|

시장보고서

상품코드

2062420

야외 조명 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Outdoor Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

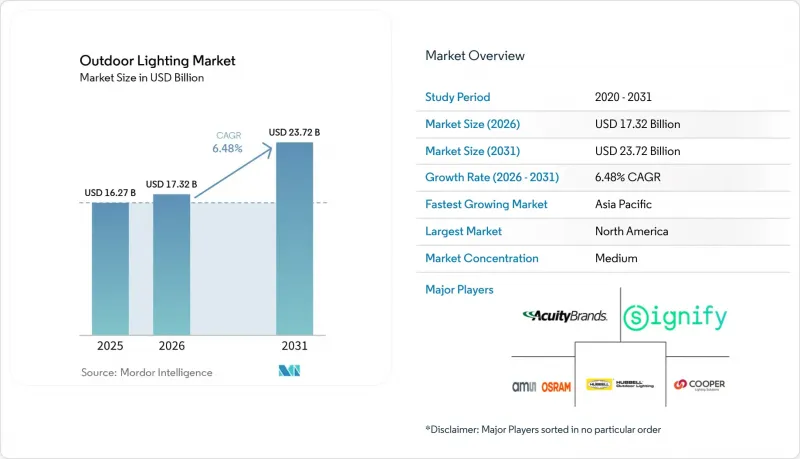

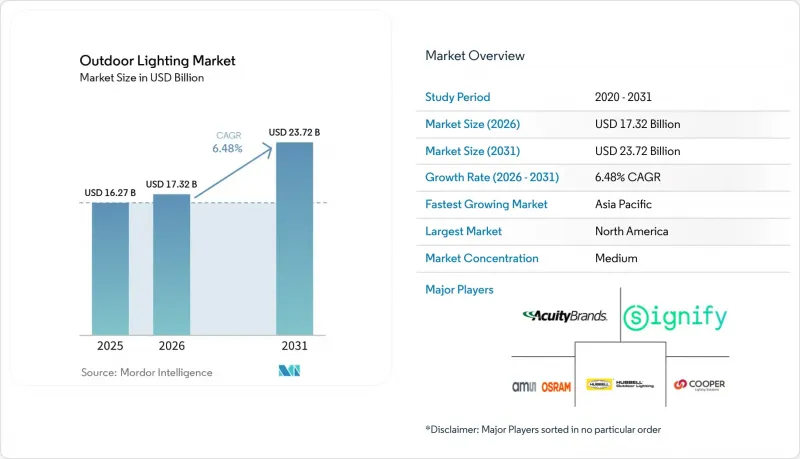

Mordor Intelligence에 의하면, 야외 조명 시장 규모는 2025년 162억 7,000만 달러로 평가되었고, 2026년 173억 2,000만 달러로 추정되고, 2031년까지 237억 2,000만 달러로 확대될 전망이며, 2026-2031년 연평균 복합 성장률(CAGR)은 6.48%를 나타낼 것으로 예측됩니다.

본 보고서는 제품 유형별(장식용, 폴형, 벽면용, 통로 및 계단용, 데크 및 파티오용, 정원용, 방범용, 플러드·스포트라이트용, 볼라드, 기타), 광원별(LED, 형광등, 백열등, 할로겐, 기타), 설치 유형별(신규 설치, 개보수), 용도별(주거용, 상업용), 유통 채널(B2B 직접 판매, 온라인 D2C, 유통업체), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준입니다.

세계의 야외 조명 시장 동향 및 인사이트

급속한 도시화와 인프라 개발

도시에서는 고정된 계통 연계형 시스템에서 성장에 맞추어 확장 가능하고 자산 관리를 강화하는 모듈식·소프트웨어 정의형 조명으로의 전환이 진행되고 있습니다. 2026년 3월, 로스앤젤레스시는 3만 2,000건에 달하는 미처리 서비스 요청과 유지관리 예산을 압박하던 만연한 전선 절도 문제에 대처하기 위해, 최대 6만 기의 태양광 발전식 도로 조명 및 지역 조명을 도입하는 2개년 계획을 승인했습니다. 이는 해당 시에 있어 역대 최대 규모의 단일 조명 투자입니다. 인도 하이데라바드시는 1,340 카롤 루피(1억 6,140만 달러) 규모의 프로그램을 승인하고, 중앙 집중식 제어·감시 시스템, 성과 기반 벌금, 그리고 가동률과 책임성을 확보하기 위한 기기 단위 추적 기능을 갖춘 76만 개의 가로등 현대화를 추진하고 있습니다. 피츠버그시는 구제 계획 자금과 채권 발행으로 얻은 수익을 결합하여 3만 5,000개 이상의 가로등을 무선 관리 및 조도 분석 기능을 갖춘 것으로 교체함으로써, 에너지 소비를 줄이고 빛 누출을 최소화했습니다. 이러한 노력은 새로운 적용 범위의 확대, 수명 주기 비용 절감, 그리고 측정 가능한 서비스 수준을 동시에 달성해야 하는 급속한 도시화가 진행 중인 지역에 대한 실용적인 방향을 제시하고 있습니다. 홍콩 무역개발국의 심리지표 데이터에 따르면, 공공 인프라 계획과 연계된 공급업체들에게 인도, 아세안, 중동이 단기적으로 가장 유망한 수요처 중 하나로 부상하고 있습니다. 아시아 지역의 LED 부품 제조 집적화는 이러한 프로젝트의 확장을 지속적으로 뒷받침하고 있습니다.

에너지 절약형 LED 솔루션에 대한 수요 증가

최저 효율 기준과 신속한 투자 회수 덕분에 LED는 야외 조명의 모든 분야에서 표준적인 선택지가 되었습니다. 2026년 3월에 시행될 뉴욕시의 ‘2025년 에너지 절약 조례’는 조명의 전력 밀도 기준을 강화함으로써, 대부분의 비주거용 실내 및 야외 조명에 있어 고효율 LED 시스템이 규제 준수를 위한 현실적인 해결책이 되었습니다. 2026년 캘리포니아주 ‘타이틀 24’ 개정으로 인해 자연광 반응형 시스템의 적용 범위가 확대되었으며, 다단계 제어를 위한 연속 조광이 의무화되었습니다. 이에 따라 시설이나 주차장의 조명 용도에서는 세밀한 제어가 가능한 네트워크 연결형 LED로의 전환이 촉진되고 있습니다. LED 시스템은 일반적으로 1와트당 100-150루멘의 광속을 제공하며, 기존 램프에 비해 에너지 소비량을 75-80% 절감할 수 있습니다. 또한, 스마트 제어를 통해 일정 제어, 재실 감지, 자연광 활용을 통해 성능이 한층 더 향상됩니다. 웨스트 서식스 카운티 전역에서 진행되는 이번 업그레이드에서는 64,000개의 가로등을 LED로 교체하고, 원격 모니터링 플랫폼에 연결할 예정입니다. 이를 통해 연간 1,070만 kWh의 전력 소비와 1,633톤의 CO2 배출 감축이 예상됩니다. 기존 주택을 재활용하는 개보수 프로그램은 자본을 보존하면서 에너지 절약 효과를 얻을 수 있습니다. 이는 대규모 도입을 통해 45-51%의 절감 효과를 기록한 소켓 교체형 LED로의 업그레이드를 통해 입증되었습니다.

초기 설치 및 개보수 비용이 높음

본격적인 스마트 조명 프로젝트의 경우, 컨트롤러, 게이트웨이, 중앙 관리 소프트웨어에 막대한 비용이 소요되므로 지자체 예산을 압박할 가능성이 있습니다. 단순한 교체 공사라 할지라도 그 규모가 매우 큽니다. 예를 들어, 웨스트 서식스에서는 4년에 걸쳐 6만 4,000개의 도로 조명 기구를 교체하는 프로젝트가 진행되고 있으며, 그 비용은 약 3,070만 달러에 달할 전망입니다. 일부 지자체는 포틀랜드시가 교통사고 다발 구간에 배정하는 전용 자금, 대규모 캠퍼스 및 상업시설의 투자 회수 기간을 단축하는 미국의 179D 세액 공제와 같은 정책 수단 및 인센티브를 통해 이러한 비용을 상쇄하고 있습니다. 그렇긴 하지만, 완전히 네트워크화된 시스템의 투자 회수 기간이 길다는 점과 프로젝트 규모를 제한하는 보조금 상한선으로 인해, 자금 사정이 어려운 지자체에서는 도입이 지연될 가능성이 있습니다. 주택 구매자들도 스마트 기능이나 태양광 발전 및 축전 기능을 갖춘 고급 야외 패키지 제품과 관련해 비슷한 장벽에 직면하고 있어, 가격에 민감한 계층에서의 보급이 지연될 가능성이 있습니다. 또한, 많은 도시에서는 계약을 체결하기 전에 상호 운용성 요건을 정의하고 여러 공급업체의 제어 스택을 검토해야 하기 때문에 거래상의 마찰도 비용 증가로 이어지고 있습니다.

부문별 분석

2025년에는 호스피탈리티, 캠퍼스, 주거 환경에서 디자이너 디자인과 마감재를 도입해 야외 경험을 확장하는 추세가 확산되면서, 장식 조명이 38.82%의 점유율로 해당 부문을 주도했습니다. 가장 빠르게 성장하고 있는 데크 및 파티오 부문은 작업 조명, 분위기 조명, 악센트 조명을 다층적으로 조합하여 야외 생활을 향상시키는 주택 리모델링에 힘입어 연평균 성장률(CAGR) 8.47%로 확대되고 있습니다. 폴 라이트나월라이트는 건축적인 포인트 역할을 할 뿐만 아니라 통로 조명으로도 기능합니다. 한편, HoReCa(호텔 및 레스토랑·카페) 시설에서는 시각적 매력과 내후성의 균형을 갖춘 IP 규격에 부합하는 조명 기구가 지정되어 있습니다. 방범 조명은 움직임에 반응하는 제어 기능과, 시각적 쾌적성을 유지하면서 활동 상황에 맞추어 광량을 조절하는 저눈부심 광학 시스템을 통해 수요가 증가하고 있습니다. 따뜻한 색조의 정원 조명과 볼라드 조명은 야간 사용 시의 쾌적성과 외관의 매력을 높여준다는 점에서 주택 프로젝트에서 계속해서 선호되고 있습니다.

이 부문 수요는 안전성과 자산 가치를 높이고, 연결성이 뛰어나며, 유지보수가 용이하고, 외관의 매력을 높이는 솔루션으로 향하는 야외 조명 시장 동향을 반영하고 있습니다. 공공 기관의 구매 담당자들은 사고 및 법적 책임을 줄이기 위해 보도와 계단의 내파괴성 및 접근성 요건 준수에 중점을 두고 있습니다. 고급 용도의 경우, 고연색성(고CRI) 조명이 호텔 및 레스토랑 등 접객 시설이나 공공 공간에서 외관, 조경, 예술 작품의 색상을 충실하게 재현하는 데 기여하고 있습니다. 또한, 야외 조명 시장에서는 설치 및 유지보수를 신속하게 진행하기 위한 방식이 채택되어, 현장에 미치는 영향을 최소화하면서 프로젝트를 조기에 완료할 수 있게 되었습니다. 데이터를 확보할 수 있는 경우, 설계자는 ‘다크 스카이’ 원칙에 따라 분위기를 해치지 않으면서 위쪽을 향한 빛을 조절하고 있습니다.

2025년 기준으로 LED 기술은 광원 구성의 68.36%를 차지했습니다. 이는 뛰어난 광속 효율, 긴 수명, 그리고 합리적인 가격 덕분에 기존 램프를 계속해서 대체하고 있음을 반영합니다. 그 밖의 광원은 더 작은 규모에서 2026-2031년 연평균 성장률(CAGR) 7.39%를 기록할 전망이며, 기술적 또는 미적 제약이 있는 특수한 틈새 시장에서 LED의 대안을 찾고 있습니다. 규제에 따른 단계적 폐지로 형광등 사용이 급감하는 한편, 따뜻한 필라멘트 빛의 색감을 재현하는 새로운 LED 제품이 등장함에 따라 백열등과 할로겐등 수요는 더욱 감소했습니다. 높은 루멘이 필요한 경기장이나 장거리 조명 용도의 경우, 광학 설계, 열 관리 및 루멘 밀도의 향상에 따라 LED 시장 점유율은 지속적으로 확대되고 있습니다. OLED 및 레이저 기반 솔루션은 실외 환경에서의 비용 및 신뢰성 제약으로 인해 특정 설계 요건이나 성능 요건으로만 제한되어 있습니다.

제어 시스템이 상호 운용 가능한 프로토콜로 표준화됨에 따라, 기획자는 보고서 작성 및 최적화를 지원하는 통합된 관리 계층을 유지하면서 서로 다른 브랜드의 LED 조명 기기를 조합하여 사용할 수 있게 되었습니다. 또한, 야외 조명 시장에서는 조명 기구와 센서의 연동이 강화되어, 교통량, 재실 현황, 환경 데이터를 수집해 지자체 분석에 활용하는 움직임이 나타나고 있습니다. 현장 수리가 가능한 부품과 모듈식 드라이버 덕분에 대규모 시설 소유주는 가동 중단 시간을 단축하고 예비 부품 재고를 줄일 수 있게 되었습니다. 에너지 규제가 강화되는 가운데, 조명 기구의 효율성과 제어성은 LED 기술이 우위를 유지하는 주요 이유로 계속 남아 있을 것입니다. LED 생태계가 점차 성숙해짐에 따라, 구매자와 시스템 통합사업자 모두에게 안정적인 성능과 지원 체계가 제공되고 있습니다.

지역별 분석

2025년에는 북미가 37.85%를 차지하며 1위를 기록했습니다. 이는 연방 정부의 인센티브, 탄탄한 지방자치단체의 도입 계획, 그리고 성숙한 유통망이 안정적인 수요를 뒷받침했기 때문입니다. 로스앤젤레스는 도난 및 유지보수 지연을 해결하기 위해 최대 6만 개의 태양광 가로등을 도입하는 사상 최대 규모의 조명 투자 계획을 승인했습니다. 피츠버그는 무선 제어 및 강화된 보고 기능을 갖춘 3만 5,000개 이상의 조명 기구를 관리하기 위해 1,500만 달러를 예산에 편성했습니다. 포틀랜드시는 유권자들의 지지를 받아 조성된 기금에서 3,700만 달러를 사고 다발 구간의 LED 가로등 설치에 투입하여, 재생에너지로 전력을 공급하고 있습니다. 상업시설의 개보수에는 179D 세액 공제가 적용되며, 여러 가지 인센티브를 조합함으로써 대규모 프로젝트의 투자 회수 기간을 단축할 수 있습니다. 지역에 제조 거점을 마련함으로써 관세 위험을 줄이고, 미국 수출 제품의 물류 안정성을 확보할 수 있습니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역으로, 스마트 시티에 대한 지출, 도시로의 인구 이동, 주택 투자 확대에 힘입어 연평균 성장률(CAGR)이 8.92%에 달하고 있습니다. 하이데라바드에서 진행된 76만 개의 조명을 대상으로 한 프로그램에서는 집중 모니터링, 가동 중단 시 벌금 부과, 완벽한 자산 추적 가능성을 결합하여 서비스 수준을 철저히 관리하고 있습니다. 아시아 전역에 걸쳐 있는 제조 및 포장 거점은 경쟁 입찰에서 전 세계 프로젝트의 비용 및 양산 측면에서의 우위를 뒷받침하고 있습니다. 시장 동향 조사에 따르면, 기존 지역을 넘어 사업 기반을 확대하려는 공급업체들에게 인도, 아세안, 중동이 우선적인 진출지로 꼽히고 있습니다. 만안 지역 지자체들은 지속가능성 목표를 달성하는 동시에, 교량 및 관문 시설에 원격 관리 시스템과 다색 조명 시스템을 도입하고 있습니다. 암만 등의 도시에서는 조도 원격 제어 및 고장 보고 기능을 갖춘 스마트 LED로 수천 개의 조명을 교체하고 있습니다.

유럽에서는 에너지 효율 규제와 순환형 경제를 위한 노력이 LED 및 재제조 가능한 설계에 대한 조달을 뒷받침하며, 꾸준한 움직임이 나타나고 있습니다. 웨스트 서식스주의 4개년 계획에 따르면, 64,000개의 조명 기구를 교체하고 감시 시스템을 통합함으로써 장기적인 유지보수 및 에너지 측면에서의 이점이 기대되고 있습니다. 덴마크에서 진행 중인 인서트 방식의 개조 작업에서는 알루미늄 하우징을 재사용함으로써 에너지 소비와 제조 시 배출량을 모두 줄이고, 우수한 투자 수익률을 달성하고 있습니다. 구형 램프의 단계적 폐지에 따라, 제어 시스템 도입 준비가 완료된 상업 및 산업 분야에서의 전환이 가속화되고 있습니다. 일부 공급업체는 리드타임 단축과 관세 위험 감소를 위해 조립 공정을 현지화하고 있지만, 업스트림 부품에 대해서는 여전히 전 세계에서 조달하고 있습니다.

중동 및 아프리카(MEA) 지역에서는 선진적인 스마트시티 구축과 전기화를 촉진하는 대규모 태양광 발전 프로그램이 추진되고 있습니다. 아부다비 시 당국은 지속가능성 기준을 충족하면서 원격 관리 기능과 시민 행사를 위한 프로그래밍 가능한 색상을 갖춘 교량 조명으로 업그레이드했습니다. 오만에서는 마스캣 힐스가 LED 성능과 RF 메쉬 컨트롤러, 중앙 플랫폼을 결합하여 신뢰성을 높이고 에너지 절약을 실현했습니다. 가나에서는 수만 개의 태양광 가로등을 도입하는 프로그램을 통해 피크 부하를 줄이고 송전망에 가해지는 부담을 완화하고자 하고 있습니다. 사하라 이남 시장에서는 굴착 공사를 피하고 디젤에 대한 의존도를 줄이기 위해 Off-grid 및 하이브리드 시스템이 중시되는 추세입니다. 반면, GCC(걸프협력회의) 회원국들 시장은 전 세계의 모범 사례에서 채택된 규격 및 기준을 더욱 엄격하게 준수하고 있습니다. 남아프리카공화국의 계획 정전 문제는 현지 유지보수 체계를 갖춘 Off-grid 공공 조명에 새로운 수요를 창출하고 있습니다.

남미에서는 자금 조달과 안정성이 확보된 지역에서 도시 재개발이 진행되면서 완만한 성장이 나타나고 있습니다. 브라질의 여러 도시에서는 국가 프로그램과 다자간 차관을 활용하여 범죄율이 높은 지역에 LED 가로등 설치를 확대되고 있습니다. 칠레에서는 일조량이 풍부한 외딴 지역이나 광산 주변의 지역사회에 태양광 가로등을 도입하고 있습니다. 일부 시장에서는 거시경제의 변동으로 인해 지자체의 조달 속도가 둔화되고 있지만, 상업 지역에서는 여전히 국지적인 민간 수요가 나타나고 있습니다. 규격의 편차와 현지 조달 정책으로 인해 국경을 넘는 공급망과 사양 수립이 복잡해지고 있습니다. 야외 조명 시장에는 여전히 많은 기회가 있으며, 자금 조달이 확보된다면 안전성, 전력 비용, 신뢰성이 향상될 것으로 기대됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the outdoor lighting market size is projected to expand from USD 16.27 billion in 2025 and USD 17.32 billion in 2026 to USD 23.72 billion by 2031, registering a CAGR of 6.48% between 2026 and 2031.

This report is Segmented by Product Type (Decorative, Post, Wall, Path and Step, Deck and Patio, Garden, Security, Flood and Spot, Bollard, Others), Light Source (LED, Fluorescent, Incandescent, Halogen, Others), Installation Type (New, Retrofit), Application (Residential, Commercial), Distribution Channel (Direct B2B, Online D2C, Distributors), and Geography. Market Forecasts in Value (USD).

Global Outdoor Lighting Market Trends and Insights

Rapid Urbanization and Infrastructure Development

Cities are shifting from static grid-tied systems to modular, software-defined lighting that scales with growth and strengthens asset control. In March 2026, Los Angeles approved a two-year plan to deploy up to 60,000 solar roadway and area lights, the city's largest single lighting investment, to address a backlog of 32,000 service requests and rampant wire theft that strained maintenance budgets. Hyderabad, India authorized an INR 1,340 crore (USD 161.4 million) program to modernize 760,000 streetlights with a Centralized Control and Monitoring System, performance-based penalties, and device-level tracking to lock in uptime and accountability. Pittsburgh combined Rescue Plan funds and bond proceeds to upgrade more than 35,000 fixtures with wireless management and illuminance analytics to cut energy use and reduce light spill. These actions reflect a pragmatic path for rapidly urbanizing regions that must combine new coverage, lifecycle savings, and measurable service levels. Hong Kong Trade Development Council sentiment data highlights India, ASEAN, and the Middle East as among the most promising near-term demand pools for suppliers aligned with public-infrastructure pipelines. Concentration of LED component manufacturing in Asia continues to underpin the scaling of such projects.

Growing Demand for Energy-Efficient LED Solutions

Minimum-efficacy rules and fast paybacks make LED the default across exterior categories. New York City's 2025 Energy Conservation Code, effective March 2026, tightened lighting power density and made high-efficacy LED systems the practical path to compliance for most nonresidential interiors and exterior lighting. California's Title 24 updates in 2026 widened daylight-responsive coverage and required continuous dimming for multilevel control, pushing site and parking applications to networked LEDs with granular control. LED systems typically deliver 100-150 lumens per watt and can reduce energy use by 75-80% compared with legacy lamps, with smart controls further improving performance through scheduling, occupancy, and daylighting. A county-wide upgrade in West Sussex will convert 64,000 streetlights to LED and connect them to a remote monitoring platform, with annual savings projected at 10.7 million kWh and 1,633 tons of CO2. Retrofit programs that reuse existing housing can preserve capital while harvesting energy savings, as shown by insert-based LED upgrades that recorded 45-51% reductions at scale.

High Initial Installation and Retrofit Costs

Full smart-lighting projects can carry premium costs for controllers, gateways, and central software, stretching municipal budgets. Even straightforward conversions show the scale at play, such as a four-year West Sussex upgrade of 64,000 roadway fixtures for an estimated USD 30.7 million. Some owners offset this with policy tools and incentives, such as Portland's dedicated funding for high-crash corridors and the U.S. 179D tax deduction, which compresses paybacks for large campuses and commercial properties. Nonetheless, long payback periods on fully networked systems and grant caps that limit project size can slow adoption in cash-constrained municipalities. Residential buyers face a similar hurdle for premium outdoor packages with smart features and solar storage, which can delay uptake in price-sensitive segments. Transaction frictions also increase costs, as many cities must define interoperability requirements and vet multi-vendor control stacks before awarding contracts.

Other drivers and restraints analyzed in the detailed report include:

- Smart City Initiatives and IoT Integration

- Rising Focus on Safety and Security

- Light Pollution and Environmental Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Decorative lighting led the category with 38.82% in 2025 as hospitality, campuses, and residential settings used designer forms and finishes to extend exterior experiences. The fastest-growing deck and patio segment is advancing at 8.47% CAGR, supported by residential upgrades where layered task, ambient, and accent lighting elevate outdoor living. Post and wall lights serve as both architectural accents and pathway illumination, while HoReCa venues specify IP-rated fixtures that balance visual appeal with weather resilience. Security lighting benefits from motion-activated controls and low-glare optics that tune output to activity while maintaining visual comfort. Warm-color garden and bollard fixtures continue to win in residential projects due to comfort and curb appeal requirements for evening use.

Demand in this segment reflects the outdoor lighting market's trend toward connected, low-maintenance, and curb-appeal solutions that enhance perceived safety and property value. Institutional buyers focus on vandal resistance and compliance with accessibility requirements in pathways and steps to reduce incidents and liability. In premium applications, high-CRI options help hospitality and public spaces maintain color fidelity for facades, landscaping, and art. The outdoor lighting market is also adopting formats for faster installation and serviceability, enabling projects to close faster with fewer site disruptions. Where data points are available, designers are aligning with dark-sky principles to control uplight while preserving ambiance.

LED technology captured 68.36% of the light source mix in 2025, reflecting superior efficacy, long life, and mature price points that continue to displace legacy lamps. Other light sources posted a 7.39% CAGR through 2026-2031 outlook from a smaller base, finding roles in specialty niches where LEDs have technical or aesthetic constraints. Regulatory phase-outs have accelerated the decline of fluorescent lamps, while new LED forms that emulate warm filament tones have further reduced demand for incandescent and halogen. In high-lumen stadium and long-throw applications, LEDs continue to expand their share as optical design, thermal management, and lumen density improve. OLED and laser-based solutions remain limited to specific design or performance briefs due to cost and reliability constraints in exterior settings.

With controls standardizing on interoperable protocols, planners can mix LED luminaires across brands while maintaining unified management layers that support reporting and optimization. The outdoor lighting market is also seeing better integration between luminaires and sensors to capture traffic, occupancy, and environmental data for municipal analytics. Field-serviceable components and modular drivers are helping large owners reduce downtime and carry fewer spares. As energy codes ratchet up, fixture efficacy and controllability will remain the main reasons LED technology maintains its dominance. Continued maturity in the LED ecosystem provides both buyers and integrators with stable performance and support baselines.

Geography Analysis

North America led with 37.85% in 2025 as federal incentives, strong municipal pipelines, and mature distribution supported steady demand. Los Angeles approved the largest lighting investment in its history to deploy up to 60,000 solar streetlights that tackle theft and service backlogs. Pittsburgh set aside USD 15 million to manage more than 35,000 fixtures with wireless controls and enhanced reporting. Portland dedicated USD 37 million from a voter-backed fund specifically for LED streetlighting on high-crash corridors and powers the load with renewable energy. Commercial retrofits benefit from the 179D deduction, which has enabled large projects to pass payback hurdles through stacked incentives. Regional manufacturing footprints reduce tariff exposure and buffer logistics for United States-bound products.

Asia-Pacific is the fastest-growing region, with a 8.92% CAGR driven by smart-city spending, urban migration, and expanding residential investment. Hyderabad's 760,000-light program couples centralized monitoring, fines for downtime, and complete asset traceability to enforce service levels. Manufacturing and packaging bases across Asia underpin cost and volume advantages for global projects during competitive tenders. Market sentiment surveys identify India, ASEAN, and the Middle East as priority destinations for suppliers growing footprints beyond incumbent regions. Municipalities in the Gulf are implementing remote management and multi-color systems for bridges and gateways while meeting sustainability targets. Cities like Amman are replacing thousands of lights with smart LEDs that support remote intensity control and fault reporting.

Europe shows steady activity as energy-efficiency rules and circularity ambitions steer procurement to LEDs and remanufacturable designs. West Sussex's four-year program will replace 64,000 fixtures and integrate a monitoring system with expected long-term maintenance and energy benefits. Insert-based retrofits in Denmark reuse aluminum housings to cut both energy and embodied emissions at favorable returns. Phase-outs of legacy lamps accelerate commercial and industrial conversions that improve controls readiness. Some vendors are localizing assembly to shorten times and limit tariff exposure while upstream components remain globally sourced.

Middle East and Africa (MEA) spans advanced smart-city deployments and large-scale solar programs that improve electrification. Abu Dhabi City Municipality upgraded bridge lighting with remote management and programmable color for civic events, while meeting sustainability criteria. In Oman, Muscat Hills combined LED performance with RF mesh controllers and a central platform to improve reliability and save energy. Ghana's program to deploy tens of thousands of solar streetlights aims to reduce peak loads and relieve grid pressure. Sub-Saharan markets often emphasize off-grid and hybrid systems to avoid trenching and reduce reliance on diesel. In contrast, GCC markets align more closely with codes and standards adopted from global best practice. South Africa's load-shedding challenges are creating niches for off-grid public lighting with local maintenance capacity.

South America shows modest growth as urban retrofits progress where funding and stability allow. Brazilian cities leverage national programs and multilateral finance to expand LED streetlighting in high-crime districts. Chile integrates solar streetlights for remote and mining-adjacent communities with high solar resources. Macroeconomic volatility in some markets has slowed municipal procurement, though pockets of private demand persist in commercial districts. Fragmented standards and local-content policies complicate cross-border supply chains and specifications. The outdoor lighting market remains opportunity-rich, with safety, power costs, and reliability gains aligning with access to funding.

- Signify (Philips Lighting)

- Nichia Corporation

- Leotek

- LSI Industries

- Pemco Lighting

- Seoul Semiconductor

- Musco Lighting

- Kichler Lighting

- Volt Lighting

- Eaton Lighting (Cooper Lighting Solutions)

- RAB Lighting

- Acuity Brands

- Fagerhult Group

- LIGMAN Lighting

- Siteco GmbH

- Kenall Manufacturing

- H. E. Williams

- Kingspan Light + Air

- Cree Lighting

- ams OSRAM

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Urbanization and Infrastructure Development

- 4.2.2 Growing Demand for Energy-Efficient Led Solutions

- 4.2.3 Smart City Initiatives and Iot Integration

- 4.2.4 Rising Focus on Safety and Security

- 4.2.5 Government Support and Energy Efficiency Mandates

- 4.2.6 Declining Led Prices and Technological Advancements

- 4.3 Market Restraints

- 4.3.1 High Initial Installation and Retrofit Costs

- 4.3.2 Light Pollution and Environmental Concerns

- 4.3.3 Regulatory Compliance Pressures

- 4.3.4 Supply Chain Vulnerabilities (E.G., Raw Material Price Fluctuations)

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

- 4.8 Insights on the Regulatory Framework for Outdoor Lighting in Key Geographies

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Decorative lighting

- 5.1.2 Post lights

- 5.1.3 Wall lights

- 5.1.3.1 Hanging lights

- 5.1.3.2 Chandeliers

- 5.1.3.3 Others (flush mounts, etc.)

- 5.1.4 Path & step lights

- 5.1.5 Deck & patio lights

- 5.1.6 Garden lights

- 5.1.7 Security lighting

- 5.1.8 Flood & spotlights

- 5.1.9 Bollard

- 5.1.10 Others (rope lights, string lights, etc.)

- 5.2 By Light Source

- 5.2.1 LED

- 5.2.2 Fluorescent

- 5.2.3 Incandescent

- 5.2.4 Halogen

- 5.2.5 Other Light Sources (HID, OLED, laser, etc.)

- 5.3 By Installation Type

- 5.3.1 New Installations

- 5.3.2 Retrofit / Replacement

- 5.4 By Application

- 5.4.1 Residential

- 5.4.2 Commercial (HoReCa, Sports centers, Healthcare, Retail, Institutional, and Others (galleries/museums, corporates, etc.))

- 5.5 By Distribution Channel

- 5.5.1 Direct Sales (B2B / Tenders)

- 5.5.2 Online / D2C

- 5.5.3 Authorized Distributors & Retailers

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 Canada

- 5.6.1.2 United States

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Peru

- 5.6.2.3 Chile

- 5.6.2.4 Argentina

- 5.6.2.5 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.6.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 India

- 5.6.4.2 China

- 5.6.4.3 Japan

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 South East Asia

- 5.6.4.7 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East And Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Signify (Philips Lighting)

- 6.4.2 Nichia Corporation

- 6.4.3 Leotek

- 6.4.4 LSI Industries

- 6.4.5 Pemco Lighting

- 6.4.6 Seoul Semiconductor

- 6.4.7 Musco Lighting

- 6.4.8 Kichler Lighting

- 6.4.9 Volt Lighting

- 6.4.10 Eaton Lighting (Cooper Lighting Solutions)

- 6.4.11 RAB Lighting

- 6.4.12 Acuity Brands

- 6.4.13 Fagerhult Group

- 6.4.14 LIGMAN Lighting

- 6.4.15 Siteco GmbH

- 6.4.16 Kenall Manufacturing

- 6.4.17 H. E. Williams

- 6.4.18 Kingspan Light + Air

- 6.4.19 Cree Lighting

- 6.4.20 ams OSRAM

7 Market Opportunities & Future Outlook

- 7.1 Smart and Connected Lighting (IoT Integration)

- 7.2 Solar-Powered and Energy-Efficient LED Lighting