|

시장보고서

상품코드

2063385

돼지 헬스케어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Swine Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

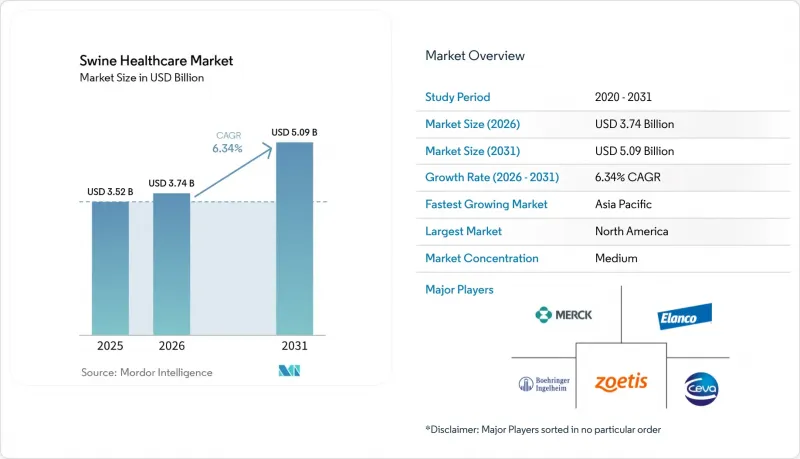

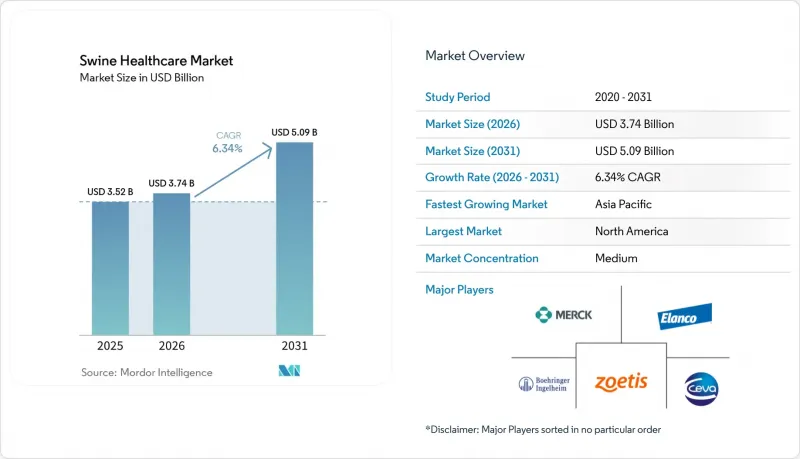

Mordor Intelligence에 의하면, 돼지 헬스케어 시장 규모는 2025년에 35억 2,000만 달러로 평가되었습니다. 2026년에 37억 4,000만 달러에서 2031년까지 50억 9,000만 달러에 이를 것으로 예측되며, 2026-2031년에 걸쳐 CAGR 6.34%로 성장할 전망입니다.

본 보고서는 제품별(진단약(ELISA, 신속면역이동법(RIM), 기타), 치료제(백신, 기타)), 질환별(삼출성 피부염, 콕시듐증, 기타), 최종 사용자별(대규모 통합 양돈 사업, 기타), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 돼지 헬스케어 시장 동향 및 인사이트

풍토병 및 국경을 넘는 돼지 질병의 발생률 증가

아프리카 돼지열병은 여전히 백신 및 진단에 대한 투자의 주요 요인으로 작용하고 있으며, 무역 제한을 초래하고 고위험 지역에서 주간 PCR 감시를 실시하도록 하고 있습니다. 돼지 생식 호흡기 증후군(PRRS)은 분만두 수 감소와 2차 감염을 통해 미국 양돈 농가에게 연간 약 6억 6,400만 달러의 손실을 초래하고 있습니다. IDEXX와 서모피셔사는 2025년, ASF, 세네카 밸리 바이러스, PCV-3를 몇 시간 이내에 감별할 수 있는 다중 PCR 패널을 출시하여 불필요한 이동 제한 및 살처분을 억제했습니다. 지속적인 질병 부담으로 인해 유전자 편집 프로젝트가 진전되고 있음에도 불구하고, 돼지 헬스케어 시장의 예방 부문은 견조한 성장세를 유지하고 있습니다. 따라서 통합 생산자들은 발생에 따른 막대한 직접 비용과 기회 비용을 피하기 위해 백신 접종률 향상과 신속한 진단을 우선시하고 있습니다.

전 세계적으로 확대되는 돼지고기 수요와 고도화되는 생산 시스템

2020년부터 2025년에 걸쳐 1인당 돼지고기 소비량은 베트남에서 8%, 필리핀에서 6%, 인도에서 12% 증가했습니다. 이러한 수요를 흡수하기 위해 개발업체는 북미의 폐쇄형 바이오보안 방식을 본뜬 1만 마리 규모의 시설에 자금을 지원했으며, 백신, 프로바이오틱스, 실시간 모니터링에 대한 기초적인 지출을 늘렸습니다. 브라질의 돼지고기 수출량은 2025년에 120만 톤에 달했습니다. 이는 통합형 대기업인 BRF S.A.와 JBS의 주도 하에 이루어진 것으로, 두 회사 모두 병원체 무감염 상태를 유지하기 위해 자체 생산 백신의 사용을 의무화하고 있습니다. 집중된 구매력은 항생제 미사용 실적을 입증한 공급업체에 보상을 제공하는 것이며, 이를 통해 진단약 및 사료 첨가제의 도입이 더욱 확대되고 있습니다. 따라서, 산업적 생산으로의 구조적 전환은 다품목 구매 계약을 정착시키고, 돼지 건강 관리 시장을 확대시키고 있습니다.

복잡하고 지역별로 상이한 규제 승인 절차 및 비용

mRNA 백신과 바이러스 벡터 백신은 미국에서 5-7년, EU에서는 그보다 더 긴 기간에 걸친 심사 절차를 거쳐야 하며, EU에서는 여러 국가에서 현장 검사가 요구됩니다. 조에티스사는 2025년까지 ASF 백신 개발비로 누적 1억 5,000만 달러 이상을 투자할 것이라고 밝혔으며, 수익은 최소 3개 주요 시장에서 승인을 얻는 데 달려 있습니다. 중국에서는 별도의 국내 심사가 의무화되어 있으며, 2024년 승인 대기 기간은 평균 42개월이었습니다. 승인까지 시간이 길어지면 기회비용이 증가합니다. 병원체가 변이하고, 양돈업자들이 임시로 자체 제작한 백신으로 전환함에 따라, 정식 승인이 내려질 시점에 해당 시장 규모가 축소되어 버리기 때문입니다. 그 때문에 중소 바이오기술 기업들은 장기적인 개발 프로젝트에 필요한 자금 조달에 어려움을 겪고 있으며, 혁신은 자금력이 풍부한 다국적 기업에 집중되고 있습니다.

부문별 분석

2025년, 치료 부문은 돼지 헬스케어 시장 점유율의 54.33%를 차지하며, PRRS 및 마이코플라스마 백신, 구충제, 항감염제에 대한 안정적인 수요를 반영하고 있습니다. 진단약은 2025년에는 상대적으로 낮은 시장 점유율에 그쳤으나, 대형 통합 기업들이 주간 PCR 모니터링 및 혈청학적 벤치마킹을 도입함에 따라 2031년까지 연평균 성장률(CAGR) 7.43%를 기록하며 의약품 부문을 능가하는 성장이 예상됩니다. ELISA 키트는 여전히 일상적인 집단 검사의 주류를 이루고 있지만, 1개의 검체에서 아프리카 돼지열병(ASF), 세네카 밸리 바이러스, PCV-3를 검출하는 다중 실시간 PCR 패널이 미국, EU, 중국의 대규모 양돈 농장들로부터 주문을 확보하고 있습니다. 치료용으로 분류되는 사료 첨가물은 EU에서 산화아연의 사용이 금지됨에 따라 수요가 유기산 및 식물성 첨가물로 전환된 결과, 2020년부터 2025년에 걸쳐 뚜렷한 연평균 성장률(CAGR)을 기록했습니다. 15분 만에 결과를 확인할 수 있는 신속 래터럴 플로우 검사는 검사 시설이 잘 갖춰지지 않은 동남아시아의 수의사들 사이에서 인기를 끌며, 프리미엄 시장 이외의 영역으로 진단 시장의 침투를 확대되고 있습니다.

치료에서 예방적 선별 검사로의 전환에 따라 해당 부문의 수익성이 향상되었으며, 소모품 정기 구매 모델이 정착되고 있습니다. IDEXX는 2025년 북미의 돼지용 PCR 검사 건수가 전년 대비 크게 증가했다고 보고했으며, 이는 검사 빈도 증가가 검사 단가 하락을 상쇄하고 있음을 보여줍니다. 2024년에 출시된 휴대용 초음파 진단 장치를 통해 농장 내 번식 관리용 영상 촬영이 가능해지면서, 그동안 충분히 다루어지지 않았던 관리 업무에 진단 기술이 도입되고 있습니다. 한때 틈새 서비스에 불과했던 자가 제조 백신은 현재, 베링거 인겔하임과 세바에 인수된 맞춤형 제조업체들에게 롱테일 수익의 기반이 되고 있습니다. 통합업체들이 분석을 활용해 백신 접종 일정을 최적화함에 따라, 치료 부문의 성장은 둔화되는 반면 진단 부문은 가속화되어, 돼지 헬스케어 시장 전체의 연평균 성장률(CAGR) 6.34%라는 추세를 유지하고 있습니다.

지역별 분석

2025년 북미는 전 세계 매출의 45.3%를 차지했습니다. 이는 7,400만 마리의 사육 두수에 더해, 수출 대상국인 멕시코, 일본, 한국에 있는 수출 파트너들에게 인증을 의무화하는 미국 농무부(USDA)의 엄격한 생물안전 규제에 따른 것입니다. 캐나다에서는 2024년에 도입된 자발적인 데이터 공유 체계를 통해 생산자들이 벤치마크를 대가로 진단 결과를 제출하도록 장려함으로써, 검사실의 성장에 기여하는 선순환이 형성되고 있습니다. 멕시코의 돼지고기 생산량은 2025년에 증가할 것이며, 미국과의 통합된 공급망으로 인해 한쪽 국가에서 질병이 발생하면 다른 쪽 국가에서의 백신 및 진단제 구매가 급격히 증가하게 될 것입니다.

아시아태평양은 2026년부터 2031년까지 연평균 성장률(CAGR) 7.54%를 나타낼 것으로 예측되며, 돼지 헬스케어 시장에서 지역별로는 가장 빠른 성장세를 보일 것으로 전망됩니다. 중국에서는 성을 넘나드는 모든 돼지 이동에 대해 PCR 검사를 의무화하는 지침에 따라, 확진 건수가 구조적으로 증가하고 있습니다. 또한, 일부 지역에서 아프리카 돼지열병(ASF)이 재발함에 따라, 돼지 사육 군의 재건이 서서히 진행되고 있음에도 불구하고 백신 수요는 여전히 유지되고 있습니다. 베트남에서는 생물안전성에 대한 보조금과 긴급 사용이 승인된 ASF 백신의 지원에 힘입어 2025년 돼지고기 생산량이 480만 톤에 달했으나, 동료 심사를 거친 유효성 데이터가 부족하여 주변 국가들의 수입 승인은 신중한 태도를 보이고 있습니다. 인도의 도시 지역 중산층에서는 돼지고기 소비량이 증가하고 있지만, 소규모 농업 종사자들로 인해 단절된 공급망이 수의학 서비스 이용을 제한하고 있어, 저비용이며 열안정성이 뛰어난 백신에는 향후 성장 여지가 있습니다.

2025년, 유럽은 전 세계 매출에 크게 기여했습니다. 그 선두에 선 것은 독일, 스페인, 프랑스였으며, 이들 국가에서는 동물 복지 규제와 산화아연 사용 금지로 인해 항생제를 사용하지 않는다고 표방하는 백신 및 사료 첨가제에 대한 지출이 촉진되고 있습니다. 스페인은 2025년에 상당한 양의 돼지고기를 중국으로 수출하고 있으며, 이는 해당 지역에서 병원체 무감염 인증의 중요성을 여실히 보여주고 있습니다. 브라질의 통합형 생산자들은 120만 톤의 수출량을 보호하기 위해 북미의 가축 건강 관리 모델을 본받고 있으며, 이로 인해 다국적 백신 및 진단제 공급업체에 대한 지출이 증가하고 있습니다. 중동 및 아프리카는 여전히 시장 규모가 작지만, 남아프리카공화국의 상업 부문과 나이지리아의 급속한 사육 두수 증가는 콜드체인과 수의사 인력 확보 문제가 개선된다면 잠재적인 수요를 창출할 가능성이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the swine healthcare market size is projected to be USD 3.52 billion in 2025, USD 3.74 billion in 2026, and reach USD 5.09 billion by 2031, growing at a CAGR of 6.34% from 2026 to 2031.

This report is Segmented by Product [Diagnostics (ELISA, Rapid Immune Migration (RIM) and More), Therapeutics (Vaccines and More)], Disease (Exudative Dermatitis, Coccidiosis, and More), End User (Large Integrated Swine Operations, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Swine Healthcare Market Trends and Insights

Rising Incidence of Endemic & Trans-boundary Swine Diseases

African Swine Fever remains the chief catalyst for vaccine and diagnostic investment, generating trade restrictions that force weekly PCR surveillance in high-risk zones . Porcine reproductive and respiratory syndrome costs U.S. producers about USD 664 million annually through lower litter sizes and secondary infections. IDEXX and Thermo Fisher launched multiplex PCR panels in 2025 that differentiate ASF, Seneca Valley virus, and PCV-3 within hours, limiting needless movement bans and culling. Sustained disease pressure keeps the swine healthcare market's preventive segment resilient even as gene-editing projects progress. Integrated producers, therefore, prioritize vaccine coverage and rapid diagnostics to avoid the steep direct and opportunity costs of outbreaks.

Expanding Global Pork Demand & Intensifying Production Systems

Per-capita pork intake climbed 8% in Vietnam, 6% in the Philippines, and 12% in India between 2020 and 2025 . To capture demand, developers financed 10,000-head facilities that copy North American closed-herd biosecurity, elevating baseline spending on vaccines, probiotics, and real-time monitoring. Brazil's pork exports reached 1.2 million t in 2025 on the back of integrated giants BRF S.A. and JBS, both mandating autogenous vaccines to protect pathogen-free status. Concentrated buying power rewards suppliers that prove antibiotic-free performance, deepening adoption of diagnostics and feed additives. The structural shift to industrial production, therefore, entrenches multi-product purchasing contracts that enlarge the swine healthcare market.

Complex, Region-Specific Regulatory Approval Timelines & Costs

mRNA and viral-vector vaccines face 5-to-7-year U.S. pathways and even longer EU vetting that demands multi-country field trials. Zoetis disclosed cumulative ASF vaccine development spend above USD 150 million through 2025, with revenues contingent on approvals in at least three large markets. China requires separate domestic trials, and the approval queue averaged 42 months in 2024. Protracted timelines raise opportunity costs as pathogens mutate and integrators pivot to interim autogenous vaccines, shrinking the eventual addressable pool once full licenses arrive. Smaller biotech firms thus struggle to finance elongated campaigns, concentrating innovation among cash-rich multinationals.

Other drivers and restraints analyzed in the detailed report include:

- Surging R&D Spend on Novel Vaccines, Diagnostics & Feed Additives

- Stricter Food-Safety / Preventive-Health Regulations Worldwide

- High Treatment & Vaccination Costs for Smallholders in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Therapeutics captured 54.33% of the swine healthcare market share in 2025, reflecting steady demand for PRRS and Mycoplasma vaccines, parasiticides, and anti-infectives. Diagnostics contributed a smaller slice in 2025, yet their value is projected to outpace drugs at a 7.43% CAGR through 2031 as large integrators adopt weekly PCR surveillance and serology benchmarking. ELISA kits still dominate routine herd screening, but multiplex real-time PCR panels that detect ASF, Seneca Valley virus, and PCV-3 from one sample are winning orders from U.S., EU, and Chinese mega-farms. Feed additives, classified within therapeutics, posted a notable CAGR between 2020 and 2025 after the EU zinc-oxide ban steered demand toward organic acids and phytogenics. Rapid lateral-flow tests that deliver results in 15 minutes are popular among Southeast Asian veterinarians who lack lab infrastructure, expanding diagnostics penetration beyond premium markets.

The shift from curative drugs to preventive screening lifts the segment's revenue intensity and embeds subscription-style purchases of consumables. IDEXX reported North American swine PCR volume up significantly year-over-year in 2025, evidencing that higher testing frequency offsets lower per-test pricing. Portable ultrasound devices released in 2024 enable on-farm reproductive imaging, nudging diagnostics into previously under-served management tasks. Autogenous vaccines, once a niche service, now underpin long-tail revenue for custom manufacturers acquired by Boehringer Ingelheim and Ceva. As integrators use analytics to refine vaccine schedules, therapeutics growth moderates while diagnostics accelerate, preserving the overall swine healthcare market's 6.34% CAGR trajectory

Geography Analysis

North America generated 45.3% of global revenue in 2025, supported by a 74 million head inventory and strict USDA biosecurity enforcement that obliges certification for export partners Mexico, Japan, and South Korea. Canada's voluntary data-sharing framework, adopted in 2024, incentivizes producers to submit diagnostic results in exchange for benchmarking, creating a positive feedback loop for laboratory growth. Mexico's pork production rose in 2025, and the integrated supply chain with the United States means disease events in one nation quickly elevate vaccine and diagnostic purchasing in the other.

Asia-Pacific is forecast to register a 7.54% CAGR during 2026-2031, marking the fastest regional advance in the swine healthcare market. China's directive that all inter-provincial pig movements pass PCR testing structurally elevates diagnostic volume, while localized ASF flare-ups sustain vaccine demand despite gradual herd rebuild. Vietnam scaled pork output to 4.8 million tonnes in 2025 on the back of biosecurity subsidies and an emergency-use ASF vaccine, yet the lack of peer-reviewed efficacy data tempers neighboring import approvals. India's urban middle class is increasing pork intake, but fragmented smallholder supply chains restrict veterinary service access, presenting future upside for low-cost thermostable vaccines.

Europe contributed significantly to global sales in 2025, led by Germany, Spain, and France, where animal-welfare rules and the zinc-oxide ban funnel expenditure into vaccines and feed additives with antibiotic-free claims. Spain shipped notable portion of pork to China in 2025, underscoring the region's stake in pathogen-free certification. Integrated Brazilian producers copy North American herd-health models to protect 1.2 million t of exports, channeling spend toward multinational vaccine and diagnostic suppliers. Middle East and Africa remain small, but South Africa's commercial sector and Nigeria's rapid herd expansion could unlock latent demand if cold-chain and veterinary staffing improve.

- ADM Animal Nutrition

- Alltech

- Boehringer Ingelheim Pharma GmbH & Co. KG

- Cargill Animal Nutrition

- Ceva

- DSM-Firmenich

- Elanco

- HIPRA Laboratories

- Huvepharma

- IDEXX

- IDVet

- Jinyu Bio-Technology

- Kemin Industries

- KM Biologics

- Merck

- Phibro Animal Health

- Thermo Fisher Scientific (Vet)

- Vaxxinova

- Vetoquinol

- Virbac

- Zoetis

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence of Endemic & Transboundary Swine Diseases

- 4.2.2 Expanding Global Pork Demand & Intensifying Production Systems

- 4.2.3 Surging R&D Spend on Novel Vaccines, Diagnostics & Feed Additives

- 4.2.4 Stricter Food-Safety / Preventive-Health Regulations Worldwide

- 4.2.5 Rapid Adoption of Precision-Livestock-Farming (PLF) Analytics

- 4.2.6 Growth Of Autogenous & Custom Vaccines in Vertically Integrated Herds

- 4.3 Market Restraints

- 4.3.1 Complex, Region-Specific Regulatory Approval Timelines & Costs

- 4.3.2 High Treatment & Vaccination Costs for Smallholders in Emerging Markets

- 4.3.3 Cold-Chain & Vaccine-Handling Gaps in Backyard / Informal Sectors

- 4.3.4 Gene-Edited ASF-Resistant Pig Lines Could Curb Future Demand

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Diagnostics

- 5.1.1.1 ELISA

- 5.1.1.2 Rapid Immuno Migration (RIM)

- 5.1.1.3 Polymerase Chain Reaction (PCR)

- 5.1.1.4 Diagnostic Imaging

- 5.1.1.5 Other Diagnostics

- 5.1.2 Therapeutics

- 5.1.2.1 Vaccines

- 5.1.2.1.1 Live Attenuated

- 5.1.2.1.2 Inactivated

- 5.1.2.1.3 Subunit / Recombinant

- 5.1.2.1.4 Autogenous / Custom

- 5.1.2.2 Parasiticides

- 5.1.2.3 Anti-infectives

- 5.1.2.4 Feed Additives

- 5.1.2.5 Other Therapeutics

- 5.1.2.1 Vaccines

- 5.1.1 Diagnostics

- 5.2 By Disease

- 5.2.1 Exudative Dermatitis (Greasy Pig)

- 5.2.2 Coccidiosis

- 5.2.3 Respiratory Diseases (incl. PRRS, MHyo)

- 5.2.4 Swine Dysentery

- 5.2.5 Porcine Parvovirus

- 5.2.6 Emerging Viral Diseases (ASF, Seneca Valley, PCV-3)

- 5.3 By End User

- 5.3.1 Large Integrated Swine Operations

- 5.3.2 Medium Commercial Farms

- 5.3.3 Smallholder / Backyard Farms

- 5.3.4 Veterinary Reference Laboratories

- 5.3.5 Government Animal-Health Agencies

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of APAC

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of MEA

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 ADM Animal Nutrition

- 6.3.2 Alltech

- 6.3.3 Boehringer Ingelheim Pharma GmbH & Co. KG

- 6.3.4 Cargill Animal Nutrition

- 6.3.5 Ceva Animal Health

- 6.3.6 DSM-Firmenich

- 6.3.7 Elanco Animal Health

- 6.3.8 HIPRA Laboratories

- 6.3.9 Huvepharma

- 6.3.10 IDEXX Laboratories

- 6.3.11 IDvet

- 6.3.12 Jinyu Bio-Technology

- 6.3.13 Kemin Industries

- 6.3.14 KM Biologics

- 6.3.15 Merck & Co., Inc.

- 6.3.16 Phibro Animal Health

- 6.3.17 Thermo Fisher Scientific (Vet)

- 6.3.18 Vaxxinova

- 6.3.19 Vetoquinol SA

- 6.3.20 Virbac

- 6.3.21 Zoetis Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment