|

시장보고서

상품코드

2063464

살균 로봇 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Sanitization Robots - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

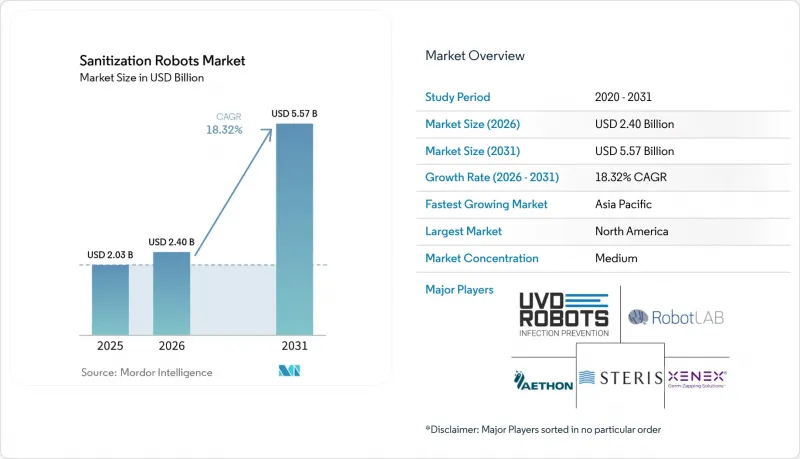

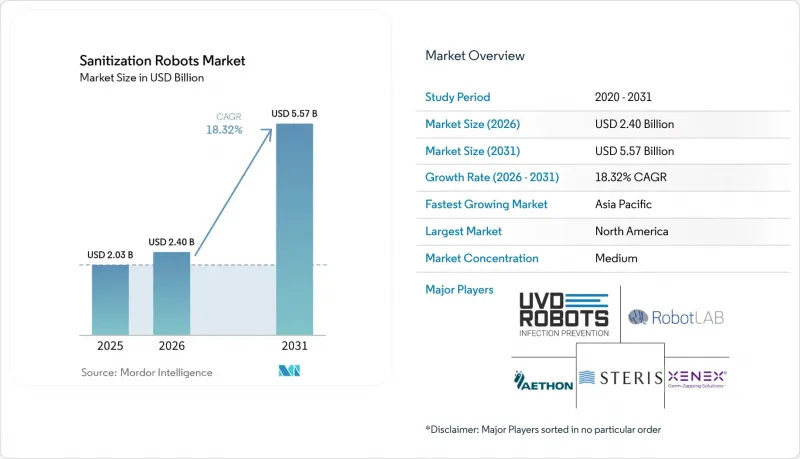

Mordor Intelligence에 의하면, 살균 로봇 시장 규모는 2025년 20억 3,000만 달러로 평가되었고, 2026년에는 24억 달러로 추정되며, 2026-2031년 CAGR 18.32%로 성장을 지속할 전망이며, 2031년까지 55억 7,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 유형별(UV-C 살균 로봇, 과산화수소 증기 로봇 등), 용도별(표면 소독, 공기 및 HVAC 소독 등), 기술별(자율형 로봇, 반자율형 로봇 등), 최종 사용자별(병원 및 진료소 등), 지역별(북미, 유럽, 아시아태평양 등)로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러) 기준으로 표시되어 있습니다.

세계의 살균 로봇 시장 동향 및 인사이트

증가하는 병원 내 감염(HAI)

HAI가 사망 위험을 높이고, 입원 기간을 연장하며, 총 비용을 증가시킨다는 증거가 계속해서 제시됨에 따라, 수동 청소를 보완하는 자동 소독 시스템의 도입이 촉진되고 있습니다. 미국의 데이터에 따르면, 병원 내 감염(HAI)과 관련된 입원은 HAI와 무관한 사례에 비해 사망률이 높고, 입원 기간의 중앙값도 더 길며, 특정 임상 범주에서는 총 비용의 중앙값이 현저히 높은 것으로 나타나, 의사 결정자들이 바이오버든을 체계적으로 줄이고 최종 청소 주기를 표준화할 수 있는 솔루션을 우선시해야 하는 이유를 뒷받침하고 있습니다. UV-C 장치 및 과산화수소 증기 시스템은 적절하게 적용될 경우 대조 시험에서 높은 불활성화 효과를 보였으며, 그 포자 살균율 및 실내 전체의 미생물 저감 효과는 여러 연구 및 업계 프로그램을 통해 입증되었습니다.

병원에서는 소독 작업을 반복 가능하고 감사 가능한 워크플로로 전환하기 위해 살균 로봇을 도입하여, 수작업에만 의존하던 방식에서 비롯된 편차를 줄이고 있습니다. 살균 로봇 시장은 숙련된 직원을 부가가치가 낮은 업무에서 해방시켜야 한다는 운영상의 필요성 외에도, 인증 및 보험사의 심사 기준이 되는 의료 환경 지표 개선이라는 이점을 누리고 있습니다. 표준화된 보고 및 감염 관리 감사가 확대됨에 따라, 디지털 문서화 및 추적 가능한 성과 데이터를 생성하는 플랫폼은 조달 결정 과정에서 더욱 유리한 위치를 차지하고 있습니다.

AI, IoT, 자율 항행 시스템의 도입 확대

자율성과 인식 기술의 발전으로 인해, 로봇은 원격 조종식 카트에서 공간 매핑, 작업 흐름 일정 설정, 결과 기록을 수행하는 자율 주행형 자산으로 점차 전환되고 있습니다. 로봇 플랫폼이 LiDAR, 비전, 클라우드 분석을 통합하여 가동률을 높이고 현장 팀의 교육 시간을 단축하고 있는 만큼, 대규모 다중 거점에서의 도입 사례는 이 기술 스택의 성숙도를 보여줍니다. 각 제조업체는 모듈형 자율주행 소프트웨어 및 청소 장비 제조업체와의 제휴를 바탕으로, 상당한 도입 실적을 달성하고 가동 중인 로봇 군의 확대를 보고하고 있습니다.

조사 데이터와 현장 검증 결과를 통해, 수동 청소를 보완하는 형태로 UV-C를 특정 부위에 집중적으로 조사함으로써, 특히 접촉 빈도가 높은 물체나 청소가 어려운 부위에서 효과가 향상된다는 사실이 입증되었습니다. 현재, AI를 활용한 조사 전략은 일부 공급업체에게 있어 제품의 핵심 분야로 자리 잡고 있습니다. IoT 기반 차량 관리를 통해 UV 광원, 배터리, 모터의 예측 유지보수가 가능해져, 예기치 못한 가동 중지 시간을 줄이고 부품 및 정비 주기와 관련된 비용 관리를 강화하고 있습니다. 따라서 살균 로봇 시장은 우선 비임상 분야의 자동화에 중점을 두고, 조직이 더 복잡한 임상용 AI에 착수하기 전에 신속한 운영 성과를 도출함으로써 실용적인 가치를 창출하는 방식으로 뒷받침되고 있습니다.

살균 로봇의 높은 초기 투자 비용 및 총 소유 비용

초기 설비 투자, 유지보수 및 가동 중단 위험은 특히 예산 압박을 받고 있는 시설의 경우, 도입 결정을 지연시키는 요인이 될 수 있습니다. 유지보수 분석에 따르면, 예기치 못한 가동 중단이나 사후 대응형 서비스 모델은 로봇 도입 시 기대 ROI를 저하시킨다는 사실이 밝혀졌으며, 로봇 군을 목표 가동률로 유지하기 위해서는 예측 유지보수, 부품 계획 및 문서화가 중요하다는 점이 부각되고 있습니다. 자금 면에서의 제약은 자본 예산이 인력 배치나 임상 장비와 경쟁 관계에 있는 지방이나 소규모 시설에서 더욱 두드러집니다. 이러한 경향은 병원 인건비 관련 조사에서도 나타나고 있으며, 추가적인 자동화 구독 서비스나 서비스 의존도가 높은 모델의 도입에 대해서는 신중한 태도를 취해야 함을 시사하고 있습니다.

주 차원의 보고서에서도 주요 지불자 범주에서 보상 마진의 악화가 기록되어 있으며, 이는 자본 부족을 더욱 심화시키고 있어, 공립 및 비영리 병원의 승인 절차에서 투자 회수 전망의 명확성이 필수적입니다. 따라서 구매자들은 병원 내 감염(HAI) 비용 회피 및 노동 생산성과 관련된 단기적인 투자 회수를 중시하고 있으며, 공간 전체에 대한 살균 승인 및 높은 포자 살균율 검증 결과가 특정 공간이나 업무 흐름에 대한 사업적 타당성을 강화하고 있습니다. 살균 로봇 시장은 비즈니스 모델을 지속적으로 발전시키고 있지만, 장기적인 투자 수익률(ROI)은 가동률, 부품 조달 체계, 그리고 감염 관리 우선순위와의 부합 여부에 달려 있습니다.

부문별 분석

2025년에는 UV-C 살균 로봇이 52.3%의 시장 점유율을 차지했으나, 과산화수소 증기 로봇은 2031년까지 연평균 성장률(CAGR) 19.34%로 성장할 것으로 전망됩니다. 이는 미국 식품의약국(FDA)이 과산화수소 증기를 '확립된 카테고리 A 멸균법'으로 인정함에 따라, 고도의 무균 환경에서의 도입이 촉진되고 있기 때문입니다. 이러한 상황에서 살균 로봇 시장에서는 병원이 신속한 대응이 필요한 업무에는 UV-C를 적용하고, 포자 살균 검증이나 잔류물이 없는 결과가 의사 결정의 기준이 되는 공간에는 VH2O2를 평가하는 경향이 지속되고 있습니다. VH2O2 적용 도입에 따른 살균 로봇 시장 규모는 통합형 촉매를 사용함으로써 수동 환기 과정 없이도 실내 전체의 미생물을 감소시킬 수 있음을 확인한, 여러 공간에서의 검증 결과에 의해 뒷받침되고 있습니다. 자율형 로봇이 수동 청소를 보완함으로써 접촉 빈도가 높은 표면의 소독 범위가 확대된다는 사실은 복도나 대기실 등 공용 공간에서 UV-C의 지속적인 사용을 뒷받침하고 있습니다. 또한, 각 업체들은 형태, 사각지대, 포자 내성에 대응하기 위해 닦아내기, UV-C, 증기 기능을 결합한 멀티 테크놀로지 플랫폼을 제공하고 있으며, 이를 통해 시설 운영 측은 공간의 요구 사항에 맞추어 방법을 선택할 수 있게 되었습니다.

VH2O2 플랫폼은 기준에 따라 일관된 포자 저감 효과와 추적 가능한 디지털 로그가 요구되는 구급차, 격리실 및 실험실을 대상으로 합니다. UV-C 플랫폼은 자율성, 커버리지의 일관성, 그리고 IEC 60335-2-65:2023을 준수하는 안전 인터록에 중점을 두고 있습니다. 이 규격은 UV 광원을 갖춘 부품에 관한 경고, 재료 및 절단 절차를 규정하고 있습니다. 살균 로봇 시장에는 정전기 분사 로봇도 포함되어 있어, 예산이 제한된 환경에서는 매력적이지만, 약제 보충 및 잔류물 발생 위험으로 인해 기기가 밀집된 공간에서의 사용은 제한됩니다. 병원 구매 담당자들은 공급업체 후보를 선정할 때 장비 수준의 승인 및 등록을 점점 더 중요하게 여기고 있으며, 다국적 승인 및 GPO(그룹 구매 조직)의 적용 범위가 경쟁상의 차별화 요소로 작용하고 있습니다. 기종에 관계없이 살균 로봇 시장은 포트폴리오 전략의 혜택을 받고 있으며, 각 의료 환경에서 방법 선택을 표준화하는 '룸 클래스' 프로토콜이 채택되고 있습니다.

2025년에는 표면 소독이 시장의 45.8%를 차지했으나, 시설들이 검증된 성능을 평가하는 기술 중립적 기준에 따라 감염성 에어로졸 제어 목표를 추구함에 따라, 공기 및 HVAC(공조) 소독은 2031년까지 연평균 성장률(CAGR) 22.21%를 나타낼 것으로 예측됩니다. 살균 로봇 시장은 이러한 변화에 대응하여 이동식 플랫폼과 덕트 내부 또는 실내 상부 솔루션을 결합함으로써, 노출 및 배출에 대한 안전 조치를 마련한 상태에서 실내에 사람이 있는 경우에도 병원체 저감 효과를 유지하고 있습니다. 공기 처리 적용 사례에서 살균 로봇 시장 규모는 가동 조건 하에서의 불활성화 및 조사 강도를 벤치마킹하는 시험 프로토콜의 혜택을 받고 있으며, 이를 통해 시설 관리자는 건물 개보수 프로그램 내 예산 배분을 정당화할 수 있게 됩니다. 사람이 머무는 구역에서는 오존 발생 및 2차 화학 반응에 주의를 기울이면서 원자외선(Far-UVC) 옵션을 검토하고 있으며, 시설 운영팀은 배출 및 노출 기준을 충족하기 위해 환기와 여과를 병행하고 있습니다. 로봇을 이용한 표면 소독과 지속적인 공기 정화를 통합한 하이브리드 청소 일정은 사람의 왕래가 잦은 구역에서 일관된 병원체 관리를 지원합니다.

공항 운영 사례는 일정 수립, 장비 조정 및 검증된 결과에 대한 참고 사례를 제공하며, 병원이나 공공시설이 어떤 환경에서도 운영 매뉴얼을 적용하는 데 도움이 되고 있습니다. 임상 공간에서는 천장 부근 및 덕트 내부를 대상으로 한 솔루션을 통해 환자 수가 정점에 달했을 때 수동 개입에 대한 의존도를 낮추었으며, 로봇을 이용한 표면 소독은 퇴실 후 청소 절차를 표준화하고 있습니다. 조달팀은 표면 소독 프로그램과 공기 처리 프로그램 간에 예산을 배분할 때, 장비 수준의 측정값, 공간의 형태, 이용자 밀도를 고려하여, 대개 감염 위험이 가장 높은 장소나 환자 통행량이 많은 장소를 기준으로 결정을 내립니다. 따라서 살균 로봇 시장은 표면 및 공기 모두에 대한 활용 사례가 확대되고 있으며, 신축 시설의 경우 사후 개조로 인한 장단점을 피하기 위해 설계 단계부터 두 가지 접근 방식을 모두 반영하고 있습니다.

지역별 분석

북미는 2025년에 45.13%의 시장 점유율을 차지한 것으로 평가되었으며, 규제 명확화, GPO(정부 조달 기관)의 활용, 그리고 환경 위생 분야의 자동화를 중시하는 병원들의 설비 투자 사이클로부터 계속해서 혜택을 보고 있습니다. 시장 전망은 임상 직군의 지속적인 이직률과 비용 압박을 보여주는 인력 데이터의 영향을 받고 있으며, 이로 인해 현장 직원을 비임상 업무에서 해방시키려는 움직임이 더욱 강화되고 있습니다. 승인 및 등록은 조달에 대한 신뢰를 뒷받침하며, 여기에는 미국 및 캐나다 전역의 임상 현장에서 허용되는 주장과 사용을 시사하는 플랫폼 수준의 이정표도 포함됩니다. 전국적인 GPO 계약을 통해 공급업체의 병원 네트워크 접근성이 개선되었으며, 로봇이 여러 거점에 걸친 서비스 제공 체계에 통합되었습니다. 이와 동시에, 해당 지역의 공항과 대규모 캠퍼스에서는 자율 주행 청소 로봇의 도입을 확대하고, 로봇의 운영 데이터를 건물 관리 시스템에 통합함으로써 야간 운영 일정을 최적화하고 넓은 면적을 효율적으로 관리하고 있습니다. 병원과 공항이 공통 운영 매뉴얼을 채택하고, 규정 준수, 문서화, 서비스 규모를 입증한 공급업체를 우선적으로 선정하는 가운데, 살균 로봇 시장은 성장세를 이어가고 있습니다.

유럽은 공급업체가 여러 국가에 진출하는 절차를 간소화해 주는 조화로운 안전 기준에 힘입어 여전히 중요한 지역입니다. 병원과 공항은 지속가능성 목표에 부합하는 ROI(투자 대비 효과) 및 수자원 회수율 지표를 문서화하여 자율 기술을 대규모로 도입하고 있으며, 주요 공항의 사례 연구에서는 로봇 군의 성능과 비용 절감 효과가 입증되었습니다. CE 마크 및 IEC 규격 준수는 위험 평가의 일원화에 기여하는 한편, 각 지역의 보상 제도와 자본 예산 규정이 병원 내 도입 속도를 좌우하고 있습니다. 북유럽 국가들은 공공 혁신 자금과 적극적인 탈탄소화 일정을 통해 시범 단계에서 본격적인 도입으로의 전환을 주도하는 경우가 많은 반면, 동유럽은 인건비가 저렴하기 때문에 일부 자동화 프로젝트의 경우 투자 수익률(ROI)을 회수하는 데 시간이 걸립니다. 살균 로봇 시장은 공급업체들이 규정 준수 문서와 공공 조달 담당자들이 조달 포털에서 요구하는 에너지 및 물 사용량 지표를 결합함으로써 발전하고 있습니다. 제약용 클린룸 및 GMP 관리 환경을 대상으로 한 국경을 초월한 파트너십은 UV-C 플랫폼의 잠재 시장을 더욱 확대되고 있습니다.

아시아태평양은 스마트 병원 프로젝트, 병상 수 확대, 공항 현대화에 힘입어 2026-2031년 연평균 성장률(CAGR) 19.60%로 가장 빠른 성장세를 보일 것으로 전망됩니다. 해당 지역의 구매자들이 중시하는 사항으로는 인구 밀집 도시 지역의 병원에서 감염 예방 효과와 노동 생산성 향상, 그리고 교통량이 많은 교통 허브에서의 일관성과 문서화가 포함됩니다. 한국과 일본에서의 조사 협력 및 새로운 플랫폼 도입은 하이브리드 설계와 노출 지침에 따른 실내 체류 시 안전 대책에 대한 관심을 높이고 있습니다. 이러한 성장의 일환으로, 세계 공급업체들은 유통업체 네트워크를 확대하고, 디지털 추적 기능을 갖춘 제약용 UV-C 제품 등 특정 분야에 특화된 제품을 제공합니다. 또한, 살균 로봇 시장은 배출물 안전성을 중시하는 공기 처리 및 플릿 보고서 기능을 갖춘 자율형 바닥 청소 기능을 높이 평가하는 운송 및 교육 분야의 공공 입찰을 통해 혜택을 보고 있습니다. 북미, 유럽, 아시아태평양 전반에서 규제 기준, 배출 시험 및 노출 과학이 설계와 조달을 좌우하는 한편, 수명 주기 분석과 유지보수 용이성은 경쟁 입찰 시 ROI(투자 대비 효과) 및 교체 여부를 결정하는 기준이 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the sanitization robots market size is expected to grow from USD 2.03 billion in 2025 to USD 2.40 billion in 2026 and is forecast to reach USD 5.57 billion by 2031 at 18.32% CAGR over 2026-2031.

This report is Segmented by Type (UV-C Disinfection Robots, Hydrogen Peroxide Vapor Robots, and More), Application (Surface Disinfection, Air & HVAC Disinfection, and More), Technology (Autonomous Robot, Semi-Autonomous Robots, and More), End User (Hospitals & Clinics, and More), and Geography (North America, Europe, Asia-Pacific and More). The Market and Forecasted in Terms of Value (USD).

Global Sanitization Robots Market Trends and Insights

Rising Hospital-Acquired Infections (HAIs)

Evidence continues to show that HAIs elevate mortality risk, lengthen hospital stays, and drive total cost, reinforcing the adoption of automated disinfection that complements manual cleaning. In U.S. data, HAI-associated hospital stays carried higher mortality and longer median length of stay than non-HAI cases, with sharply higher median total cost across select clinical categories, underscoring why decision-makers prioritize solutions that can systematically lower bioburden and standardize terminal cleaning cycles. UV-C devices and vaporized hydrogen peroxide systems demonstrate high levels of inactivation in controlled studies when applied correctly, with spore kill rates and whole-room microbial reduction validated in several research and industry programs.

Hospitals adopt sanitization robots to turn disinfection into a repeatable, auditable workflow, reducing variability from manual-only approaches. The sanitization robots market benefits from the operational need to free skilled staff from low-value tasks while improving environment-of-care metrics that factor into accreditation and payer scrutiny. As standardized reporting and infection control audits scale, platforms that create digital documentation and traceable performance data gain an added advantage in procurement decisions.

Growing Adoption of AI, IoT, and Autonomous Navigation Systems

Advances in autonomy and perception are shifting robots from remote-controlled carts to self-navigating assets that map spaces, schedule workflows, and document outcomes. Large multisite deployments illustrate the maturation of this stack, as robotics platforms integrate LiDAR, vision, and cloud analytics to raise utilization and reduce training time for frontline teams. Manufacturers report significant installed bases and active fleet growth, supported by modular autonomy software and partnerships with cleaning equipment.

Study data and field evidence also point to targeted UV-C application improving outcomes when it augments manual cleaning, especially on high-touch objects and difficult areas, with AI-driven exposure strategies now a product focus for some vendors. IoT fleet management enables predictive maintenance for UV sources, batteries, and motors, reducing unplanned downtime and tightening cost control on parts and service intervals. The sanitization robots market is therefore supported by a practical path to value that leans on nonclinical automation first, delivering quick operational wins before organizations pursue more complex clinical AI.

High Capital Cost and Total Cost of Ownership of Sanitization Robots

Initial capex, maintenance, and downtime risk can slow decisions, especially in facilities under budget pressure. Maintenance analytics show that unplanned downtime and reactive service models erode expected ROI in robotics deployments, highlighting the importance of predictive maintenance, parts planning, and documentation to keep fleets operating at target utilization. Financial constraints are more visible in rural and smaller facilities where capital budgets compete with staffing and clinical equipment, a pattern reflected in hospital labor expenditure studies that imply cautious adoption of additional automation subscriptions or service-heavy models.

State-level reporting has also documented negative reimbursement margins for key payer categories, which compounds capital scarcity and makes payback clarity essential for approval cycles in public and nonprofit hospitals. Buyers therefore emphasize short payback tied to HAI cost avoidance and labor productivity, with whole-room reduction authorizations and high spore kill validation strengthening the business case in certain rooms or workflows. The sanitization robots market continues to evolve its commercial models, but long-term ROI depends on uptime, parts logistics, and alignment with infection control priorities.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Smart Hospitals, Airports, and Smart City Infrastructure

- Increasing Regulatory Pressure for Infection Prevention Compliance

- Safety Concerns Related to UV-C Exposure and Human Interaction Limits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

UV-C disinfection robots held 52.3% in 2025, while hydrogen peroxide vapor robots are projected to expand at an 19.34% CAGR through 2031, with the FDA's recognition of vaporized hydrogen peroxide as an Established Category A sterilization method reinforcing adoption in high-sterility settings. In this context, the sanitization robots market continues to see hospitals apply UV-C for speed-sensitive turnover tasks and evaluate VH2O2 for rooms where spore kill validation and residue-free outcomes drive decision criteria. The sanitization robots market size for VH2O2-enabled deployments is supported by multi-room validation that confirms whole-room microbial reduction without manual ventilation steps when integrated catalysts are used. Evidence that high-touch surface coverage improves when autonomous robots augment manual cleaning supports continued UV-C utilization in general-purpose areas like corridors and waiting rooms. Vendors are also shipping multi-technology platforms that blend wiping, UV-C, and vapor capabilities to address geometry, shadowing, and spore tolerance, which lets facilities match method to room needs.

VH2O2 platforms target ambulances, isolation rooms, and labs where standards require consistent spore reductions and traceable digital logs. UV-C platforms focus on autonomy, coverage consistency, and safety interlocks aligned to IEC 60335-2-65:2023, which specifies warnings, materials, and disconnection instructions for components with UV sources. The sanitization robots market also includes electrostatic spray robots, which appeal in budget-constrained settings, although chemical replenishment and residue risks limit use in device-dense rooms. Hospital buyers increasingly evaluate device-level authorizations and registrations when shortlisting vendors, making multi-country approvals and GPO coverage competitive differentiators. Across types, the sanitization robots market benefits from a portfolio approach, with room-class protocols that standardize method selection for each environment of care.

Surface disinfection accounted for 45.8% in 2025, while air and HVAC disinfection is projected to grow at a 22.21% CAGR through 2031 as facilities pursue infectious aerosol control targets under technology-neutral standards that credit verified performance. The sanitization robots market aligns to this shift by pairing mobile platforms with in-duct or upper-room solutions that maintain pathogen reduction when rooms are occupied, subject to exposure and emissions safeguards. The sanitization robots market size for air handling use cases benefits from test protocols that benchmark inactivation or irradiance under operating conditions, enabling facility managers to justify allocations within building upgrade programs. In occupied zones, Far-UVC options are under evaluation with attention to ozone formation and secondary chemistry, and facility teams layer ventilation and filtration to satisfy emissions and exposure criteria. Hybrid cleaning schedules that integrate robotic surface disinfection with continuous air treatment support consistent pathogen control in high-footfall areas.

Airport operations offer reference cases on scheduling, fleet coordination, and validated results that help hospitals and public buildings translate playbooks across environments. In clinical spaces, upper-room and in-duct solutions reduce reliance on manual interventions during peak census while robotic surface disinfection standardizes turnover steps for terminal cleaning. Procurement teams weigh device-level measurements, room geometry, and occupant density when allocating budget between surface and air programs, often anchoring decisions to the locations that demonstrate the highest infection risk or patient throughput. The sanitization robots market therefore advances on both surface and air use cases, and new-build facilities are embedding both pathways at design stage to avoid retrofit tradeoffs.

Geography Analysis

North America held 45.13% in 2025 and continues to benefit from regulatory clarity, GPO leverage, and hospital capital cycles that emphasize automation for environmental hygiene. The market outlook is influenced by workforce data that show persistent turnover and cost pressure in clinical roles, which intensifies the push to free frontline staff from nonclinical work. Authorizations and registrations support procurement confidence, including platform-level milestones that signal allowable claims and use in clinical rooms across the U.S. and Canada. National GPO agreements improve vendor access to hospital networks and embed robots in multisite service offerings. In parallel, airports and large campuses in the region are expanding autonomous cleaning fleets and integrating robot performance data into building systems to optimize nighttime schedules and cover large floor areas. The sanitization robots market maintains momentum as hospitals and airports adopt common playbooks and prioritize vendors that demonstrate compliance, documentation, and service scale.

Europe remains a significant region supported by harmonized safety standards that simplify multi-country go-to-market work for vendors. Hospitals and airports adopt autonomy at scale with documented ROI and water recovery metrics that align with sustainability targets, with case studies from large airports demonstrating fleet performance and savings. CE marking and IEC-standard alignment help centralize risk assessments, while local reimbursement and capital budgeting rules shape the speed of hospital adoption. Nordic countries often lead on pilot-to-scale transitions due to public innovation funding and aggressive decarbonization timelines, while Eastern Europe's lower wages elongate ROI for some automation projects. The sanitization robots market advances as vendors pair compliance documentation with energy and water metrics that public buyers need for procurement portals. Cross-border partnerships that target pharmaceutical cleanrooms and GMP-controlled environments further extend addressable markets for UV-C platforms.

Asia-Pacific is projected to post the fastest growth at a 19.60% CAGR during 2026-2031, supported by smart hospital projects, hospital bed expansion, and airport modernizations. Buyer priorities in the region include infection prevention gains and workforce productivity in dense urban hospitals, and consistency and documentation in high-traffic transportation hubs. Research collaborations and new platform introductions within Korea and Japan add momentum around hybrid designs and in-occupancy safety considerations aligned to exposure guidelines. As part of this growth, international vendors are expanding distributor networks and segment-specific offerings, such as pharma-oriented UV-C variants with digital traceability. The sanitization robots market also benefits from public tenders in transport and education that value emissions-safe air treatment and autonomous floor care backed by fleet reporting. Across North America, Europe, and Asia-Pacific, regulatory standards, emissions testing, and exposure science shape engineering and procurement, while lifecycle analytics and serviceability define ROI and renewal in competitive bids.

- Aethon Inc.

- Akara Robotics Ltd.

- Dimer UVC Innovations

- Finsen Technologies Ltd.

- KEENON Robotics

- Nevoa Inc.

- OhmniLabs (OhmniClean)

- OMRON

- OTSAW Digital Pte. Ltd.

- RobotLAB Inc.

- SESTO Robotics Pte. Ltd.

- Skytron

- STERIS

- Surfacide LLC

- Taimi Robotics Technology Co., Ltd.

- Tru-D SmartUVC LLC

- UVD Robots ApS (Blue Ocean Robotics ApS)

- Xenex Disinfection Services Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Hospital-Acquired Infections (HAIs)

- 4.2.2 Growing Adoption of AI, IoT, and Autonomous Navigation Systems

- 4.2.3 Expansion of Smart Hospitals, Airports, and Smart City Infrastructure

- 4.2.4 Increasing Regulatory Pressure for Infection Prevention Compliance

- 4.2.5 EVS Labor Shortages and Wage Inflation Catalyze Automation Adoption

- 4.2.6 Evolving far-UVC Exposure Limits Enable In-Occupancy Disinfection Use-Cases

- 4.3 Market Restraints

- 4.3.1 High Capital Cost and Total Cost of Ownership of Sanitization Robots

- 4.3.2 Safety Concerns Related to UV-C Exposure and Human Interaction Limits

- 4.3.3 Mixed Real-World Efficacy Evidence Slows Procurement Decisions

- 4.3.4 Procurement Complexity (AMRs Vs Towers Vs HPV) Muddies ROI and Compliance

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 UV-C Disinfection Robots

- 5.1.2 Hydrogen Peroxide Vapor (HPV) Robots

- 5.1.3 Electrostatic Spray Robots

- 5.1.4 Hybrid / Multi-technology Robots

- 5.2 By Application

- 5.2.1 Surface Disinfection

- 5.2.2 Air & HVAC Disinfection

- 5.2.3 Room / Corridor Sanitization

- 5.2.4 Others

- 5.3 By Technology

- 5.3.1 Autonomous Robot

- 5.3.2 Semi-autonomous Robots

- 5.3.3 Remote-controlled Robots

- 5.4 By End User

- 5.4.1 Hospitals & Clinics

- 5.4.2 Government & Public Infrastructure

- 5.4.3 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Aethon Inc.

- 6.3.2 Akara Robotics Ltd.

- 6.3.3 Dimer UVC Innovations

- 6.3.4 Finsen Technologies Ltd.

- 6.3.5 KEENON Robotics

- 6.3.6 Nevoa Inc.

- 6.3.7 OhmniLabs (OhmniClean)

- 6.3.8 Omron Corporation

- 6.3.9 OTSAW Digital Pte. Ltd.

- 6.3.10 RobotLAB Inc.

- 6.3.11 SESTO Robotics Pte. Ltd.

- 6.3.12 Skytron LLC

- 6.3.13 STERIS

- 6.3.14 Surfacide LLC

- 6.3.15 Taimi Robotics Technology Co., Ltd.

- 6.3.16 Tru-D SmartUVC LLC

- 6.3.17 UVD Robots ApS (Blue Ocean Robotics ApS)

- 6.3.18 Xenex Disinfection Services Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment