|

시장보고서

상품코드

2063562

통증 완화 패치 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Pain Relief Patches - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

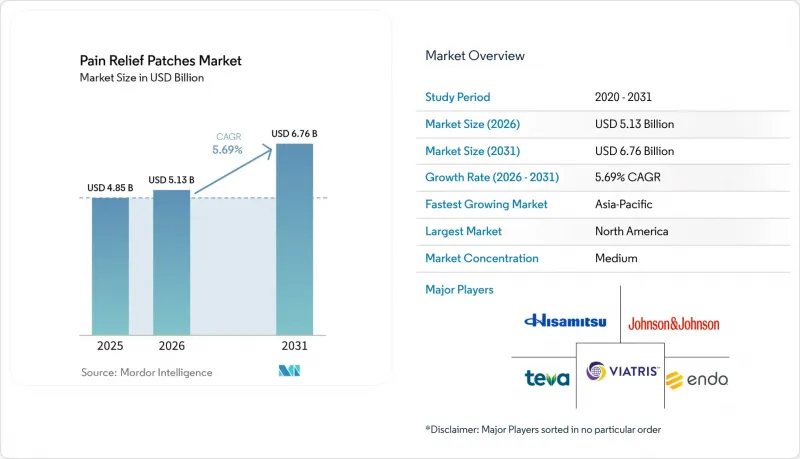

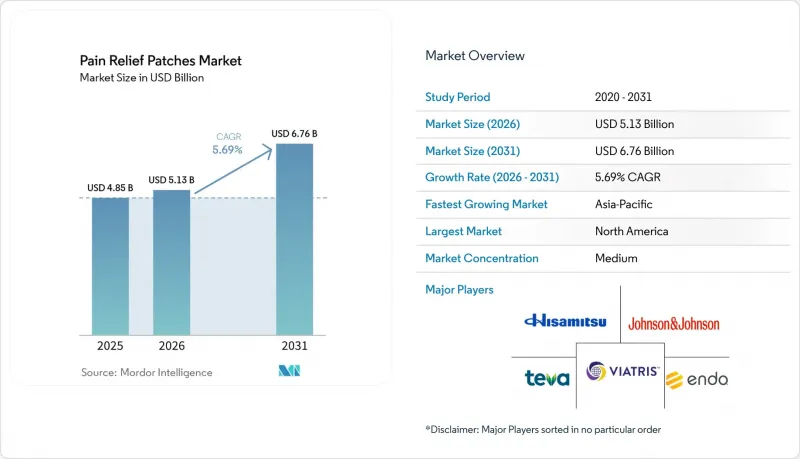

Mordor Intelligence에 의하면, 통증 완화 패치 시장 규모는 2025년 48억 5,000만 달러로 평가되었습니다. 2026년 51억 3,000만 달러에서 2031년까지 67억 6,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 5.69%를 나타낼 것으로 예측됩니다.

본 보고서는 제품 유형(오피오이드 패치, 비오피오이드 패치), 용도(만성 통증, 급성 통증 등), 유통 채널(병원 약국 등), 최종 사용자(병원, 재택치료, 클리닉·재활센터), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 통증 완화 패치 시장 동향 및 인사이트

소매 및 전자상거래 채널에서 일반의약품(OTC) 제품의 도입 가속화

일반의약품 중 경피 흡수형 제품은 약국 진열대에서 디지털 마켓플레이스로 점차 전환되고 있으며, 이로 인해 구매 과정이 간소화될 뿐만 아니라, 자주 이용하는 사용자에게 비용 효율을 높여주는 대용량 패키지를 제공할 수 있게 되었습니다. 히사미츠 제약은 표준 우편함에 들어갈 수 있도록 설계된 대용량 전자상거래용 옵션을 도입하여, 만성적인 사용자 편의성을 높이는 동시에 배송에 따른 탄소 배출량을 줄이고 있습니다. 온라인 채널로의 전환은 특수한 형태의 제품에 대한 접근성 확대로도 이어지고 있습니다. 소노마 파마슈티컬스가 미국의 주요 소매 체인점에서 화상용 하이드로겔 패치를 출시한 사례가 바로 그것입니다. 전자상거래 분야의 대용량 패키지는 제조업체에 가격 책정의 유연성을 제공할 뿐만 아니라, 만성 질환 환자의 복약 순응도를 높이는 정기 구매 모델을 뒷받침합니다. 경피 흡수형 제제에 관한 미국의 품질 기준 개정에서는 밀착성과 투여량의 균일성이 중시되고 있으며, 이로 인해 기존 대기업들이 유리한 입지를 차지하는 한편, OTC 시장의 성장도 촉진되고 있습니다. 이러한 요인들이 복합적으로 작용하여, 신속성, 편의성, 그리고 신뢰할 수 있는 브랜드를 추구하는 소비자 수요에 힘입어, 통증 완화 패치 시장에서 전자상거래 및 전국 규모의 소매업의 역할이 강화되고 있습니다.

고령화가 만성 통증의 유병률을 높입니다.

세계적인 고령화 추세에 따라, 전신에 미치는 영향을 최소화하는 국소적이고 지속적인 진통 솔루션에 대한 수요가 증가하고 있습니다. 2030년까지 전 세계 인구의 6분의 1이 60세 이상이 될 것으로 예상되며, 이는 장기적인 통증 관리가 필요한 만성 근골격계 질환 증가와 관련이 있습니다. 미국에서는 성인의 4분의 1 가까이가 만성 통증으로 고통받고 있으며, 고령층일수록 유병률이 높습니다. 지침에서는 고령자에게 특정 경구약의 사용에 주의를 기울일 것을 권고하고 있으며, 리도카인, 디클로페낙, 캡사이신 등의 외용제에 대한 의존도가 높아지고 있습니다. 연구에 따르면 고령자의 통증이 지속적이라는 점이 지적되고 있으며, 경피 흡수형 제제를 포함한 개별화된 다각적인 접근 방식의 필요성이 강조되고 있습니다. 의료 종사자들이 고령 환자에 대해 일관된 치료 성과와 약물 위험 감소를 우선시함에 따라, 이러한 추세가 통증 완화 패치에 대한 수요를 뒷받침하고 있습니다.

피부 자극 및 부착 불량

피부 반응이나 접착력 문제는 제품 사용 중단을 초래하는 주요 요인이며, 리콜 사례는 실제 사용 시 접착력이나 박리 성능이 불충분할 때 발생하는 결과를 여실히 보여주고 있습니다. 2025년 초, 특정 펜타닐 경피 흡수 제제의 일부 로트가 점착성 결함으로 인해 리콜되었습니다. 이는 간병인이나 가족에게 약물 잔류로 인한 노출 위험을 초래하는 것이었습니다. 2024년 말에 확인된 규정 준수 문제는 외용 진통제에 대해 엄격한 접착력 시험 프로토콜과 로트 출하 관리가 필수적임을 여실히 보여주었습니다. OTC 리도카인 제품으로 인한 국소적인 피부 반응이나 접촉성 피부염 등의 이상반응 보고가 이어지면서, 저자극성 접착제와 다양한 피부 유형에서 일관된 접착력을 확보하는 데 대한 관심이 높아지고 있습니다. 각 제조업체들은 접착력과 통기성의 균형을 맞추고 자극의 위험을 줄이기 위해 실리콘계 및 하이드로콜로이드계 접착 시스템을 채택하는 경향이 강해지고 있습니다. 시장 감시를 강화하고 표시 관행을 개선함으로써, 판매 중단 및 리콜을 최소화하고 통증 완화 패치 시장의 성장을 뒷받침하는 것을 목표로 하고 있습니다.

부문별 분석

2025년, 비오피오이드계 패치는 통증 완화 패치 시장의 62.34%를 차지했으며, 만성 비암성 통증에 대한 오피오이드계 치료에서 비오피오이드계 치료로의 전환을 배경으로 2031년까지의 연평균 성장률(CAGR)은 8.10%를 나타낼 것으로 전망됩니다. 이 시장은 특히 다제 병용 요법을 받고 있거나 동반 질환이 있는 고령 환자에게 비오피오이드계 치료를 권장하는 표시 변경 및 안전 권고에 힘입어 성장하고 있습니다. 각 제약사는 12-24시간에 걸쳐 안정적으로 약물을 방출하는 얇고 착용감이 편안한 패치를 제공하기 위해 약물 함유 접착제 플랫폼의 혁신에 주력하고 있으며, 이를 통해 복약 순응도가 향상되고 추가 투약의 필요성이 줄어들고 있습니다. 업계에서는 치료의 지속성을 높이는 연포장 및 장시간 착용 설계에 힘입어, 다양한 요구에 부응하기 위해 비오피오이드 제제 및 규격의 확충이 진행되고 있습니다.

2025년에는 만성 통증 치료 용도가 시장의 44.23%를 차지했습니다. 이는 퇴행성 관절염, 요통, 신경 장애 등의 증상을 안정화시키는 서방형 제제가 주도한 결과입니다. 임상 지침에서는 고령자에게 경구약에 수반되는 위험을 줄일 수 있는 외용제를 권장하고 있습니다. 경구 투여를 최소화하면서도 일상생활을 영위할 수 있게 해주는 장시간 지속형 패치에 대한 수요가 증가하고 있으며, 비오피오이드 제제의 밀착성과 착용감이 개선됨에 따라 일관된 통증 완화가 보장되고 증상의 변동이 줄어들고 있습니다.

스포츠 관련 통증 시장은 가장 빠르게 성장하고 있는 부문으로, 자가 관리 트렌드, 온라인 구매 편의성, 그리고 훈련 및 회복 과정에서의 국소 투여의 이점에 힘입어 2031년까지 연평균 성장률(CAGR)이 7.60%를 나타낼 것으로 전망됩니다. 근육이나 관절에 직접 붙이는 패치는 잦은 투여로 인한 중단 없이 활동을 할 수 있게 해줍니다. 멘톨, 메틸살리실산 또는 리도카인을 함유한 일반의약품(OTC) 제품은 훈련 일정에 맞춘 정기 구매 및 멀티팩 제공에 힘입어 소매 시장에서 입지를 유지하고 있으며, 이 부문의 성장을 지속시키고 있습니다.

지역별 분석

2025년, 북미는 통증 완화 패치 시장 점유율의 39.67%를 차지했으나, 아시아태평양은 2031년까지 연평균 성장률(CAGR)이 8.50%를 나타낼 것으로 예측되어 가장 빠르게 성장하는 지역으로 부상했습니다. 미국에서는 2025년 오피오이드 패치의 표시 변경에 따라, 만성 비암성 통증에 대한 국소 비오피오이드 진통제로의 전환이 촉진되었습니다. 미국 성인의 만성 통증 유병률이 높다는 점은 일상생활 기능을 지원하는 장시간 지속형 패치에 대한 수요를 이끌고 있습니다. 전문용 패치는 일관되고 강력한 진통이 필요한 증례에 대응하기 위해 종양학 및 완화의료 분야에서 여전히 필수적입니다.

유럽에서는 통증 완화 패치 시장에서 규제 당국의 엄격한 위험-이익 관리가 반영되면서, 지속 가능한 포장 및 소재에 대한 관심이 높아지고 있습니다. 2024년 고효능 경피 흡수형 제제에 관한 안전성 정보가 갱신됨에 따라, 환자 선정 기준과 위험 완화 조치가 더욱 세분화되었습니다. 환경에 대한 우려로 인해 재활용 가능하거나 생분해성 소재에 대한 관심이 높아지고 있는 반면, 제품의 안전성은 확립된 생체적합성 기준을 준수하고 있습니다. 각국에서는 의료 폐기물 문제를 해결하기 위한 생산자 책임 제도의 도입을 검토하고 있습니다. OTC(일반의약품) 및 비오피오이드계 패치는 대용량 팩 옵션의 확대와 교육 컨텐츠의 확충을 통해 약국 및 온라인 플랫폼에서 보급이 확대되고 있습니다.

가장 빠르게 성장하고 있는 아시아태평양은 소득 증가, 일본 등 일부 국가의 고령화, 그리고 소매 및 디지털 약국의 확산으로 인한 혜택을 누리고 있습니다. 이 시장은 강력한 브랜드의 입지와 외용약에 대한 소비자의 친숙함에 힘입어 2031년까지 연평균 성장률(CAGR) 8.50%를 기록하며 성장할 것으로 전망됩니다. 히사미츠 제약과 같은 기업들은 혁신적인 제품 디자인과 전자상거래 전략을 활용하여, 확실한 배송과 재구매를 가능하게 하는 얇아서 우편함에 들어갈 수 있는 포장을 제공합니다. 헬스케어 서비스 이용 기회 확대와 셀프케어 카테고리의 확충은 일상생활에 미치는 지장을 최소화하면서 특정 증상을 완화하고자 하는 소비자의 요구와 부합합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the pain relief patches market size is projected to expand from USD 4.85 billion in 2025 and USD 5.13 billion in 2026 to USD 6.76 billion by 2031, registering a CAGR of 5.69% between 2026 to 2031.

This report is Segmented by Product Type (Opioid Patches, Non-Opioid Patches), Application (Chronic Pain, Acute Pain, and More), Distribution Channel (Hospital Pharmacies, and More), End User (Hospitals, Home-Care Settings, Clinics & Rehabilitation Centers), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Pain Relief Patches Market Trends and Insights

Accelerated OTC Adoption in Retail & E-Commerce Channels

Over-the-counter transdermal products are increasingly moving from pharmacy shelves to digital marketplaces, streamlining the purchasing process and enabling larger unit sizes that improve cost efficiency for frequent users. Hisamitsu has introduced bulk-format e-commerce options designed to fit standard mailboxes, enhancing convenience for chronic users while reducing delivery-related emissions. The shift to online channels is also expanding access to specialty formats, as seen with Sonoma Pharmaceuticals' launch of a burn-relief hydrogel patch in major U.S. retail chains. Larger pack sizes in e-commerce provide manufacturers with greater pricing flexibility and support subscription models that encourage adherence for long-term conditions. Updated U.S. quality standards for transdermal systems emphasize adhesion and dose consistency, favoring established players while supporting OTC market growth. These factors collectively strengthen the role of e-commerce and national retail in the pain relief patches market, driven by consumer demand for speed, convenience, and trusted brands.

Aging Population Driving Chronic Pain Prevalence

The aging global population is driving demand for localized, sustained pain relief solutions that minimize systemic exposure. By 2030, one-sixth of the global population is expected to be 60 or older, correlating with a rise in chronic musculoskeletal conditions requiring long-term pain management.In the U.S., chronic pain affects nearly a quarter of adults, with higher prevalence among older age groups. Guidelines caution against certain oral medications for seniors, increasing reliance on topical formulations like lidocaine, diclofenac, and capsaicin. Studies highlight the persistence of pain in older adults, emphasizing the need for personalized and multimodal approaches, including transdermal options. These trends sustain demand for pain relief patches as healthcare providers prioritize consistent treatment outcomes and reduced medication risks for aging patients.

Skin-Irritation & Adhesion Failures

Dermal reactions and adhesion issues are key factors driving product discontinuation, with recalls underscoring the consequences of inadequate adhesion or release performance in practical use. In early 2025, specific fentanyl transdermal lots were recalled due to adhesion failures, which posed risks of residual drug exposure to caregivers and household members. Compliance issues identified in late 2024 highlighted the critical need for stringent adhesion testing protocols and batch-release controls for topical analgesics. Reports of adverse events, such as local skin reactions and contact dermatitis from OTC lidocaine products, have intensified the focus on hypoallergenic adhesives and consistent adhesion across various skin types. Manufacturers are increasingly adopting silicone- and hydrocolloid-based adhesive systems to balance tack and breathability, reducing irritation risks. Enhanced market surveillance and updated labeling practices aim to minimize discontinuities and recalls, supporting growth in the pain relief patches market.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push Away from Systemic Opioids

- Technological Advances in Drug-in-Adhesive & Microneedle Patches

- Stringent FDA / EMA Clinical-Trial Cost & Timeline

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, non-opioid patches captured 62.34% of the pain relief patches market, with an expected CAGR of 8.10% through 2031, driven by a shift from opioid-based treatments for chronic non-cancer pain. The market is supported by labeling changes and safety advisories encouraging non-opioid options, particularly for older patients with polypharmacy and comorbidities. Manufacturers are innovating drug-in-adhesive platforms to deliver thin, comfortable patches with consistent release over 12-to-24-hour windows, enhancing adherence and reducing the need for rescue medication. The industry is expanding non-opioid formulations and sizes to cater to diverse needs, supported by flexible packaging and long-wear designs that improve therapy persistence.

Chronic pain applications accounted for 44.23% of the market in 2025, driven by sustained-release delivery that stabilizes symptoms in conditions like osteoarthritis, lower back pain, and neuropathy. Clinical guidelines favor topical solutions for older adults, reducing risks associated with oral medications. Long-wear patches that enable daily activities while minimizing oral dosing are in demand, supported by improved adhesion and comfort in non-opioid designs, ensuring consistent relief and reducing variability.

Sports-related pain is the fastest-growing segment, with a projected CAGR of 7.60% through 2031, fueled by self-care trends, online availability, and localized delivery benefits during training or recovery. Patches applied directly to muscles or joints allow activity without frequent dosing interruptions. OTC formats with menthol, methyl salicylate, or lidocaine maintain strong retail presence, supported by subscription and multi-pack offers catering to training schedules, sustaining growth in this segment.

Geography Analysis

In 2025, North America captured 39.67% of the pain relief patches market share, while Asia-Pacific emerged as the fastest-growing region with an 8.50% CAGR projected through 2031. In the United States, updated opioid patch labeling in 2025 encouraged a shift toward topical non-opioid analgesics for chronic non-cancer pain. The high prevalence of chronic pain among U.S. adults drives demand for long-wear patches that support daily functionality. Specialty patches remain critical for oncology and palliative care, addressing cases requiring consistent and strong analgesia.

In Europe, the pain relief patches market reflects stringent benefit-risk management by regulators and a growing focus on sustainable packaging and materials. Safety updates for high-potency transdermals in 2024 refined patient selection and risk mitigation practices. Environmental concerns are driving interest in recyclable or biodegradable materials, while product safety adheres to established biocompatibility standards. National initiatives are exploring producer responsibility programs to address healthcare waste. OTC and non-opioid patches are gaining traction in pharmacies and online platforms, supported by larger pack options and educational content.

Asia-Pacific, the fastest-growing region, benefits from rising incomes, aging demographics in countries like Japan, and improvements in retail and digital pharmacy reach. The market is projected to grow at an 8.50% CAGR through 2031, supported by strong brand presence and consumer familiarity with topical solutions. Companies like Hisamitsu leverage innovative product designs and e-commerce strategies, offering thin, mailbox-compatible packs for reliable delivery and repeat usage. Expanding healthcare access and self-care categories align with consumer preferences for targeted relief with minimal disruption to daily routines.

- 3M

- Abbott Laboratories

- Bayer

- Endo International

- Grunenthal GmbH

- GlaxoSmithKline

- Hisamitsu Pharmaceutical

- IBSA Institut Biochimique SA

- Johnson & Johnson

- Mentholatum Company

- NEXGEL, Inc.

- Novartis

- Pfizer

- Sanofi

- Sorrento Therapeutics

- Teikoku Pharma USA

- Teva Pharmaceutical Industries

- Topical BioMedics

- UCB

- Viatris

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated OTC Adoption in Retail & E-Commerce Channels

- 4.2.2 Aging Population Driving Chronic Pain Prevalence

- 4.2.3 Regulatory Push Away from Systemic Opioids

- 4.2.4 Technological Advances in Drug-in-Adhesive & Microneedle Patches

- 4.2.5 Smart Patch R&D Linking Sensors with Companion Apps

- 4.2.6 ESG-Driven Shift to Bio-Degradable Patch Substrates

- 4.3 Market Restraints

- 4.3.1 Skin-Irritation & Adhesion Failures

- 4.3.2 Stringent FDA / EMA Clinical-Trial Cost & Timeline

- 4.3.3 Disposal-Related Environmental Scrutiny

- 4.3.4 Counterfeit Patches in Low-Regulation E-Commerce

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Opioid Patches

- 5.1.2 Non-Opioid Patches

- 5.2 By Application

- 5.2.1 Chronic Pain

- 5.2.2 Acute Pain

- 5.2.3 Post-Operative Pain

- 5.2.4 Sports & Injury-Related Pain

- 5.3 By Distribution Channel

- 5.3.1 Hospital Pharmacies

- 5.3.2 Drug & Retail Pharmacies

- 5.3.3 Online Providers

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Home-Care Settings

- 5.4.3 Clinics & Rehabilitation Centres

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 3M Company

- 6.3.2 Abbott Laboratories

- 6.3.3 Bayer AG

- 6.3.4 Endo International plc

- 6.3.5 Grunenthal GmbH

- 6.3.6 GSK plc

- 6.3.7 Hisamitsu Pharmaceutical Co., Inc.

- 6.3.8 IBSA Institut Biochimique SA

- 6.3.9 Johnson & Johnson (Janssen)

- 6.3.10 Mentholatum Company

- 6.3.11 NEXGEL, Inc.

- 6.3.12 Novartis AG

- 6.3.13 Pfizer Inc.

- 6.3.14 Sanofi SA

- 6.3.15 Sorrento Therapeutics, Inc.

- 6.3.16 Teikoku Pharma USA

- 6.3.17 Teva Pharmaceutical Industries Ltd.

- 6.3.18 Topical BioMedics, Inc.

- 6.3.19 UCB Pharma

- 6.3.20 Viatris Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment