|

시장보고서

상품코드

2063463

의료용 드론 배송 서비스 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Medical Drone Delivery Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

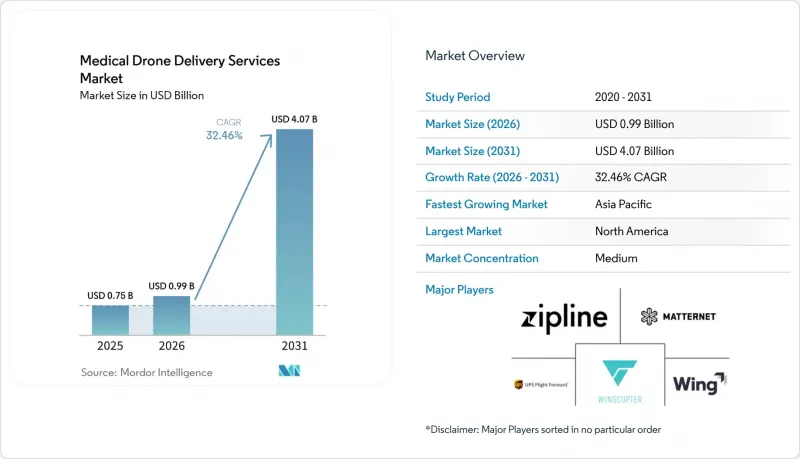

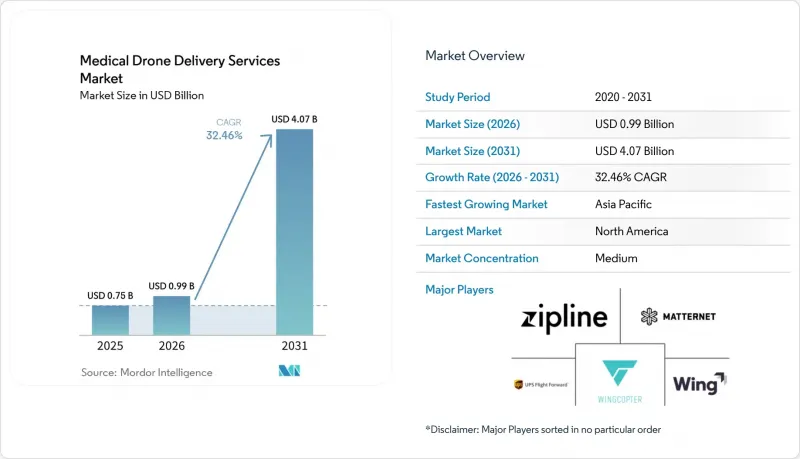

Mordor Intelligence에 의하면, 의료용 드론 배송 서비스 시장 규모는 2025년 7억 5,000만 달러로 평가되었고, 2026년에는 9억 9,000만 달러로 추정되고, 2031년까지 40억 7,000만 달러에 이를 것으로 예상되고 있으며, 2026-2031년 CAGR 32.46%로 성장할 전망입니다.

본 보고서는 용도별(혈액 수송, 백신 접종, 의약품, 장기 수송, 진단, 응급 키트), 플랫폼별(멀티로터, 고정익, 하이브리드 VTOL), 최종 사용자별(병원, 응급 의료 서비스(EMS), 혈액 은행, 정부 기관, 약국, 검사 기관), 배송 모델별(B2B, B2C, 긴급 배송), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카(MEA), 남미)로 분류되어 있습니다. 예상 금액은 달러(USD)로 표시되어 있습니다.

세계의 의료용 드론 배송 서비스 시장 동향 및 인사이트

드론 물류 시스템을 일상적으로 도입하는 국가 차원의 공중보건 프로그램

가나, 르완다, 인도의 정부 자금 지원 네트워크는 시범 운영 단계에서 제도적 조달 단계로 전환되었으며, 5년 이내에 전국적인 보급률을 달성하는 동시에 백신 폐기량을 최대 80%, 혈액 낭비를 67% 줄였습니다. 이러한 성과는 수요가 예측 가능하고, 도로 상황이 열악하며, 임상적 긴급성이 높은 경우, 의료용 드론 배송 서비스 시장이 지상 운송 수단을 대체할 수 있음을 보여줍니다. WHO의 2024년판 초저온 콜드체인 지침은 mRNA 백신 접종 캠페인에서 드론의 활용을 더욱 정당화하고, 예산 배분 지침을 제시하고 있습니다. 이에 따라 각 부처는 드론을 필수 의료 서비스 예산 항목에 포함시켜, 상업적 지속가능성을 뒷받침할 수 있는 안정적인 비행 횟수를 확보하고 있습니다.

BVLOS의 일상화가 1대 다 운용과 규모 확대를 가능하게 합니다.

제안된 미국 Part 108 규정 및 영국 민간항공청(CAA)의 2025년 로드맵은 감지 및 회피 기능, C2 링크, 항공 위험 평가에 관한 성능 기준을 법적으로 규정하고 있으며, 기존에는 면제 조치에만 의존하던 허가를 반복 가능한 인증으로 전환하고 있습니다. DroneUp사가 2024년에 획득한 BVLOS(시야 외 비행) 승인을 통해, 이 회사는 단일 허브에서 여러 월마트 약국으로 배송할 수 있게 되었으며, 배송 건당 인건비를 60% 절감했습니다. 유럽에서는 U-space 규정에 따라 27개 국가에서 전자적 가시성이 의무화되어 있으며, 국경을 넘어 사업을 영위하는 사업자는 EU를 단일 시장으로 취급할 수 있게 됩니다. 이러한 통합된 체계는 의료용 드론 배송 서비스 시장의 성장을 가속화할 것입니다. 왜냐하면 루트 확장이 새로운 면제 조치가 아니라, 소프트웨어 업데이트를 통해 확장 가능해졌기 때문입니다.

복잡하고 끊임없이 변화하는 BVLOS/공역 승인이 일상 업무를 제약하고 있습니다.

규제 마련이 진행되고는 있지만, 사업자들은 여전히 FAA의 면제 조치나 EASA의 SORA에 따른 12-24개월의 인증 절차를 거쳐야 하며, 이로 인해 사전 승인된 노선에 비해 투자 수익률(ROI)이 40-60% 하락하고 있습니다. 소규모 기업들은 수년에 걸쳐 지속될 자금 유출을 견뎌낼 자본력이 부족하기 때문에 자동화된 승인 포털이 완전히 정착될 때까지는 의료용 드론 배송 서비스 시장이 자금력이 풍부한 기존 기업들에게 유리한 상황이 계속될 것입니다.

부문별 분석

의료용 드론 배송 서비스 시장에서 혈액 수송이 가장 큰 비중을 차지하고 있으며, 2025년에는 35.31%를 나타낸 것으로 평가되었습니다. 이는 골든 아워 외상 프로토콜이나 산과적 출혈 사례에서 1시간 이내에 보충이 필요하기 때문입니다. 르완다의 네트워크는 2024년, 키갈리 이외 지역의 국내 혈액 공급량 중 4분의 3을 항공 운송으로 배달하여 사망률을 절반으로 줄이고 폐기량을 대폭 감축했습니다. 백신 접종 프로그램은 2위를 차지하고 있으며, WHO가 권장하는 초저온 드론 운송 경로를 활용해 외딴 지역의 진료소에 백신을 공급하고 있습니다. 검사 시료의 운송은 검사 결과의 신속성이 암이나 심장 질환의 치료 성과를 좌우하기 때문에 그 중요성이 커지고 있으며, 지방자치단체가 심정지 생존율을 10% 향상시키겠다는 목표를 내건 것을 배경으로, 응급용 AED의 배송량은 가장 급격한 증가세를 보이고 있습니다.

그러나 성장의 초점은 장기 및 조직 이식으로 옮겨가고 있으며, 2031년까지 연평균 성장률(CAGR) 33.64%로 확대될 것으로 전망됩니다. 이는 의료용 드론 배송 서비스 시장의 모든 용도 중 가장 높은 성장률입니다. Wingcopter 198과 같은 차세대 기체는 최대 6kg까지 적재할 수 있으며, 3곳으로의 동시 배송 임무를 수행할 수 있어, 이식 네트워크는 콜드체인 요건을 충족하면서 각막, 피부 이식편, 골수 운송 시험을 실시할 수 있게 됩니다. 또한, 2024년 FDA가 드론에 탑재되는 배터리 구동형 온도 로거를 승인한 것도 긍정적인 요인으로 작용하고 있습니다. 이번 변경을 통해 병원 조달팀은 고가 장기의 운송에 필요한 기록의 증빙을 확보할 수 있게 됩니다.

2025년 기준으로 고정익 항공기는 플랫폼 점유율의 45.21%를 차지했으며, 지방의 허브 앤 스포크 노선에서 톤킬로미터당 비용의 벤치마크로서 여전히 우위를 점하고 있습니다. 또한 일부 노선에서는 동일한 배터리 팩을 사용하더라도 멀티로터 기체보다 더 긴 비행 거리를 기록하고 있습니다. Zipline사의 'P2 Zip'은 3.5kg의 적재 용량으로 100km를 비행하며, 단일 거점에서 수십 개의 진료소에 서비스를 제공함으로써 이용률을 크게 높이고, 배송당 비용을 한 자릿수 수준으로 낮추고 있습니다. 그러나 의료용 드론 배송 서비스 시장은 하이브리드 VTOL 기체의 영향을 점점 더 많이 받고 있습니다. 사업자들이 좁은 도심 지역의 옥상에도 착륙할 수 있으면서도 외딴 농촌 거점까지 도달할 수 있는 단일 기체 군을 요구하는 가운데, 이 시장은 2031년까지 연평균 성장률(CAGR) 34.31%로 성장할 것으로 전망됩니다.

Wingcopter 198은 하이브리드 항공기로서의 매력을 여실히 보여주고 있습니다. 수직 이착륙이 가능하며, 6kg의 적재량으로 75km를 비행하고, 충전 없이 3회 연속 투하가 가능합니다. 이 기체는 현재 말라위와 아일랜드의 공중보건 시스템에서 운용되고 있습니다.

지역별 분석

북미는 지역별 매출액에서 가장 큰 비중을 차지하며 39.23%의 점유율을 기록했습니다. 이는 Part 135 인증 사업자 및 주 전체의 농촌 의료 프로그램에 의해 지원되고 있습니다. 2024년 노스캐롤라이나주에서 이 시스템이 도입됨에 따라, 애팔래치아 지역과 3차 의료 센터가 1시간 이내에 연결되었으며, 구불구불한 산길에 비해 드론이 지닌 비교우위가 입증되었습니다. 미국 재향군인부(VA)가 2025년에 실시하는 시범 사업은 연방 정부의 지원을 강화하기 위한 것으로, 2027년까지 50개 센터로 확대될 가능성이 있습니다. 같은 해, 캐나다에서 최초로 BVLOS(시야 외 비행)가 승인되어 원주민 커뮤니티에 대한 서비스 제공이 시작된 반면, 멕시코에서는 과달라하라의 의료 지구에서 지역 진료소까지 이어지는 샌드박스 회랑 구축 방안이 검토되고 있습니다.

아시아태평양은 가장 급격한 성장이 예상되며, 2031년까지 연평균 성장률(CAGR) 35.61%로 성장할 전망입니다. 인도의 2024년 드론 규정 개정에 따라 Skye Air Mobility사는 텔랑가나주에서 쌓은 성공 사례를 19개 주로 확대할 수 있게 되었으며, 한편 중국민용항공국(CAAC)이 지원하는 선전과 항저우의 저고도 시험 구역에서는 메가시티 규모의 도시 노선이 시험되고 있습니다. 일본은 ANA와 야마토 항공의 항공편을 통해 외딴 섬의 의료 격차 해소에 힘쓰고 있으며, 이는 호주 CASA의 승인을 받은 퀸즐랜드주의 네트워크를 본뜬 것입니다.

유럽에서는 2024년 U-space 규정의 시행이 호재가 되고 있습니다. 영국의 NHS는 Apian의 물류망을 활용해 병리 검체 운송 시간을 대폭 단축했으며, 독일은 주를 넘나드는 장기 검체 시범 사업에 자금을 지원하고, 아일랜드의 HSE는 지방의 일반의들을 위해 Wingcopter의 하이브리드 항공기를 도입했습니다. 중동 및 아프리카에는 가장 오랜 역사를 지닌 국가 차원의 드론 네트워크가 존재합니다. 가나의 6개 허브, 르완다의 전국적 커버리지, 케냐의 방사선 치료용 검체 운송 경로는 몬순 시즌을 포함해 연중 내내 높은 내구성을 보여주고 있습니다. 라틴아메리카는 다소 뒤처져 있지만, 브라질의 ANAC는 BVLOS(시야 밖 비행) 기준을 마련 중이며, 이는 의료용 드론 배송 서비스 시장의 새로운 가능성을 시사하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the medical drone delivery services market size is expected to increase from USD 0.75 billion in 2025 to USD 0.99 billion in 2026 and reach USD 4.07 billion by 2031, growing at a CAGR of 32.46% over 2026-2031.

This report is Segmented by Application (Blood Transfer, Vaccination, Drugs, Organ Transport, Diagnostics, Emergency Kits), Platform (Multirotor, Fixed-Wing, Hybrid VTOL), End-User (Hospitals, EMS, Blood Banks, Government, Pharmacies, Labs), Delivery Model (B2B, B2C, Emergency), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Forecasts are in Value (USD).

Global Medical Drone Delivery Services Market Trends and Insights

National-Scale Public-Health Programs Adopting Routine Drone Logistics

Government-funded networks in Ghana, Rwanda, and India have moved from demonstrations to institutional procurement, cutting vaccine spoilage by up to 80% and blood waste by 67% while achieving nationwide coverage within five years. These outcomes show that the medical drone delivery services market can displace ground fleets when demand is predictable, roads are poor, and clinical urgency is high. WHO's 2024 ultra-cold-chain guidance further legitimizes drones for mRNA campaigns, providing a template for budget allocation. Ministries are therefore bundling drones into their essential-health-services line items, ensuring steady flight volumes that underpin commercial sustainability.

BVLOS Normalization Enabling 1-to-Many Operations and Scale

The proposed U.S. Part 108 rule and the UK CAA's 2025 roadmap codify performance criteria for detect-and-avoid, C2 links, and air-risk assessment, turning waiver-only permissions into repeatable certifications. DroneUp's BVLOS approval in 2024 let it serve multiple Walmart pharmacies from one hub, slashing per-delivery labor costs by 60%. In Europe, U-space regulations mandate electronic conspicuity across 27 countries, letting cross-border operators treat the EU as a single market. These aligned frameworks accelerate the medical drone delivery services market because route expansion now scales through software updates rather than new exemptions.

Complex, Evolving BVLOS/Airspace Approvals Limit Routine Ops

Even with rulemaking underway, operators still navigate 12- to 24-month certification cycles under FAA waivers and EASA SORA, depressing ROI by 40-60% versus pre-approved corridors. Smaller firms lack the capital to endure multi-year burn, tilting the medical drone delivery services market toward well-funded incumbents until automated approval portals mature

Other drivers and restraints analyzed in the detailed report include:

- Hospital-at-Home and Telehealth Driving Small-Batch Prescription Fulfillment

- Cold-Chain Last-Mile for Temperature-Sensitive Vaccines and Biologics

- Weather, Payload, and Battery-Energy-Density Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Blood transfer controls the largest share of the medical drone delivery services market, with 35.31% in 2025, as golden-hour trauma protocols and OB hemorrhage cases demand sub-hour replenishment . Rwanda's network delivered three-quarters of national blood outside Kigali by air in 2024, halving mortality and slashing waste. Vaccination programs rank second, leveraging WHO-endorsed ultra-cold drone corridors to remote clinics. Diagnostic samples gain momentum as lab turnaround drives oncology and cardiac outcomes, and emergency AED drops post the steepest volume growth, as municipalities target 10% gains in cardiac-arrest survival.

The growth spotlight, however, is shifting to organ and tissue consignments, which are projected to expand at a 33.64% CAGR through 2031, the fastest rate among all applications in the medical drone delivery services market size. Next-generation airframes such as Wingcopter 198 can carry up to 6 kg and support triple-drop missions, enabling transplant networks to test cornea, skin-graft, and bone-marrow runs while meeting cold-chain requirements. Momentum also comes from the FDA's 2024 green light for battery-powered temperature loggers on drones, a change that gives hospital procurement teams the documentation trail they need for high-value organs.

Fixed-wing designs held 45.21% of platform share in 2025 and still set the benchmark for cost per ton-kilometer on rural hub-and-spoke lanes, with some routes posting longer endurance than multirotors on identical battery packs. Zipline's P2 Zip flies 100 km with 3.5 kg payloads, servicing dozens of clinics from a single dock and pushing utilization rates high enough to drop per-delivery costs into single-digit territory. The medical drone delivery services market, however, is increasingly influenced by hybrid VTOL airframes, which are forecast to grow at a 34.31% CAGR to 2031 as operators seek a single fleet that can land on tight urban rooftops while still reaching distant rural posts.

Wingcopter 198 typifies this hybrid appeal: it lifts vertically, cruises 75 km with a 6 kg payload, and can make three sequential drops without recharging, a profile now in use in Malawi and Ireland's public health systems.

Geography Analysis

North America generated the highest regional revenue, holding 39.23% share, underwritten by Part 135-certified operators and statewide rural-health programs. North Carolina's 2024 rollout links Appalachia to tertiary centers in under an hour, confirming drones' comparative advantage over winding mountain roads. The U.S. VA's 2025 pilot adds federal heft and may scale to 50 centers by 2027. Canada's first BVLOS approval in the same year serves Indigenous communities, while Mexico explores sandbox corridors from Guadalajara medical districts to regional clinics.

Asia-Pacific posts the steepest outlook, expanding at 35.61% CAGR through 2031. India's 2024 Drone Rules amendments let Skye Air Mobility replicate Telangana successes across 19 states, while CAAC-backed low-altitude pilot zones in Shenzhen and Hangzhou test urban corridors at megacity scale. Japan solves island medicine gaps via ANA and Yamato flights, mirroring Australia's CASA-approved Queensland network.

Europe benefits from 2024 U-space enforcement. The UK NHS slices the majority off pathology transit times with Apian routes, Germany funds cross-state organ sample pilots, and Ireland's HSE adopts Wingcopter hybrids for rural GPs. Middle East & Africa host the oldest national drone grids; Ghana's six hubs, Rwanda's countrywide coverage and Kenya's radiotherapy sample lanes demonstrate year-round resilience even through monsoons. Latin America lags but Brazil's ANAC is drafting BVLOS norms, hinting at new frontiers for the medical drone delivery services market.

- Apian

- Avy

- DHL Parcelcopter

- Drone Delivery Canada

- Jedsy

- Matternet

- MissionGO

- RigiTech

- Skye Air Mobility

- Skyports Drone Services

- Spright (Air Methods)

- Swoop Aero

- TechEagle

- UPS Flight Forward

- Vayu

- Wing

- Wingcopter

- Zipline

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 National-Scale Public Health Programs Adopting Routine Drone Logistics

- 4.2.2 BVLOS Normalization Enabling 1-To-Many Operations and Scale

- 4.2.3 Hospital-At-Home and Telehealth Driving Small-Batch Prescription Fulfillment

- 4.2.4 Cold-Chain Last-Mile for Temperature-Sensitive Vaccines and Biologics

- 4.2.5 Integration With Hospital/LIS/ERP For Automated Replenishment

- 4.2.6 UTM/ADSP Services Reduce Airspace Friction and Operational Cost

- 4.3 Market Restraints

- 4.3.1 Complex, Evolving BVLOS/Airspace Approvals Limit Routine Operations

- 4.3.2 Weather, Payload, And Battery-Energy-Density Constraints

- 4.3.3 Community Noise/Acceptance Constraints in Dense Areas

- 4.3.4 Unit Economics Sensitive to Labor Intensity Until 1-To-Many Is Routine

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Application

- 5.1.1 Blood & Plasma Transfer

- 5.1.2 Vaccination Programs

- 5.1.3 Drugs/Pharmaceuticals

- 5.1.4 Organ & Tissue Transport

- 5.1.5 Diagnostic Samples & Lab Logistics

- 5.1.6 Emergency Kits/AED/Antivenom

- 5.2 By Platform Type

- 5.2.1 Multirotor

- 5.2.2 Fixed-Wing

- 5.2.3 Hybrid VTOL

- 5.3 By Service Model

- 5.3.1 Hospitals & Health Systems

- 5.3.2 Emergency Medical Services (EMS)/Ambulance

- 5.3.3 Blood Banks & Transfusion Centers

- 5.3.4 Government & Public Health Programs

- 5.3.5 Pharmacies & Distributors

- 5.3.6 Laboratories/Pathology Networks

- 5.4 By Delivery Model

- 5.4.1 B2B Facility-to-Facility

- 5.4.2 B2C Home & Hospital-at-Home

- 5.4.3 Emergency Dispatch to Scene

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Apian

- 6.3.2 Avy

- 6.3.3 DHL Parcelcopter

- 6.3.4 Drone Delivery Canada

- 6.3.5 Jedsy

- 6.3.6 Matternet

- 6.3.7 MissionGO

- 6.3.8 RigiTech

- 6.3.9 Skye Air Mobility

- 6.3.10 Skyports Drone Services

- 6.3.11 Spright (Air Methods)

- 6.3.12 Swoop Aero

- 6.3.13 TechEagle

- 6.3.14 UPS Flight Forward

- 6.3.15 Vayu

- 6.3.16 Wing

- 6.3.17 Wingcopter

- 6.3.18 Zipline

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment