|

시장보고서

상품코드

2062429

잉크젯 코더 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Inkjet Coders - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

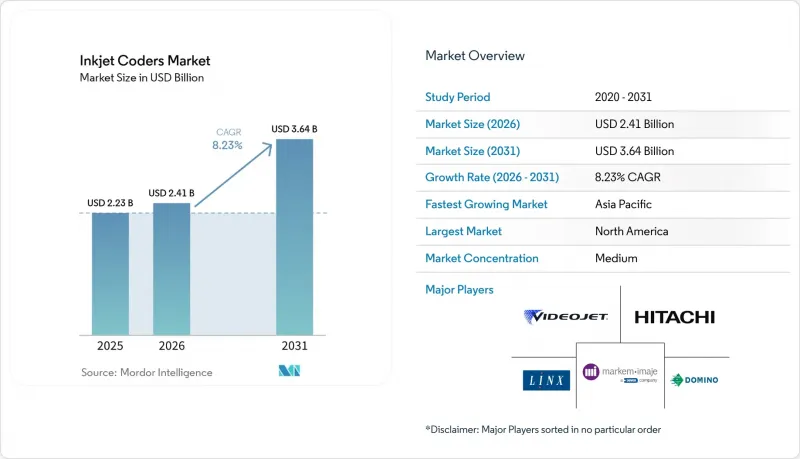

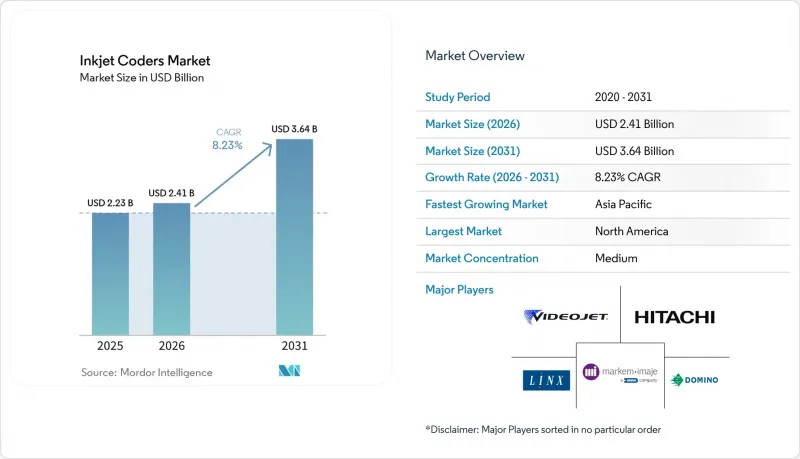

Mordor Intelligence에 의하면, 잉크젯 코더 시장 규모는 2025년 22억 3,000만 달러로 평가되었고, 2026년에는 24억 1,000만 달러로 추정되고, 2031년까지 36억 4,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 8.23%로 성장할 전망입니다.

본 보고서는 기술별(연속 잉크젯 등), 최종 이용 산업별(식품 및 음료, 의약품 및 헬스케어 등), 잉크 유형별(용제형 염료 잉크, UV 경화형 및 LED 잉크 등), 기판별(플라스틱, 종이 및 판지 등), 지역별(북미, 아시아태평양 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 잉크젯 코더 시장 동향 및 분석

엄격한 시리얼화 및 추적성 규정

미국 및 유럽연합(EU)의 의약품 공급망 관련 법률에 따라, 모든 처방약 포장에 ISO/IEC 15415 등급 1.5 이상의 데이터 매트릭스 바코드를 표기해야 하며, 제조업체들은 규정을 준수하는 고해상도 인쇄를 위해 코더를 개조하거나 교체해야 하는 상황에 직면해 있습니다. 중국의 국가의약품감독관리국과 인도의 iVEDA 수출 프로그램 역시 아시아 생산자들에게 동일한 요건을 확대 적용했으며, 2025년 10월 발효되는 사우디아라비아의 이중 언어 의무화 조치에 따라 조달 체크리스트에 다중 문자 세트 지원 기능이 추가되었습니다. 식품의 추적성 분야도 마찬가지로 발전하고 있으며, 미국 FSMA 규정 204 및 GS1의 'Sunrise 2027' 이니셔티브에 따라 고위험 식품에는 소매점에서 판독 가능한 일련번호가 부여된 2차원 코드를 표시해야 합니다. 이러한 정책들이 맞물려 의사결정 기간이 단축됨에 따라, 규정 준수 요건을 충족한 잉크젯 코더를 시장 솔루션으로 도입하는 것이 설비 투자 계획의 핵심이 되고 있습니다.

고속 FMCG 생산 라인의 보급

음료, 유제품, 스낵 식품 공장에서는 현재 분당 1,200개 속도로 가동되고 있으며, 인쇄 가능 시간은 수 분의 1초로 단축되었습니다. Markem-Imaje사의 9750 열전사 잉크젯 프린터는 2024년 시범 운영에서 시간당 12만 캔을 처리하는 성과를 거두며, 소문자 코드 인쇄 분야에서 기존 연속 잉크젯 방식에 비해 뛰어난 처리 능력을 입증했습니다. 도미노의 Gx 시리즈는 플렉서블 필름 위에서도 동일한 속도를 구현하며, 플로랩 파우치에 선명하고 대비가 높은 인쇄 품질을 보장합니다. 아시아태평양의 음료 생산 거점에서는 도입이 진행되고 있으며, 북미의 유제품 제조업체에서는 HDPE 용기 생산 라인의 개조가 이루어지고 있습니다. 리젝트 스테이션에 연결된 카메라가 모든 코드를 실시간으로 검사하여 리콜이나 벌금 부과 위험을 방지합니다.

VOC 관련 배출 규제로 인해 용제형 잉크 사용이 제한됨

캘리포니아주 대기자원국(CARB)의 상한 규제 및 EU의 REACH 규정에 따른 메틸에틸케톤, 톨루엔, 크실렌에 대한 제한으로 인해, 각 변환업체들은 용제형 잉크를 UV 경화형 또는 수성 잉크로 대체할 수밖에 없는 상황입니다. 용제형 잉크는 여전히 HDPE나 PP에 대해 뛰어난 접착력을 발휘하지만, 새로운 VOC 기준치로 인해 대기 오염 물질을 제거하고 식품 접촉 재료로의 이주에 관한 규제도 준수하는 UV-LED 기술의 도입이 가속화되고 있습니다.

부문별 분석

열전사 잉크젯 라인은 확대되는 음료 및 유제품 시장 수요를 흡수하며 해당 부문의 연평균 성장률(CAGR)을 9.9%로 끌어올렸으나, 2025년 매출의 43.2%는 여전히 연속 잉크젯 방식이 차지했습니다. 연속 잉크젯 방식의 잉크젯 코더 시장 규모는 플라스틱, 필름, 골판지 등 다양한 소재에 대응할 수 있는 비접촉 방식의 범용성 덕분에 계속해서 성장하고 있습니다. 고해상도 피에조식 드롭-온-디맨드 플랫폼은 의약품 시리얼화 분야에서 시장 점유율을 확대하고 있으며, 기존 시스템으로는 구현할 수 없는 ISO/IEC 표준 수준의 데이터 매트릭스 코드를 인쇄하고 있습니다. 밸브 제트 방식의 채택은 글자 높이가 그래픽의 정밀도보다 더 중요시되는 건축자재 및 농약 포장 분야에서 계속해서 호조를 보였습니다. 교세라의 80 mPa·s 액체를 분사할 수 있는 1,584 노즐 모델로 대표되는 고점도용 피에조 헤드의 연구 개발이 진행되고 있으며, 이를 통해 잉크젯 기술은 장식용 코팅 및 3D 성형 금형 분야로 확대될 것입니다.

스케일링에 관한 교훈은 다릅니다. 열전사 헤드는 분당 1,000개 이상의 라인 속도를 처리하는 환경에서 뛰어난 성능을 발휘하지만, 노즐의 수명과 카트리지 비용은 여전히 엄격한 검토 대상입니다. 이에 반해, 연속 잉크젯 벤더들은 자체 세척 기능이나 코드당 소모품 비용 절감과 같은 프린트 헤드 진단 기능으로 대응하며, 연포장 분야에서의 우위를 지키고 있습니다. 따라서 혼합 기술의 도입이 일반적이며, 공장은 가동 시간을 희생하지 않고도 적절한 헤드를 적절한 기판에 할당할 수 있게 되었습니다.

2025년에는 식품 및 음료 부문이 매출의 40.5%를 차지했습니다. 이는 방대한 SKU 수와 소매업체의 2차원 바코드 요구 사항이 배경에 있습니다. 이 부문은 다양한 제품 범주에 폭넓게 적용되고 있어 계속해서 지배적인 위치를 유지하고 있습니다. 그러나 의약품 및 헬스케어 분야는 전 세계적인 시리얼화 이니셔티브에 힘입어 연평균 성장률(CAGR) 9.7%라는 가장 빠른 성장세를 보이고 있습니다. 주로 식품 기업 수요에 힘입어 성장하는 잉크젯 코더 시장은 그 견고한 입지를 유지할 것으로 예측됩니다. 동시에, 주사용 바이오의약품, 프리필드 주사기, 의료기기 키트에 대한 고해상도 코딩 수요가 증가함에 따라, 수익성이 높은 판매량 확대의 기회가 창출되고 있습니다. 또한, 전자기기 제조업체들은 IPC 추적성 기준을 충족하기 위해 UV 경화형 및 레이저 하이브리드 기술을 채택하고 있으며, 자동차 및 항공우주 산업에서는 엔진 블록과 복합재 패널용으로 밸브 제트 코더를 도입하고 있습니다.

화장품 브랜드 역시, 특히 지워지지 않는 바코드 관련 규제 등 변화하는 요건에 대응하기 위해 UV-LED 잉크로의 전환을 추진하고 있습니다. 이 잉크들은 소프트 터치 라미네이트 표면을 손상시키지 않고 매끄럽게 밀착되도록 특별히 설계되어, 규정 준수를 보장하는 동시에 제품의 미관을 유지합니다. 업계 전반에서 추적 가능성과 규정 준수에 대한 중요성이 커지고 있는 것이 코딩 및 마킹 기술의 혁신을 촉진하고 있습니다. 그 결과, 각 제조업체는 이러한 수요에 부응하면서 업무 효율을 높이기 위해 첨단 솔루션에 대한 투자를 확대되고 있습니다. 이러한 추세는 업계 고유의 요구 사항을 지원하고, 엄격한 규제와 소비자의 기대가 초래하는 과제를 해결하는 데 있어 코딩 기술이 수행하는 지극히 중요한 역할을 여실히 보여주고 있습니다.

지역별 분석

북미는 DSCSA 및 FSMA 규정 204를 배경으로 2025년 매출의 33.3%를 차지했으며, 제약 및 고위험 식품 공장에서 2D 지원 프린터의 광범위한 도입을 촉진하고 있습니다. 제조업체들은 코더를 MES 및 ERP 시스템과 통합하여 가변 데이터의 자동화 및 원격 진단을 수행함으로써, 인적 오류와 인건비를 절감하고 있습니다. 캘리포니아주의 VOC 규제 강화로 인해 UV-LED로의 전환이 가속화되고 있지만, 높은 초기 투자 비용으로 인해 중소규모 가공업체들의 도입이 주저되고 있습니다.

아시아태평양은 중국의 보툴리눔툭신(보톡스) 제품 시리얼화, 인도의 GS1 QR 코드 의무화, 그리고 해당 지역 수출업체에 영향을 미치는 사우디아라비아의 이중 언어 바코드 규정에 힘입어 9.1%라는 가장 높은 연평균 성장률(CAGR)을 기록하고 있습니다. 투자 사례로는 동남아시아 시장을 대상으로 연간 700만 제곱미터를 생산하는 사토(SATO)의 1,130만 달러 규모 태국 라벨 공장을 들 수 있습니다. 청두 케리에르(Chengdu Carriere)와 같은 현지 업체들은 유럽 및 미국 브랜드보다 30-40% 저렴한 가격의 모듈형 코더를 출시하여 중소기업 시장에서 점유율을 확보하고 있습니다.

유럽에서는 '위조 의약품 지침 2단계' 및 2024년 '포장 폐기물 규정'에 따라 재사용 가능한 용기와 VOC 무함유 잉크 사용이 의무화됨에 따라 여전히 큰 수요가 유지되고 있습니다. 고급 브랜드들은 UV-LED로 업그레이드를 추진하고 있지만, 비용 효율을 중시하는 기업들은 CIJ 프린터를 에코솔벤트 잉크용으로 개조하고 있습니다. 독일, 영국, 프랑스는 인더스트리 4.0 분야의 코더 통합을 주도하고 있는 반면, 동유럽 국가들은 규정 준수 요건과 예산 제약 사이의 균형을 맞추고 있습니다. 또한, EU 기준에 부합하는 중동 및 아프리카의 시리얼화 법안과 남미 전역에서 시행이 시작된 브라질의 디지털 의약품 여권도 시장의 성장세를 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the inkjet coders market size is expected to increase from USD 2.23 billion in 2025 to USD 2.41 billion in 2026 and reach USD 3.64 billion by 2031, growing at a CAGR of 8.23% over 2026-2031.

This report is Segmented by Technology (Continuous Inkjet, and More), End-Use Industry (Food and Beverage, Pharmaceuticals and Healthcare, and More), Ink Type (Solvent-Based Dye Inks, UV-Curable and LED Inks, and More), Substrate Material (Plastics, Paper and Paperboard, and More), and Geography (North America, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Inkjet Coders Market Trends and Insights

Stringent Serialization and Traceability Regulations

Drug-supply-chain laws in the United States and the European Union now obligate every prescription pack to carry Data Matrix barcodes that pass ISO/IEC 15415 grade 1.5 or higher, pushing manufacturers to retrofit or replace coders for compliant high-resolution printing. China's National Medical Products Administration and India's iVEDA export program extended the same requirement to Asian producers, while Saudi Arabia's dual-language mandate, effective October 2025, added multi-character-set capability to procurement checklists. Food traceability is moving in parallel, as the U.S. FSMA Rule 204 and the GS1 Sunrise 2027 initiative force high-risk foods to carry serialized 2D codes readable at retail. Collectively, these policies compress decision windows, making compliance-ready inkjet coders market solutions central to capital plans.

Proliferation of High-Speed FMCG Production Lines

Beverage, dairy, and snack plants now run at 1,200 units per minute, narrowing the print window to fractions of a second. Markem-Imaje's 9750 thermal inkjet achieved 120,000 cans per hour in 2024 trials, highlighting throughput advantages over legacy continuous inkjet on small-character codes. Domino's Gx-Series meets similar speeds on flexible films, ensuring crisp, high-contrast marks on flow-wrap pouches. Asia-Pacific beverage hubs lead installations, while North American dairies retrofit HDPE jug lines. Cameras wired into reject stations verify every code in real time, safeguarding against recalls and penalties.

VOC-Related Emissions Rules Limiting Solvent-Based Inks

California Air Resources Board caps and EU REACH limits on methyl ethyl ketone, toluene, and xylene force converters to replace solvent inks with UV-curable or water-based formulations. Although solvent inks still offer superior adhesion on HDPE and PP, new VOC thresholds accelerate UV-LED adoption that eliminates airborne pollutants and aligns with food-contact migration rules.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Shift to Sustainable, Washable and Returnable Packaging

- Integration of CIJ/TIJ Heads into Industry 4.0 MES Stacks

- Capital-Expenditure Freezes in Recession-Exposed Sectors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Thermal inkjet lines captured expanding beverage and dairy demand, pushing the segment toward a 9.9% CAGR, while continuous inkjet still held 43.2% of 2025 revenue. The inkjet coders market size for continuous inkjet remains buoyed by its non-contact versatility across plastics, films and corrugate. High-resolution piezo drop-on-demand platforms gained share in pharmaceutical serialization, printing Data Matrix codes at ISO/IEC grades that legacy systems cannot match. Adoption of valve-jet units stayed strong in construction and agro-chemical packaging where character height outweighs graphic fidelity. Ongoing R&D in high-viscosity piezo heads, exemplified by Kyocera's 1,584-nozzle model able to jet 80 mPa*s fluids, will extend inkjet into decorative coatings and 3D molds.

Scaling lessons differ. Thermal heads excel where line speeds exceed 1,000 units per minute, yet nozzle lifespan and cartridge cost remain scrutinized. Continuous inkjet vendors counter with self-cleaning printhead diagnostics and lower per-code consumables, defending dominance in flexible packaging. Mixed-technology footprints are therefore common, allowing plants to allocate the right head to the right substrate without sacrificing uptime.

Food and beverage lines accounted for 40.5% of the revenue in 2025, driven by extensive SKU counts and retailer requirements for 2D barcodes. This segment remains dominant due to its broad application across various product categories. However, the pharmaceutical and healthcare sectors are experiencing the fastest growth, with a compound annual growth rate (CAGR) of 9.7%, fueled by global serialization initiatives. The inkjet coders market, primarily led by food companies, is expected to maintain its stronghold. At the same time, the increasing demand for high-resolution coding in injectable biologics, pre-filled syringes, and medical-device kits is creating opportunities for higher-margin unit volumes. Additionally, electronics manufacturers are adopting UV-curable and laser hybrid technologies to meet IPC traceability standards, while automotive and aerospace industries are integrating valve-jet coders for engine blocks and composite panels.

Cosmetics brands are also adapting to evolving requirements, particularly indelible batch-code regulations, by transitioning to UV-LED inks. These inks are specifically designed to bond seamlessly to soft-touch laminates without causing blemishes, ensuring compliance and maintaining product aesthetics. The growing emphasis on traceability and regulatory compliance across industries is driving innovation in coding and marking technologies. As a result, manufacturers are increasingly investing in advanced solutions to meet these demands while enhancing operational efficiency. This trend highlights the critical role of coding technologies in supporting industry-specific needs and addressing the challenges posed by stringent regulations and consumer expectations.

Geography Analysis

North America contributed 33.3% of 2025 revenue on the back of DSCSA and FSMA Rule 204, spurring wide deployment of 2D-capable printers in pharmaceutical and high-risk food plants. Producers integrate coders with MES and ERP suites to automate variable data and remote diagnostics, reducing manual errors and labor overhead. California's tougher VOC caps accelerate UV-LED conversions, although high capital cost tempers rollout among smaller processors.

Asia-Pacific registers the fastest 9.1% CAGR, fueled by China's botulinum-toxin serialization, India's GS1 QR mandates, and Saudi Arabia's dual-language barcode rule that impacts exporters across the region. Investments include SATO's USD 11.3 million Thai label plant that produces 7 million m2 annually to service Southeast Asia. Local vendors such as Chengdu Kelier scale modular coders priced 30-40% below Western brands, capturing share in small-to-medium enterprises.

Europe sustains sizeable demand under the Falsified Medicines Directive Phase 2 and the 2024 Packaging Waste Regulation, which require reusable containers and VOC-free inks. Premium brands upgrade to UV-LED while cost-sensitive firms retrofit CIJ with eco-solvent blends. Germany, the U.K. and France spearhead Industry 4.0 coder integration, whereas Eastern Europe balances compliance needs against budget constraints. Additional momentum stems from Middle East and African serialization laws aligned with EU standards and Brazil's digital drug passport now active across South America.

- Videojet Technologies, Inc.

- Markem-Imaje SAS

- Domino Printing Sciences plc

- Hitachi Industrial Equipment Systems Co., Ltd.

- Linx Printing Technologies Ltd.

- Control Print Limited

- REA Elektronik GmbH

- Matthews International Corporation (Matthews Marking Systems)

- Needham Ink Technologies Ltd.

- FoxJet LLC

- InkJet, Inc.

- KEYENCE Corporation

- Koenig and Bauer Coding GmbH (KBA-Metronic)

- KGK Jet India Pvt. Ltd.

- RN Mark Inc.

- Squid Ink Manufacturing Inc.

- Weber Marking Systems GmbH

- Zanasi S.r.l.

- HSA Systems A/S

- Leibinger GmbH

- EBS Ink-Jet Systeme GmbH

- ATD Ltd. (ALE)

- Guangzhou EC-JET Electronic Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent Serialization and Traceability Regulations

- 4.2.2 Proliferation of High-Speed FMCG Production Lines

- 4.2.3 Rapid Shift to Sustainable, Washable and Returnable Packaging

- 4.2.4 Integration of CIJ/TIJ Heads into Industry 4.0 MES Stacks

- 4.2.5 Adoption of UV-Curable Inks for Counterfeit Mitigation

- 4.2.6 AI-Enabled Predictive-Maintenance Algorithms for Print-Heads

- 4.3 Market Restraints

- 4.3.1 VOC-Related Emissions Rules Limiting Solvent-Based Inks

- 4.3.2 Capital-Expenditure Freezes in Recession-Exposed Sectors

- 4.3.3 Rising Competition from Laser Coders on High-Contrast Packs

- 4.3.4 Supply-Chain Bottlenecks for Piezo Print-Head Components

- 4.4 Industry Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Continuous Inkjet (CIJ)

- 5.1.2 Thermal Inkjet (TIJ)

- 5.1.3 Piezo Drop-on-Demand

- 5.1.4 Valve-Jet / Large-Character

- 5.2 By End-Use Industry

- 5.2.1 Food and Beverage

- 5.2.2 Pharmaceuticals and Healthcare

- 5.2.3 Electronics and Electrical

- 5.2.4 Automotive and Aerospace

- 5.2.5 Cosmetics and Personal Care

- 5.2.6 Chemicals and Industrial Manufacturing

- 5.3 By Ink Type

- 5.3.1 Solvent-Based Dye Inks

- 5.3.2 UV-Curable and LED Inks

- 5.3.3 Water-Based Inks

- 5.3.4 Food-Grade and Edible Inks

- 5.3.5 Pigmented and Specialty Inks

- 5.4 By Substrate Material

- 5.4.1 Plastics (HDPE, PET, PP)

- 5.4.2 Paper and Paperboard

- 5.4.3 Glass

- 5.4.4 Metals (Aluminum, Steel)

- 5.4.5 Flexible Films and Laminates

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Videojet Technologies, Inc.

- 6.4.2 Markem-Imaje SAS

- 6.4.3 Domino Printing Sciences plc

- 6.4.4 Hitachi Industrial Equipment Systems Co., Ltd.

- 6.4.5 Linx Printing Technologies Ltd.

- 6.4.6 Control Print Limited

- 6.4.7 REA Elektronik GmbH

- 6.4.8 Matthews International Corporation (Matthews Marking Systems)

- 6.4.9 Needham Ink Technologies Ltd.

- 6.4.10 FoxJet LLC

- 6.4.11 InkJet, Inc.

- 6.4.12 KEYENCE Corporation

- 6.4.13 Koenig and Bauer Coding GmbH (KBA-Metronic)

- 6.4.14 KGK Jet India Pvt. Ltd.

- 6.4.15 RN Mark Inc.

- 6.4.16 Squid Ink Manufacturing Inc.

- 6.4.17 Weber Marking Systems GmbH

- 6.4.18 Zanasi S.r.l.

- 6.4.19 HSA Systems A/S

- 6.4.20 Leibinger GmbH

- 6.4.21 EBS Ink-Jet Systeme GmbH

- 6.4.22 ATD Ltd. (ALE)

- 6.4.23 Guangzhou EC-JET Electronic Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment