|

시장보고서

상품코드

2062377

K-12 교원용 기술 트레이닝 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)K-12 Technology Training For Teachers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

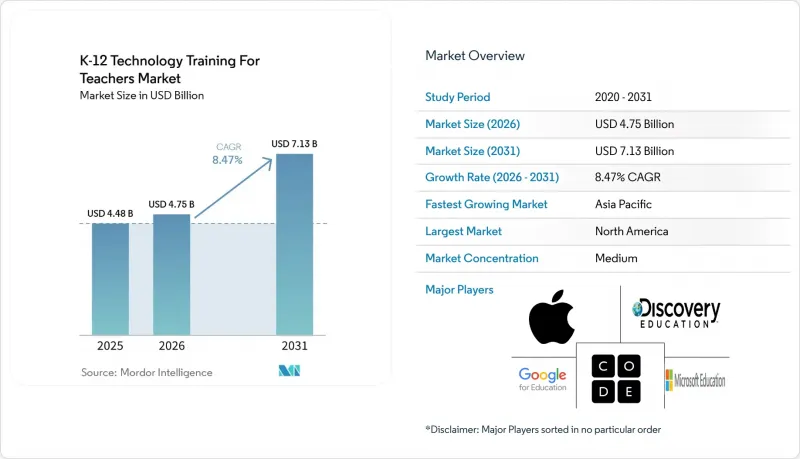

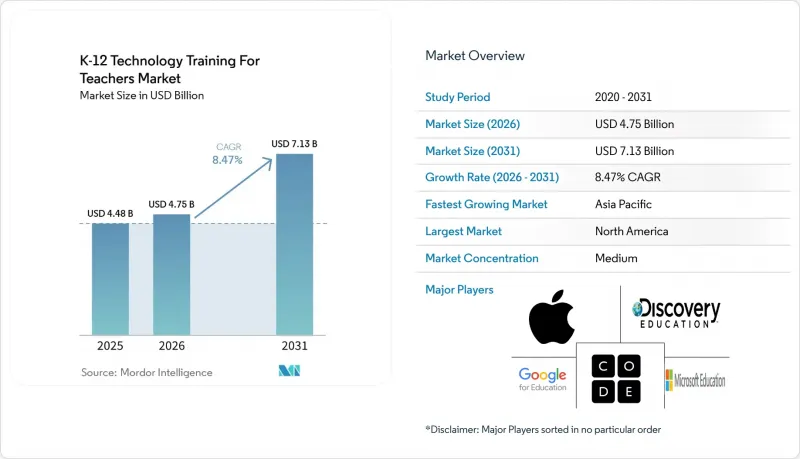

Mordor Intelligence에 의하면, K-12 교원용 기술 트레이닝 시장 규모는 2025년 44억 8,000만 달러로 평가되었고, 2026년 47억 5,000만 달러로 추정되고, 2031년까지 71억 3,000만 달러로 확대될 전망이며, 2026-2031년 CAGR 8.47%를 나타낼 것으로 예측됩니다.

본 보고서는 교육 형태별(온라인 자율 학습형, 강사 주도형 가상 연수 등), 제공 방식별(구독형 PD 플랫폼, 종량제 코스 등), 기술 분야별(기초 디지털 리터러시, STEM 등), 최종 사용자층별(초등학교 교사, 중학교 교사 등) 및 지역별로 분류되어 있습니다. 시장 전망치는 금액(달러) 단위로 제시되어 있습니다.

세계의 K-12 교원용 기술 트레이닝 시장 동향과 인사이트

하이브리드형 PD의 도입이 전 세계적으로 가속화되고 있습니다.

라이브 코호트 세션과 비동기식 마이크로 레슨을 융합한 혼합형 전문 역량 개발은 근무 시간 외의 부담을 늘리지 않으면서 수료율과 수업에 대한 실질적인 적용을 향상시키려는 학군의 요구에 부응하는 형태로 확대되고 있습니다. LAUSD의 마이크로 크레덴셜 제도는 대면 수업 시간, 온라인 모듈, 실습 과제를 명확하게 구분하고 있으며, 이는 높은 수료율과 급여 포인트 취득 자격으로 이어져 교사들의 참여 의욕을 높이고 있습니다. 학군 팀은 모델 제시 및 질의응답을 위한 실시간 소통, 바쁜 일정에 맞춘 유연한 진행 속도 조절, 그리고 수업에 활용하기 전에 오해를 해소할 수 있는 내장형 진행 상황 확인 기능을 꼽았으며, 이러한 요소들은 2026년의 실무적 요구 사항에 부합합니다. PowerSchool University의 오픈 랩과 제품 업데이트에 따른 내장형 마이크로 트레이닝은 교사가 이미 사용하고 있는 도구 내에서 시간적 제약이 있는 워크플로우 변경에 대응함으로써, 하이브리드형 학습 경로를 보완합니다. 이러한 노력은 LMS 및 컨텐츠 업데이트에 따른 이탈률을 낮추고, K-12 교원용 기술 트레이닝 시장에서 새로운 기능의 지속적인 활용을 촉진합니다. 하이브리드 형식이 계약 시간 및 인정 학점과 조화를 이루게 됨에 따라, 기술 소양을 대대적으로 향상시키려는 학군에게 이는 점차 기본 선택지가 되어가고 있습니다.

생성형 AI를 활용한 수업용 전문성 개발(PD)에 대한 수요

각 학군은 PD 카탈로그에서 AI 리터러시와 책임 있는 이용에 대한 프레임워크를 우선시함으로써, 학생들의 AI에 대한 친숙도와 교사의 AI 대응 도구 활용 수준 간의 숙련도 격차를 해소하는 방향으로 나아가고 있습니다. 구글은 2026년 4월 ‘Gemini Certified Educator’ 시험을 도입하고 6개월간의 무료 이용 기간을 제공함으로써, 검증된 AI 자격증을 전 세계 K-12 교육자들에게 역량을 입증하는 확장 가능한 지표로 자리매김했습니다. 마이크로소프트의 ‘Elevate for Educators’ 프로그램은 2026년에 무료 자격증, AI 커뮤니티, 그리고 수업 계획 및 평가를 안전한 실천과 연계하는 ‘Teach in Microsoft 365 Copilot’ 앱을 출시했습니다. Discovery Education의 연계 생태계는 IBM SkillsBuild PD와 AI TeacherTools를 통합하고 있어, 교육자들은 교실 자료와 학생 데이터를 바탕으로 상황에 맞는 조언을 받을 수 있습니다. 정책 또한 추진력으로 작용하고 있으며, 중국이 2026년 4월에 발표한 ‘AI 플러스 교육’ 계획에서는 2030년까지 교사 자격 시험에 AI 역량을 포함시키기로 규정되어 있어, 이에 따라 교육 시스템 전반에서 AI에 초점을 맞춘 PD(전문 역량 개발)에 대한 수요가 확대되고 있습니다. 이러한 동향은 2026년 K-12 교원용 기술 트레이닝 시장에서 AI 활용 역량과 안전한 실천에 대한 최저 기준을 높이는 계기가 될 것입니다.

ESSER 종료 후 PD 예산은 축소됩니다.

2025년 지급 기한 연장 제한으로 인해 의무적으로 지급해야 할 자금의 향방이 불투명해졌고, 이에 따라 제공업체에 대한 지급이 일시 중단되면서 많은 학군에서 수년에 걸친 전문성 개발(PD) 계획에 차질이 생겼습니다. 2026년, 강력한 증거 시스템을 갖춘 학군은 전문성 개발(PD) 이수 현황을 학생의 성과 및 검증된 자격과 연계함으로써 예산 갱신을 보다 효과적으로 주장할 수 있게 될 것입니다. 제2-A편의 자금은 여전히 기반이 되고 있지만, 관리자는 현재 학교 간에 인정되는 자격 인증 및 급여 가산에 대한 명확한 방향을 제시하는 제안을 우선시하고 있습니다. 각 교육 서비스 제공업체들은 증거 기반 포트폴리오와 규정 준수 대응 모듈을 도입하여 이에 대응하고 있으며, 이를 통해 교육구는 예산이 축소되는 상황에서도 연수 기회를 유지할 수 있게 되었습니다. 이러한 추세는 K-12 교원용 기술 트레이닝 시장에서 그 효과를 입증하고 고용주에 관계없이 자격을 상호 인정받을 수 있음을 보여주는 솔루션에 유리한 조건을 제공합니다. 이러한 변화로 인해 일회성 워크숍은 줄어들고, 검증된 평가 체계와 투명한 수강자 명단을 갖춘 여러 차례에 걸친 연수 시리즈가 중시되고 있습니다.

부문별 분석

2025년에는 온라인 자기 주도형 및 가상 형식이 37.38%의 점유율을 차지했으나, 교사들이 유연한 진도 조절과 실시간 그룹 교류를 요구함에 따라 블렌디드 러닝은 2031년까지 연평균 성장률(CAGR) 14.36%를 나타낼 것으로 예측됩니다. K-12 교원용 기술 트레이닝 시장은 동기식 모델과 비동기식 실습을 결합한 하이브리드형으로의 전환이 진행되고 있으며, 이는 근무 시간과의 조화를 도모하고 야간 장시간 세션으로 인한 번아웃을 완화하기 위한 것입니다. 학군은 학점 및 수료증 취득에 포트폴리오와 수업 내 실습을 필수 요건으로 삼음으로써 수료율을 높이고 있으며, 이를 통해 새로운 기술을 보다 깊이 있게 습득할 수 있도록 돕고 있습니다. LMS 포털에 통합된 플랫폼 업데이트에 관한 마이크로 트레이닝은 이용 시 적시에 지원을 제공하며, 일상적인 활용을 강화합니다. 대시보드 내에서 대상 범위를 좁혀 제시된 PD(전문 역량 개발) 제안을 보여주는 컨텐츠 생태계는 교육자가 연수를 학생들의 실제 요구와 연계하는 데 도움이 되고 있습니다. 교육 서비스 제공업체가 하이브리드 교육 설계를 학군에서 인정하는 평가 기준에 따른 자격 요건과 연계함에 따라, K-12 교원용 기술 트레이닝 시장이 그 혜택을 누리고 있습니다.

'CS Principles'나 'CSA'와 같은 교육 과정에서 혼합형 과정에 근거에 기반한 피드백이나 수업 실습에 관한 코칭이 포함될 경우, 수료율과 지속률이 향상됩니다. 학군이 실시간 교류와 비동기식 연습을 결합한 코호트 모델을 표준화해 나감에 따라, K-12 교원용 기술 트레이닝 시장에서 혼합형 교육 방식의 규모가 확대될 것으로 예측됩니다. 이동이 제한된 상황에서는 실시간 가상 워크숍이 하나의 대안이 될 수 있지만, 대규모 학군의 경우 시차나 서비스 범위 제한으로 인해 여전히 참여에 제약이 따르고 있습니다. 제공업체는 업데이트 후 교사가 모듈 전체를 다시 수강하지 않고도 워크플로를 재학습할 수 있도록 짧은 복습 컨텐츠를 추가했으며, 이것이 2026년의 지속적인 변경 주기를 뒷받침하고 있습니다. 인증 자격 및 학군의 급여 체계와의 일관성 덕분에, 증거 기반의 과제와 실무 중심의 과제를 포함하는 혼합형 과정을 이수하려는 교사의 의욕이 높아집니다. 이 형식은 K-12 교원용 기술 트레이닝 시장에서 기존의 자기 주도형 모델보다 더 높은 성장세가 예상됩니다.

2025년에는 학군 전체 계약 및 교육 기관 대상 프로그램이 39.87%를 차지했습니다. 이는 플랫폼 제공업체가 다년 주기로 갱신되는 SIS(학생 정보 시스템) 및 LMS(학습 관리 시스템) 계약에 PD(교원 연수)를 포함시켰기 때문입니다. 교육자들이 학교 간 이동이 가능한 이수 누적형 인증이나 증거 기반의 자격을 요구함에 따라, 인증 기반 및 구독형 플랫폼은 연평균 성장률(CAGR) 15.44%로 성장할 것으로 전망됩니다. K-12 교원용 기술 트레이닝 시장은 교육구가 대규모 생태계 계약을 유지하면서 계약 갱신 기간 사이에 새로운 역량 요건에 대응하기 위해 구독형 과정을 추가하는 이러한 구조를 반영하고 있습니다. 구글은 2026년, 언어나 맥락에 관계없이 AI 리터러시를 대규모로 보급하기 위해 ‘Gemini 교육자 인증’의 6개월 무료 이용 기간을 도입했습니다. 마이크로소프트의 ‘Elevate for Educators’는 교육구가 학교 네트워크 내에서 활용할 수 있는 무료 자격증 및 AI 커뮤니티를 제공하여, 동료 간의 지원과 지속성을 유지할 수 있도록 돕습니다. 이러한 변화로 인해 K-12 교원용 기술 트레이닝 시장 전반에서 자격의 이전 가능성이 높아지고, 일회성 워크숍에 대한 의존도가 낮아지고 있습니다.

2025년 K-12 교원용 기술 트레이닝 시장에서 학군 전체 계약이 가장 큰 비중을 차지하고 있지만, 급여 체계 및 계약 갱신과의 명확한 연계 덕분에 구독형 및 인증 모델이 현재 더욱 빠르게 확대되고 있습니다. 협회와 비영리 단체들은 수강 시간이 아닌 수업에서의 성과를 평가함으로써 능력 중심의 평가를 확대하고 있으며, 이는 자율적으로 활동하는 교육자들과 전문 자격 취득을 목표로 하는 중등 교육 교사들로부터 지지를 받고 있습니다. 주 정부의 지원 프로그램은 적용 범위와 코호트 구성에 따라 수료율에 영향을 미칩니다. 이것들은 학군이 우선순위가 높은 자격 인증 제공 파트너를 선정할 때 고려하는 요소들입니다. 명부 동기화 및 수료 기록의 상호 운용성은 관리상의 부담을 줄이고 PD 코디네이터의 감사 절차를 간소화하기 때문에 도입을 촉진하는 요인이 되고 있습니다. 인증의 명확성이 높아짐에 따라, K-12 교원용 기술 트레이닝 시장에서 구독 및 인증 프로그램 코호트는 학군 전체 계약을 보완하는 지속적인 요소로 자리 잡고 있습니다.

지역별 분석

2025년, 북미는 K-12 교원용 기술 트레이닝 시장의 37.35%를 차지했습니다. 이는 각 학군이 PD를 수년에 걸친 생태계 계약과 연계하여, ESSER 종료 후 제공업체에 대한 지급 및 계약 갱신에 영향을 미친 전환 과정을 관리했기 때문입니다. 주 차원의 컴퓨터 과학(CS) 인증 정책에 따라, 역량을 문서화하고 중학교 및 고등학교 전체의 인력 배치 계획을 충족하는 체계적인 코호트에 대한 수요가 증가했습니다. OneRoster 및 Ed-Fi와 같은 상호운용성 표준은 자격의 이전 가능성과 명부 관리 업무를 지속적으로 정립해 왔으며, 학군의 감사 및 규정 준수를 간소화했습니다. 벤더가 주최하는 행사나 오픈 랩 형식의 활동을 통해, 교사들이 일상적으로 사용하는 구체적인 도구에 대해 엔지니어로부터 실무 중심의 지도를 받음으로써, 새로운 기능의 도입이 가속화되었습니다. 2024년 주요 플랫폼에서 발생한 소유권 변경은 2026년에 학군 전체 차원에서 정착률을 높이기 위한 수단으로서 번들형 PD의 역할을 강화했습니다.

아시아태평양에서는 각국의 프로그램이 교사를 대상으로 한 AI 소양 및 자격 요건에 부합하는 연수를 우선시하고 있어, 2031년까지 연평균 성장률(CAGR) 13.38%로 확대될 것으로 전망됩니다. 아시아태평양의 K-12 교원용 기술 트레이닝 시장은 각국 교육부가 자격 정보를 국가 플랫폼에 통합하고, 도입을 지속해 나갈 수 있는 동료 커뮤니티를 구축함에 따라 성장이 예상됩니다. 중국의 ‘AI 플러스 교육’ 계획에 따르면, 2030년까지 교사 자격 시험에 AI 역량을 포함시키는 것이 의무화되어 있으며, 이것이 장기적인 전문성 개발(PD) 수요의 기반이 되고 있습니다. ‘러닝 임팩트 재팬’ 등의 지역 교류를 통해 상호 운용성과 증거 추적을 지원하는 기준, 노력, PD 설계의 실천이 확산되고 있습니다. SEAMEO가 주도하는 이니셔티브와 각국의 프로젝트에서는 다양한 학교 제도에 횡단적으로 적용 가능한 혼합형 방식과 역량 프레임워크가 계속해서 중시되고 있습니다.

유럽에서는 회원국들이 DigCompEdu를 준수하며, 실시간 그룹 학습과 국가 플랫폼에 기반을 둔 비동기형 모듈을 결합한 하이브리드형 전문성 개발(PD)을 확대하고 있어, 꾸준한 확산세가 이어지고 있습니다. 기기 및 디스플레이 생태계는 지속적인 PD와 교원 커뮤니티가 지속적인 활용과 교실 내 혁신을 주도하는 모범적인 학교를 평가했습니다. 라틴아메리카에서는 민관 협력 프로그램 및 지역 파트너를 통해 중등 교육 및 중학교 단계에서 진행자를 둔 워크숍을 제공하며, 컴퓨터 과학(CS) 및 인공지능(AI) 교사 연수를 추진하고 있습니다. 중동 및 아프리카에서는 인증 프로그램 및 플랫폼과의 제휴가 공식적인 PD 커뮤니티를 촉진하고 있지만, 예산과 통신 환경이 해당 지역의 진척 속도와 규모를 좌우하고 있습니다. 이러한 지역적 추세는 2026년 K-12 교원용 기술 트레이닝 시장의 다양한 성장 전망을 전반적으로 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the k-12 technology training for teachers market size is projected to expand from USD 4.48 billion in 2025 and USD 4.75 billion in 2026 to USD 7.13 billion by 2031, registering a CAGR of 8.47% between 2026 to 2031.

This report is Segmented by Training Modality (Online Self-Paced, Instructor-Led Virtual, and More), Delivery Mode (Subscription-Based PD Platforms, Pay-As-You-Go Courses, and More), Technology Focus (Basic Digital Literacy, STEM, and More), End-User Level (Elementary School Teachers, Middle School Teachers, and More), and Geography. The Market Forecasts are Provided in Value (USD).

Global K-12 Technology Training For Teachers Market Trends and Insights

Hybrid PD Adoption Accelerates Globally

Blended professional development that merges live cohort sessions with asynchronous micro-lessons is scaling as districts seek better completion and classroom transfer without increasing after-hours demands. LAUSD's micro-credentialing structure uses a clear split between face-to-face time, online modules, and applied homework, leading to high completion and salary point eligibility, which reinforces teacher participation. District teams cite real-time interaction for modeling and Q&A, flexible pacing for busy schedules, and embedded check-ins that surface misconceptions before classroom use, which fit practical needs in 2026. PowerSchool University's open labs and embedded micro-trainings around product updates complement hybrid pathways by addressing time-sensitive workflow changes within the tools teachers already use. These practices reduce churn during LMS or content updates and encourage sustained use of new features inside the K-12 technology training for teachers market. As hybrid formats align with contract time and recognized credits, they become a default choice for districts upgrading technology fluency at scale.

Generative AI Classroom PD Demand

Districts are moving to close the proficiency gap between student familiarity with AI and teacher use of AI-aligned tools by prioritizing AI literacy and responsible-use frameworks in PD catalogs. Google introduced the Gemini Certified Educator exam in April 2026, offering a six-month free window, positioning verified AI credentials as a scalable signal of competency for K-12 educators worldwide. Microsoft's Elevate for Educators program created no-cost credentials, AI communities, and a Teach in Microsoft 365 Copilot app that aligns lesson planning and assessments with safe practice in 2026. Discovery Education's connected ecosystem integrates IBM SkillsBuild PD and AI TeacherTools, so educators receive contextual nudges tied to classroom resources and student data. Policy is also a catalyst, with China's April 2026 AI Plus Education plan embedding AI competencies into teacher qualification exams by 2030, which expands AI-focused PD demand system-wide. These developments raise the floor for AI literacy and safe practice in the K-12 technology training for teachers market in 2026.

Post-ESSER PD Budgets Compress

Late-liquidation limits in 2025 created uncertainty for obligated funds and paused payments to providers, which disrupted multi-year PD planning in many districts. Districts with strong evidence systems can better defend renewals by linking PD completions to student outcomes and verified credentials in 2026. Title II-A funding remains a baseline, but administrators now prioritize offers with clear pathways to endorsements and salary credits that are recognized across schools. Providers have adapted with evidence portfolios and compliance-ready modules that help districts retain training lines within slimmer budgets. This favors solutions that demonstrate impact and credential portability across employers in the K-12 technology training for teachers market. The shift reduces one-off workshops and elevates multi-session sequences with verified assessments and transparent rostering.

Other drivers and restraints analyzed in the detailed report include:

- CS Mandates Expand Teacher PD

- Rapid LMS Upgrades Require Retraining

- Teacher Burnout Limits PD Time

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Online self-paced and virtual formats held 37.38% share in 2025, while blended learning is projected to grow at 14.36% CAGR through 2031 as teachers seek live cohort interaction with flexible pacing. The K-12 technology training for teachers market is shifting toward hybrid pathways that pair synchronous modeling with asynchronous practice, aligning with contract time and reducing burnout from extended evening sessions. Districts improve completion when portfolios and classroom application are required for credit and compensation, which encourages deeper transfer of new skills. Embedded micro-training on platform updates within LMS portals provides timely support at points of use, which strengthens day-to-day adoption. Content ecosystems that surface targeted PD nudges inside dashboards are helping educators link training to real student needs. The K-12 technology training for teachers market benefits when providers align a hybrid design to assessment-backed credentials recognized by districts.

Completion and persistence are stronger when blended courses include feedback on evidence and coaching on classroom implementation for curricula such as CS Principles and CSA. The K-12 technology training for teachers market size for blended modality is projected to grow as districts standardize cohort models with live touchpoints and asynchronous practice. Live virtual workshops remain an option when travel is limited, yet time zones and coverage still constrain participation in large districts. Providers add bite-sized refreshers so teachers can relearn workflows after updates without repeating full modules, which supports continuous change cycles in 2026. Alignment to recognized credentials and district salary lanes increases teacher motivation to complete blended pathways that include evidence and applied tasks. This modality is positioned to outpace legacy self-paced models inside the K-12 technology training for teachers market.

District-wide contracts and institutional programs accounted for 39.87% in 2025, as platform providers embedded PD into SIS and LMS agreements that renew on multi-year cycles. Certification-based and subscription platforms are forecast to grow at 15.44% CAGR as educators seek stackable recognition and evidence-based credentials that travel between schools. The K-12 technology training for teachers market reflects this mix as districts maintain large ecosystem agreements while adding subscription cohorts to address emerging competencies between contract refreshes. Google introduced a six-month free window for Gemini educator certification in 2026 to seed AI literacy at scale across languages and contexts. Microsoft's Elevate for Educators adds no-cost credentials and AI communities that districts can deploy within school-based networks to support peers and maintain continuity. These shifts increase credential portability and reduce reliance on one-off workshops across the K-12 technology training for teachers market.

Despite district-wide contracts accounting for the largest share of the K-12 technology training for teachers market in 2025, subscription and certification models now expand faster due to clear crosswalks into salary lanes and renewals. Associations and nonprofits scale competency-based assessment by validating classroom evidence rather than seat time, which appeals to self-directed educators and secondary teachers pursuing endorsements. State stipend programs influence completion rates based on coverage levels and cohort structure, factors that districts consider when choosing delivery partners for high-priority endorsements. Interoperability for roster sync and completion records is an adoption driver, since it lowers administrative overhead and simplifies audits for PD coordinators. As recognition clarity improves, subscription and certification cohorts become a regular complement to district-wide agreements inside the K-12 technology training for teachers market.

Geography Analysis

North America accounted for 37.35% of the K-12 technology training for teachers market share in 2025 as districts aligned PD with multi-year ecosystem contracts and managed post-ESSER transitions that affected provider payments and renewals. State-level CS endorsement policies strengthened demand for structured cohorts that document competencies and satisfy staffing plans across middle and high school. Interoperability standards such as OneRoster and Ed-Fi continued to shape credential portability and rostering practices, simplifying district audits and compliance. Vendor events and open-lab formats accelerated the adoption of new features as teachers received hands-on guidance from engineers on the exact tools they use every day. Ownership changes at major platforms in 2024 reinforced the role of bundled PD as a retention lever across large districts in 2026.

Asia-Pacific is projected to expand at a 13.38% CAGR through 2031 as national programs prioritize AI literacy and credential-aligned training for teachers. The K-12 technology training for teachers market in Asia-Pacific is set to grow as ministries embed credentials into national platforms and build peer communities that sustain adoption. China's AI Plus Education plan mandates AI competencies in teacher qualification exams by 2030, which anchors long-term PD demand. Regional exchanges such as Learning Impact Japan spread standards, work, and PD design practices that support interoperability and evidence tracking. SEAMEO-led initiatives and national projects continue to emphasize blended formats and competency frameworks that scale across diverse school systems.

Europe maintains steady adoption as member states align with DigCompEdu and expand hybrid PD that combines live cohorts and asynchronous modules anchored to national platforms. Device and display ecosystems recognize exemplary schools where ongoing PD and teacher communities drive sustained use and classroom innovation. Latin America advances CS and AI teacher training through public-private programs and regional partners that deliver facilitated workshops in secondary and middle grades. In the Middle East and Africa, recognition programs and platform partnerships encourage formal PD communities, while budgets and connectivity shape local pacing and scale. These regional patterns collectively support a diverse growth outlook for the K-12 technology training for teachers market in 2026.

- Google for Education

- Microsoft Education

- Apple Education

- Discovery Education

- BetterLesson

- Instructure (Canvas / Impact)

- PowerSchool (Schoology Learning)

- ISTE + ASCD (ISTE Certification)

- Common Sense Education (PD)

- Code.org (Teacher Professional Learning)

- LEGO Education (Professional Development)

- Edmentum (Professional Services)

- HMH (Professional Learning)

- Savvas Learning Company (Professional Learning)

- Amplify (Professional Development)

- Nearpod (PD / Camp Engage)

- Seesaw (Training & PD)

- Promethean (Learn Promethean)

- SMART Technologies (Learn SMART)

- GoGuardian (Training / University)

- Teq (OTIS for Educators)

- D2L Brightspace (K-12 Professional Learning)

- Blackboard / Anthology (Professional Development)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hybrid PD adoption accelerates globally

- 4.2.2 Generative AI classroom PD demand

- 4.2.3 CS mandates expand teacher PD

- 4.2.4 Rapid LMS upgrades require retraining

- 4.2.5 Micro-credential incentives spur upskilling

- 4.2.6 Interoperability, rostering standards demand training

- 4.3 Market Restraints

- 4.3.1 Post-ESSER PD budgets compress

- 4.3.2 Teacher burnout limits PD time

- 4.3.3 Fragmented credential recognition slows uptake

- 4.3.4 Procurement, privacy reviews delay pilots

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Competitive Rivalry

- 4.7.2 Threat of New Entrants

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Bargaining Power of Suppliers

- 4.7.5 Threat of Substitutes

5 Market Size & Growth Forecasts

- 5.1 By Training Modality

- 5.1.1 Online Self-paced

- 5.1.2 Instructor-led Virtual

- 5.1.3 Blended

- 5.1.4 On-site Workshops

- 5.2 By Delivery Mode

- 5.2.1 Subscription-based PD Platforms

- 5.2.2 Pay-as-you-go Courses

- 5.2.3 District-wide Contracts

- 5.2.4 Certification Programs

- 5.3 By Technology Focus

- 5.3.1 Basic Digital Literacy

- 5.3.2 STEM / Coding & Robotics

- 5.3.3 LMS Utilisation

- 5.3.4 Emerging Tech (AR/VR, AI)

- 5.3.5 Cyber-security & Data Privacy

- 5.4 By End-User Level

- 5.4.1 Elementary School Teachers

- 5.4.2 Middle School Teachers

- 5.4.3 High School Teachers

- 5.4.4 Special Education Teachers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 Canada

- 5.5.1.2 United States

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 BENELUX

- 5.5.3.7 NORDICS

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 South-East Asia

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East & Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East & Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles [(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)]

- 6.4.1 Google for Education

- 6.4.2 Microsoft Education

- 6.4.3 Apple Education

- 6.4.4 Discovery Education

- 6.4.5 BetterLesson

- 6.4.6 Instructure (Canvas / Impact)

- 6.4.7 PowerSchool (Schoology Learning)

- 6.4.8 ISTE + ASCD (ISTE Certification)

- 6.4.9 Common Sense Education (PD)

- 6.4.10 Code.org (Teacher Professional Learning)

- 6.4.11 LEGO Education (Professional Development)

- 6.4.12 Edmentum (Professional Services)

- 6.4.13 HMH (Professional Learning)

- 6.4.14 Savvas Learning Company (Professional Learning)

- 6.4.15 Amplify (Professional Development)

- 6.4.16 Nearpod (PD / Camp Engage)

- 6.4.17 Seesaw (Training & PD)

- 6.4.18 Promethean (Learn Promethean)

- 6.4.19 SMART Technologies (Learn SMART)

- 6.4.20 GoGuardian (Training / University)

- 6.4.21 Teq (OTIS for Educators)

- 6.4.22 D2L Brightspace (K-12 Professional Learning)

- 6.4.23 Blackboard / Anthology (Professional Development)

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment