|

시장보고서

상품코드

2062454

플레이아웃 자동화 및 채널 인 어 박스 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Playout Automation And Channel-In-A-Box - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

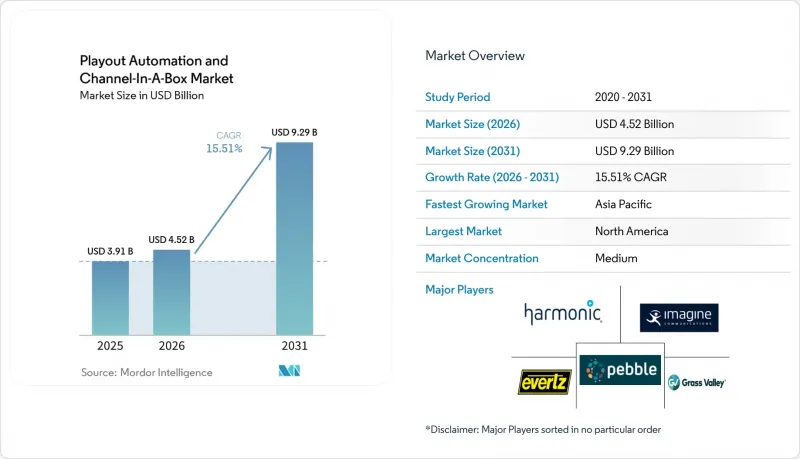

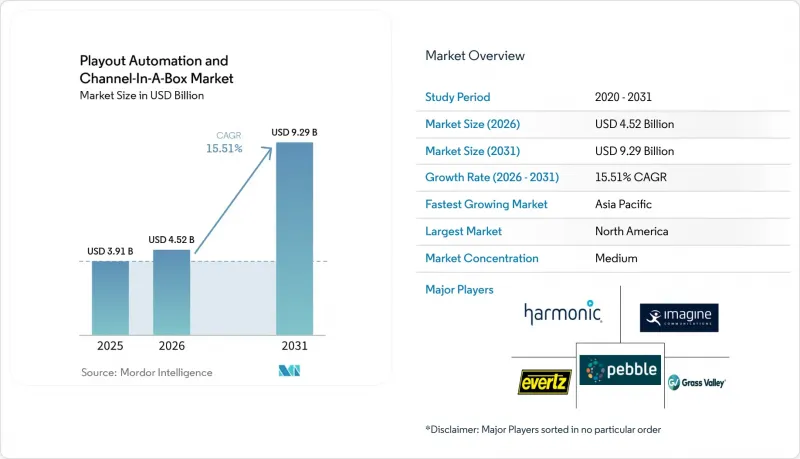

Mordor Intelligence에 의하면, 플레이아웃 자동화 및 채널 인 어 박스 시장 규모는 2025년 39억 1,000만 달러로 평가되었고, 2026년 45억 2,000만 달러로 추정되고, 2031년까지 92억 9,000만 달러로 확대될 전망이며, 2026-2031년 CAGR 15.51%를 나타낼 것으로 예측됩니다.

본 보고서는 구성 요소별(하드웨어, 소프트웨어, 서비스), 배포 모델별(온프레미스, 클라우드, 하이브리드), 최종 사용자 산업별(지상파 및 위성 방송 사업자, 케이블 네트워크 사업자, OTT/스트리밍 플랫폼 등), 채널 유형별(싱글 채널 자동화, 멀티 채널 자동화) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 플레이아웃 자동화 및 채널 인 어 박스 시장 동향과 인사이트

IP 기반 플레이아웃 인프라로의 전환

방송 사업자들은 원격 제작, 유연한 라우팅, 대규모 이벤트를 위한 클라우드 버스트 용량을 가능하게 하는 SMPTE ST 2110 IP 워크플로우를 도입하기 위해 SDI 마스터 컨트롤 룸을 폐지하고 있습니다. PBS는 170개 이상의 방송국을 연결하는 MPLS 백본 전반에 걸쳐 위성 링크를 Ateme TITAN Edge로 대체함으로써 전송 비용을 50% 절감하고, ATSC 3.0의 지역적 확산의 길을 열었습니다. BBC 월드 서비스는 Zixi 전송 기술을 탑재한 Encompass Altitude Connect를 사용하여 IP 전환을 완료함으로써, 전 세계 라디오 및 TV 파트너들에게 그 신뢰성을 입증했습니다. IP 라우팅을 통해 배선과 하드웨어는 줄어들지만, 패킷 손실 관리와 프레임 단위의 정확한 동기화는 스포츠 중계에서 여전히 중요하며, 아시아태평양의 인력 부족으로 인해 완전한 도입이 지연되고 있습니다.

OTT 및 FAST 채널의 급증

광고주들이 프로그래매틱 광고 공간으로 전환하고, 시청자들이 광고가 포함된 스트리밍을 선호하게 됨에 따라 OTT 및 FAST 사업자의 확장이 가장 빠르게 진행되고 있습니다. Amagi는 CLOUDPORT 플랫폼에서 전년 대비 21% 증가한 동영상 재생 시간을 처리했으며, 그 대부분은 FAST로 분류되는 신규 채널이었습니다. AIS PLAY는 PlayBox Neo의 ‘채널 인 어 박스(Channel-in-a-Box)’ 장치를 6대 추가함으로써 태국 리그 축구 중계 편수를 두 배로 늘렸으며, 저비용이면서 신속한 서비스 개시에 대한 지역적 수요를 여실히 드러냈습니다. 클라우드 플레이아웃을 통해 50만 달러의 하드웨어 비용을 절감하고, 시즌 한정 팝업 채널을 개설할 수도 있게 되었지만, 광고 공개에 관한 규정이 지역마다 제각각이어서 규정 준수 측면에서 복잡성이 발생하고 있습니다.

하드웨어 업그레이드에 따른 막대한 초기 설비 투자

소규모 방송사들은 50만 달러에 달하는 마스터 컨트롤 시스템 전면 개편 비용을 조달하는 데 어려움을 겪고 있으며, 이로 인해 IP 도입이 지연되면서 성장률이 2.1포인트 하락하고 있습니다. 클라우드 모델은 종량제 요금제를 채택하고 있지만, 전환을 위해서는 여전히 네트워크 업그레이드와 병행 운영 기간이 필요합니다. Sky Deutschland가 Vodafone의 케이블 전송을 IP로 전환했을 때, Sky Q 하드웨어로 셋톱박스를 교체하는 데 막대한 비용이 소요되어, 다운스트림 공정의 자본 지출에 미치는 영향이 드러났습니다.

부문별 분석

2025년 기준으로 서비스 부문은 16.11%라는 가장 높은 연평균 성장률(CAGR)을 기록한 반면, 하드웨어 부문은 플레이아웃 자동화 및 채널 인 어 박스 시장에서 45.89%라는 최대 점유율을 차지했습니다. 매니지드 플레이아웃 제공업체는 컨텐츠 제작, 인코딩, 모니터링, 전송 서비스를 통합하여 제공하기 때문에 컨텐츠 소유자는 24시간 운영되는 제어실에 인력을 배치할 필요가 없습니다. Comcast Technology Solutions는 여러 클라이언트 피드를 단일 IP 방송 운영 센터로 통합함으로써, 중앙 집중식 모니터링 체계를 통해 인력과 시설 비용을 절감하는 방법을 보여주었습니다. 데이터 주권을 엄격하게 적용하는 시장에서는 온프레미스형 어플라이언스가 로컬 스토리지 요건을 충족하기 때문에 하드웨어는 여전히 필수적입니다. 구독형 소프트웨어 유지보수는 일시적인 설비 투자를 통해 발생한 매출을 지속적인 수익으로 전환함으로써, 공급업체가 현금 흐름을 안정화하고 기능 업데이트를 지속적으로 제공할 수 있게 해줍니다. 예측 기간 동안 방송 사업자들이 인프라 유지 관리가 아닌 컨텐츠 확보에 설비 투자를 집중함에 따라, 플레이아웃 자동화 및 CiaB 시장의 서비스 규모는 확대되고 있습니다.

통합 지원 계약에 대한 수요도 서비스 수익을 끌어올리고 있으며, PlayBox Neo의 24시간 대응 ASM 및 TS 프로그램은 소프트웨어 업그레이드와 원격 문제 해결을 보장합니다. 북미와 유럽에서는 성숙한 생태계 속에서 예측 가능한 운영 비용(OPEX)이 중요시되기 때문에 도입이 확대되고 있습니다. 한편, 아시아태평양 지역과 중동에서는 하드웨어 중심의 경향이 강한 반면, 라이브 스포츠 중계의 경우 광대역 대역폭과 지연 문제가 여전히 우려 사항으로 남아 있습니다. 인제스트용 하드웨어를 현장에 설치하는 한편, 일정 관리를 클라우드 오케스트레이션에 맡기는 하이브리드형 접근 방식이 과도기의 가교 역할을 하며 부상하고 있으며, 이를 통해 벤더와의 관계를 공고히 하고 수년에 걸친 SLA 수익원을 확보하고 있습니다.

방송 사업자들이 시장 출시 기간 단축과 유연한 확장성을 우선시하는 가운데, 클라우드는 2025년에 매출의 41.36%를 차지하며 연평균 16.17%의 성장률을 기록했습니다. Amagi CLOUDPORT는 AES-128 암호화 및 역할 기반 권한 관리 기능을 갖춘 멀티 리전 중복성을 제공하여, 고객이 단 며칠 만에 전 세계적인 FAST 네트워크를 구축할 수 있도록 지원합니다. 방송 사업자가 계절 한정 팝업 방송을 송출하거나, 새로운 온프레미스 하드웨어를 도입하지 않고도 언어 버전을 추가하는 경우, 클라우드 플레이아웃 자동화 및 CiaB 시장 점유율은 확대될 것입니다. 하이브리드 모델은 일반적인 플레이아웃은 로컬에서 유지하면서, 주요 대회 기간 중에는 트래픽을 AWS나 Azure로 분산시켜 지연 시간과 확장성의 균형을 맞추기 때문에 여전히 인기를 끌고 있습니다.

주권법에 구속되는 국내 네트워크나 SDI(위성 방송 인프라)를 통한 전송에 의존하는 네트워크에서는 온프레미스 시스템이 여전히 중요한 역할을 수행하고 있습니다. Arqiva는 단일 리전의 클라우드부터 고객 소유의 테넌트 환경에 이르기까지 다양한 도입 옵션을 제공하며, 엔지니어는 지리적 장애 조치(failover)를 정밀하게 제어할 수 있습니다. 사이버 보안 위험이 클라우드에 대한 열의를 식히고 있지만, 각 벤더사는 ISO 27001 준수 및 실시간 위협 모니터링을 통해 이에 대응하고 있습니다. 인터넷 백본 용량이 향상됨에 따라 클라우드의 단위당 경제성이 강화되어, 2031년까지 온프레미스의 점유율을 넘어설 것으로 전망됩니다.

지역별 분석

북미는 2025년에 32.84%의 시장 점유율을 유지했습니다. 이는 SMPTE ST 2110의 조기 도입과 견고한 관리형 서비스 생태계에 힘입은 결과입니다. PBS가 지상파 IP 방송으로 전환함으로써 위성 통신 비용을 50% 절감할 수 있었던 점은 공영 방송사에게도 상업적 실현 가능성이 있음을 입증하고 있습니다. Comcast의 드라이 크릭 허브는 방송 및 스트리밍 브랜드의 플레이아웃을 통합 관리함으로써 규모의 경제를 여실히 보여주고 있습니다. 캐나다와 멕시코에서는 지방 지역의 대역폭 부족으로 인해 도입 속도가 더딘 편이지만, 두 나라 모두 미국에 거점을 둔 국경 간 서비스 센터를 활용하고 있습니다. ATSC 1.0과 3.0의 병렬 출력을 의무화하는 FCC 규제로 인해, 멀티 스탠다드 재생이 가능한 ‘채널 인 어 박스(Channel-in-a-Box)’형 기기에 대한 수요가 증가하고 있습니다.

아시아태평양은 16.51%라는 가장 높은 연평균 성장률(CAGR)을 기록하고 있습니다. 인도, 일본, 동남아시아에서는 지역 언어 방송을 지원하기 위해 SDI에서 IP로의 전환이 진행되고 있는 반면, OTT 사업자들은 모바일 우선 소비자를 유치하기 위해 노력하고 있습니다. Sky New Zealand의 AMPP 도입은 하이브리드 클라우드의 성장세를 뒷받침하고 있습니다. 태국의 AIS PLAY는 PlayBox Neo 기기를 통해 스포츠 채널 수를 두 배로 늘렸는데, 이는 지역 방송권 계약이 용량 확충을 주도하고 있음을 반영한 것입니다. 일본의 엄격한 ARIB UHD 규격은 하드웨어의 교체 주기를 앞당기고 있지만, 중국과 인도는 주권상의 이유로 온프레미스 장비에 의존하고 있습니다. 한국과 호주에서는 평상시에는 현지에서 플레이아웃을 진행하고, 라이브 이벤트 시에는 클라우드로 부스트함으로써 비용과 성능의 균형을 맞추고 있습니다.

유럽에서는 공공 서비스의 의무로서 보편적인 접근성이 요구되는 한편, 예산 제약으로 인해 엔지니어들이 위성 및 케이블 비용을 절감하기 위해 IP로 전환하는 움직임이 나타나고 있으며, 이에 따라 꾸준한 성장을 보이고 있습니다. BBC 월드 서비스는 유럽 전역에서 완전한 IP 전환을 완료했으며, Sky Deutschland는 Vodafone의 케이블 가입자들을 IPTV로 전환시켜 헤드엔드 비용을 절감하는 동시에 인터랙티브 기능을 추가했습니다. 스웨덴의 BoxerTV가 지상파 방송에서 철수한 것은 지상파 주파수 대역의 가치를 둘러싼 논의를 활발하게 만들었으며, 정책 입안자들이 OTT를 지원하도록 부추기고 있습니다. 남미, 중동 및 아프리카에서는 접속 환경의 격차와 수입 관세로 인해 도입이 지연되고 있지만, 매니지드 서비스 공급업체들이 설비 투자(CAPEX)를 구독료로 전환하는 운영 비용(OPEX) 모델을 통해 방송 사업자들을 유치하고 있어, 도입이 서서히 진행되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the playout automation and channel-in-a-box market size is projected to expand from USD 3.91 billion in 2025 and USD 4.52 billion in 2026 to USD 9.29 billion by 2031, registering a 15.51% CAGR between 2026 and 2031.

This report is Segmented by Component (Hardware, Software, and Services), Deployment Model (On-Premise, Cloud, and Hybrid), End-User Industry (Terrestrial and Satellite Broadcasters, Cable Network Operators, OTT/Streaming Platforms, and More), Channel Type (Single-Channel Automation, and Multi-Channel Automation), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Playout Automation And Channel-In-A-Box Market Trends and Insights

Shift Toward IP-Based Playout Infrastructure

Broadcasters are retiring SDI master-control rooms in favor of SMPTE ST 2110 IP workflows that enable remote production, flexible routing, and cloud-burst capacity for major events. PBS replaced satellite links with Ateme TITAN Edge across its MPLS backbone connecting more than 170 stations, reducing distribution cost by 50% and paving the way for ATSC 3.0 regional rollout. BBC World Service completed an IP migration using Encompass Altitude Connect with Zixi transport, proving reliability for global radio and TV partners. While IP routing trims cabling and hardware, packet loss management and frame-accurate sync remain critical for live sports, and skill shortages in Asia-Pacific delay full adoption.

Proliferation of OTT and FAST Channels

OTT and FAST operators expand quickest as advertisers pivot to programmatic inventory and viewers favor ad-supported streaming. Amagi processed 21% more video hours year over year on its CLOUDPORT platform, with most new channels classed as FAST. AIS PLAY doubled Thai League football feeds after adding six PlayBox Neo channel-in-a-box units, underscoring regional demand for low-cost rapid launch. Cloud playout eliminates USD 500 000 hardware spends and allows seasonal pop-up channels, though fragmented advertising-disclosure rules create compliance complexity across jurisdictions.

High Upfront Capital Expenditure for Hardware Refresh

Smaller broadcasters struggle to finance USD 500 000 master-control overhauls, delaying IP adoption and subtracting 2.1 percentage points from growth. Although cloud models offer pay-as-you-go pricing, migration still incurs network upgrades and dual-run periods. Sky Deutschland's shift of Vodafone cable feeds to IP required costly set-top box swaps to Sky Q hardware, demonstrating downstream capital impacts.

Other drivers and restraints analyzed in the detailed report include:

- Need for Cost-Effective Multi-Channel Operations

- Regulatory Push Toward HD and UHD Broadcasting

- Complex Integration with Legacy Automation Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services recorded the fastest 16.11% CAGR while hardware held the largest 45.89% share of the playout automation and channel-in-a-box market in 2025. Managed playout providers bundle origination, encoding, monitoring, and distribution so content owners avoid staffing 24-hour control rooms. Comcast Technology Solutions consolidated multiple client feeds into a single IP Broadcast Operations Center, illustrating how centralized oversight trims personnel and facility expense. Hardware remains critical in markets enforcing data-sovereignty, where on-premise appliances satisfy local storage mandates. Subscription-based software maintenance converts one-time capital sales into recurring revenue, letting vendors smooth cash flow and continuously push feature updates. Over the forecast period, the playout automation and channel-in-a-box market size for services is widening as broadcasters reallocate capex toward content acquisition rather than infrastructure upkeep.

Demand for integrated support contracts also lifts service revenue, with PlayBox Neo's 24-hour ASM and TS programs guaranteeing software upgrades and remote troubleshooting. North America and Europe drive adoption because mature ecosystems value predictable opex. Asia-Pacific and the Middle East lean toward hardware while wide-area bandwidth and latency remain concerns for live sports. Hybrid engagements that place ingest hardware on site but route schedules to cloud orchestration are emerging as a transitional bridge, anchoring vendor relationships and locking in multiyear SLA revenue streams.

Cloud captured 41.36% revenue in 2025, growing 16.17% annually as broadcasters prioritize time-to-market and elastic scaling. Amagi CLOUDPORT provisions multi-region redundancy with AES-128 encryption and role-based permissions, allowing clients to stand up global FAST networks in days. The playout automation and channel-in-a-box market share for cloud rises when operators spin seasonal pop-up feeds or add language variants without new on-premise hardware. Hybrid models remain popular where baseline playout stays local but surges burst to AWS or Azure during major tournaments, balancing latency and scalability.

On-premise systems stay relevant for national networks bound by sovereignty laws or reliant on SDI contribution. Arqiva offers deployment choices from single-region cloud to customer-owned tenancy, giving engineers precise control over geographic failover. Cybersecurity risk tempers cloud enthusiasm, but vendors respond with ISO 27001 compliance and real-time threat monitoring. As internet backbone capacity improves, cloud's unit economics strengthen, positioning it to eclipse on-premise share before 2031.

Geography Analysis

North America retained 32.84% market share in 2025, supported by early SMPTE ST 2110 adoption and robust managed-service ecosystems. PBS's conversion to IP terrestrial distribution cut satellite spend by 50%, proving commercial viability for public broadcasters. Comcast's Dry Creek hub centralizes playout for broadcast and streaming brands, highlighting scale economics. Canadian and Mexican uptake is slower due to rural bandwidth gaps, yet both leverage cross-border service bureaus housed in the United States. FCC rules mandating parallel ATSC 1.0 and 3.0 outputs elevate demand for channel-in-a-box appliances capable of multi-standard playout.

Asia-Pacific records the fastest 16.51% CAGR. India, Japan, and Southeast Asia replace SDI with IP to support regional language feeds, while OTT operators chase mobile-first consumers. Sky New Zealand's AMPP deployment underscores hybrid cloud momentum. Thailand's AIS PLAY doubled sports channels via PlayBox Neo appliances, reflecting how local rights deals drive incremental capacity. Japan's stringent ARIB UHD specifications quicken hardware refresh cycles, whereas China and India lean on on-premise gear for sovereignty reasons. South Korea and Australia run baseline playout locally then burst to cloud during live events, balancing cost and performance.

Europe demonstrates steady growth as public-service mandates require universal access yet budgets push engineers toward IP to curtail satellite and cable costs. BBC World Service completed a full IP handoff across the continent, and Sky Deutschland shifted Vodafone cable customers to IPTV, reducing head-end fees while adding interactive features. Sweden's BoxerTV exit from DTT catalyzes debate over terrestrial spectrum value, nudging policymakers toward OTT support. South America, the Middle East, and Africa trail due to connectivity gaps and import tariffs, but managed-service vendors entice broadcasters with opex models that convert capex into subscription fees, stimulating gradual adoption.

- Grass Valley Canada Holdings Limited

- Imagine Communications Corp.

- Harmonic Inc.

- Evertz Microsystems Ltd.

- Pebble Beach Systems Group plc

- Dalet S.A.

- PlayBox Neo Ltd.

- BroadStream Solutions Inc.

- Florical Systems, Inc.

- Aveco s.r.o.

- Cinegy GmbH

- Rohde and Schwarz GmbH and Co KG

- Ross Video Ltd.

- Amagi Corporation

- Hexaglobe SAS (SGT)

- Pixel Power Ltd.

- ENCO Systems Inc.

- Switch Media Pty Ltd.

- Logitek Electronic Systems Inc.

- Crispin Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift Toward IP-Based Playout Infrastructure

- 4.2.2 Proliferation of OTT and FAST Channels

- 4.2.3 Need for Cost-Effective Multi-Channel Operations

- 4.2.4 Regulatory Push Toward HD and UHD Broadcasting

- 4.2.5 Adoption of ML-Driven Automated QC in Playout Chains

- 4.2.6 Rising Demand for Disaster-Recovery Pop-Up Channels

- 4.3 Market Restraints

- 4.3.1 High Upfront Capital Expenditure for Hardware Refresh

- 4.3.2 Complex Integration with Legacy Automation Systems

- 4.3.3 Skill Shortage in SMPTE ST 2110 Workflows

- 4.3.4 Cybersecurity Concerns for Cloud-Based Playout

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Deployment Model

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By End-user Industry

- 5.3.1 Terrestrial and Satellite Broadcasters

- 5.3.2 Cable Network Operators

- 5.3.3 OTT / Streaming Platforms

- 5.3.4 Other End-User Inudustries

- 5.4 By Channel Type

- 5.4.1 Single-Channel Automation

- 5.4.2 Multi-Channel Automation

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Grass Valley Canada Holdings Limited

- 6.4.2 Imagine Communications Corp.

- 6.4.3 Harmonic Inc.

- 6.4.4 Evertz Microsystems Ltd.

- 6.4.5 Pebble Beach Systems Group plc

- 6.4.6 Dalet S.A.

- 6.4.7 PlayBox Neo Ltd.

- 6.4.8 BroadStream Solutions Inc.

- 6.4.9 Florical Systems, Inc.

- 6.4.10 Aveco s.r.o.

- 6.4.11 Cinegy GmbH

- 6.4.12 Rohde and Schwarz GmbH and Co KG

- 6.4.13 Ross Video Ltd.

- 6.4.14 Amagi Corporation

- 6.4.15 Hexaglobe SAS (SGT)

- 6.4.16 Pixel Power Ltd.

- 6.4.17 ENCO Systems Inc.

- 6.4.18 Switch Media Pty Ltd.

- 6.4.19 Logitek Electronic Systems Inc.

- 6.4.20 Crispin Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment