|

시장보고서

상품코드

2062446

유전체 재료 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Dielectric Material - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

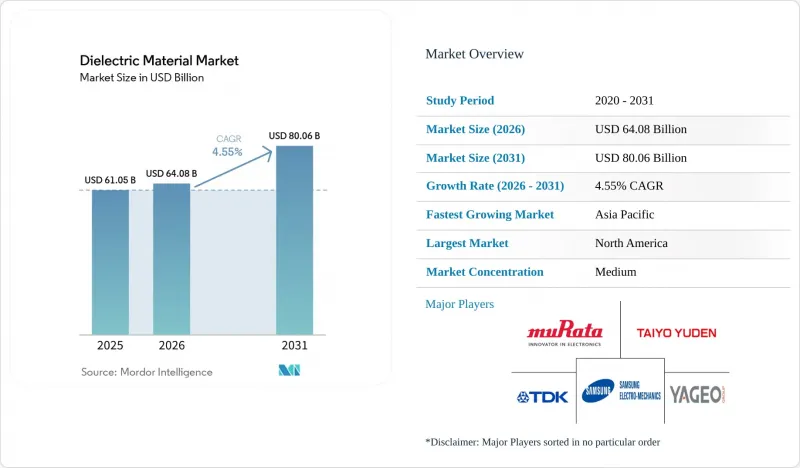

Mordor Intelligence에 의하면, 유전체 재료 시장 규모는 2025년에 610억 5,000만 달러로 평가되었고, 2026년에 640억 8,000만 달러로 추정되고, 2031년까지 800억 6,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 4.55%로 성장할 전망입니다.

본 보고서는 재료 유형별(세라믹, 폴리머 필름, 유리 및 유리 세라믹 등), 폼 팩터별(MLCC 유전체, 박막/후막 유전체 등), 유전율 범주별(Low-K, Medium-K 등), 용도별(수동 전자 부품 등), 최종 이용 산업별(소비자 가전 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 유전체 재료 시장 동향 및 인사이트

전기차의 보급이 고에너지 밀도 필름 커패시터 수요를 끌어올리고 있습니다.

800V 배터리로 전환되는 전기차 아키텍처에서는 105°C에서도 치명적인 고장이 발생하지 않으면서 900Vdc에서 5J/cm³ 이상을 축적할 수 있는 필름 커패시터가 필요합니다. 나노 알루미늄 전극으로 강화된 금속화 폴리프로필렌 권선은 이러한 기준을 충족하며, 과도적인 스파이크 발생 후 자가 복구 기능을 갖추고 있어 인버터 제조업체는 15년 보증을 자신 있게 제공할 수 있습니다. 100 kHz 이상에서 작동하는 실리콘 카바이드 스위치는 고조파 스트레스를 증가시키지만, 다층 폴리프로필렌·폴리에틸렌 필름이 열을 더 빠르게 확산시켜 인버터의 무게를 1.5 kg 줄여줍니다. 1,000회의 열충격 시험과 2,000시간의 습도 노화 시험으로 구성된 인증 주기가 현재 제품 출시 일정을 좌우하는 주요 요소가 되어, 대규모 인증이 가능한 기존 제조업체에 수주량이 집중되고 있습니다. 이에 대해 자동차 제조업체들은 수년에 걸친 공급 계약을 체결함으로써 향후 10년 동안 수요 전망을 확보하고 있습니다.

5G 및 고주파 통신 기기의 급속한 확산

24GHz를 초과하는 밀리파 무선은 기판에 대해 0.002 미만의 손실 탄젠트(tanδ)를 요구하며, 이에 따라 필터와 커플러를 단일 적층 블록으로 통합한 저온 동시 소성 알루미나·유리 복합재료가 널리 보급되고 있습니다. 각 매크로셀 무선 장비는 수백 개의 고주파 커패시터를 소비하며, 2025년까지 중국에 100만 곳 이상의 5G 기지국이 설치될 예정인 만큼, 수요를 견인하는 효과가 매우 크다고 할 수 있습니다. 온도 안정성이 뛰어난 X7R 적층체는 -55°C에서 +125°C 범위 내에서 정전용량을 ±15% 이내로 유지하며, 옥상이나 도로의 갠트리에 설치되는 실외용 및 차량용 무선기의 요구 사항을 충족합니다. 통신 사업자가 2026년에 독립형 5G 코어 네트워크로 전환함에 따라, 엣지 서버에는 100A의 리플 정격을 가진 다층 세라믹 커패시터의 대규모 뱅크가 필요하지만, 현재 이 사양을 충족할 수 있는 공급업체는 극소수에 불과합니다.

고유전율 세라믹용 희토류 원소의 가격 변동 및 공급 제한

중국의 수출 할당 조치에 따라 2024-2025년 이트륨 및 란탄 산화물의 가격이 15-25% 변동하면서, X7R 및 X8R 스택의 원자재비가 직접적으로 상승했습니다. 일본과 한국의 제조업체들은 6개월 분의 재고에 의존할 수밖에 없었으며, 이로 인해 운전자금이 묶이고, 매출총이익률이 200베이시스포인트 하락했습니다. 비스무트-나트륨 티타네이트나 칼륨-나트륨 니오브산염으로 대체할 경우 유전율이 최대 30% 저하되므로, 적층 수가 점차 증가하여 소형화에 따른 이점이 상실되고 있습니다. 지정학적 리스크를 배경으로 미국 에너지부는 국내 분리 공장에 자금을 지원하고 있으나, 2028년 이전에 상업적 규모의 생산이 시작될 가능성은 낮으며, 중기적으로는 유전체 재료 시장이 불안정한 상황이 지속될 것으로 보입니다.

부문별 분석

세라믹 등급은 유전율이 10,000을 초과하는 티타네이트 바륨 계열 소재의 장점을 바탕으로 X5R 및 X7R 규격을 충족하며, 2025년에는 유전체 재료 시장 점유율의 46.11%를 차지했습니다. 파워 일렉트로닉스 설계자들이 -40°C에서 +150°C에 이르는 온도 사이클에 대한 내열 충격성을 요구함에 따라, 유리 및 유리 세라믹 소재의 대체품 시장은 2031년까지 연평균 4.96%의 성장률을 기록하고 있습니다. 폴리머 필름은 자동차 및 태양광 발전용 인버터에서 자가 복구 기능을 통해 과열 고장을 방지함으로써, 틈새 시장인 고전압 분야를 차지하고 있습니다. 마이카와 탄탈륨 산화물은 비용보다 수명의 신뢰성이 더 중요시되는 항공우주용 레이더나 임베디드 디바이스에 여전히 특화되어 사용되고 있습니다.

바륨·스트론튬 티타네이트 박막 기술의 발전으로 5G용 가변 필터가 실현되고 있습니다. 한편, 칼륨·나트륨 니오브산 압전체는 무연화를 실현하고 있지만, 퀴리 점이 400°C라는 과제에 직면해 있습니다. 리튬-알루미늄-규산염 상을 포함하는 유리 세라믹 기판은 현재 갈륨 질화물 HEMT에 사용되고 있으며, 팽창 계수가 거의 제로이기 때문에 다이(die)에 가해지는 응력을 줄여줍니다. 폴리머 필름 공급업체는 폴리프로필렌과 폴리에틸렌 나프탈레이트를 적층하여 열전도율을 35% 향상시켰으며, 이를 통해 유전체 재료 시장은 전기차의 15년 수명을 견딜 수 있는 내구성을 실현할 가능성이 있습니다.

다층 세라믹 커패시터(MLC)는 스마트폰, 전기차(EV), 산업용 드라이브가 의존하는 타의 추종을 불허하는 부피 효율 덕분에 2025년 매출의 39.42%를 차지했습니다. 한편, 유전체 잉크 및 페이스트는 플렉서블 PET에 롤-투-롤 방식으로 안테나 및 센서를 인쇄하는 기술이 보급되면서 연평균 성장률(CAGR) 4.81%를 기록하며 급성장하고 있습니다. 알루미나 또는 AlN 위의 박막 및 두꺼운 막 코팅은 하이브리드 마이크로파 모듈에 적용되며, 한편 소결 블록을 기계 가공하여 만든 벌크 시트는 트랙션 드라이브 및 펄스 전력 연구 분야에서 여전히 중요한 역할을 하고 있습니다.

바륨 티타네이트 나노 입자와 은 플레이크를 배합한 잉크는 0.1Ω/□ 미만의 시트 저항을 실현하고 있지만, 900°C에서의 소결은 폴리머 기판의 한계에 부딪히기 때문에 포토닉 플래시 소결이 새로운 개척 분야로 떠오르고 있습니다. 신뢰성이 MLCC에 미치지 못하며, 500회의 열 사이클 후 15%의 드리프트가 발생하기 때문에 자동차 분야로의 도입이 지연되고 있습니다. 중전압 진공 차단기에서는 여전히 벌크 유리 세라믹 판이 주류를 이루고 있으며, 유전체 재료 시장에서 각 폼 팩터가 각각의 최적 용도를 계속 유지하고 있다는 점이 부각되고 있습니다.

지역별 분석

아시아태평양은 2025년에 유전체 재료 시장 점유율 47.67%를 유지한 것으로 평가되었으며, 2031년까지 연평균 성장률(CAGR) 5.22%로 성장할 것으로 전망됩니다. 일본과 한국은 월 100억 개 규모의 서브 0201 규격 생산이 가능한, 분말부터 실장까지의 일괄 생산 라인을 활용하여 수십억 개 규모의 MLCC 생산을 뒷받침하고 있습니다. 중국의 Fenghua Advanced Technology와 Torch Electron은 노동력에 대한 보조금 및 지방 자치 단체의 우대 조치를 활용하여 소비자용 부문에서 시장 점유율을 확대하고 있지만, 자동차용 등급의 품질 기준에는 아직 미치지 못하고 있습니다. 인도의 생산 연계형 인센티브 제도는 대만계 기업의 수동 부품 조립 유치를 통해, 공급 다각화로 인한 영향을 완화하는 데 기여하고 있습니다.

2025년에는 유럽과 북미의 매출이 전체의 약 35%를 차지한 것으로 평가되었습니다. 이는 독일의 800V 구동 시스템 프로젝트와, 터빈의 수명을 50년으로 예상하여 유리 세라믹 커패시터를 지정하고 있는 프랑스의 해상 풍력 발전소가 주도하고 있습니다. 브뤼셀이 주도하는 PFAS 규제로 인해 필름에서 세라믹으로의 대체가 가속화되고 있는 반면, 미국의 CHIPS법에 따른 520억 달러 규모의 지출로 인해 고유전율(High-K) 유전체 생산량이 애리조나주와 텍사스주의 신규 팹으로 집중되고 있습니다. 캐나다 서스캐처원주와 퀘벡주에서 진행 중인 희토류 탐사는 2028년 이후 이트륨에 대한 의존도를 완화할 가능성이 있지만, 단기적인 공급은 여전히 아시아를 중심으로 이루어지고 있습니다.

중동 및 아프리카 및 남미는 통신망 밀도 향상과 재생에너지 도입을 배경으로, 2025년에는 나머지 18%를 차지했습니다. 사우디아라비아의 NEOM 도시 계획에서는 광범위한 5G 구축을 위해 저손실 세라믹 커패시터의 채택이 명시되어 있으며, 아랍에미리트의 950MW 태양광 발전소에서는 스트링 인버터에 폴리프로필렌 커패시터가 채택되고 있습니다. 남아프리카공화국의 전기차 전환은 AEC-Q200 규격을 준수하는 수동 부품과 관련해 지역 유통업체와의 제휴를 촉진하고 있는 반면, 브라질의 25GW 규모 풍력 발전 설비는 현지 조립을 우대하는 15%의 수입 관세에도 불구하고, 중전압 커패시터 수요를 끌어올리고 있습니다. 아르헨티나의 리튬 붐은 배터리 팩에 대한 투자를 유치하며, 배터리 관리 및 충전 기기용 유전체 재료에 대한 하류 수요를 창출하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the dielectric material market size is projected to be USD 61.05 billion in 2025, USD 64.08 billion in 2026, and reach USD 80.06 billion by 2031, growing at a CAGR of 4.55% from 2026 to 2031.

This report is Segmented by Material Type (Ceramic, Polymer Film, Glass and Glass-Ceramics, and More), Form Factor (MLCC Dielectric, Thin/Thick Film Dielectric, and More), Dielectric Constant Category (Low-K, Medium-K, and More), Application (Passive Electronic Components, and More), End-Use Industry (Consumer Electronics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Dielectric Material Market Trends and Insights

Proliferation of Electric Vehicles Boosting Demand for High-Energy Film Capacitors

Electric-vehicle architectures moving to 800-volt batteries need film capacitors that store more than 5 J/cm3 at 900 Vdc without catastrophic failure at 105 °C. Metalized polypropylene winds enhanced with nano-aluminum electrodes meet these thresholds and self-heal after transient spikes, giving inverter makers confidence in 15-year warranties. Silicon-carbide switches that toggle above 100 kHz increase harmonic stress, prompting multilayer polypropylene-polyethylene films to spread heat faster and shave 1.5 kg from inverter weight. Qualification cycles that run 1,000 thermal shocks and 2,000 h humidity aging now dominate launch schedules and tilt volume toward incumbents that can certify at scale. Automakers have responded with multi-year allocation contracts, locking in visibility into demand through the decade.

Rapid Expansion of 5G and High-Frequency Communication Devices

Millimeter-wave radios above 24 GHz impose loss-tangent limits below 0.002 on substrates, propelling low-temperature co-fired alumina-glass composites that condense filters and couplers into a single laminated block. Each macro-cell radio consumes hundreds of high-frequency capacitors, and with over 1 million 5G sites installed in China by 2025, volume pull-through is significant. Temperature-stable X7R stacks maintain +-15% capacitance from -55 °C to +125 °C, meeting the requirements of outdoor and automotive radios deployed on rooftops and roadway gantries. As operators pivot to standalone 5G core networks in 2026, edge servers require large banks of 100 A ripple-rated multilayer ceramic capacitors, a spec only a handful of suppliers can meet today.

Volatile Prices and Limited Supply of Rare-Earth Elements for High-K Ceramics

Yttrium and lanthanum oxides swung 15-25% in price during 2024-2025 after export-quota moves in China, adding direct material inflation to X7R and X8R stacks. Japanese and South Korean producers resorted to six-month stockpiles, tying up working capital and slicing 200 bp off gross margins. Substitution with bismuth-sodium-titanate or potassium-sodium-niobate lowers permittivity by up to 30%, so layer counts creep upward, eroding miniaturization gains. Geopolitical risk has attracted U.S. Department of Energy funding for domestic separation plants, yet commercial volumes are unlikely before 2028, keeping the dielectric material market exposed in the mid-term.

Other drivers and restraints analyzed in the detailed report include:

- Miniaturization Trend in Consumer Electronics Driving Ultra-Thin MLCC Dielectrics

- Growth in Renewable Energy Installations Requiring High-Voltage Power Capacitors

- Stringent Environmental Rules on Fluorinated Polymer Dielectrics Disposal

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ceramic grades secured 46.11% of the dielectric material market share in 2025 on the strength of barium-titanate systems that pack dielectric constants above 10,000, meeting X5R and X7R codes. Glass and glass-ceramic alternatives are growing at 4.96% through 2031 as power-electronics designers seek thermal-shock tolerance for -40 °C to +150 °C cycling. Polymer films hold a niche high-voltage territory, where self-healing prevents runaway failure in automotive and solar inverters. Mica and tantalum oxide remain specialized for aerospace radar and implantable devices, where lifetime reliability eclipses cost.

Advances in barium-strontium-titanate thin films support 5G tunable filters, while potassium-sodium-niobate piezoelectrics offer lead-free compliance but face 400 °C Curie points. Glass-ceramic substrates with lithium-aluminum-silicate phases are now being used in gallium-nitride HEMTs, offering near-zero expansion that reduces die stress. Polymer-film suppliers layer polypropylene with polyethylene naphthalate to lift thermal conductivity by 35%, giving the dielectric material market size a shot at durability for 15-year electric-vehicle lifetimes.

Multilayer ceramic capacitor stacks accounted for 39.42% of 2025 revenue, thanks to unmatched volumetric efficiency that smartphones, EVs, and industrial drives rely on. Dielectric inks and pastes, however, are sprinting at a 4.81% CAGR, promoted by roll-to-roll antenna and sensor printing on flexible PET. Thin- and thick-film coatings on alumina or AlN address hybrid microwave modules, while bulk sheets machined from sintered blocks stay relevant for traction drives and pulsed-power labs.

Ink formulations blending barium-titanate nanoparticles with silver flakes hit sheet resistances below 0.1 Ω/□, yet 900 °C sinter limits polymer substrates, so photonic flash sintering is the new frontier. Reliability lags MLCCs, with 15% drift after 500 thermal cycles, delaying automotive adoption. Bulk glass-ceramic plates still dominate medium-voltage vacuum interrupters, underlining how each form factor defends its sweet spot within the dielectric material market.

Geography Analysis

Asia-Pacific retained 47.67% of the dielectric material market share in 2025 and is forecast to grow at a 5.22% CAGR through 2031. Japan and South Korea anchor multibillion-unit MLCC output, leveraging vertically integrated powder-to-placement lines capable of sub-0201 geometries at 10 billion units per month. China's Fenghua Advanced Technology and Torch Electron are buying shares in consumer-grade segments by parlaying labor subsidies and provincial incentives, though they still lag automotive-grade quality metrics. India's production-linked incentive program is attracting passive-component assembly from Taiwan-origin firms, helping cushion the impact of supply diversification.

Europe and North America combined for roughly 35% of revenue in 2025, led by Germany's 800 V drivetrain projects and France's offshore wind farms that specify glass-ceramic capacitors for 50-year turbine lives. Brussels-driven PFAS restrictions are accelerating film-to-ceramic substitution, while the United States CHIPS Act's USD 52 billion outlay is pulling high-K dielectric volume into new Arizona and Texas fabs. Canada's rare-earth exploration in Saskatchewan and Quebec could temper dependence on yttrium post-2028, yet near-term supply remains Asia-centric.

Middle East and Africa, plus South Americ, a, accounted for the remaining 18% in 2025, driven by telecom densification and renewable-energy rollouts. Saudi Arabia's NEOM city blueprint specifies low-loss ceramic nodes for pervasive 5G, and the United Arab Emirates' 950 MW solar park relies on polypropylene capacitors in string inverters. South Africa's EV shift is driving partnerships with regional distributors for AEC-Q200 passives, while Brazil's 25 GW wind fleet is boosting demand for medium-voltage capacitors despite 15% import tariffs that favor local assembly. Argentina's lithium boom is drawing battery-pack investments, creating downstream pull for dielectric materials in battery-management and charging gear.

- Murata Manufacturing Co., Ltd.

- TDK Corporation

- Taiyo Yuden Co., Ltd.

- Kyocera Corporation

- KEMET Corporation (a Yageo Company)

- Yageo Corporation

- Nippon Chemi-Con Corporation

- Samwha Electric Co., Ltd.

- Vishay Intertechnology, Inc.

- Rubicon Technology, Inc.

- Rogers Corporation

- Showa Denko Materials Co., Ltd.

- Panasonic Holdings Corporation

- Walsin Technology Corporation

- Samsung Electro-Mechanics Co., Ltd.

- Ferro Corporation

- Cangzhou Mingzhu Plastic Co., Ltd.

- Hexagon Energy Materials Limited

- Solvay S.A.

- AVX Corporation (a Kyocera Group Company)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Expansion of 5G and High-Frequency Communication Devices

- 4.2.2 Proliferation of Electric Vehicles Boosting Demand for High-Energy Film Capacitors

- 4.2.3 Growth in Renewable Energy Installations Requiring High-Voltage Power Capacitors

- 4.2.4 Miniaturization Trend in Consumer Electronics Driving Ultra-Thin MLCC Dielectrics

- 4.2.5 Emerging Use of Ferroelectric Hafnium-Oxide in Advanced Logic and Memory Chips

- 4.2.6 Rising Adoption of Wireless-Charging Furniture with Embedded Dielectric Resonators

- 4.3 Market Restraints

- 4.3.1 Volatile Prices and Limited Supply of Rare-Earth Elements for High-K Ceramics

- 4.3.2 Stringent Environmental Rules on Fluorinated Polymer Dielectrics Disposal

- 4.3.3 Reliability Issues of Additive-Manufactured Dielectric Inks

- 4.3.4 Thermal-Runaway Concerns in Solid-State Capacitor Banks

- 4.4 Industry Value-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Ceramic

- 5.1.2 Polymer Film

- 5.1.3 Glass and Glass-Ceramics

- 5.1.4 Other Material Type

- 5.2 By Form Factor

- 5.2.1 Multilayer Ceramic Chip Capacitor (MLCC) Dielectric

- 5.2.2 Thin / Thick Film Dielectric

- 5.2.3 Bulk Sheet / Plate

- 5.2.4 Dielectric Ink and Paste

- 5.3 By Dielectric Constant Category

- 5.3.1 Low-K

- 5.3.2 Medium-K

- 5.3.3 High-K

- 5.4 By Application

- 5.4.1 Passive Electronic Components, Capacitors, Resonators

- 5.4.2 Semiconductor Gate Dielectric

- 5.4.3 Power Electronics Insulation

- 5.4.4 RF and Microwave Substrates

- 5.4.5 Printed and Flexible Electronics

- 5.5 By End-Use Industry

- 5.5.1 Consumer Electronics

- 5.5.2 Automotive and E-Mobility

- 5.5.3 Energy and Power, Renewables, Grid

- 5.5.4 Telecommunications

- 5.5.5 Industrial and Manufacturing

- 5.5.6 Aerospace and Defense

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East

- 5.6.4.1 Saudi Arabia

- 5.6.4.2 United Arab Emirates

- 5.6.4.3 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Egypt

- 5.6.5.3 Rest of Africa

- 5.6.6 South America

- 5.6.6.1 Brazil

- 5.6.6.2 Argentina

- 5.6.6.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Murata Manufacturing Co., Ltd.

- 6.4.2 TDK Corporation

- 6.4.3 Taiyo Yuden Co., Ltd.

- 6.4.4 Kyocera Corporation

- 6.4.5 KEMET Corporation (a Yageo Company)

- 6.4.6 Yageo Corporation

- 6.4.7 Nippon Chemi-Con Corporation

- 6.4.8 Samwha Electric Co., Ltd.

- 6.4.9 Vishay Intertechnology, Inc.

- 6.4.10 Rubicon Technology, Inc.

- 6.4.11 Rogers Corporation

- 6.4.12 Showa Denko Materials Co., Ltd.

- 6.4.13 Panasonic Holdings Corporation

- 6.4.14 Walsin Technology Corporation

- 6.4.15 Samsung Electro-Mechanics Co., Ltd.

- 6.4.16 Ferro Corporation

- 6.4.17 Cangzhou Mingzhu Plastic Co., Ltd.

- 6.4.18 Hexagon Energy Materials Limited

- 6.4.19 Solvay S.A.

- 6.4.20 AVX Corporation (a Kyocera Group Company)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment