|

시장보고서

상품코드

2062425

양자 네트워킹 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Quantum Networking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

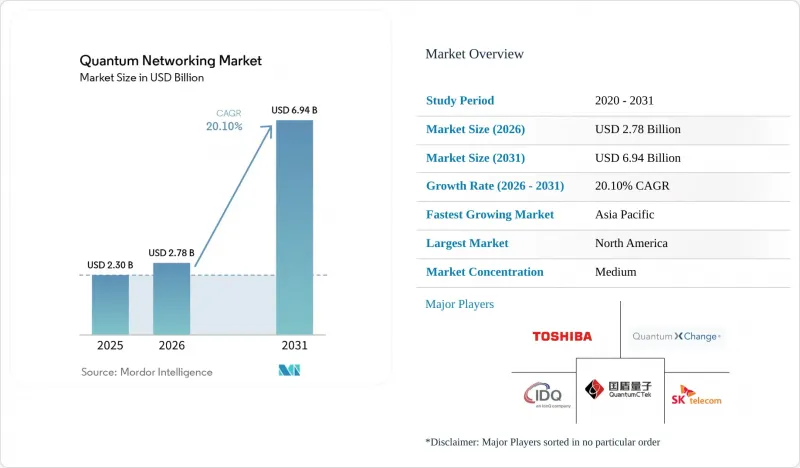

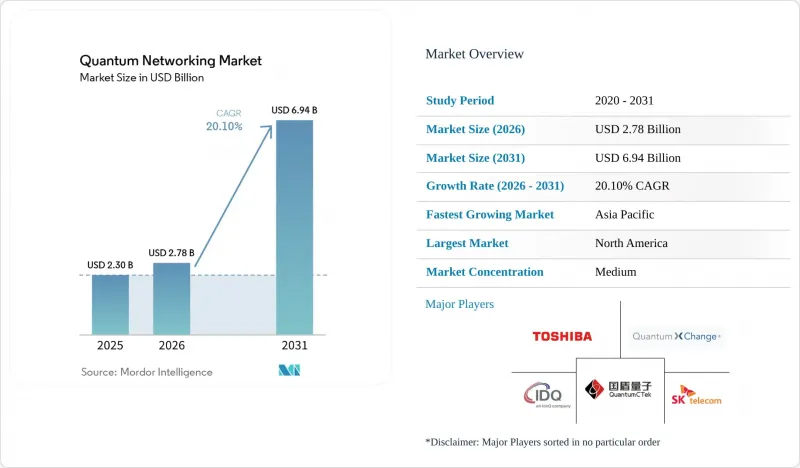

Mordor Intelligence에 의하면, 양자 네트워킹 시장 규모는 2026년 27억 8,000만 달러에서 2031년까지 69억 4,000만 달러로 확대되고 2026년부터 2031년에 걸쳐 CAGR은 20.1%를 나타낼 것으로 예측됩니다.

본 보고서는 구성 요소(하드웨어, 소프트웨어, 서비스), 용도(양자 키 배포, 보안 클라우드 통신 등), 최종 사용자(정부·국방, 대기업, 통신 및 IT, 금융 서비스 등), 네트워크 유형(지상 광섬유 네트워크, 자유 공간 광 링크 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 양자 네트워킹 시장 동향과 인사이트

양자 기술을 활용하는 적대 세력에 의한 사이버 보안 위협의 심화

국가 주체의 공격자들이 내결함성 양자 컴퓨터의 등장을 예상하여 암호화된 트래픽을 캐시하기 위해, ‘Harvest-now-decrypt-later(지금 수집하고 나중에 복호화)’ 방식의 공격이 가속화되고 있습니다. 기존의 공개 키 암호가 취약해지는 가운데, QKD는 무차별 대입 공격을 통한 복호화를 무력화시키는 증명 가능한 안전성을 갖춘 키를 제공합니다. 미국은 2024년에 포스트 양자 알고리즘을 확정했으나, 기존 시스템의 개량에는 수년이 소요되기 때문에 QKD가 즉각적인 위험 경감 효과를 가져올 기회가 생겨나고 있습니다. 중국은 2025년에 양자 백본을 요하네스버그까지 확장함으로써, 안전한 키 교환의 지정학적 중요성을 부각시켰습니다. JP모건 체이스 등 대형 은행들은 소프트웨어만 사용하는 대안에 비해 지연 시간이 18% 단축되었습니다는 점을 이유로, 이미 QKD를 통해 트레이딩 데스크를 연결하고 있습니다.

정부 자금 증가와 국가 프로그램

공적 자금은 민간 투자의 위험을 줄여줍니다. 미국 에너지부는 2025년에 전국 규모의 양자 인터넷 프로토타입 개발에 6억 2,500만 달러를 배정했습니다. 유럽의 EuroQCI는 1만 킬로미터에 달하는 국경을 넘는 네트워크에 7억 3,000만 유로(8억 2,300만 달러)를 투자하고 있습니다. 7억 5,000만 달러 규모의 인도 ‘국가 양자 미션’은 2,000킬로미터에 달하는 백본을 건설 중이며, 한편 일본의 도쿄와 오사카를 연결하는 600킬로미터 구간의 링크는 2024년에 1Mbps를 넘는 전송 속도를 달성했습니다. 이러한 연계된 프로그램은 표준 규격 준수를 가속화하고, 벤더 생태계를 활성화시킵니다.

양자 중계기 및 위성 탑재체에 대한 막대한 설비 투자

신뢰할 수 있는 노드 없이 QKD를 100킬로미터 이상으로 확장하려면 양자 리피터를 도입해야 하지만, 그 비용은 대당 약 200만-500만 달러에 달할 전망입니다. 예를 들어, 500킬로미터 길이의 메트로 루프에는 약 10대의 중계기를 설치해야 하며, 특히 예산이 제한된 개발도상 지역에서는 비용이 크게 증가합니다. 또한, QKD 구현을 위한 위성 페이로드 역시 발사 1회당 5,000만-1억 5,000만 달러라는 막대한 비용이 소요됩니다. spacenews.com의 보도에 따르면, 지상국의 광학 부품 비용은 2,000만 달러를 넘기도 하며, 이러한 상황은 더욱 악화되고 있습니다. 이러한 막대한 비용은 대규모 확산에 큰 걸림돌이 되며, 도입은 주로 풍부한 자금력을 갖춘 국가들, 혹은 선진적인 양자 통신 기술에 대한 투자를 전략적 과제로 삼아 추진하는 국가들로 한정될 것입니다.

부문별 분석

2025년 기준으로, 하드웨어는 양자 네트워킹 시장의 60.18%를 차지했습니다. 양자 난수 생성기, 단일 광자 소스, 애벌란시 포토다이오드는 안전한 통신 링크의 기반을 형성하고 있습니다. 통신 사업자들이 이러한 자산을 기반으로 한 관리형 서비스를 확대함에 따라, 서비스에 기인한 양자 네트워킹 시장 규모는 연평균 성장률(CAGR) 20.68%로 급성장할 것으로 전망됩니다. 인피니온의 극저온 대응 검출기는 통신용 파장대에서 85%의 효율을 달성하여, 실용 가능한 광섬유 전송 거리를 연장했습니다. Quantum Computing Inc.의 박막 리튬니오브산 제품 라인 등, 파운드리 시설의 병행적인 규모 확대를 통해 2027년까지 분기당 1만 개의 포토닉 회로를 출하하는 것을 목표로 하고 있습니다.

서비스 수익은 고가의 재구매 고객에 드는 비용을 수천 개에 달하는 기업용 회선을 통해 상각할 수 있는 통신 사업자들 사이에서 점차 집중되고 있습니다. Orange Business Services의 ‘Quantum Defender’는 QKD를 구독형 방식으로 제공하여, 설비 투자를 운영비로 전환하고 있습니다. 이 모델을 통해 기업은 막대한 초기 투자 없이도 양자 키 배포를 도입할 수 있게 되어, 더 다양한 기업이 이를 이용하기 쉬워졌습니다. 또한, 각 소프트웨어 벤더들은 QKD 시스템에 키 관리 오케스트레이션을 통합함으로써 제품을 강화하고, 기존 IT 인프라와의 원활한 통합을 실현하고 있습니다. 이러한 솔루션에는 레거시 시스템과의 하위 호환성을 확보하고, 미래 전망에 대한 우려를 해소하기 위해 포스트 양자 알고리즘도 포함되어 있습니다. 하드웨어의 상품화가 진행됨에 따라, 경쟁의 초점은 소프트웨어 자동화, 서비스 품질, 그리고 기업 고객의 변화하는 요구를 충족시키는 종합적이고 확장 가능한 솔루션을 제공하는 능력으로 점차 이동하고 있습니다.

2025년 기준으로 양자 키 배포는 양자 네트워킹 시장의 62.28%를 차지했으나, 분산형 양자 컴퓨팅이 가장 빠르게 성장하고 있으며, 2031년까지 연평균 성장률(CAGR)이 20.97%를 나타낼 것으로 전망됩니다. 얽힘을 통해 여러 프로세서를 연결함으로써, 단일 사이트의 한계를 넘어서는 논리 양자비트의 규모 확장이 가능해집니다. 이는 IBM이 3노드 네트워크를 활용하여 변분 고유값 솔버의 처리 속도를 40% 향상시킨 것으로 입증된 기능입니다. 각 하이퍼스케일러 기업들은 현재 QKD와 포스트 양자암호를 융합한 하이브리드 아키텍처를 시범 도입하고 있으며, 최대 100Gbps의 데이터센터 간 연결 보안을 확보하고 있습니다.

유럽의 NIS2 지침이 중요 인프라 사업자에게 양자 내성 암호화 대책의 이행을 의무화함에 따라, 안전한 클라우드 통신이 큰 주목을 받고 있습니다. 이 지침에 따라, 조직은 엄격한 규정을 준수하기 위해 안전한 데이터 전송을 최우선으로 삼아야 합니다. 양자 센서 네트워크는 여전히 틈새 시장용이지만, 고정밀 시간 동기화 및 중력 이상 감지 분야에서 보여주는 잠재력 덕분에 국방 분야에서의 관심이 높아지고 있습니다. 이러한 네트워크는 방위 능력 강화에 있어 매우 중요한 역할을 할 것으로 기대됩니다. 또한, 분산 컴퓨팅이 지속적으로 발전함에 따라 트래픽 패턴은 양자 얽힘을 활용한 백본에 대한 의존도가 점점 높아질 것으로 예측됩니다. 이러한 변화로 인해, 첨단 컴퓨팅 환경에서 안전하고 효율적인 통신을 유지하는 데 필수적인 저지연 QKD(양자 키 배분) 링크에 대한 수요가 더욱 높아질 것입니다.

지역별 분석

북미는 2025년에 매출의 50.49%를 차지했는데, 이는 막대한 벤처 자금, 엄격한 은행 규제, 그리고 미국 에너지부가 개발한 17노드 양자 인터넷 프로토타입이 주도한 결과입니다. 캐나다는 2025년, 에너지 및 통신 자산을 확보하기 위해 3억 6,000만 캐나다 달러(2억 6,700만 달러)를 투자한 반면, 멕시코는 대학 주도의 QKD 링크 시범 프로젝트를 시작했습니다. 이 지역 시장에서 주도적인 지위는 실리콘밸리, 보스턴, 토론토에 집중된 하이퍼스케일러, 방위 관련 기업, 포토닉스 분야 스타트업이 형성한 강력한 생태계에 기인합니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 20.88%를 기록하며 성장할 것으로 전망됩니다. 중국은 1만 킬로미터, 145노드로 구성된 국가 백본망을 운영하고 있으며, 자국의 기술 발전에 주력하고 있음을 보여주고 있습니다. 일본, 한국, 싱가포르는 도시 지역의 QKD 클러스터를 확대하고 있으며, 인도는 2028년까지 2,000킬로미터 규모의 양자 백본 구축에 7억 5,000만 달러를 배정했습니다. 호주는 리피터 상태의 유지 시간을 연장하기 위한 양자 메모리 연구에 자금을 지원하고 있습니다. 이 지역 내의 규격은 여전히 분열되어 있지만, 정부의 강력한 지원 덕분에 지역 전체의 확장성이 가속화되고 있습니다.

유럽은 EuroQCI가 제공하는 7억 3,000만 유로(8억 4,990만 달러)의 자금 지원과 일관된 규제 체계의 혜택을 누리고 있습니다. 도이치 텔레콤이 수행한 30킬로미터 양자 얽힘 텔레포테이션은 도시 지역에서의 적용을 입증하는 데 성공했으며, NIS2의 요건이 기업 내 도입을 뒷받침하고 있습니다. 영국, 독일, 프랑스, 이탈리아, 스페인은 2027년까지 EuroQCI 체제 하에서 상호 연결될 것으로 예상되는 국내 백본망을 구축하고 있습니다. 소규모 경제권도 이에 뒤따르고 있지만, 통신 시장의 분열로 인해 통일된 도입이 지연되고 있습니다. 중동 및 아프리카 및 남미는 출발이 늦었지만, 집중적인 진전을 보이고 있습니다. 사우디아라비아는 QKD를 활용해 해상 에너지 자산을 보호하고 있으며, UAE는 주권 데이터 링크의 시범 운영을 진행하고 있습니다. 남아프리카공화국은 국내 설비 투자 제약을 피하기 위해 중국의 베이징-요하네스버그 양자 노선에 참여했습니다. 브라질은 위성 지상국 공동 개발을 추진하고 있으며, 칠레는 광업용 양자 센싱 기술에 자금을 지원하고 있습니다. 그러나 이러한 지역에서는 예산이 제한적이기 때문에 대규모 도입이 제한되고 있습니다. 신흥 시장 전체에서는 광섬유 인프라의 한계를 극복하기 위해 허브 앤 스포크 방식의 위성 모델이 검토되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the quantum networking market size is projected to expand from USD 2.78 billion in 2026 to USD 6.94 billion by 2031, registering a CAGR of 20.1% over 2026-2031.

This report is Segmented by Component (Hardware, Software, and Services), Application (Quantum Key Distribution, Secure Cloud Communications, and More), End-User (Government and Defense, Large Enterprises, Telecom and IT, Financial Services, and More), Network Type (Terrestrial Fiber Networks, Free-Space Optical Links, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Quantum Networking Market Trends and Insights

Escalating Cybersecurity Threat from Quantum-Capable Adversaries

Harvest-now-decrypt-later campaigns are accelerating as nation-state actors cache encrypted traffic in anticipation of fault-tolerant quantum computers. With classical public-key cryptography vulnerable, QKD delivers provably secure keys that nullify brute-force decryption. The United States finalized post-quantum algorithms in 2024, yet retrofit efforts will take years, creating a window where QKD provides immediate risk mitigation.China extended its quantum backbone to Johannesburg in 2025, underscoring the geopolitical stakes of secure key exchange. Major banks such as JPMorgan Chase have already linked their trading desks via QKD, citing a 18% reduction in latency compared to software-only alternatives.

Rising Government Funding and National Programs

Public financing de-risks private investment. The U.S. Department of Energy allocated USD 625 million in 2025 for a nationwide quantum-internet prototype.Europe's EuroQCI funnels EUR 730 million (USD 823 million) into a 10,000-kilometer cross-border network. India's USD 750 million National Quantum Mission is constructing a 2,000-kilometer backbone, while Japan's 600-kilometer Tokyo-Osaka link exceeded 1 Mbps key rates in 2024.These coordinated programs accelerate alignment with standards and catalyze vendor ecosystems.

High CAPEX for Quantum Repeaters and Satellite Payloads

Extending QKD beyond 100 kilometers without trusted nodes requires deploying quantum repeaters, which cost approximately USD 2-5 million each. For instance, a 500-kilometer metro loop may require installing around 10 repeaters, significantly increasing costs, particularly in developing regions where budgets are constrained. Additionally, satellite payloads for QKD implementation add substantial expenses, ranging from USD 50-150 million per launch. This is further compounded by the cost of ground-station optics, which can exceed USD 20 million, as reported by spacenews.com. These high costs create significant barriers to large-scale rollouts, limiting adoption primarily to nations with substantial financial resources or those driven by strategic mandates to invest in advanced quantum communication technologies.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Progress in Fiber and Satellite QKD Field-Trials

- Integration Prospects with 6G Mobile Core Networks

- Lack of Global Interoperability Standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware held 60.18% quantum networking market share in 2025. Quantum random-number generators, single-photon sources, and avalanche photodiodes form the bedrock of secure links. The quantum networking market size attributable to services is projected to grow sharply, with a 20.68% CAGR, as operators wrap managed offerings around these assets. Infineon's cryogenic-ready detector reached 85% efficiency at telecom wavelengths, lengthening viable fiber spans. Parallel foundry scale-ups, such as Quantum Computing Inc.'s thin-film lithium-niobate line, aim to ship 10,000 photonic circuits per quarter by 2027.

Service revenue is consolidating among carriers that can amortize the cost of costly repeaters across thousands of enterprise circuits. Orange Business Services' Quantum Defender prices QKD as a subscription, converting capital outlays into operating expenses. This model allows enterprises to adopt quantum key distribution without significant upfront investments, making it more accessible to a broader range of businesses. Additionally, software vendors are enhancing their offerings by layering key-management orchestration on top of QKD systems, enabling seamless integration with existing IT infrastructures. These solutions are also incorporating post-quantum algorithms to ensure backward compatibility with legacy systems, addressing concerns about future-proofing. As hardware becomes increasingly commoditized, the focus of competition is shifting toward software automation, service quality, and the ability to deliver comprehensive, scalable solutions that meet the evolving needs of enterprise customers.

Quantum key distribution accounted for 62.28% of the quantum networking market in 2025, yet distributed quantum computing is the fastest riser, with a 20.97% CAGR through 2031. Linking multiple processors via entanglement scales logical qubits beyond single-site ceilings, a capability IBM proved by accelerating a variational eigensolver 40% using a three-node network. Hyperscalers now pilot hybrid architectures that blend QKD with post-quantum cryptography to secure data-center interconnects at up to 100 Gbps.

Secure cloud communications are gaining significant traction as the European NIS2 directive mandates that critical infrastructure operators implement quantum-safe encryption measures. This directive has driven organizations to prioritize secure data transmission to ensure compliance with stringent regulations. Quantum sensor networks, while still a niche application, are drawing increasing interest from the defense sector due to their potential in precision timing and gravitational anomaly detection. These networks are expected to play a pivotal role in enhancing defense capabilities. Furthermore, as distributed computing continues to evolve, traffic patterns are anticipated to increasingly rely on entanglement-enabled backbones. This shift will further amplify demand for low-latency QKD (Quantum Key Distribution) links, which are essential for maintaining secure, efficient communication in advanced computing environments.

Geography Analysis

North America captured 50.49% revenue in 2025, driven by significant venture funding, stringent banking regulations, and the U.S. Department of Energy's 17-node quantum internet prototype. Canada invested CAD 360 million (USD 267 million) in 2025 to secure energy and telecom assets, while Mexico initiated pilot projects for university-run QKD links. The region's market leadership is attributed to a strong ecosystem of hyperscalers, defense contractors, and photonics startups concentrated in Silicon Valley, Boston, and Toronto.

Asia-Pacific is projected to grow at a CAGR of 20.88% through 2031. China operates a 10,000-kilometer, 145-node national backbone, highlighting its focus on sovereign technological advancements. Japan, South Korea, and Singapore are expanding metropolitan QKD clusters, while India has allocated USD 750 million for a 2,000-kilometer quantum spine by 2028. Australia is funding quantum memory research to extend the storage time of repeater states. Although regional standards remain fragmented, strong government support is accelerating scalability across the region.

Europe benefits from EUR 730 million (USD 849.9 million) in EuroQCI funding and cohesive regulatory frameworks. Deutsche Telekom's 30-kilometer entanglement teleportation has validated urban deployments, while NIS2 mandates are driving enterprise adoption. The United Kingdom, Germany, France, Italy, and Spain are developing national backbones that are expected to interconnect under EuroQCI by 2027. Smaller economies are following suit, although fragmented telecom markets are slowing uniform adoption. The Middle East and Africa, along with South America, are trailing but showing targeted progress. Saudi Arabia is securing offshore energy assets using QKD, and the UAE is piloting sovereign data links. South Africa has joined China's Beijing-Johannesburg quantum route, bypassing domestic capital expenditure constraints. Brazil is collaborating on satellite ground stations, and Chile is funding quantum sensing for mining applications. However, limited budgets in these regions are tempering large-scale deployments. Across emerging markets, hub-and-spoke satellite models are being explored to overcome limitations in the fiber infrastructure.

- Alibaba Group Holding Limited (Alibaba Quantum Laboratory)

- Alphabet Inc. (Google Quantum AI)

- Amazon Web Services, Inc.

- Anellos Photonics Inc.

- Atos SE

- Baidu, Inc.

- BT Group plc

- China Aerospace Science and Industry Corporation Limited

- D-Wave Quantum Inc.

- Fujitsu Limited

- Huawei Technologies Co., Ltd.

- ID Quantique SA

- Infineon Technologies AG

- IonQ, Inc.

- Nokia Corporation

- Quantum Xchange, Inc.

- QuTech (Stichting Veldhoven Institute)

- Rigetti and Co, LLC

- SK Telecom Co., Ltd.

- Toshiba Digital Solutions Corporation

- Verizon Communications Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Cybersecurity Threat from Quantum-Capable Adversaries

- 4.2.2 Rising Government Funding and National Programs

- 4.2.3 Rapid Progress in Fiber and Satellite QKD Field-Trials

- 4.2.4 Integration Prospects with 6G Mobile Core Networks

- 4.2.5 Photonic Chip Foundry Scale-Ups Lowering Component Costs

- 4.2.6 Hyperscaler Push for Hybrid Quantum-Secure Cloud Interconnect

- 4.3 Market Restraints

- 4.3.1 High CAPEX for Quantum Repeaters and Satellite Payloads

- 4.3.2 Lack of Global Interoperability Standards

- 4.3.3 Fiber PMD Limits Reach without Trusted Nodes

- 4.3.4 Shortage of Cryogenic Infrastructure in Emerging Economies

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Application

- 5.2.1 Quantum Key Distribution (QKD)

- 5.2.2 Secure Cloud Communications

- 5.2.3 Distributed Quantum Computing

- 5.2.4 Quantum Sensor Networks

- 5.2.5 Other Applications

- 5.3 By End-User

- 5.3.1 Government and Defense

- 5.3.2 Large Enterprises

- 5.3.3 Telecom and IT

- 5.3.4 Financial Services

- 5.3.5 Healthcare and Life Sciences

- 5.3.6 Energy and Utilities

- 5.3.7 Research and Academia

- 5.4 By Network Type

- 5.4.1 Terrestrial Fiber Networks

- 5.4.2 Free-Space Optical Links

- 5.4.3 Satellite-Based Links

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Singapore

- 5.5.4.7 Malaysia

- 5.5.4.8 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Alibaba Group Holding Limited (Alibaba Quantum Laboratory)

- 6.4.2 Alphabet Inc. (Google Quantum AI)

- 6.4.3 Amazon Web Services, Inc.

- 6.4.4 Anellos Photonics Inc.

- 6.4.5 Atos SE

- 6.4.6 Baidu, Inc.

- 6.4.7 BT Group plc

- 6.4.8 China Aerospace Science and Industry Corporation Limited

- 6.4.9 D-Wave Quantum Inc.

- 6.4.10 Fujitsu Limited

- 6.4.11 Huawei Technologies Co., Ltd.

- 6.4.12 ID Quantique SA

- 6.4.13 Infineon Technologies AG

- 6.4.14 IonQ, Inc.

- 6.4.15 Nokia Corporation

- 6.4.16 Quantum Xchange, Inc.

- 6.4.17 QuTech (Stichting Veldhoven Institute)

- 6.4.18 Rigetti and Co, LLC

- 6.4.19 SK Telecom Co., Ltd.

- 6.4.20 Toshiba Digital Solutions Corporation

- 6.4.21 Verizon Communications Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment