|

시장보고서

상품코드

2063381

사료용 프로바이오틱스 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Feed Probiotics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

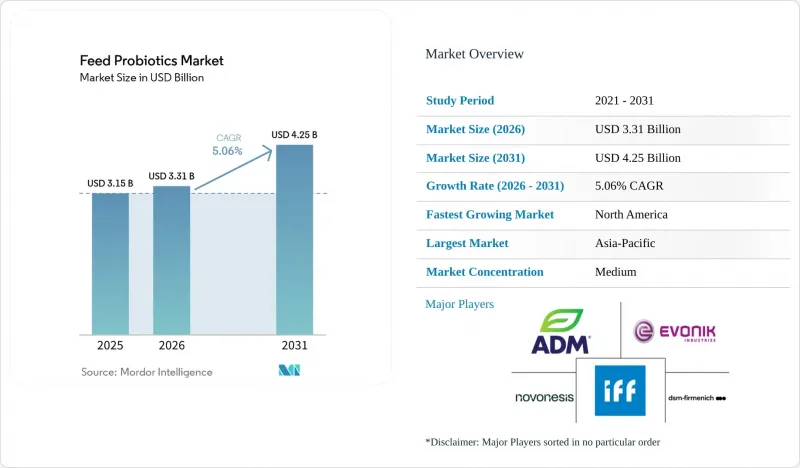

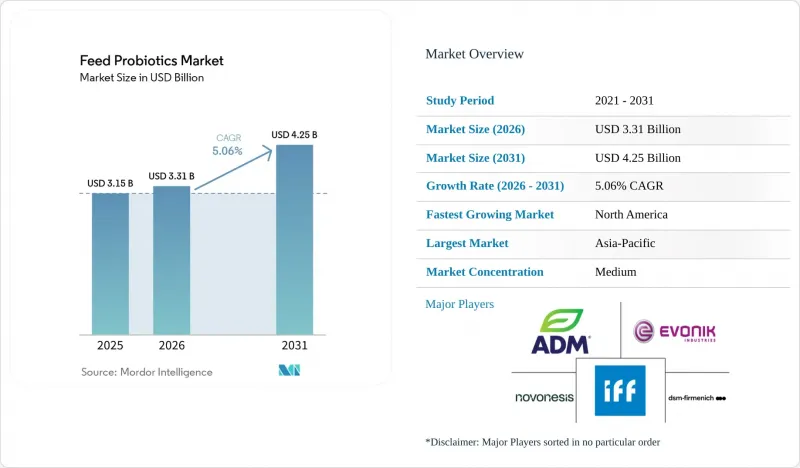

Mordor Intelligence에 의하면, 사료용 프로바이오틱스 시장 규모는 2025년에 31억 5,000만 달러로 평가되었습니다. 2026년 33억 1,000만 달러에서 2031년까지 42억 5,000만 달러로 성장하여 2026-2031년까지 연평균 복합 성장률(CAGR)은 5.06%를 나타낼 것으로 예측됩니다.

본 보고서는 부가 첨가물별(비피더스균, 엔테로코커스, 유산균, 페디오코커스, 연쇄상구균, 기타 프로바이오틱스), 동물별(수산물 양식, 가금류, 반추동물, 돼지, 기타 동물), 지역별(북미, 남미, 유럽, 아시아태평양, 중동, 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러)과 수량(톤)으로 제시되어 있습니다.

세계의 사료용 프로바이오틱스 시장 동향 및 인사이트

항생제계 성장촉진제의 규제와 항생제 미사용 생산

항생제 계열 성장 촉진제에 대한 규제로 인해 사료용 프로바이오틱스 시장 수요가 증가하고 있습니다. 이는 축산 농업 종사자들이 장내 환경의 건강과 생산성을 유지하기 위해 항생제를 대체할 수 있는 방법을 찾고 있기 때문입니다. 인도 식품안전기준청(FSSAI)은 2025년 4월 1일부터 시행되는 규정을 발표하고, 식용 동물에 대한 일부 의학적으로 중요한 항생제의 사용을 금지했습니다. 이러한 규제 변경에 따라, 대체 솔루션으로서 프로바이오틱스 기반 사료 첨가제의 도입이 촉진되고 있습니다. 바실러스속과 락토바실러스속을 기반으로 한 프로바이오틱스에 대한 수요가 증가하고 있습니다. 이러한 제품들은 항생제 계열의 성장 촉진제에 의존하지 않고 사료 효율, 소화 안정성 및 동물의 건강을 향상시키기 위한 것입니다.

가금류 생산 규모와 사료 효율에 대한 관심

육계 생산은 사료 효율과 생산의 최적화에 크게 좌우되기 때문에 가금류 생산 규모는 사료용 프로바이오틱스 시장의 꾸준한 수요를 지속적으로 견인하고 있습니다. 미국 농무부(USDA) 해외농업국(FAS)에 따르면, 전 세계 닭고기 생산량은 2026년까지 1억 1,070만 톤에 달할 것으로 예상되며, 이는 전년 대비 3% 증가한 수치입니다. 이러한 성장은 주로 중국, 브라질, 미국에서의 생산 확대에 기인한 것입니다. 이러한 수준의 가금류 생산량 증가는 장내 환경의 건강을 지원하고, 영양소 이용 효율을 높이며, 집약적인 육계 생산 시스템에서 생산 안정성을 확보해 주는 프로바이오틱스 사료 첨가제에 대한 수요를 높이고 있습니다.

현장 수준에서의 균주 성능 변동

현장 차원의 성능 편차는 사료용 프로바이오틱스 시장에 있어 중대한 과제가 되고 있습니다. 왜냐하면 프로바이오틱스의 효능은 상업적 양식 환경에 따라 크게 달라질 수 있기 때문입니다. 칠레 산티아고에 있는 칠레 대학교의 연구진들이 『Frontiers in Animal Science』지에 발표한 2025년 메타분석에 따르면, 분석 대상이 된 실험 조건 하에서 바실러스계 프로바이오틱스는 육계의 체중 증가를 평균 152g 증가시킨 반면, 락토바실러스계 프로바이오틱스는 평균 221.6g의 개선 효과를 보였습니다. 프로바이오틱스의 균주나 생산 환경에 따라 결과에 이러한 편차가 나타나는 것은 축산 농업 종사자들의 신뢰를 저해할 우려가 있으며, 그 결과 반복적인 사용이 제한되어 사료용 프로바이오틱스 제품의 보다 광범위한 상용화가 저해될 가능성이 있습니다.

부문별 분석

2025년 기준으로, 사료용 프로바이오틱스 시장에서 비피더스균의 점유율은 34.0%로 가장 높은 비중을 차지했습니다. 이러한 우위는 소화 안정성과 생후 초기 장 건강이 최우선 과제로 꼽히는 가금류, 돼지, 송아지, 수산 양식 분야의 영양 프로그램에서 비피더스균이 광범위하게 상업적으로 활용된 데 기인합니다. 각 공급업체들은 다양한 동물 모델에서 미생물학적 안정성과 사료 효율을 향상시키기 위해, 비피더스균에 유산균 및 바실러스 속 균주를 조합한 다균주 프로바이오틱스 제제의 개발을 가속화하고 있습니다. 또한, 이 카테고리는 주요 축산국에서 규제 승인이 확립되어 있는 점에 힘입어 전 세계의 통합 사료 제조업체와 대규모 동물성 단백질 생산업체들의 채택을 촉진하고 있습니다.

비피더스균을 활용한 사료용 프로바이오틱스 시장 규모는 2026년부터 2031년까지 연평균 성장률(CAGR) 5.4%라는 가장 높은 성장률을 기록하며 확대될 것으로 전망됩니다. 이러한 성장은 특히 송아지용 스타터 사료, 자돈용 육성 사료, 부화장용 영양 프로그램, 수산 양식용 사료 분야에서 어린 동물의 미생물군집 관리에 대한 관심이 높아지고 있는 데 기인합니다. 생산자들은 생산성을 저해하지 않으면서 소화 효율을 높이고 항생제 사용을 줄이는 생산 시스템을 지원하는 프로바이오틱스 솔루션에 주력하고 있습니다. 경쟁 전략은 과학적으로 검증된 균주 조합이나 상업적인 사료 가공 요건에 부합하는 내열성 제제로 점차 전환되고 있습니다. 이러한 추세에 따라 전 세계의 기존 축산업 및 신흥 수산 양식 분야에서 비피더스균을 기반으로 한 제품의 채택이 더욱 확대되고 있습니다.

지역별 분석

아시아태평양은 2025년에 32.5%를 차지하며, 사료용 프로바이오틱스 시장에서 가장 규모가 큰 지역 점유율을 기록했습니다. 이 두 가지 주요 강점은 해당 지역이 수산 양식 및 육상 가축 양식 두 부문 모두에서 우위를 유지하고 있다는 사실에서 비롯됩니다. 미국 농무부(USDA)에 따르면, 중국은 해당 지역에서 프로바이오틱스의 최대 단일 국가 수요 시장으로 자리매김하고 있으며, 이는 세계 2위의 닭고기 생산국이라는 지위에 힘입은 것입니다. 2026년의 생산량은 1,730만 톤으로 예상됩니다. 동남아시아에서는 태국, 베트남, 인도네시아, 필리핀 등의 새우 생산국에서 프로바이오틱스 수요가 집중되고 있으며, 급성 간췌장 괴사증(AHPND)에 대한 생물안전 대책의 일환으로 사료 및 양식 연못의 수질 관리에 바실러스속 및 락토바실러스속 제품이 활용되고 있습니다.

북미는 2026년부터 2031년까지 연평균 성장률(CAGR) 5.5%로 가장 높은 성장이 예상되며, 기술적으로 선진적이고 고부가가치 시장으로 평가받고 있습니다. 미국은 세계 최대의 단일 국가로서 닭고기 생산량을 자랑합니다. 이러한 성장은 대규모 상업적 축산 사업, 정밀 영양 프로그램의 광범위한 도입, 항생제 사용을 줄인 축산 시스템에 대한 수요 증가에 힘입어 이루어지고 있습니다. 미국 농무부 해외농업국에 따르면, 미국의 닭고기 생산량은 2025년 2,170만 톤에서 2026년에는 2,220만 톤으로 증가할 것으로 예상되며, 이는 가금류 생산 분야에서 프로바이오틱스 사료 첨가제의 중요한 상업적 기반이 형성될 것임을 의미합니다. 또한, 대형 사료·축산 통합 기업들은 사료 효율 향상과 장내 환경 최적화를 도모하기 위해 직접 투여형 미생물 프로그램에 대한 투자를 확대되고 있습니다.

남미, 특히 브라질과 아르헨티나에서는 수출 지향적인 가금류 및 돼지 생산 시스템을 통해 계속해서 의미 있는 상업적 수요를 창출하고 있습니다. 유럽은 수년에 걸친 항균제 감축 정책, 엄격한 사료 제조 기준, 미생물 제품에 대한 강력한 규제 감독에 힘입어 여전히 성숙한 지역으로 자리매김하고 있습니다. 한편, 중동 및 아프리카에서는 일부 국가에서 가금류 통합 사육의 확대, 수산 양식 투자, 배합 사료 생산 확대를 배경으로 사료용 프로바이오틱스의 도입이 점차 증가하고 있습니다. 이 지역의 주요 수요 시장은 사우디아라비아, 튀르키예, 남아프리카공화국, 이집트 등이며, 이들 국가의 상업적 축산 사업자들은 현대적인 집약형 축산 시스템을 뒷받침하기 위해 사료 효율, 소화 안정성, 항생제를 사용하지 않는 영양 솔루션에 주력하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 개 보고서의 내용

제3장 주요 요약과 주요 조사 결과

제4장 주요 산업 동향

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 CEO에 대한 주요 전략적 질문

KTH 26.06.26According to Mordor Intelligence, the feed probiotics market size was valued at USD 3.15 billion in 2025 and is projected to grow from USD 3.31 billion in 2026 to USD 4.25 billion by 2031, with a CAGR of 5.06% during 2026 to 2031.

This report is Segmented by Sub Additive (Bifidobacteria, Enterococcus, Lactobacilli, Pediococcus, Streptococcus, and Other Probiotics), by Animal (Aquaculture, Poultry, Ruminants, Swine, and Other Animals), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Global Feed Probiotics Market Trends and Insights

Antibiotic-Growth-Promoter Restrictions and Antibiotic-Free Production

Restrictions on antibiotic growth promoters are driving increased demand in the feed probiotics market, as livestock producers seek non-antibiotic alternatives to support gut health and production performance. The Food Safety and Standards Authority of India (FSSAI) has announced restrictions, effective April 1, 2025, banning the use of several medically important antibiotics in food-producing animals. This regulatory change is encouraging the adoption of probiotic-based feed additives as replacement solutions. The demand for Bacillus- and Lactobacillus-based probiotics is rising, as these products enhance feed efficiency, digestive stability, and animal health without relying on antibiotic growth promoters.

Poultry Production Scale and Feed Efficiency Focus

The scale of poultry production continues to drive strong demand in the feed probiotics market, as broiler operations rely heavily on feed efficiency and production optimization. According to the United States Department of Agriculture (USDA) Foreign Agricultural Service (FAS), global chicken meat production is projected to reach 110.7 million metric tons by 2026, reflecting a 3% increase from the previous year. This growth is primarily attributed to expansions in China, Brazil, and the United States. The rising poultry output at this level is increasing the demand for probiotic feed additives, which support gut health, enhance nutrient utilization, and ensure production consistency in intensive broiler systems.

Field-Level Strain Performance Variability

Field-level performance variability poses a significant challenge for the feed probiotics market, as the efficacy of probiotics can vary widely across different commercial farming environments. A 2025 meta-analysis published in Frontiers in Animal Science by researchers from Universidad de Chile, Santiago, Chile, found that Bacillus-based probiotics increased broiler body weight gain by an average of 152 g, while Lactobacillus-based probiotics demonstrated an average improvement of 221.6 g under the analyzed trial conditions. These variations in results across probiotic strains and production environments can undermine confidence among livestock producers, limiting repeat usage and impeding the broader commercialization of feed probiotic products.

Other drivers and restraints analyzed in the detailed report include:

- Asia-Pacific Livestock and Aquaculture Intensification

- Better Heat-Stable Bacillus and Dry-Format Formulations

- Multi-Jurisdiction Microbial Registration Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The feed probiotics market share for bifidobacteria held the largest 34.0% in 2025. This dominance is attributed to their extensive commercial application in poultry, swine, calf, and aquaculture nutrition programs, where digestive stability and early-life gut health are key priorities. Suppliers are increasingly developing multi-strain probiotic formulations that combine bifidobacteria with Lactobacillus and Bacillus species to enhance microbial stability and feed performance across various animal systems. Additionally, the category benefits from established regulatory acceptance in major livestock-producing countries, facilitating adoption by integrated feed manufacturers and large-scale animal protein producers globally.

The feed probiotics market size for bifidobacteria is forecast to grow at the fastest 5.4% CAGR from 2026 to 2031. This growth is driven by an increasing emphasis on microbiome management in young animals, particularly in calf starters, nursery pig diets, hatchery nutrition programs, and aquaculture feeds. Producers are focusing on probiotic solutions that enhance digestive efficiency and support antibiotic-reduced production systems without compromising productivity. Competitive strategies are shifting toward scientifically validated strain combinations and heat-stable formulations that align with commercial feed processing requirements. These developments are promoting broader adoption of bifidobacteria-based products across established livestock industries and emerging aquaculture sectors worldwide.

Geography Analysis

Asia-Pacific accounted for the largest geographic share of the feed probiotics market, holding 32.5% in 2025. This dual leadership is attributed to the region's dominance in both aquaculture and terrestrial livestock categories. According to the United States Department of Agriculture (USDA), China remains the largest single-country demand center for probiotics in the region, driven by its position as the world's second-largest chicken meat producer, forecasted at 17.3 million metric tons in 2026. In Southeast Asia, shrimp-producing nations such as Thailand, Vietnam, Indonesia, and the Philippines represent a concentrated demand for probiotics, with acute hepatopancreatic necrosis disease (AHPND) biosecurity programs driving the use of Bacillus and Lactobacillus solutions in feed and pond-water applications.

North America is projected to grow at the fastest 5.5% CAGR from 2026 to 2031 and ranks as a technically advanced and high-value market, with the United States accounting for the world's largest single-country chicken meat production. This growth is supported by large commercial livestock operations, widespread adoption of precision nutrition programs, and rising demand for antibiotic-reduced animal production systems. According to the United States Department of Agriculture Foreign Agricultural Service, United States chicken meat production is forecast to increase from 21.7 million metric tons in 2025 to 22.2 million metric tons in 2026, creating a significant commercial base for probiotic feed additives in poultry production. Additionally, large integrated feed and livestock companies are investing in direct-fed microbial programs to improve feed efficiency and optimize gut health.

South America continues to contribute meaningful commercial demand through export-oriented poultry and swine production systems, particularly in Brazil and Argentina. Europe remains a mature region supported by long-standing antimicrobial reduction policies, advanced feed manufacturing standards, and strong regulatory oversight for microbial products. Meanwhile, the Middle East and Africa are gradually increasing their adoption of feed probiotics, driven by expanding poultry integration, aquaculture investments, and compound feed production in selected countries. Key demand centers in this region include Saudi Arabia, Turkey, South Africa, and Egypt, where commercial livestock operators are focusing on feed efficiency, digestive stability, and non-antibiotic nutritional solutions to support modern intensive animal production systems.

- Novonesis A/S

- DSM-Firmenich AG

- Evonik Industries AG

- International Flavors & Fragrances Inc.

- Archer Daniels Midland Company

- Cargill, Incorporated

- Lallemand Inc.

- Kemin Industries, Inc.

- Lesaffre International, SAS

- Adisseo France SAS (China National BlueStar (Group) Co., Ltd.)

- Phibro Animal Health Corporation

- Alltech, Inc.

- Huvepharma AD

- Qingdao Vland Biotech Group Co., Ltd.

- Kerry Group plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Animal Headcount

- 4.1.1 Poultry

- 4.1.2 Ruminants

- 4.1.3 Swine

- 4.2 Feed Production

- 4.2.1 Aquaculture

- 4.2.2 Poultry

- 4.2.3 Ruminants

- 4.2.4 Swine

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 Brazil

- 4.3.3 Canada

- 4.3.4 China

- 4.3.5 France

- 4.3.6 Germany

- 4.3.7 India

- 4.3.8 Indonesia

- 4.3.9 Italy

- 4.3.10 Japan

- 4.3.11 Mexico

- 4.3.12 Netherlands

- 4.3.13 Philippines

- 4.3.14 Russia

- 4.3.15 South Africa

- 4.3.16 South Korea

- 4.3.17 Spain

- 4.3.18 Thailand

- 4.3.19 Turkey

- 4.3.20 United Kingdom

- 4.3.21 United States

- 4.3.22 Vietnam

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Antibiotic-growth-promoter restrictions and antibiotic-free production

- 4.5.2 Poultry production scale and feed efficiency focus

- 4.5.3 Asia-Pacific livestock and aquaculture intensification

- 4.5.4 Better heat-stable Bacillus and dry-format formulations

- 4.5.5 Carbon-intensity reduction and Scope 3 pressure in animal protein

- 4.5.6 Shrimp disease management and water-quality programs

- 4.6 Market Restraints

- 4.6.1 Field-level strain performance variability

- 4.6.2 Multi-jurisdiction microbial registration burden

- 4.6.3 Pelleting and storage viability losses for non-spore strains

- 4.6.4 Postbiotic and paraprobiotic substitution risk

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Sub Additive

- 5.1.1 Bifidobacteria

- 5.1.2 Enterococcus

- 5.1.3 Lactobacilli

- 5.1.4 Pediococcus

- 5.1.5 Streptococcus

- 5.1.6 Other Probiotics

- 5.2 By Animal

- 5.2.1 Aquaculture

- 5.2.1.1 Fish

- 5.2.1.2 Shrimp

- 5.2.1.3 Other Aquaculture Species

- 5.2.2 Poultry

- 5.2.2.1 Broiler

- 5.2.2.2 Layer

- 5.2.2.3 Other Poultry Birds

- 5.2.3 Ruminants

- 5.2.3.1 Beef Cattle

- 5.2.3.2 Dairy Cattle

- 5.2.3.3 Other Ruminants

- 5.2.4 Swine

- 5.2.5 Other Animals

- 5.2.1 Aquaculture

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Chile

- 5.3.2.4 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 Italy

- 5.3.3.4 Netherlands

- 5.3.3.5 Russia

- 5.3.3.6 Spain

- 5.3.3.7 United Kingdom

- 5.3.3.8 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 China

- 5.3.4.2 India

- 5.3.4.3 Japan

- 5.3.4.4 Indonesia

- 5.3.4.5 South Korea

- 5.3.4.6 Thailand

- 5.3.4.7 Vietnam

- 5.3.4.8 Australia

- 5.3.4.9 Philippines

- 5.3.4.10 Rest of Asia-Pacific

- 5.3.5 Middle East

- 5.3.5.1 Iran

- 5.3.5.2 Turkey

- 5.3.5.3 Saudi Arabia

- 5.3.5.4 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 Egypt

- 5.3.6.2 Kenya

- 5.3.6.3 South Africa

- 5.3.6.4 Rest of Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments)

- 6.4.1 Novonesis A/S

- 6.4.2 DSM-Firmenich AG

- 6.4.3 Evonik Industries AG

- 6.4.4 International Flavors & Fragrances Inc.

- 6.4.5 Archer Daniels Midland Company

- 6.4.6 Cargill, Incorporated

- 6.4.7 Lallemand Inc.

- 6.4.8 Kemin Industries, Inc.

- 6.4.9 Lesaffre International, SAS

- 6.4.10 Adisseo France SAS (China National BlueStar (Group) Co., Ltd.)

- 6.4.11 Phibro Animal Health Corporation

- 6.4.12 Alltech, Inc.

- 6.4.13 Huvepharma AD

- 6.4.14 Qingdao Vland Biotech Group Co., Ltd.

- 6.4.15 Kerry Group plc