|

시장보고서

상품코드

2063383

소매업 빅데이터 분석 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Big Data Analytics In Retail - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

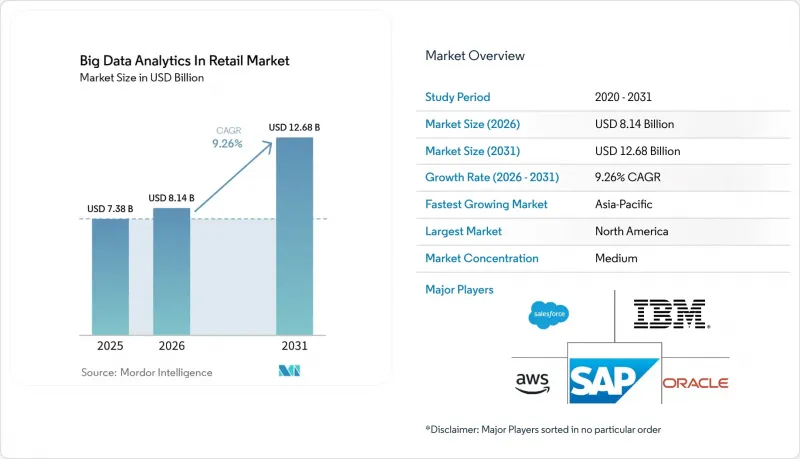

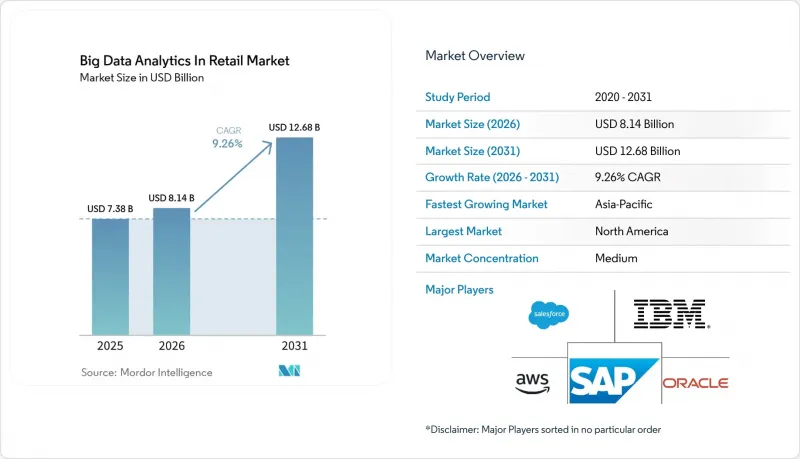

Mordor Intelligence에 의하면, 소매업 빅데이터 분석 시장 규모는 2025년에 73억 8,000만 달러로 평가되었습니다. 2026년에 81억 4,000만 달러에서 2031년까지 126억 8,000만 달러에 이를 것으로 예측되며, CAGR은 9.26%를 나타낼 전망입니다.

본 보고서는 용도(머천다이징 및 공급망 분석, 기타), 사업 형태(중소기업, 기타), 도입 형태(On-Premise 및 클라우드), 분석 유형(기술적 분석, 기타), 구성 요소(소프트웨어 및 서비스), 소매 형태(전자상거래 스토어, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 소매업 빅데이터 분석 시장 동향 및 인사이트

실시간 옴니채널 개인화의 급증

소매업체들은 클릭 스트림, POS, 모바일 앱 이벤트를 수 밀리초 이내에 수집하는 스트리밍 엔진을 탑재하여, 쇼핑객의 최신 행동을 반영한 제안 및 추천을 제공합니다. 아마존 웹 서비스(Amazon Web Services)는 2025년 기조 연설에서 이 기능을 계절적 성수기 동안 장바구니 포기율을 낮추는 데 필수적인 요소로 소개했습니다. 월마트는 미국 전역의 4,700개 매장에서 진행한 캠페인을 통해 비콘 신호와 온라인 구매 이력을 결합함으로써, 카테고리 전반에 걸친 장바구니 가치를 12% 향상시켰습니다. 이 접근 방식에서는 과소평가된 코호트가 훈련 데이터를 왜곡할 가능성이 있으므로, 엄격한 공정성 검증이 필요합니다. 이러한 위험에 대해 유럽의 인공지능법은 투명성 관련 의무를 통해 대응하고 있습니다.

소매 미디어 네트워크와 자사 데이터의 통합

사이트 내 광고 플랫폼은 노출과 장바구니 매출을 연결하는 구매 기반 타겟팅에 힘입어, 2025년에는 전 세계적으로 500억 달러의 수익을 창출했습니다. Kroger는 개인정보 보호형 클린룸 내에서 익명화된 로열티 데이터를 활용함으로써 광고주 기반을 38% 확대했습니다. 스노우플레이크와 구글 클라우드는 2026년 초에 공동 개발한 클린룸 제품을 공식 발표했으며, 원시 데이터를 공개하지 않고도 데이터셋 간의 결합을 가능하게 했습니다.

기존 POS 및 ERP 시스템의 세분화

2025년 전미소매협회(NRF)의 조사에 따르면, 미국 체인점의 63%가 상호 운용성이 부족한 거래 시스템을 최소 3개 이상 운영하고 있어, 통합된 고객 프로파일 구축 및 실시간 재고 관리가 지연되고 있습니다. 대규모 체인의 경우, 시스템 교체 비용이 5,000만 달러를 초과하는 경우가 많아 고객 대상 투자에 부담을 주고 있습니다. 배치 추출은 1초 이내의 의사결정을 방해하며, 실시간 개인화 및 가격 최적화를 통해 얻을 수 있는 이점을 제한하고 있습니다.

부문별 분석

부정 감지 시장은 2031년까지 연평균 성장률(CAGR) 10.76%로 확대되고 있으며, 소매업 빅데이터 분석 시장에서 가장 빠르게 성장하고 있는 용도으로 자리매김하고 있습니다. 옴니채널 결제 흐름을 노린 계정 탈취 및 합성 ID 공격으로 인해, 그래프 분석 및 행동 생체 인식 기술에 대한 투자가 촉진되고 있습니다. 고객 분석은 2025년 매출의 37.29%를 차지했지만, 세분화 및 생애 가치(LTV) 모델이 성숙해짐에 따라 그 성장 곡선은 정체되는 추세를 보였습니다. 머천다이징 및 공급망 팀은 현재 날씨나 소셜 미디어의 여론과 같은 외부 요인을 바탕으로 재고 보충을 자동화하는 예측형 엔진에 의존하고 있습니다.

운영 인텔리전스 대시보드는 상품화가 진행됨에 따라, 벤더들은 약국의 규정 준수 추적 등 산업별 특화형 부가 기능을 탑재해야 하는 압박을 받고 있습니다. 소매 시장의 빅데이터 분석 시장 규모 중, 부정 행위 감지에 기인하는 부분은 ‘즉시 구매·후불’ 및 디지털 지갑의 보급으로 인해 위협의 범위가 확대됨에 따라 더욱 커질 것으로 예측됩니다. 각 벤더사는 원활한 결제 경험을 유지하면서 오탐률을 낮게 억제하는 모델을 통해 차별화를 꾀하고 있습니다. 또한, 소매업체들은 부정 행위에 대한 인사이트를 개인화 워크플로에 통합하고, 고위험 프로파일에 대해 추가 검증을 실시함으로써 보안과 고객 경험 간의 균형을 맞추고 있습니다.

중소기업은 창고 관리, 머신러닝, 시각화 기능을 통합한 종량제 클라우드 플랫폼을 활용하여 연평균 성장률(CAGR) 9.61%로 매출을 확대될 전망입니다. 대기업은 수년에 걸친 공급업체 계약과 더 큰 인력 예산을 바탕으로, 2025년 지출의 63.24%를 차지했습니다. AutoML 기능과 미리 구축된 커넥터를 통해 지역 식료품점은 사내 데이터 엔지니어가 없어도 고급 도구를 도입할 수 있게 되었으며, 고급 분석 기능이 널리 보급되고 있습니다.

대형 체인점들은 여전히 대폭적인 물량 할인을 협상하고 있지만, 복잡한 조직 구조로 인해 전사적인 확대가 지연되고 있습니다. 컴포저블 커머스를 통해 전체 스택을 전면 개편하는 대신 최고 수준의 모듈을 통합할 수 있게 됨에 따라, 중소기업(SME)에서 발생하는 소매 시장의 빅데이터 분석 규모가 확대되고 있습니다. 클라우드 제공업체는 탄력적으로 확장 가능한 스타터 플랜을 통해 이러한 소매업체들을 유치하고, 자본적 위험 없이 실험을 할 수 있도록 지원하고 있습니다. 인력 부족은 여전히 제약 요인으로 작용하고 있지만, 매니지드 서비스와 가이드가 포함된 노트북이 기술 격차를 완화하고 있습니다.

지역별 분석

북미는 고객 데이터 플랫폼의 조기 도입과 분석 업체들이 구축한 긴밀한 생태계의 지원에 힘입어 2025년 매출의 47.62%를 차지했습니다. 이 지역은 현재 단계적인 최적화 단계로 접어들고 있으며, 소매업체들은 기존 투자에 더해 클린룸과 설명 가능한 AI를 도입하고 있습니다. 아시아태평양은 중국의 대형 소셜 커머스 기업들과, 2025년 12월 기준 116억 건의 거래를 처리하며 분석 파이프라인용 상세한 행동 데이터를 생성한 인도의 Unified Payments Interface(UPI)에 힘입어 11.01%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다.

중국에서는 Alipay와 WeChat이 결제, 소셜 참여, 고객 충성도를 단일 생태계로 통합하고 있기 때문에 폐쇄형 어트리뷰션이 가능합니다. 이는 서유럽 시장이 재현하는 데 어려움을 겪고 있는 강점입니다. 일본과 한국에서는 무인 매장의 시범 운영이 진행되고 있으며, 엣지 추론 및 컴퓨터 비전에 대한 수요가 증가하고 있습니다. 호주는 소매 거래 데이터의 오픈 뱅킹 방식의 이동성을 촉진하는 데이터 공유 규제를 확대하고 있으며, 이는 다른 관할 구역에 선례가 될 것으로 보입니다.

유럽은 엄격한 데이터 보호 규정으로 인해 성장세가 주춤하고 있지만, 원시 데이터를 이동시키지 않고 분산형 노드 간에 모델을 학습시키는 ‘페더레이티드 러닝’의 실증 실험에서 주도적인 역할을 하고 있습니다. 중동의 고급 소매업체와 대형 마트는 관광 산업의 회복에 발맞추어 수익성이 높은 개인화 엔진을 도입하고 있는 반면, 아프리카의 초기 단계에 있는 전자상거래는 간헐적인 연결 환경을 위해 설계된 경량형 모바일 우선 분석 기술에 의존하고 있습니다. 남미에서는 거시경제의 변동과 클라우드 인프라의 격차로 인해 성장세가 둔화되고 있지만, 브라질의 대형 체인업체들은 환율 변동과 수입 관세를 조정하는 모델을 시범 운영하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the big data analytics in retail market size is projected to be USD 7.38 billion in 2025, USD 8.14 billion in 2026, and reach USD 12.68 billion by 2031, advancing at a 9.26% CAGR across the period.

This report is Segmented by Application (Merchandising and Supply Chain Analytics, and More), Business Type (Small and Medium Enterprises, and More), Deployment Mode (On-Premise, and Cloud), Analytics Type (Descriptive Analytics, and More), Component (Software, and Services), Retail Format (E-Commerce Stores, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Big Data Analytics In Retail Market Trends and Insights

Surge in Real-Time Omni-Channel Personalisation

Retailers have embedded streaming engines that ingest clickstream, point-of-sale, and mobile-app events within milliseconds, allowing offers and recommendations that mirror a shopper's most recent action. Amazon Web Services spotlighted this capability in its 2025 keynote as critical for reducing cart abandonment during seasonal peaks. Walmart's rollout across 4,700 United States stores combined beacon signals and online histories to boost cross-category basket value by 12%. The approach requires rigorous fairness checks because under-represented cohorts can skew training data, a risk the European Artificial Intelligence Act addresses through transparency mandates.

Integration of Retail Media Networks with First-Party Data

On-site advertising platforms generated USD 50 billion global revenue in 2025, fueled by purchase-based targeting that links impressions to in-basket sales. Kroger grew its advertiser base 38% by activating anonymized loyalty data inside privacy-preserving clean rooms. Snowflake and Google Cloud formalized joint clean-room products in early 2026, enabling cross-dataset joins without exposing raw records.

Fragmentation of Legacy POS and ERP Stacks

A 2025 National Retail Federation survey showed 63% of United States chains operate at least three transaction systems lacking interoperability, delaying unified customer profiles and real-time inventory. Replacement costs often exceed USD 50 million for large chains, crowding out customer-facing investments. Batch extracts inhibit sub-second decisioning, limiting benefits from real-time personalization and price optimization.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Edge Analytics for In-Store IoT

- Growing Adoption of AI-Powered Price Optimisation Engines

- Privacy-Centric Browser and OS Restrictions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fraud Detection is growing at a 10.76% CAGR through 2031, making it the fastest-moving application within the big data analytics in retail market. Account-takeover and synthetic identity attacks targeting omnichannel payment flows are driving investment in graph-analysis and behavioral biometrics. Customer Analytics still delivered 37.29% of 2025 revenue, but its trajectory is flattening as segmentation and lifetime-value models mature. Merchandising and supply-chain teams now rely on prescriptive engines that automate replenishment based on external factors such as weather and social sentiment.

Operational intelligence dashboards have become commoditized, pressuring vendors to embed vertical add-ons like pharmacy compliance tracking. The big data analytics in retail market size attributed to Fraud Detection is expected to widen as buy-now-pay-later and digital wallets expand the threat surface. Vendors are differentiating through low-false-positive models that preserve frictionless checkout. Retailers also integrate fraud insights into personalization workflows so high-risk profiles trigger additional verification, balancing security with customer experience.

Small and Medium Enterprises are set to expand revenue at 9.61% CAGR, leveraging usage-based cloud platforms that bundle warehousing, machine learning, and visualization. Large Enterprises controlled 63.24% of 2025 spending, anchored by multi-year vendor contracts and larger staffing budgets. AutoML features and pre-built connectors let regional grocers deploy advanced tools without in-house data engineers, democratizing sophisticated analytics capabilities.

Large chains still negotiate deep volume discounts, yet their complex organizations slow company-wide rollouts. The big data analytics in retail market size flowing from SMEs is rising as composable commerce lets them plug in best-of-breed modules instead of overhauling entire stacks. Cloud providers lure these retailers with starter tiers that scale elastically, allowing experimentation without capital risk. Talent shortages remain a constraint, though managed services and guided notebooks mitigate the skills gap.

Geography Analysis

North America supplied 47.62% of 2025 revenue, supported by early adoption of customer data platforms and a dense ecosystem of analytics vendors. The region is now shifting toward incremental optimization, with retailers layering clean rooms and explainable AI atop existing investments. Asia-Pacific is forecast to record the highest 11.01% CAGR, propelled by China's social-commerce giants and India's Unified Payments Interface, which processed 11.6 billion transactions in December 2025, producing granular behavioral data for analytics pipelines.

In China, closed-loop attribution is feasible because Alipay and WeChat integrate payments, social engagement, and loyalty in a single ecosystem, an advantage Western markets struggle to replicate. Japan and South Korea are piloting cashierless stores, boosting demand for edge inference and computer vision. Australia is expanding data-sharing regulations that encourage open banking-style portability for retail transaction data, setting a precedent for other jurisdictions.

Europe faces slower growth owing to stringent data-protection rules, yet it plays a lead role in federated learning trials that train models across decentralized nodes without moving raw data. Middle East luxury retailers and hypermarkets are adopting high-margin personalization engines as tourism rebounds, while Africa's nascent e-commerce relies on lightweight, mobile-first analytics designed for intermittent connectivity. South America's expansion is tempered by macroeconomic volatility and cloud-infrastructure gaps, though Brazil's leading chains are piloting models that adjust for currency swings and import tariffs.

- SAP SE

- International Business Machines Corporation

- Oracle Corporation

- Salesforce, Inc.

- Amazon Web Services, Inc.

- Adobe Inc.

- Microsoft Corporation

- Google LLC

- QlikTech International AB

- Zoho Corporation Pvt. Ltd.

- Alteryx, Inc.

- RetailNext Inc.

- MicroStrategy Incorporated

- Hitachi Vantara LLC

- Fuzzy Logix, Inc.

- Teradata Corporation

- Cloudera, Inc.

- Informatica LLC

- Splunk Inc.

- Databricks, Inc.

- Snowflake Inc.

- SAS Institute Inc.

- dunnhumby Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Real-Time Omni-Channel Personalisation

- 4.2.2 Rise of Headless Commerce Architectures

- 4.2.3 Integration of Retail Media Networks with First-Party Data

- 4.2.4 Expansion of Edge Analytics for In-Store IoT

- 4.2.5 Growing Adoption of AI-Powered Price Optimisation Engines

- 4.2.6 Mainstreaming of Customer Data Platforms (CDPs) in Retail

- 4.3 Market Restraints

- 4.3.1 Fragmentation of Legacy POS and ERP Stacks

- 4.3.2 Privacy-Centric Browser and OS Restrictions

- 4.3.3 Shortage of Retail Data Science Talent

- 4.3.4 Escalating Cloud Egress and Data Movement Costs

- 4.4 Industry Value / Supply-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Merchandising and Supply Chain Analytics

- 5.1.2 Social Media Analytics

- 5.1.3 Customer Analytics

- 5.1.4 Operational Intelligence

- 5.1.5 Pricing Optimisation

- 5.1.6 Fraud Detection

- 5.1.7 Other Applications, Application

- 5.2 By Business Type

- 5.2.1 Small and Medium Enterprises

- 5.2.2 Large Enterprises

- 5.3 By Deployment Mode

- 5.3.1 On-Premise

- 5.3.2 Cloud

- 5.4 By Analytics Type

- 5.4.1 Descriptive Analytics

- 5.4.2 Diagnostic Analytics

- 5.4.3 Predictive Analytics

- 5.4.4 Prescriptive Analytics

- 5.5 By Component

- 5.5.1 Software

- 5.5.2 Services

- 5.6 By Retail Format

- 5.6.1 E-Commerce Stores

- 5.6.2 Brick-and-Mortar Stores

- 5.6.3 Omnichannel Retailers

- 5.6.4 Direct-to-Consumer Brands

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 United Kingdom

- 5.7.2.2 Germany

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 South Korea

- 5.7.3.5 Rest of Asia-Pacific

- 5.7.4 Middle East

- 5.7.4.1 Israel

- 5.7.4.2 Saudi Arabia

- 5.7.4.3 United Arab Emirates

- 5.7.4.4 Turkey

- 5.7.4.5 Rest of Middle East

- 5.7.5 Africa

- 5.7.5.1 South Africa

- 5.7.5.2 Egypt

- 5.7.5.3 Rest of Africa

- 5.7.6 South America

- 5.7.6.1 Brazil

- 5.7.6.2 Argentina

- 5.7.6.3 Rest of South America

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 International Business Machines Corporation

- 6.4.3 Oracle Corporation

- 6.4.4 Salesforce, Inc.

- 6.4.5 Amazon Web Services, Inc.

- 6.4.6 Adobe Inc.

- 6.4.7 Microsoft Corporation

- 6.4.8 Google LLC

- 6.4.9 QlikTech International AB

- 6.4.10 Zoho Corporation Pvt. Ltd.

- 6.4.11 Alteryx, Inc.

- 6.4.12 RetailNext Inc.

- 6.4.13 MicroStrategy Incorporated

- 6.4.14 Hitachi Vantara LLC

- 6.4.15 Fuzzy Logix, Inc.

- 6.4.16 Teradata Corporation

- 6.4.17 Cloudera, Inc.

- 6.4.18 Informatica LLC

- 6.4.19 Splunk Inc.

- 6.4.20 Databricks, Inc.

- 6.4.21 Snowflake Inc.

- 6.4.22 SAS Institute Inc.

- 6.4.23 dunnhumby Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment