합 비용에 직면하게 될 것입니다. 이로 인해 전환 비용이 증가하면서, 소규모 전문 업체보다 기존의 국경 간 공급업체가 우대받는 경향이 나타나고 있으며, 그 결과 동맹 전체에서 군용 웨어러블 시장의 확대 속도가 둔화되고 있습니다.

부문별 분석

2025년에는 바디웨어가 41.55%로 가장 큰 점유율을 차지한 것으로 평가되었으며, 이 분야는 여전히 군용 웨어러블 시장의 주요 수요원으로 자리 잡고 있습니다. 이러한 위상은 바디웨어가 이미 보호 및 하중 운반의 핵심 역할을 담당하고 있다는 사실을 반영하며, 기존 조달 채널을 통해 전자 기기를 통합하는 데 있어 진입 장벽이 가장 낮은 분야로 자리매김하고 있습니다. 헬멧이 모듈식 디지털 아키텍처로 진화함에 따라, 헤드웨어의 중요성은 점점 더 커지고 있습니다. Anduril사의 EagleEye 프로그램은 방탄 보호 기능, AI 기반 비전 시스템, 그리고 명령 인터페이스를 통합한 플랫폼으로서 이러한 추세를 잘 보여주고 있습니다. 아이웨어는 야간 시야 기능 및 디스플레이 업그레이드를 통해 계속해서 활용되고 있는 반면, 리스트웨어와 히어러블은 국소적인 제어, 팀 상황 인식, 그리고 보안 통신 분야에서 규모는 작지만 유용한 역할을 계속 수행하고 있습니다. 따라서 군용 웨어러블 시장은 엑소스켈레톤이 해당 부문의 최첨단에서 가장 강력한 성장 동력을 이끌고 있음에도 불구하고, 시장 규모 확대 측면에서는 여전히 안정적인 바디본형 제품의 조달에 의존하고 있습니다.

외골격 시장은 2031년까지 연평균 성장률(CAGR) 6.65%를 나타낼 것으로 예측되며, 웨어러블 유형별 세분화에서 군용 웨어러블 시장이 가장 빠르게 성장하는 부문이 될 것입니다. 이러한 추세는 실증 프로그램에서 실전적 유용성으로의 명확한 전환을 반영하고 있으며, 특히 부대 규모의 확대보다는 지구력, 하중 운반 능력, 반복적인 부하가 중요한 임무에서 두드러지게 나타납니다. 단기적으로 가장 유력한 징후는 2026년 3월 우크라이나에서 나타났습니다. 해당국 군은 전투 환경에서의 부담을 줄이고 포병의 장전 작업 효율을 높이기 위해 전선에서 외골격 사용을 시작했습니다. 군용 웨어러블 업계에서는 이러한 유형의 실전 사용 실적이 실험실에서의 성능 데이터보다 더 중요하게 여겨집니다. 왜냐하면 조달 기관은 웨어러블 지원 시스템이 실전에서의 스트레스, 정비에 대한 압박, 불확실한 전원 환경 속에서도 제대로 작동한다는 증거를 요구하고 있기 때문입니다.

용도별로는 통신 및 컴퓨팅 분야가 주도적이며, 2025년 군용 웨어러블 시장 전체의 37.20%를 차지했으며, 네트워크 기반 작전이 여전히 현재 수요의 중심임을 보여주고 있습니다. 이 범주는 개별 병사를 더 광범위한 부대와 연결해 주는 무전기, 전술 디스플레이, 전투 관리 인터페이스에 의해 뒷받침되고 있습니다. 시각·감시 분야는 야간 투시 장치나 확장 디스플레이 프로그램을 통해 계속해서 자금을 조달하고 있지만, 부대가 더욱 열악한 환경이나 통신 두절 상황에 대비함에 따라 내비게이션 및 위치 파악 분야의 중요성이 커지고 있습니다. 방호 및 생존성은 장기간에 걸친 조달 주기와 밀접하게 연관되어 있어, 여전히 가장 안정적인 수요 기반을 제공합니다. 또한, WARP와 같은 시스템이 훈련의 안전성이나 부대의 즉각 대응 태세 측면에서 실용적인 가치를 입증함에 따라, 건강 및 스트레스 모니터링도 그 중요성이 커지고 있습니다. 따라서 군용 웨어러블 시장은 활용 범위를 넓혀가고 있습니다. 그러나 가장 큰 지출은 여전히 통신 분야에 집중되어 있으며, 가장 급격한 변화는 병사들의 전체 장비에 대한 전력 관리 방식에서 일어나고 있습니다.

전력 및 에너지 관리 시장은 2031년까지 연평균 성장률(CAGR) 5.80%를 나타낼 것으로 전망되며, 군용 웨어러블 시장에서 가장 빠르게 성장하는 용도 분야로 부상하고 있습니다. 이러한 증가는 근본적인 운영상의 요인에 기인합니다. 즉, 디스플레이, 센서, 무선 기기 또는 연산 모듈이 하나씩 추가될 때마다 병사의 전력 수요가 증가하기 때문입니다. 이 부문의 중요성이 커지고 있는 이유는 현대의 군인용 장비가 더 이상 독립된 장치로서 최적화될 수 없기 때문입니다. 대신, 공유된 전력 제어 로직, 더 높은 배터리 밀도, 그리고 장기 임무 중 전반적인 에너지 손실의 저감이 요구됩니다. 군용 웨어러블 업계에서 에너지 관리는 보조 기능에서 시스템 설계의 핵심으로 자리매김하고 있습니다. 이는 가동 시간이 임무 시간, 기동성, 장비의 무게에 직접적인 영향을 미치기 때문입니다.

지역별 분석

2025년 기준 북미는 시장의 47.65%를 차지했으며, 이 지역은 군용 웨어러블 시장 및 전 세계 방위용 웨어러블 조달에서 가장 큰 점유율을 기록했습니다. 이러한 우위는 미국의 방위 예산 규모, 주요 시스템 통합사업자의 존재, 그리고 기존 주요 기업과 신생 기술 기업 모두를 수용할 수 있는 조달 기반에서 비롯됩니다.

유럽에서는 프로그램 활동이 조화를 이루고 있으며, 이는 각국의 조달 및 공동 산업 이니셔티브 양측 모두에서 군용 웨어러블 시장을 견인하고 있습니다. 2025년 IVAS 프로그램의 전환, 즉 Anduril사와 Microsoft사가 향후 개발 및 클라우드 지원을 위해 제휴를 확대한 것은 성능에 대한 기대가 충족되지 않을 경우 해당 지역이 얼마나 신속하게 프로그램의 주도권을 재편할 수 있는지를 보여주었습니다. 영국은 2026년 2월, 국방부가 BlackTree Technologies사에 ‘Dismounted Data System’ 계약(최대 8,600만 파운드=1억 1,699만 달러 상당)을 수주함으로써 이 지역의 입지를 더욱 공고히 했습니다. 이 AI 지원 시스템에는 무전기, 헤드셋, 디스플레이 태블릿, 케이블, 배터리, 파우치, 안테나가 포함되어 있으며, 2026년 9월부터 영국 육군에 단계적으로 납품될 예정이며, 2027년까지 전면적인 도입이 완료될 전망입니다. 2026년 4월, 독일 IdZ-ES의 수시 발주에 따라 2025년 2월의 기본 계약에 근거한 주요 물량이 발주되었습니다. 이는 라인메탈사와 BAAINBw에게 있어 병사용 시스템 조달 분야에서 가장 큰 규모의 기본 계약이 될 것입니다. 10억 4,000만 유로(12억 1,000만 달러) 규모의 이번 수주에는 기존 시스템의 현대화, 소대용 시스템 237세트 추가 조달, 그리고 IT 장비, 광학 장비, 광전자 장비, 군복, 방호 장비, 관련 서비스를 담당하는 하청업체에 대한 지원이 포함되어 있습니다. 지역적 역량 구축은 공동 개발 프로젝트, 특히 스마트웨어 기술과 관련하여 7개국과 20개 파트너를 연결하는 ‘ARMETISS’에서도 두드러지게 나타납니다. 이는 유럽이 장비 구매를 확대하고 있을 뿐만 아니라, 향후 교체 주기를 대비해 통일된 아키텍처를 확립하고 지역 산업 역량을 강화하기 위해 노력하고 있다는 점에서 중요합니다. 반면, 중동 및 아프리카는 전체 시장에서 차지하는 비중이 작습니다. 그러나 첨단 광학 기기, 헤드마운트형 시스템 및 현장용 방호 장비 제조에 대한 관심이 높아짐에 따라, 지역 파트너십을 맺고 있는 공급업체들에게는 선택적인 성장 기회가 생기고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 6.45%를 기록하며 성장할 것으로 예상되며, 군용 웨어러블 분야에서 가장 빠르게 성장하는 지역 시장이 될 전망입니다. 이러한 성장 속도는 국방 예산 증가, 국산화율에 관한 규제 강화, 그리고 안보상의 과제를 안고 있는 환경 속에서 대규모 지상군의 현대화 필요성을 반영하고 있습니다. 인도의 F-INSAS 구상, 한국의 ‘워리어 플랫폼’ 사업, 그리고 중국의 외골격 및 디지털 병사 도구 분야에 대한 지속적인 투자는 해당 지역이 단일 도입 모델에 의존하고 있는 것이 아니라 서로 다른 산업 전략을 가진 여러 국가적 경로를 걷고 있음을 보여줍니다. 또한 호주는 웨어러블 기기 도입에 있어 장시간 작동이라는 목표를 뒷받침하는 배터리 개발을 통해 이러한 추세에 더욱 큰 의미를 더하고 있습니다. 더 큰 전략적 영향으로는 아시아·태평양 지역의 성장이 해당 지역공급 능력과 수요를 형성하고 있다는 점을 들 수 있습니다. 이는 각국의 프로그램의 회복탄력성을 향상시킬 가능성이 있지만, 한편으로는 더 광범위한 군용 웨어러블 시장 전체에서 상호운용성의 격차를 더욱 심화시킬 가능성도 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the military wearables market size is projected to expand from USD 4.53 billion in 2025 and USD 4.70 billion in 2026 to USD 5.67 billion by 2031, registering a CAGR of 3.82% between 2026 and 2031.

This report is Segmented by Wearable Type (Headwear, Eyewear, Wristwear, Bodywear, Hearables, and Exoskeletons), Application (Communication and Computing, Vision and Surveillance, and More), End-User (Land Forces, Airborne Forces, and Naval Forces), Core Technology (Smart Textiles, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Military Wearables Market Trends and Insights

Increased Global Investment in Next-Generation Soldier Modernization Programs

Defense modernization spending is the clearest demand anchor for the military wearables market because several large soldier programs are now in delivery rather than concept stages. Germany moved the pace higher when Rheinmetall secured a EUR 3.1 billion (USD 3.21 billion) framework for IdZ-ES soldier systems in February 2025, covering up to 368 platoon-level equipment sets through 2030. That program received another boost in April 2026 with a EUR 1.0 billion (USD 1.21 billion) call-off order for 8,600 additional soldiers, which extended near-term visibility into demand for networked armor, night vision, and tactical computing. Canada added another clear procurement signal in May 2025 when its Department of National Defense contracted Logistik Unicorp for CAD 19.70 million (USD 14.19 million) to deliver modernized equipment for 3,000 soldiers as part of its light forces upgrade effort. These awards matter beyond the top line because each soldier system order pulls through demand for protective carriers, embedded electronics, textiles, power modules, and rugged interfaces across the military wearables market. The result is a procurement environment where large national contracts keep prime contractors central. Still, they also create a larger downstream opportunity set for subsystem vendors that can meet military qualification standards.

Growing Operational Need for Real-Time Biometric and Health Monitoring

Real-time physiological monitoring is becoming a practical capability in the military wearables market rather than a limited pilot concept. The US Army announced that the Wearable All-Hazard Remote Monitoring Program was deployed to select special operations units in late 2025 and is scheduled for broader joint-force deployment in fiscal year 2026. That shift matters because it shows that wearable systems are now expected to support training, safety, hazard awareness, and mission readiness within the same hardware environment. RTI International's AlphaWear program integrates heat strain and infection risk monitoring into a defense-focused precision health platform. Launched in October 2025, AlphaWear is a wearable data platform for US military personnel that enables real-time tracking of heat stress, infection risk, and mental health using fitness-style devices. This technology highlights the growing role of wearables in enhancing military readiness and operational efficiency. As this capability expands, the military wearables market is separating further from consumer formats, as military designs must accommodate ballistic protection, communications gear, and contested field conditions rather than comfort-led daily use, strengthening a protected niche where defense-specific integration matters as much as sensor performance. It also raises the value of software layers that can turn raw biometric data into usable alerts without adding more hardware burden per soldier.

Lack of Standardized Interoperability Frameworks Across Allied Forces

Interoperability remains a structural brake on the military wearables market because coalition operations still do not operate around a single shared hardware and data standard. The US Army's Mission Partner Kit enhanced multinational command-and-control connectivity during exercises such as Saber Strike 24 and Saber Junction 24 by enabling shared situational awareness, secure chat, voice communication, and collaboration tools. However, significant challenges persist in achieving broader coalition interoperability, particularly regarding incompatible communication networks, data-sharing protocols, classification rules, and the adoption of standardized software-based frameworks across allied formations. Europe is trying to address that gap through structured programs such as the ACHILE effort, which is working to harmonize next-generation dismounted soldier systems across multiple member states through 2027. The same push is visible in the broader European defense base, where the ARMETISS program is developing common smart garment modules across a multi-country consortium. Until these efforts translate into procurement-level interface discipline, armies will continue to face higher integration costs whenever national wearable stacks meet in joint deployments. That raises switching costs and tends to favor established cross-border suppliers over smaller specialists, which slows the pace at which the military wearables market can scale across alliances.

Other drivers and restraints analyzed in the detailed report include:

- Integration of Augmented-Reality Systems for Battlefield Visualization

- Open-Standard Modular AI Accelerators Reducing SWaP for On-Edge Processing

- High Cybersecurity Costs Outweighing ROI Compared to Legacy Equipment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bodywear accounted for the largest share in 2025, with 41.55%, and that base still defines the center of volume in the military wearables market. This position reflects the fact that bodywear already sits at the core of protection and load carriage, which makes it the easiest layer for electronics integration to enter through existing purchasing channels. Headwear is becoming increasingly significant as helmets evolve toward modular digital architectures. Anduril's EagleEye program exemplifies this trend by integrating ballistic protection, AI-enabled vision, and command interfaces into a unified platform. Eyewear remains active through night vision and display upgrades, while wristwear and hearables continue to serve smaller but useful roles in local control, team awareness, and protected communications. The military wearables market, therefore, still depends on stable body-borne procurement for scale, even as exoskeletons attract the strongest growth narrative at the edge of the segment.

Exoskeletons are forecast to grow at a 6.65% CAGR through 2031, making them the fastest-growing category in the military wearables market within the wearable type segmentation. That pace reflects a clear shift from demonstration programs toward operational relevance, especially in missions where endurance, load carriage, and repetitive strain matter more than broad unit scale. The strongest near-term signal came from Ukraine in March 2026, when forces began using exoskeletons on the frontline to reduce strain and improve artillery loading productivity under combat conditions. In the military wearable industry, this type of live use carries more weight than lab performance because procurement agencies look for evidence that wearable support systems can work under field stress, maintenance pressure, and uncertain power conditions.

Communication and computing led the application split, accounting for 37.20% of the military wearables market in 2025, indicating that networked operations remain central to current demand. This category remains anchored by radios, tactical displays, and battle management interfaces that connect the individual soldier to the wider unit. Vision and surveillance continue to attract funding through night-vision and augmented display programs, while navigation and positioning are gaining weight as forces prepare for more degraded or denied-signal environments. Protection and survivability still provide the most stable volume base because they are tied to long-established procurement cycles, and health and stress monitoring is gaining ground as systems like WARP show practical value in training safety and force readiness. The military wearables market is therefore broadening across applications. However, the largest spending still follows communications, while the fastest change is occurring in how programs manage power across the full soldier kit.

Power and energy management is projected to grow at a CAGR of 5.80% through 2031, emerging as the fastest-growing application area within the military wearables market. The increase is attributed to a fundamental operational factor: each additional display, sensor, radio, or computing module raises the soldier's power requirements. The segment is gaining importance because modern soldier kits can no longer be optimized as independent devices; instead, they need shared power logic, higher battery density, and lower overall energy waste during extended missions. In the military wearable industry, energy management is moving from a support function to a core part of system design because endurance directly affects mission time, mobility, and gear weight.

Geography Analysis

North America held 47.65% of the market in 2025, giving the region the largest share of the military wearables market and of global defense wearable procurement. Its lead comes from the depth of US defense budgets, the presence of major system integrators, and a procurement base that can absorb both established primes and newer technology firms.

Europe is seeing synchronized program activity, and that is lifting the military wearables market across both national procurement and shared industrial initiatives. The IVAS program's shift in 2025, when Anduril and Microsoft expanded their partnership for future development and cloud support, showed how quickly the region can redirect program leadership when performance expectations are not met. The UK reinforced this regional momentum in February 2026 when the MoD awarded BlackTree Technologies a contract worth up to GBP 86 million (USD 116.99 million) for the Dismounted Data System. The AI-capable system includes radios, headsets, display tablets, cables, batteries, pouches, and antennas, with deliveries to the UK Army planned in tranches from September 2026 and full rollout expected by 2027. In April 2026, Germany's IdZ-ES call-off order activated a major tranche under the February 2025 framework contract, the largest soldier-systems procurement framework for Rheinmetall and BAAINBw. The EUR 1.04 billion (USD 1.21 billion) order includes modernizing existing systems, procuring 237 additional platoon systems, and supporting subcontractors involved in IT equipment, optics, optronics, military clothing, protective gear, and related services. Regional capability building is also visible in common development projects, especially ARMETISS, which links seven nations and 20 partners around smart garment technologies. This is significant as Europe is increasing its equipment purchases but also working to establish a unified architecture and enhance local industrial capabilities for future replacement cycles. In contrast, the Middle East and Africa account for a smaller share of the overall market. However, interest in advanced optics, head-mounted systems, and localized protective manufacturing is driving selective growth opportunities for suppliers with regional partnerships.

Asia Pacific is forecast to grow at a 6.45% CAGR through 2031, making it the fastest-growing regional market for military wearables. This pace reflects rising defense budgets, stronger indigenous content rules, and the need to modernize large ground forces in contested security environments. India's F-INSAS effort, South Korea's Warrior Platform work, and China's continued investment in exoskeletons and digital soldier tools show that the region is not relying on a single model of adoption, but on several national pathways with different industrial strategies. Australia also adds relevance through battery development work that supports the longer endurance goals behind wearable deployments. The larger strategic effect is that Asia Pacific growth is building local supply capacity and demand, which may improve resilience for national programs but can also deepen interoperability gaps across the wider military wearables market.

- BAE Systems plc

- Lockheed Martin Corporation

- Thales Group

- Elbit Systems Ltd.

- Safran SA

- Northrop Grumman Corporation

- Rheinmetall AG

- RTX Corporation

- L3Harris Technologies, Inc.

- Honeywell International Inc.

- SAAB AB

- Gentex Corporation

- Teledyne Technologies Incorporated

- Ekso Bionics Holdings, Inc.

- Black Diamond Advanced Technology, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased global investment in next-generation soldier modernization programs

- 4.2.2 Growing operational need for real-time biometric and health monitoring

- 4.2.3 Advancements in battery energy density enhancing mission endurance

- 4.2.4 Deployment of AI-driven sensor fusion for enhanced situational awareness

- 4.2.5 Emergence of low-SWaP photonics enabling wearable directed-energy technologies

- 4.2.6 Integration of augmented reality (AR) systems for battlefield visualization and mission planning

- 4.3 Market Restraints

- 4.3.1 Lack of standardized interoperability frameworks across allied forces

- 4.3.2 High cybersecurity costs outweighing ROI compared to legacy equipment

- 4.3.3 Geopolitical instability impacting lithium and critical battery material supply chains

- 4.3.4 Rising ethical concerns over continuous biometric surveillance of soldiers

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of Substitutes

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Bargaining Power of Suppliers

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Wearable Type

- 5.1.1 Headwear

- 5.1.2 Eyewear

- 5.1.3 Wristwear

- 5.1.4 Bodywear

- 5.1.5 Hearables

- 5.1.6 Exoskeletons

- 5.2 By Application

- 5.2.1 Communication and Computing

- 5.2.2 Vision and Surveillance

- 5.2.3 Navigation and Positioning

- 5.2.4 Power and Energy Management

- 5.2.5 Protection and Survivability

- 5.2.6 Health and Stress Monitoring

- 5.3 By End-User

- 5.3.1 Land Forces

- 5.3.2 Airborne Forces

- 5.3.3 Naval Forces

- 5.4 By Core Technology

- 5.4.1 Smart Textiles

- 5.4.2 AR/VR Optics and Waveguides

- 5.4.3 AI-Driven Sensor Fusion

- 5.4.4 Energy Harvesting

- 5.4.5 Wearable Robotics and Actuators

- 5.4.6 Flexible and Transparent Displays

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 BAE Systems plc

- 6.4.2 Lockheed Martin Corporation

- 6.4.3 Thales Group

- 6.4.4 Elbit Systems Ltd.

- 6.4.5 Safran SA

- 6.4.6 Northrop Grumman Corporation

- 6.4.7 Rheinmetall AG

- 6.4.8 RTX Corporation

- 6.4.9 L3Harris Technologies, Inc.

- 6.4.10 Honeywell International Inc.

- 6.4.11 SAAB AB

- 6.4.12 Gentex Corporation

- 6.4.13 Teledyne Technologies Incorporated

- 6.4.14 Ekso Bionics Holdings, Inc.

- 6.4.15 Black Diamond Advanced Technology, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment