|

시장보고서

상품코드

2062482

그래핀 배터리 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Graphene Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

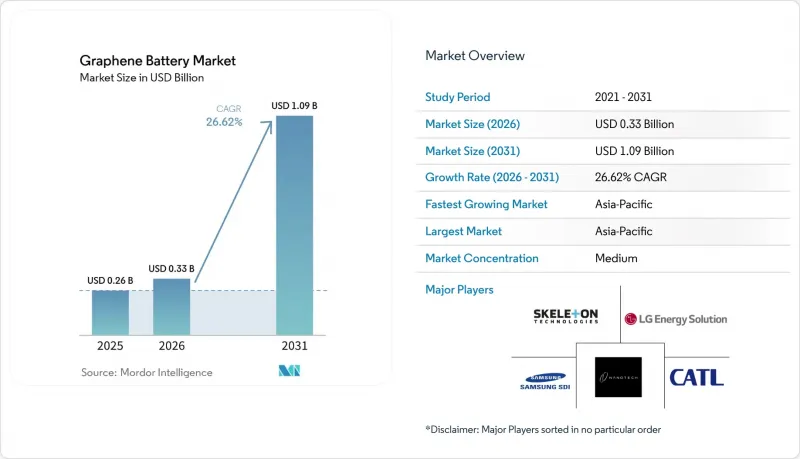

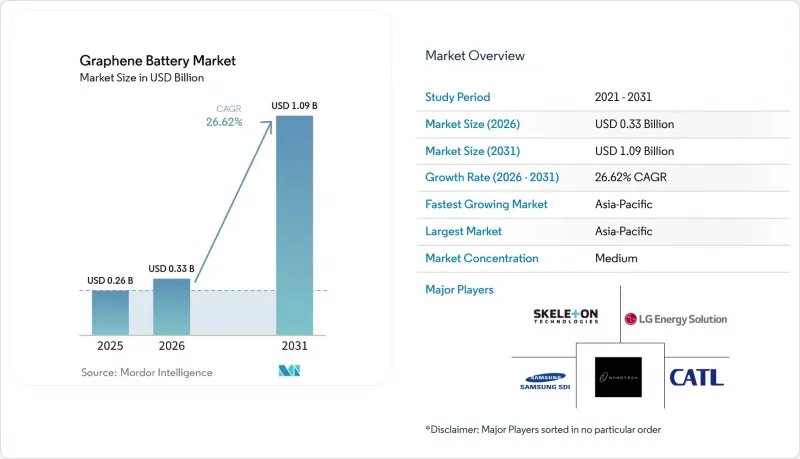

Mordor Intelligence에 의하면, 그래핀 배터리 시장 규모는 2025년에 2억 6,000만 달러로 평가되었습니다. 2026년에 3억 3,000만 달러에서 2031년까지 10억 9,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 26.62%를 나타낼 것으로 전망됩니다.

본 보고서는 유형별(리튬이온·그래핀 배터리, 그래핀 슈퍼커패시터, 납산·그래핀 배터리 등), 용도별(자동차, 가정용 전자기기, 에너지 저장, 산업용 로봇·기계 등), 지역별(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 그래핀 배터리 시장 동향 및 인사이트

전기차(EV) 주도 수요 증가

중국의 듀얼 크레딧 정책, EU의 2035년 내연기관 단계적 폐지, 캘리포니아주의 ‘Advanced Clean Cars II’ 규정 등 제로 배출 규제로 인해, 자동차 제조업체들은 20분 이내에 80%의 충전률을 달성해야 합니다. 그래핀은 전하 이동 저항을 줄여, 과열 없이 3C 이상의 전류를 흐르게 할 수 있습니다. 2026년 3월 타타 넥슨 EV 시뮬레이션 결과, 그래핀을 첨가함으로써 충전 속도가 22-27% 향상되고 셀 온도가 최대 15℃ 낮아지는 것으로 나타났습니다. 삼성의 그래핀 볼 코팅이 적용된 NCM 양극재는 4.5V에서 100회 사이클 후에도 97.3%의 용량을 유지하여, 고출력 조건에서의 내구성이 확인되었습니다. 플릿 사업자에게는 배터리 팩의 소형화와 주행 중 충전을 통해 적재 중량과 공회전 시간이 줄어든다는 이점이 있습니다. 이러한 요인들이 복합적으로 작용함에 따라, 그래핀 배터리 시장은 규제 준수 및 총소유비용(TCO) 목표 달성을 위한 단기적 실현 수단으로서의 입지를 확고히 하고 있습니다.

뛰어난 에너지 밀도와 초고속 충전

그래핀의 2,630 m²/g에 달하는 표면적과 1만 cm²/V·s를 초과하는 전하 운반체 이동도는 활물질의 충진율과 전자 수송 효율을 동시에 높여줍니다. 모나쉬 대학의 다중 스케일 환원-산화 그래핀 슈퍼커패시터는 99.5 Wh/L 및 69.2 kW/L를 달성하여, 납산 배터리에 필적하는 성능을 발휘하면서도 슈퍼커패시터 특유의 출력을 유지했습니다. 2026년 1월에 발표된, 레이저 사전 리튬화 처리를 거친 실리콘-그래핀 음극은 5 A/g의 전류 밀도에서 1,700 mAh/g을 초과했으며, 2,000회 사이클에 걸쳐 용량 저하를 2% 미만으로 억제했습니다. GMG사의 알루미늄 이온 파우치 셀은 3.2분 만에 62% 충전을 달성했으며, 6분 내 완전 충전을 목표로 하고 있어, 그래핀이 저비용으로 비리튬계 화학 시스템을 개척하는 길을 제시하고 있습니다. 이러한 획기적인 성과는 그래핀이 리튬 이온 배터리의 성능을 향상시킬 뿐만 아니라, 대체 화학 시스템을 위한 길을 열어준다는 사실을 입증하고 있습니다.

그래핀 소재의 높은 비용

고순도 그래핀은 여전히 전극 첨가제의 비용을 2배로 끌어올려, 보급형 전기차와 가정용 전자기기의 이익률을 압박하고 있습니다. CATL은 2025년에 첨단 소재를 활용한 황화물계 전고체 배터리의 비용이 기존 리튬 이온 배터리의 3-5배에 달할 것이라고 지적했습니다. 산화 그래핀이 탄소나노튜브와 동등한 비용 수준에 도달할 때까지(아마도 2028년경), 그 채택은 고급 틈새 시장에 국한될 것이며, 이는 그래핀 배터리 시장의 성장을 약 4.5포인트 억제할 것으로 보입니다.

부문별 분석

2025년 시점에서 리튬이온·그래핀 배터리는 매출 점유율의 54.1%를 차지했으며, 기존의 NCM 및 LFP 제품 라인에 1-5 중량%의 그래핀 첨가제를 단계적으로 도입하는 추세가 뚜렷합니다. 고체 전지는 아직 개발 단계에 있지만, 그래핀 코팅이 황화물 전해질을 안정화하고 덴드라이트 발생을 억제함으로써 셀 에너지 밀도를 500 Wh/kg이라는 목표치에 도달하도록 높이기 위해 연평균 성장률(CAGR) 37.0%로 시장이 확대될 것으로 전망됩니다.

그래핀 슈퍼커패시터는 그래핀 배터리 시장에서 규모는 작지만 전략적으로 중요한 위치를 차지하고 있습니다. 모나쉬 대학의 99.5 Wh/L 파우치형 전지는 체적 에너지 밀도가 납산 배터리에 필적하며, 69.2 kW/L의 출력을 실현할 수 있음을 입증했습니다. 신흥 알루미늄 이온 및 리튬-황계 화학계는 ‘기타’ 범주를 형성하고 있습니다. GMG사의 알루미늄 이온 파우치 전지는 6분 만에 충전이 가능하며, Lyten사의 3D 그래핀 리튬-황 양극재는 2024년에 자동차용 시험용으로 출하되었습니다. 통합 기술이 성숙해짐에 따라, 이러한 대체 화학 계열의 그래핀 배터리 시장 규모는 확대될 것이며, 기존의 리튬 이온 배터리를 뛰어넘는 다양한 수익원을 창출할 것으로 예측됩니다.

지역별 분석

아시아·태평양 지역은 2025년에 전 세계 수요의 44.9%를 차지했으며, 중국과 한국의 흑연 광산, 그래핀 합성, 셀 조립 거점의 집적에 힘입어 2031년까지 연평균 27.8%의 성장률을 나타낼 것으로 전망됩니다. CATL이 2027년까지 500 Wh/kg의 전고체 프로토타입을 구현하겠다는 로드맵은 현지 유력 기업이 그래핀을 활용해 성능의 한계를 비약적으로 뛰어넘은 좋은 사례입니다.

북미는 생산량 면에서는 뒤처져 있지만, 공공 자금 면에서는 앞서고 있습니다. 미국 에너지부(DOE)가 Lyten사의 리튬-황 배터리 시범 프로젝트를 지원한 것과 공군의 이산화탄소(CO2)를 흑연으로 전환하는 프로젝트는 안보 문제를 배경으로 한 공급 다각화에 대한 관심을 보여주고 있습니다. 캐나다의 NanoXplore사에 대한 초고출력 원통형 배터리 지원금은 틈새 시장에서 고부가가치를 창출하는 용도 분야에서 해당 지역의 입지를 더욱 공고히 하고 있습니다.

유럽은 GRAPHERGIA와 같은 컨소시엄에 자금을 지원함으로써 입지를 다지고 있으며, 플렉서블 슈퍼커패시터와 건식 전극 리튬 이온 배터리를 통해 기술 성숙도를 3-4에서 5로 높이는 것을 목표로 하고 있습니다. 호주 퀸즐랜드주의 프로그램은 중요 광물 자원과 부가가치가 높은 알루미늄 이온 배터리 시범 공장을 연계하고 있는 반면, 인도의 생산 연계형 인센티브 제도는 국내 그래핀 공급업체를 배터리 생산 라인에 참여시키고 있습니다. 전반적으로 그래핀 배터리 시장은 아시아 시장 규모, 북미의 국방 관련 자금, 그리고 유럽의 규제 및 연구 개발에 따른 성장 동력의 혜택을 받고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the graphene battery market size is projected to be USD 0.26 billion in 2025, USD 0.33 billion in 2026, and reach USD 1.09 billion by 2031, growing at a CAGR of 26.62% from 2026 to 2031.

This report is Segmented by Type (Lithium-Ion Graphene Batteries, Graphene Supercapacitors, Lead-Acid Graphene Batteries, and More), Application (Automotive, Consumer Electronics, Energy Storage, Industrial Robotics & Machinery, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Graphene Battery Market Trends and Insights

EV-led Demand Acceleration

Zero-emission mandates such as China's dual-credit policy, the EU's 2035 engine phase-out, and California's Advanced Clean Cars II rule are forcing automakers to meet 80% state-of-charge targets in under 20 minutes . Graphene lowers charge-transfer resistance, enabling 3C-plus currents without runaway heat. A March 2026 simulation of a Tata Nexon EV showed 22-27% faster charging and up to 15 °C lower cell temperatures when graphene was added. Samsung's graphene-ball-coated NCM cathode retained 97.3% capacity after 100 cycles at 4.5 V, confirming durability under high power . Fleet operators benefit because smaller packs or opportunity charging cut payload weight and idle time. Together, these factors position the graphene battery market as a near-term enabler for regulatory compliance and total-cost-of-ownership goals.

Superior Energy Density & Ultra-Fast Charging

Graphene's 2,630 m2/g surface area and carrier mobility above 10,000 cm2/V*s simultaneously raise active-material loading and electron transport. Monash University's multiscale reduced graphene oxide supercapacitor delivered 99.5 Wh/L and 69.2 kW/L, rivaling lead-acid while keeping supercapacitor power. A January 2026 laser-prelithiated silicon-graphene anode surpassed 1,700 mAh/g at 5 A/g with <2% fade over 2,000 cycles. GMG's aluminum-ion pouch cell hit 62% charge in 3.2 minutes and targets a full 6-minute charge, demonstrating how graphene opens non-lithium chemistries at lower cost. These milestones prove that graphene not only upgrades lithium-ion but also unlocks alternative chemistries.

High Cost of Graphene Materials

High-purity graphene still doubles electrode additive cost, squeezing margins in entry-level EVs and consumer electronics. CATL noted in 2025 that sulfide solid-state cells with advanced materials run 3-5 times the cost of conventional lithium-ion. Until reduced graphene oxide reaches parity with carbon nanotubes, likely by 2028, adoption will cluster in premium niches and curb the graphene battery market expansion by roughly 4.5 percentage points.

Other drivers and restraints analyzed in the detailed report include:

- Government R&D Funding Incentives

- Declining Graphene Production Costs

- Limited Commercial-Scale Manufacturing Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-ion graphene batteries held 54.1% revenue share in 2025, underlining the preference for incremental 1-5 wt% graphene additives in established NCM and LFP lines. Solid-state variants, though nascent, are forecast to expand at a 37.0% CAGR because graphene coatings stabilize sulfide electrolytes and suppress dendrites, raising cell energy toward 500 Wh/kg targets.

Graphene supercapacitors occupy a small yet strategically important corner of the graphene battery market. Monash University's 99.5 Wh/L pouch cell proves volumetric energy can rival lead-acid while delivering 69.2 kW/L power. Emerging aluminum-ion and lithium-sulfur chemistries form the "Others" bucket; GMG's aluminum-ion pouch cell charges in six minutes, and Lyten's 3D-graphene lithium-sulfur cathodes shipped for automotive tests in 2024. As integration techniques mature, the graphene battery market size for these alternative chemistries is expected to widen, offering diversified revenue streams beyond conventional lithium-ion.

Geography Analysis

Asia-Pacific generated 44.9% of global demand in 2025 and is projected to grow at 27.8% through 2031, thanks to integrated graphite mines, graphene synthesis, and cell assembly hubs in China and South Korea. CATL's roadmap toward 500 Wh/kg solid-state prototypes by 2027 exemplifies how local champions use graphene to leapfrog performance ceilings.

North America trails in volume but leads in public funding. The U.S. DOE's backing for Lyten's lithium-sulfur pilot and the Air Force's CO2-to-graphite project indicate security-driven interest in supply diversification. Canada's NanoXplore grant for ultra-high-power cylindrical cells further cements the region's role in niche, high-value applications.

Europe positions itself through consortium funding like GRAPHERGIA, aiming to lift technology readiness from 3-4 to 5 via flexible supercapacitors and dry-electrode lithium-ion cells . Australia's Queensland program links critical mineral reserves to value-added aluminum-ion pilot plants, while India's Production-Linked Incentive schemes draw domestic graphene suppliers into battery lines. Overall, the graphene battery market benefits from Asia's scale, North America's defense capital, and Europe's regulatory and R&D pull.

- Samsung SDI Co. Ltd.

- LG Energy Solution Ltd.

- Nanotech Energy Inc.

- Skeleton Technologies OU

- Contemporary Amperex Technology Ltd. (CATL)

- Panasonic Holdings Corp.

- Huawei Technologies Co., Ltd.

- Talga Group Ltd.

- NanoXplore Inc.

- Graphene Manufacturing Group Ltd.

- XG Sciences Inc.

- Lyten Inc.

- Vorbeck Materials Corp.

- Cabot Corporation

- ZEN Graphene Solutions Ltd.

- Grabat Energy S.A.

- Real Graphene USA

- Tesla Inc.

- EnGraphene Inc.

- Graphenano S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV-led demand acceleration

- 4.2.2 Superior energy density & ultra-fast charging

- 4.2.3 Government R&D funding incentives

- 4.2.4 Declining graphene production costs

- 4.2.5 Integration with solid-state battery architectures

- 4.2.6 High-power UAV & aerospace adoption

- 4.3 Market Restraints

- 4.3.1 High cost of graphene materials

- 4.3.2 Limited commercial-scale manufacturing capacity

- 4.3.3 Inconsistent quality in CVD graphene flakes

- 4.3.4 Environmental & safety concerns over nano-emissions

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Lithium-ion Graphene Batteries

- 5.1.2 Graphene Supercapacitors

- 5.1.3 Lead-acid Graphene Batteries

- 5.1.4 Solid-state Graphene Batteries

- 5.1.5 Others

- 5.2 By Application

- 5.2.1 Automotive

- 5.2.2 Consumer Electronics

- 5.2.3 Energy Storage

- 5.2.4 Industrial Robotics and Machinery

- 5.2.5 Aerospace and Defense

- 5.2.6 Others

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 NORDIC Countries

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 ASEAN Countries

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Egypt

- 5.3.5.5 Rest of Middle East and Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Samsung SDI Co. Ltd.

- 6.4.2 LG Energy Solution Ltd.

- 6.4.3 Nanotech Energy Inc.

- 6.4.4 Skeleton Technologies OU

- 6.4.5 Contemporary Amperex Technology Ltd. (CATL)

- 6.4.6 Panasonic Holdings Corp.

- 6.4.7 Huawei Technologies Co., Ltd.

- 6.4.8 Talga Group Ltd.

- 6.4.9 NanoXplore Inc.

- 6.4.10 Graphene Manufacturing Group Ltd.

- 6.4.11 XG Sciences Inc.

- 6.4.12 Lyten Inc.

- 6.4.13 Vorbeck Materials Corp.

- 6.4.14 Cabot Corporation

- 6.4.15 ZEN Graphene Solutions Ltd.

- 6.4.16 Grabat Energy S.A.

- 6.4.17 Real Graphene USA

- 6.4.18 Tesla Inc.

- 6.4.19 EnGraphene Inc.

- 6.4.20 Graphenano S.A.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment