|

시장보고서

상품코드

2063544

어레이 계측기 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Array Instruments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

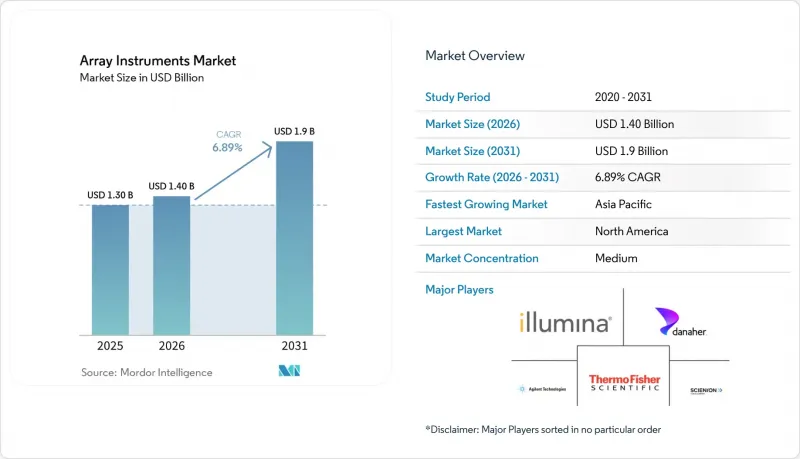

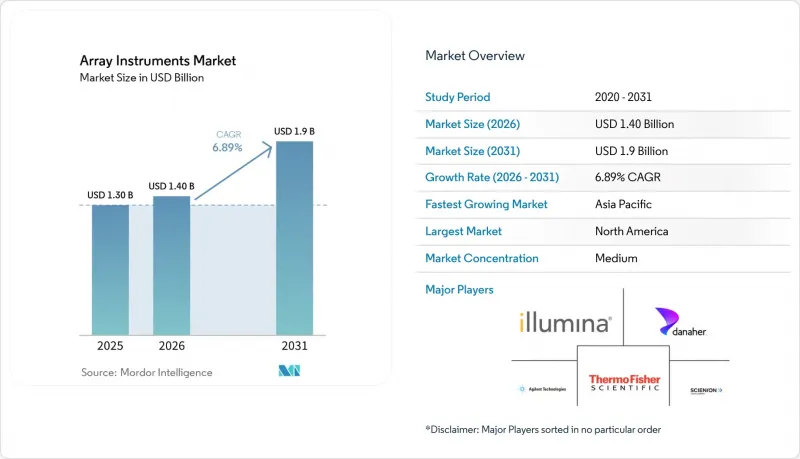

Mordor Intelligence에 의하면, 어레이 계측기 시장 규모는 2025년에 13억 달러로 평가되었습니다. 2026년 14억 달러에서 2031년까지 19억 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 6.89%를 나타낼 전망입니다.

본 보고서는 제품 유형(스캐너, 어레이어/스포터, 하이브리다이제이션/처리 시스템 등), 용도(유전자 발현, 유전형 분석, CMA, DNA 메틸화, 단백질 마이크로어레이 등), 최종 사용자(연구 기관, 제약/생명공학 기업, 임상 실험실, CRO, 정부 산하 연구소), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 어레이 계측기 시장 동향 및 인사이트

소아과 및 세포유전학 분야에서 CMA의 1단계 도입이 임상검사실의 스캐너 도입을 가속화

소아과학회 및 유전학회의 재검증을 거쳐, 염색체 마이크로어레이 검사는 발달 지연, 자폐 스펙트럼 장애 및 다발성 선천성 기형의 진단에 있어 첫 단계로 자리 잡았습니다. 지적 장애 코호트에서 진단율은 20%에 달하며, 기존의 핵형 분석에 비해 뚜렷한 개선이 나타납니다. CytoScan Dx 등 FDA 승인을 받은 검사법을 통해 병원은 검사를 원내에서 수행할 수 있게 되어, 외부 검사 의뢰를 절반으로 줄이고 연간 25만 달러 이상의 비용 절감을 실현하는 동시에, 미국 내 보험사의 지급 거절률도 낮추고 있습니다. 베일러 제네틱스(Baylor Genetics)와 같은 주요 검사 기관은 5,000개 이상의 유전자를 포괄하는 맞춤형 400K 어레이에 대해 2주간의 결과 보고 주기를 실현하고 있으며, 스캐너의 가동률을 높게 유지하고 있습니다. 상환 방식이 명확해지고 설비 투자 예산이 확보됨에 따라, 임상검사실에서는 지침에 따라 의무화된 검사량에 부합하도록 스캐너를 교체하거나 추가로 구입할 계획을 세우고 있습니다. 시퀀싱이 다른 분야에서 시장 점유율을 확대하고 있는 가운데에도, 이러한 요인들이 어레이 계측기 시장을 지탱하고 있습니다.

유전자 발현 및 유전자형 분석 어레이는 여전히 중개 연구의 워크플로우에서 핵심을 이루고 있습니다.

RNA-seq의 유연성에도 불구하고, 마이크로어레이는 확립된 파이프라인, 샘플당 비용이 저렴하다는 점, 분석 시간이 짧다는 점 등 고유한 장점을 가지고 있습니다. 종양학 분야의 비교 연구에 따르면, 특정 암종에서 마이크로어레이를 기반으로 한 단백질 예측 모델의 성능이 RNA-seq과 동등한 것으로 나타났습니다. 일루미나(Illumina)는 2025 회계연도에 어레이 소모품 부문에서 2억 9,700만 달러의 매출을 기록했는데, 이는 BeadArray 분석을 수행하는 iScan 및 NextSeq 550 하이브리드 시스템의 도입 규모가 여전히 크다는 사실을 뒷받침합니다. 93만 개의 프로브를 탑재한 EPIC v2.0 메틸화 어레이는 단일 스캐너로 주당 3,000개 이상의 샘플을 처리할 수 있어, 플랫폼의 연속성이 필수적인 종단적 코호트 연구에서 마이크로어레이는 없어서는 안 될 존재가 되었습니다. 많은 수의 프로브와 정액 요금제의 조합은 예산의 예측 가능성을 중시하는 연구소를 확실히 끌어들이고 있습니다. 이러한 요소들이 복합적으로 작용하여, 기기 시장의 어레이 분야가 급속한 대체 현상으로 인한 타격을 받지 않도록 보호하고 있습니다.

탐색 연구 및 다양한 유전형 분석/CNV 응용 분야에서 NGS의 대체 수단

시퀀싱 비용의 감소와 프로브에 의존하지 않는 광범위한 분석 범위 덕분에, NIH의 자금 지원과 학계의 관심은 RNA-seq, 전체 엑솜, 전체 유전체 분석으로 이동하고 있습니다. 미국 의학유전학회(ACMG)는 2024년, 일부 신경발달장애 적응증에 있어 유전체 시퀀싱이 CMA를 대체할 가능성이 있다고 밝혔습니다. 일루미나사의 어레이 매출은 2025년에 총 매출의 8%까지 감소한 반면, 시퀀싱은 큰 비중을 차지했습니다. 그러나 샘플 비용이 저렴하기 때문에 대규모 메틸화 역학 연구나 특정 농업 유전체학 워크플로우에서는 여전히 어레이가 선호되고 있습니다. 이러한 균형 덕분에 어레이 계측기 시장에서의 점유율 감소는 급격한 것이 아니라 완만한 양상을 보이고 있습니다.

부문별 분석

재현성을 높이기 위해 슬라이드 취급 및 세척 과정을 자동화하는 연구실이 늘어나면서, 하이브리다이제이션 및 처리 시스템 시장은 연평균 성장률(CAGR) 7.31%로 확대되고 있습니다. 이 부문의 급속한 성장은 성숙기에 접어든 스캐너 부문과는 대조적이지만, 스캐너는 2025년 어레이 계측기 시장의 매출액 중 43.18%를 차지했습니다. 가격대는 리퍼비시 제품인 GenePix(1만 6,500달러)부터 SpotLight Turbo 모델(7만 3,500달러)까지 폭넓게 구성되어 있어, 리소스 수준에 따른 예산에 맞추어 선택할 수 있습니다.

현재, 자동화 패키징이 조달의 핵심을 이루고 있습니다. 최신 처리 라인에서는 sCMOS 이미저와 바코드가 부착된 액체 핸들러를 결합하여, IVDR 감사 추적을 위해 데이터를 LIMS로 직접 전송하고 있습니다. 하이브리드화 시스템용 어레이 계측기 시장은 이러한 규정 준수 중심 수요를 활용할 준비가 되어 있는 한편, 높은 양자 효율을 실현하는 카메라의 혁신 덕분에 총비용 곡선은 양호한 상태를 유지하고 있습니다. 동남아시아와 아프리카의 신흥 시장에서는 레이저 방식의 이전 세대 기종을 건너뛰고 바로 이러한 이미저로 넘어가는 경향이 있어, 공급업체 입장에서는 신규 판매 대수 증가가 예상됩니다.

지역별 분석

북미는 FDA의 의료기기 승인 및 확립된 지불 체계에 힘입어 2025년 매출의 38.19%를 차지했습니다. CMA를 병원 내부로 이전하는 병원들이 소모품에 대한 지속적인 수요를 뒷받침하고 있습니다. 해당 지역의 안테나 장비 시장은 안정적이지만 성숙기에 접어들었으며, 신규 도입보다는 교체 수요가 판매 대수를 주도하고 있습니다.

아시아태평양은 시장의 견인차 역할을 하고 있으며, 2031년까지 연평균 성장률(CAGR) 7.39%로 성장하고 있습니다. 인도의 진단 시장이 급성장하고 있는 데다, 중국 국가의약품감독관리국(NMPA)의 의료기기 승인까지 더해지면서 스캐너와 하이브리다이저에 대한 잠재적 수요가 촉발되고 있습니다. 테마섹의 Molbio 투자와 노보 홀딩스의 MedGenome 투자 등 자금 유입을 통해, 새로운 검사실에 어레이와 시퀀서를 도입하기 위한 자금이 확보되었습니다.

유럽에서는 IVDR과 관련된 인증 대기 상황이 단기 매출을 끌어내리고 있지만, QIAstat-Dx와 같이 이미 CE 마크를 획득한 플랫폼의 존재는 규제 준수가 가능함을 보여주고 있습니다. 장기적인 업그레이드 주기는 소규모 키트 제조업체들이 더욱 엄격해진 규제 하에서 얼마나 신속하게 재인증을 획득할 수 있는지에 달려 있습니다. 한편, 라틴아메리카와 아프리카에서는 막대한 설비 투자를 피할 수 있는 시약 임대 계약에 포함된 카메라식 이미저가 채택되고 있어, 초기 도입 규모는 작지만 향후 도입 대수가 확대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the array instruments market size was valued at USD 1.30 billion in 2025 and is estimated to grow from USD 1.40 billion in 2026 to reach USD 1.9 billion by 2031, at a CAGR of 6.89% during the forecast period (2026-2031).

This report is Segmented by Product Type (Scanners, Arrayers/Spotters, Hybridization/Processing Systems, and More), Application (Gene Expression, Genotyping, CMA, DNA Methylation, Protein Microarrays, and More), End User (Research Institutes, Pharma/Biotech, Clinical Labs, Cros, Government Labs), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are in Value (USD).

Global Array Instruments Market Trends and Insights

CMA First-Tier Adoption in Pediatrics and Cytogenetics Accelerates Scanner Installs in Clinical Labs

Chromosomal microarray testing is entrenched as the first diagnostic step for developmental delay, autism spectrum disorder, and multiple congenital anomalies after reaffirmations by pediatric and genetics societies. Diagnostic yields reach 20% in intellectual-disability cohorts, a clear improvement over conventional karyotyping. FDA-cleared assays such as CytoScan Dx allow hospitals to internalize testing, cutting external send-outs in half and saving more than USD 250,000 annually, while also shrinking denial rates from U.S. payers. Leading reference labs like Baylor Genetics report two-week result cycles for custom 400K arrays covering over 5,000 genes, keeping scanner utilization high. As reimbursement clarity widens and capital budgets unlock, clinical labs are queuing follow-on purchases for replacement or additional scanners aligned with guideline-mandated volumes. These factors sustain the array instruments market even as sequencing gains share in other domains.

Gene Expression and Genotyping Arrays Remain Core in Translational Research Workflows

Despite the flexibility of RNA-seq, microarrays retain niche advantages such as mature pipelines, lower per-sample cost, and shorter analysis time. Comparative studies in oncology show microarray-based protein-prediction models perform on par with RNA-seq for selected cancers. Illumina logged USD 297 million in array consumables for fiscal 2025, underscoring a still-large installed base of iScan and NextSeq 550 hybrids that run BeadArray assays. The 930 K-probe EPIC v2.0 methylation array pushes weekly capacity over 3,000 samples on a single scanner, making microarrays indispensable for longitudinal cohort studies where platform continuity is critical. High probe counts coupled with flat pricing lock in laboratories that value predictable budgets. Collectively, these elements insulate a sizeable revenue stream within the array of instruments market from rapid substitution.

Substitution by NGS in Discovery and Many Genotyping/CNV Applications

Sequencing's declining cost and probe-independent breadth have shifted NIH funding and academic momentum toward RNA-seq, whole-exome, and whole-genome assays. The American College of Medical Genetics clarified in 2024 that genome sequencing may supersede CMA for some neurodevelopmental indications. Illumina's array revenue fell to 8% of total in 2025, while sequencing accounted for a significant share. Yet arrays remain preferred for large-scale methylation epidemiology and certain agrigenomics workflows due to lower sample cost. The balance yields gradual, not abrupt, erosion in the array instruments market.

Other drivers and restraints analyzed in the detailed report include:

- Academic and Pharma R&D Capex Refresh Cycles Favor Automated, Higher-Throughput Microarray Instruments

- Asia-Pacific Research Expansion and Molecular Diagnostics Uptake Increase Instrument Demand

- High Upfront Instrument Cost and Total Cost of Ownership

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybridization and processing systems are expanding at a 7.31% CAGR as labs automate slide handling and washing to lift reproducibility. This segment's faster pace contrasts with the mature scanner category, which still accounted for 43.18% of 2025 revenue in the array instruments market. Price dispersion ranges from refurbished USD 16,500 GenePix units to USD 73,500 SpotLight Turbo models, aligning budgets across resource tiers.

Automation bundling is now central to procurement; modern processing lines pair sCMOS imagers with bar-coded liquid handlers, feeding data directly to LIMS for IVDR audit trails. The array instruments market for hybridization systems is poised to capitalize on this compliance-driven demand, while camera innovations achieving high quantum efficiency keep total-cost curves favorable. Emerging markets in Southeast Asia and Africa often leapfrog to such imagers, bypassing laser-based predecessors and giving vendors new-unit upside.

Geography Analysis

North America accounted for 38.19% of 2025 revenue, driven by FDA device clearances and established payer frameworks. Hospitals transitioning CMA in-house underpin recurring consumable demand. The array instruments market in the region is steady but mature, with replacement rather than greenfield installs driving unit sales.

Asia-Pacific is the locomotive, expanding at a 7.39% CAGR through 2031. India's diagnostics boom, coupled with China's NMPA approvals for medical instruments, unlocks pent-up demand for scanners and hybridizers. Funding influxes, such as Temasek's backing of Molbio and Novo Holdings' stake in MedGenome, ensure capital is available to outfit new labs with arrays and sequencers.

Europe faces IVDR-linked certification queues that are dampening near-term sales, though CE-marked platforms like QIAstat-Dx show compliance is achievable. Long-run upgrade cycles hinge on how swiftly small kit makers can revalidate under the tighter regime. Elsewhere, Latin America and Africa are adopting camera-based imagers bundled under reagent-rental deals that sidestep heavy capex, thereby expanding the future install base, albeit from a low baseline.

- Agilent Technologies

- Arrayit

- Arrayjet

- Aurora Biomed

- BioDot

- CapitalBio Technology

- Danaher

- Grace Bio-Labs

- Illumina

- InDevR

- Innopsys

- LI-COR Biosciences

- M2-Automation

- Quansys Biosciences

- SCIENION

- SciGene

- Sensovation (Miltenyi Biotec)

- Tecan Group

- Thermo Fisher Scientific

- Toray Industries (3D-Gene)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 CMA First-Tier Adoption In Pediatrics and Cytogenetics Accelerates Scanner Installs In Clinical Labs

- 4.2.2 Gene Expression and Genotyping Arrays Remain Core in Translational Research Workflows

- 4.2.3 Academic And Pharma R&D Capex Refresh Cycles Favor Automated, Higher-Throughput Microarray Instruments

- 4.2.4 APAC Research Expansion and Molecular Diagnostics Uptake Increase Instrument Demand

- 4.2.5 Multiplexed Proteomic Microarrays in Vaccine and Immunology QA/QC Expand Need for Arrayers And Compact Imagers

- 4.2.6 Camera-Based Microarray Imaging Lowers TCO Vs. Laser-Confocal Scanners, Aiding Adoption In Cost-Constrained Labs

- 4.3 Market Restraints

- 4.3.1 Substitution By NGS (RNA-Seq, WES/WGS) In Discovery and Many Genotyping/CNV Applications

- 4.3.2 High Upfront Instrument Cost and Total Cost of Ownership (Scanners, Automated Processors)

- 4.3.3 Reimbursement Variability and Payer Utilization Controls Slow Clinical Uptake Outside Select Indications

- 4.3.4 Export Controls/Sanctions Limiting Access to Lasers/Optics/Electronics Curb Installs In Russia And Select Markets

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Microarray Scanners

- 5.1.2 Microarray Arrayers / Spotters

- 5.1.3 Hybridization / Processing Systems (washers, ovens, processors)

- 5.1.4 Automated Workstations & Autoloaders

- 5.2 By Application

- 5.2.1 Gene Expression Profiling

- 5.2.2 Genotyping / SNP Analysis

- 5.2.3 Chromosomal Microarray Analysis (aCGH/CMA)

- 5.2.4 DNA Methylation / Epigenetics

- 5.2.5 Protein Microarray Applications (proteomics, immunoassay)

- 5.2.6 Drug Discovery & Biomarker Discovery

- 5.3 By End User

- 5.3.1 Research & Academic Institutes

- 5.3.2 Pharmaceutical & Biotechnology Companies

- 5.3.3 Clinical / Diagnostic Laboratories

- 5.3.4 CROs & Service Providers

- 5.3.5 Government & Non-profit Laboratories

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Agilent Technologies

- 6.3.2 Arrayit Corporation

- 6.3.3 Arrayjet

- 6.3.4 Aurora Biomed

- 6.3.5 BioDot

- 6.3.6 CapitalBio Technology

- 6.3.7 Danaher Corporation

- 6.3.8 Grace Bio-Labs

- 6.3.9 Illumina, Inc.

- 6.3.10 InDevR

- 6.3.11 Innopsys

- 6.3.12 LI-COR Biosciences

- 6.3.13 M2-Automation

- 6.3.14 Quansys Biosciences

- 6.3.15 SCIENION

- 6.3.16 SciGene

- 6.3.17 Sensovation (Miltenyi Biotec)

- 6.3.18 Tecan Group

- 6.3.19 Thermo Fisher Scientific

- 6.3.20 Toray Industries (3D-Gene)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment