|

시장보고서

상품코드

2063384

소 헬스케어 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Cattle Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

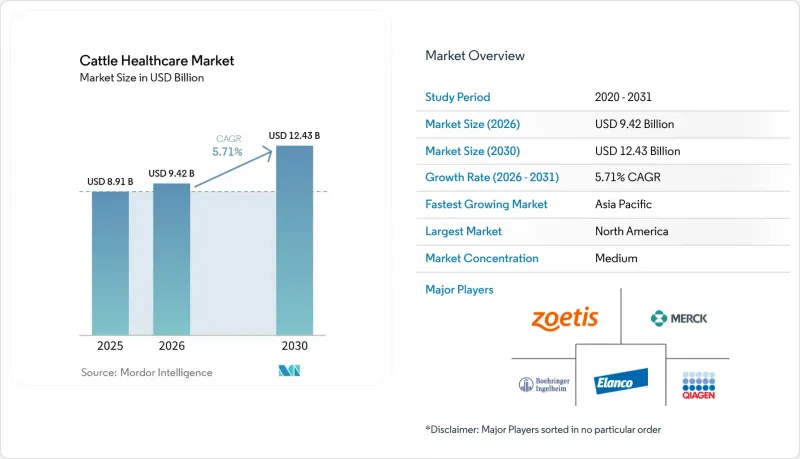

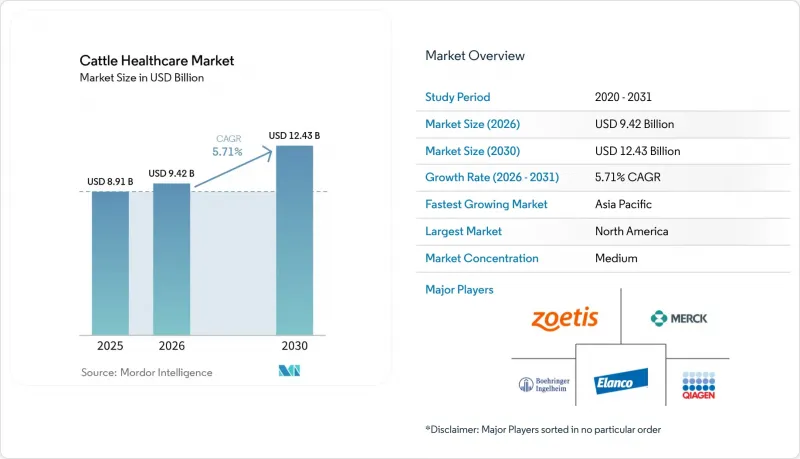

Mordor Intelligence에 의하면, 소 헬스케어 시장 규모는 2025년 89억 1,000만 달러로 평가되었고, 2026년 94억 2,000만 달러로 추정되고, 2030년까지 124억 3,000만 달러로 확대될 전망이며, 2026-2030년 CAGR 5.71%를 나타낼 것으로 예측됩니다.

본 보고서는 제품 유형별(치료제(백신 등), 진단제(면역 진단제 등)), 질병별(BRD, 유방염, BVD, 구제역 등), 최종 사용자별(낙농장, 육우 비육장, 번식 시설, 동물병원, 정부 기관, 목장), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

세계의 소 헬스케어 시장 동향 및 인사이트

전 세계 동물성 단백질 소비의 급증

아시아태평양의 쇠고기 소비량은 2025년에 3.2% 증가하여 세계 평균을 크게 상회했습니다. 이에 따라 예방적 건강 관리 프로토콜을 통해 개체당 생산성을 향상시켜야 할 필요성이 더욱 커지고 있습니다. 현재 중동의 바이어들은 OIE(국제수역사무국)의 기준을 상회하는 수의학적 증명서를 요구하고 있어, 수출업체들은 신속한 진단 및 추적 시스템 구축에 투자할 수밖에 없는 상황입니다. 인도에서는 2025년에 젖소가 210만 마리 증가했으나, 무증상 유방염으로 인해 생산량이 여전히 최대 20%까지 감소하고 있어, 현장 면역 진단법에는 분명한 성장 여지가 있습니다. 중국의 도시 소비자들은 항생제 잔류량이 적다고 표시된 우유에 12% 더 높은 가격을 지불하고 있으며, 이에 따라 협동조합들은 예방적 생물학적 제제의 도입을 추진하고 있습니다. 전반적으로 볼 때, 수요 증가는 사육두수 확대에 기인한 것이 아니라, 정밀한 건강 관리에 대한 투자를 통해 기존 젖소에서 잔류물이 없는 고품질의 우유를 생산해 낸 데서 비롯된 것입니다.

예방 의료 지원금 확대

2025년 미국 농무부(USDA)가 시행한 1억 8,000만 달러 규모의 매칭 보조금은 자동 백신 접종, 감시 네트워크 및 농장 내 생물 보안 강화를 대상으로 하여, 생산자의 투자 회수 기간을 2년 미만으로 단축했습니다. 현재, 공동농업정책(CAP)의 보조금을 통해 동물 복지 및 메탄 배출 목표를 충족하는 통합적인 가축 건강 관리 계획 비용의 최대 60%가 지원되고 있으며, 기후 목표와 질병 예방이 사실상 하나로 통합되어 있습니다. 브라질에서는 과도기에 있는 주를 대상으로 구제역 백신 비용의 40%를 지원하는 보조금 제도를 시범적으로 도입했으며, 프로그램 종료 전 단기간에 생물학적 제제에 대한 수요가 급증했습니다. 생산자가 보조금 제도의 혜택을 통해 발병률이나 도태 손실의 감소를 체감하게 되면, 예전 상태로 되돌아가는 경우는 거의 없으며, 백신이나 진단제에 대한 구조적인 수요를 정착시키는 '래칫 효과'가 발생합니다.

차세대 생물학적 제제의 콜드체인 및 제제 비용

mRNA 제품은 -20℃에서 -70℃ 사이의 온도에서 보관해야 하지만, 2025년 시점에서 인도와 사하라 사막 이남 아프리카의 유통업체 대부분은 초저온 보관 설비를 갖추고 있지 않았습니다. 동남아시아에서는 폐기율이 18%에 달했고, 제조업체들은 최대 25%의 과잉 출하를 감수해야 했으며, 이로 인해 입고 비용이 상승했습니다. 세바사의 보고에 따르면, 동결건조된 mRNA 프로토타입은 실온에서 6개월간 보관할 수 있지만, 1회분당 비용이 35% 상승합니다. 이러한 상충 관계로 인해 가격에 민감한 지역에서의 도입이 제한되고 있습니다. 그 결과, 첨단 생물학적 제제는 경제적으로 여유가 있는 지역에 한정되어 있고, 신흥 시장에서는 오래되고 효과가 낮은 치료법에 의존할 수밖에 없는 양극화된 가축 헬스케어 시장이 형성되고 있습니다.

부문별 분석

2025년, 치료제는 소 헬스케어 시장에서 83.1%의 점유율을 유지했습니다. 이는 백신, 구충제, 항감염제 등 기본적인 생물안전의 토대가 되는 약품에 대한 의존이 여전히 지속되고 있음을 반영합니다. 한편, 진단약의 경우, 현장 진단용 PCR 장비나 농장용 바이오센서를 통해 결과가 나오는 시간이 30분 미만으로 단축됨에 따라, 2031년까지 연평균 7.22%의 성장률이 예상됩니다. 2025년에는 Neogen사의 미국 농무부(USDA) 승인을 받은 4,200달러짜리 휴대용 BVD 검출기에 힘입어, 분자진단 플랫폼이 진단 분야 매출에서 큰 비중을 차지했습니다. 면역 진단은 여전히 판매량 면에서 우위를 점하고 있지만, 포화 상태에 이른 선진국 시장에서는 성장세가 둔화되고 있습니다. 치료제 분야에서는 소매업체와 규제 당국의 항생제 사용 규제 강화에 따라, 항감염제보다 백신 수요가 증가하고 있습니다.

진단 분야로의 전환은 전략적 전환을 여실히 보여주고 있습니다. 특히 항생제 내성이 정책적 감시 대상이 되고 있는 상황에서 아픈 동물을 치료하는 것보다 질병 발생을 미연에 방지하는 것이 더 높은 수익을 가져다주기 때문입니다. 휴대용 초음파 진단기나 신속 화학 검사는 여전히 틈새 시장 제품이지만, 조기 임신 확인을 통해 분만 간격을 단축할 수 있는 번식용 소 사육 분야에서 그 수요가 증가하고 있습니다. 도입이 확대됨에 따라, 진단 기술은 소 사육군의 성과를 벤치마킹하는 부가적인 데이터 분석 서비스 시장 규모를 확대할 것으로 예측됩니다.

지역별 분석

북미는 2025년 매출의 41.2%를 차지했습니다. 이는 미국의 대규모 낙농장 및 비육 목장들이 소매업체의 지속가능성 지표를 달성하기 위해 로봇 기술, AI를 활용한 모니터링, 그리고 독자적인 생물학적 제제에 투자했기 때문입니다. 캐나다 공급 관리형 낙농 부문에서는 예방 의료에 개체당 평균 142캐나다 달러(105달러)를 재투자하고 있으며, 이는 북미 대륙 전체 평균보다 18% 높은 수치입니다. 외국 자본에 힘입어 멕시코의 비육 목장이 확대되면서 호흡기 백신 매출이 증가하고 있지만, 위조 의약품과 규제 미비 사항이 성장을 저해하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 6.98%로 성장을 지속하고, 있으며, 인도에서는 '국가 축산 미션'의 보조금을 통해 3억 300만 마리의 소 사육에 대한 디지털화가 진행되고 있고, 중국에서는 2030년까지 젖소 1,000마리 이상을 보유한 목장의 생산량을 전체 우유 생산량의 절반으로 늘리는 것을 목표로 하고 있습니다. 일본과 한국은 엄격한 잔류 기준에 따라 1인당 지출액이 세계 최고 수준입니다. 한편, 호주의 수출 지향형 목장 경영자들은 질병 없는 지위를 유지하기 위해 진드기 및 매개생물에 대한 백신을 요구하고 있습니다. 동남아시아에서는 콜드체인의 제약으로 인해 차세대 생물학적 제제의 도입이 제한되고 있어, 기존의 불활성화 백신이 계속 사용되고 있습니다.

유럽은 소 헬스케어 시장에서 큰 비중을 차지하고 있으며, 항생제 사용 감축 정책이 백신 대체 및 대체 요법을 촉진하고 있습니다. 독일과 프랑스의 목장에서는 고급 소매업체를 대상으로 저잔류 상태를 입증하는 진단 기술에 막대한 투자를 하고 있습니다. 남미는 브라질의 2억 2,400만 마리의 소 사육 규모를 활용하고 있지만, 원자재 관세나 자금 조달 여건에 따라 수요 변동이 주기적으로 나타나고 있습니다. 중동 및 아프리카는 여전히 시장 규모가 가장 작은 지역이지만, GCC(걸프협력회의) 국가들의 기후 조절 낙농장과 사하라 이남 아프리카의 질병 근절 캠페인은 높은 수익률을 보이는 생물학적 제제에 대한 수요를 견인하는 틈새 성장 동력이 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the cattle healthcare market size is projected to expand from USD 8.91 billion in 2025 and USD 9.42 billion in 2026 to USD 12.43 billion by 2030, registering a CAGR of 5.71% between 2026 to 2030.

This report is Segmented by Product Type [Therapeutics (Vaccines and More), Diagnostics (Immunodiagnostics and More)], Disease (BRD, Mastitis, BVD, FMD, and More), End User (Dairy Farms, Beef Feedlots, Breeding Operations, Veterinary Clinics, Government Institutes, Ranches), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Cattle Healthcare Market Trends and Insights

Surging Global Consumption of Animal Protein

Beef intake in Asia-Pacific rose 3.2% in 2025, far above the world average, reinforcing the need to lift per-animal productivity through preventive health protocols . Middle Eastern buyers now demand veterinary certificates that exceed OIE baselines, obliging exporters to invest in rapid diagnostics and traceability. India added 2.1 million milking cows in 2025, yet subclinical mastitis still erodes yields by up to 20%, creating clear headroom for point-of-care immunodiagnostics. Urban Chinese consumers are paying 12% more for milk labeled low in antibiotic residues, nudging cooperatives toward prophylactic biologics. Altogether, demand growth is less about herd expansion and more about squeezing higher, residue-free output from existing cattle through precision health investments.

Expansion of Preventive-Care Subsidies

USDA matching grants worth USD 180 million in 2025 covered automated vaccination, surveillance networks, and on-farm biosecurity upgrades, lowering producer payback periods to under two years. Common Agricultural Policy payments now reimburse up to 60% of the cost of integrated herd-health plans that meet animal-welfare and methane targets, effectively bundling climate goals with disease prevention. Brazil piloted a 40% vaccine subsidy for foot-and-mouth disease in transitioning states, spiking short-term biologics demand before the program sunsets. Once producers experience lower morbidity and cull losses under subsidized regimes, they rarely revert, creating a ratchet effect that locks in structural demand for vaccines and diagnostics.

Cold-Chain & Formulation Costs for Next-Gen Biologics

mRNA products demand -20 °C to -70 °C storage, yet majority of distributors in India and in sub-Saharan Africa lacked ultra-cold equipment in 2025. Spoilage reached 18% in Southeast Asia, forcing manufacturers to overship by up to 25% and lifting landed costs. Ceva reported that lyophilized mRNA prototypes last six months at room temperature but raise per-dose cost by 35%, a trade-off that limits adoption in price-sensitive areas. The result is a two-tier cattle healthcare market where advanced biologics stay locked in temperate, well-capitalized regions while emerging markets rely on older, less effective options.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of AI-Based Wearables

- mRNA & Nanoparticle Vaccine Breakthroughs

- Acute Shortage of Large-Animal Veterinarians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Therapeutics maintained an 83.1% share of the cattle healthcare market in 2025, reflecting enduring reliance on vaccines, parasiticides, and anti-infectives that underpin basic biosecurity. Diagnostics, however, are forecast to grow 7.22% annually to 2031 as point-of-care PCR devices and on-farm biosensors compress result times to under 30 minutes. Molecular platforms captured a significant share of diagnostic revenue in 2025, buoyed by Neogen's USDA-approved handheld BVD detector priced at USD 4,200. Immunodiagnostics still dominate unit volumes, yet growth slows in saturated developed markets. Within therapeutics, vaccine demand outperforms anti-infectives as retailers and regulators clamp down on antibiotic use.

The tilt toward diagnostics underscores a strategic shift: preventing outbreaks delivers higher returns than treating sick animals, particularly as antimicrobial resistance attracts policy scrutiny. Mobile ultrasound and rapid chemistries remain niche but gain traction in breeding herds where early pregnancy confirmation tightens calving intervals. As uptake widens, diagnostics are set to boost the cattle healthcare market size for ancillary data-analytics services that benchmark herd performance.

Geography Analysis

North America held 41.2% of 2025 revenue as U.S. mega-dairies and feedlots invested in robotics, AI-based monitoring and proprietary biologics to hit retailer sustainability metrics. Canada's supply-managed dairy sector reinvested an average CAD 142 (USD 105) per cow in preventive care, 18% above the continental mean. Mexican feedlot expansion, buoyed by foreign capital, boosts respiratory vaccine sales, although counterfeit therapeutics and regulatory gaps temper growth.

Asia-Pacific rides a 6.98% CAGR as India's 303 million-head herd digitizes under National Livestock Mission subsidies, and China targets half of milk output from 1,000-plus-cow dairies by 2030. Japan and South Korea post world-leading per-head spend due to strict residue standards, while Australia's export-oriented graziers demand tick and vector vaccines for disease-free status. Southeast Asian cold-chain limitations restrain uptake of next-gen biologics, keeping older killed vaccines in rotation.

Europe accounts for a significant share of the cattle healthcare market, with antibiotic-reduction policies driving vaccine substitution and alternative therapies. German and French herds invest heavily in diagnostics that document low-residue status for premium retailers. South America leverages Brazil's 224 million-head herd yet sees cyclical demand swings tied to antigen tariffs and credit access. The Middle East and Africa remain smallest by value; however, GCC climate-controlled dairies and sub-Saharan disease-eradication campaigns are niche engines of higher-margin biologics demand.

- AgriLabs

- Biogenesis Bago

- Boehringer Ingelheim Animal Health GmbH

- Ceva Sante Animale

- Dechra Pharmaceuticals

- Elanco Animal Health Inc.

- Hester Biosciences Ltd.

- Huvepharma Inc.

- IDEXX

- Indian Immunologicals

- Jinyu Bio-Technology Co.

- Merck Animal Health (MSD)

- Neogen Corp.

- Norbrook Laboratories Ltd.

- Ourofino Saude Animal SA

- Phibro Animal Health

- Tianjin Ringpu Bio-Pharma

- Vetoquinol

- Virbac

- Zoetis

- Zydus Animal Health & Investments Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Global Consumption Of Animal Protein

- 4.2.2 Expansion Of Preventive-Care Subsidies (US & EU)

- 4.2.3 Adoption Of AI-Based Wearables for Early-Stage Disease Detection

- 4.2.4 mRNA & Nanoparticle Vaccine Breakthroughs

- 4.2.5 Carbon-Credit Premiums for Low-Methane Herds

- 4.2.6 Blockchain-Verified Provenance Schemes Boosting Herd-Health Spend

- 4.3 Market Restraints

- 4.3.1 Cold-Chain & Formulation Costs for Next-Gen Biologics

- 4.3.2 Acute Shortage of Large-Animal Veterinarians

- 4.3.3 Producer Push-Back on Data Ownership & Interoperability

- 4.3.4 Tariff Volatility on Key Antigen Inputs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Therapeutics

- 5.1.1.1 Vaccines

- 5.1.1.2 Parasiticides

- 5.1.1.3 Anti-infectives

- 5.1.1.4 Anti-inflammatories

- 5.1.1.5 Medical Feed Additives

- 5.1.1.6 Other Therapeutics

- 5.1.2 Diagnostics

- 5.1.2.1 Immunodiagnostics

- 5.1.2.2 Molecular Diagnostics

- 5.1.2.3 Diagnostic Imaging

- 5.1.2.4 Point-of-Care Devices & Biosensors

- 5.1.2.5 Clinical Chemistry

- 5.1.2.6 Other Diagnostics

- 5.1.1 Therapeutics

- 5.2 By Disease

- 5.2.1 Bovine Respiratory Disease (BRD)

- 5.2.2 Mastitis

- 5.2.3 Bovine Viral Diarrhoea (BVD)

- 5.2.4 Foot & Mouth Disease (FMD)

- 5.2.5 Parasitic Infestations

- 5.2.6 Metabolic & Reproductive Disorders

- 5.2.7 Lumpy Skin & Other Vector-borne

- 5.3 By End User

- 5.3.1 Dairy Farms

- 5.3.2 Beef Feedlots

- 5.3.3 Breeding Operations

- 5.3.4 Veterinary Hospitals & Clinics

- 5.3.5 Government & Research Institutes

- 5.3.6 Ranches

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of APAC

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of MEA

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AgriLabs

- 6.3.2 Biogenesis Bago

- 6.3.3 Boehringer Ingelheim Animal Health GmbH

- 6.3.4 Ceva Sante Animale

- 6.3.5 Dechra Pharmaceuticals PLC

- 6.3.6 Elanco Animal Health Inc.

- 6.3.7 Hester Biosciences Ltd.

- 6.3.8 Huvepharma Inc.

- 6.3.9 IDEXX Laboratories Inc.

- 6.3.10 Indian Immunologicals Ltd.

- 6.3.11 Jinyu Bio-Technology Co.

- 6.3.12 Merck Animal Health (MSD)

- 6.3.13 Neogen Corp.

- 6.3.14 Norbrook Laboratories Ltd.

- 6.3.15 Ourofino Saude Animal SA

- 6.3.16 Phibro Animal Health Corp.

- 6.3.17 Tianjin Ringpu Bio-Pharma

- 6.3.18 Vetoquinol SA

- 6.3.19 Virbac SA

- 6.3.20 Zoetis Inc.

- 6.3.21 Zydus Animal Health & Investments Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment