|

시장보고서

상품코드

2063607

땅콩 알레르기 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Peanut Allergy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

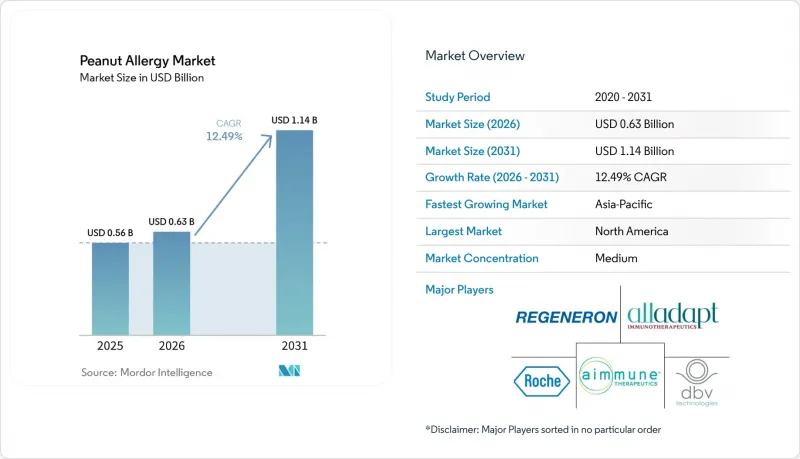

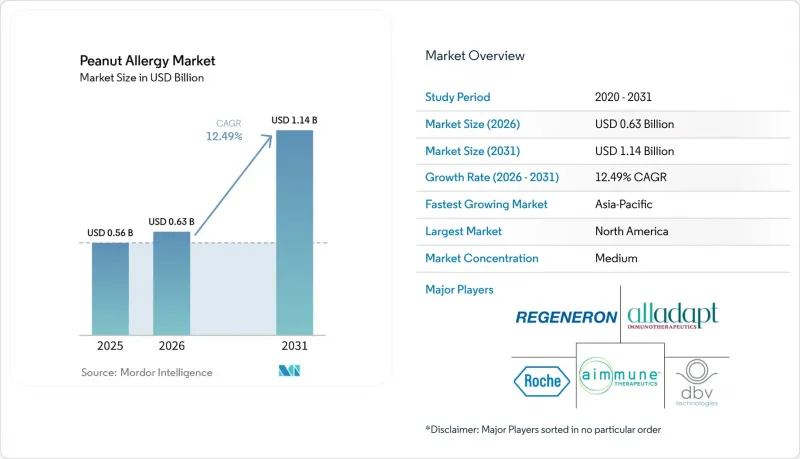

Mordor Intelligence에 의하면, 땅콩 알레르기 시장 규모는 2025년 5억 6,000만 달러에서 2026년에는 6억 3,000만 달러로 확대되어 2031년까지 11억 4,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 12.49%로 성장할 전망입니다.

본 보고서는 치료법/치료 방식(면역요법, 에피네프린, 항히스타민제, 기타), 투여 경로(경구, 주사, 기타), 환자 연령대(유아, 소아·청소년, 성인) 및 지역(북미, 유럽, 아시아·태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러) 기준으로 표시되어 있습니다.

세계 땅콩 알레르기 시장 동향 및 인사이트

항-IgE 생물학적 제제의 승인으로 인해 치료 대상이 되는 환자층이 확대되었습니다.

2024년 2월, IgE 매개 식품 알레르기에 대한 오말리주맙의 승인이 내려짐에 따라, 치료의 초점은 단일 알레르겐에 대한 탈감작에서 여러 식품에 걸친 우발적 노출에 대한 예방으로 전환되었습니다. 이는 여러 가지 알레르기를 동시에 앓고 있는 가족에게 있어 일상적인 위험 관리와 부합하는 것입니다. 주요 OUTMATCH 임상시험 데이터에 따르면, 치료군 참가자의 68%가 중등도에서 중증의 증상 없이 최소 600mg의 땅콩 단백질을 섭취할 수 있었던 반면, 위약군에서는 5%에 그쳤습니다. 또한, 실생활에서의 노출과 관련된 역치에서 우유, 달걀, 캐슈넛에 대한 내성도 동시에 향상된 것으로 나타났으며, 이를 통해 종합적인 방어 및 단일 알레르겐 탈감작 요법에 관한 논의의 틀이 재구성되었습니다. 2025년 3월에 발표된 2상 임상시험 결과에 따르면, 오마리주맙 단독 요법을 받은 환자에서 심각한 이상반응은 관찰되지 않았습니다. 이에 반해, 경구 면역요법에서는 이상반응 발생률이 높았고, 오말리주맙 치료군에서는 에피네프린 사용 빈도가 낮았기 때문에 용량 점진적 증량 과정에서 빈번하게 발생하는 반응을 우려하는 가족들에게 안전성을 최우선으로 하는 전략의 매력이 더욱 커졌습니다.

2-4주 간격으로 투여함으로써 여러 알레르겐에 대한 방어 효과를 얻을 수 있다는 점은 매일 투여해야 한다는 점이나 일상생활에 지장을 준다는 이유로 그동안 치료를 꺼려왔던 환자들을 끌어들이게 되어, 실제 적응증을 확대하는 결과를 가져올 것입니다. 이 임상 프로파일은 경구 치료에 내재된 일상적인 반응 위험에 시달리지 않고도 가족이 실질적인 보호 효과를 추구할 수 있도록 함으로써, 공동 의사결정의 새로운 기준을 확립합니다. 더 많은 의료기관이 생물학적 제제를 치료 과정에 도입함에 따라, 땅콩 알레르기 시장에서는 최대의 탈감작보다는 안정적인 안전성을 중시하는 환자층을 확보할 수 있을 것으로 예측됩니다.

OIT 적용 대상의 유아 확대로 인해 조기 시작과 보급이 가속화됨

2024년 7월 Palforzia의 적응증이 1세에서 3세까지 확대된 것은 매우 어린 아이들의 면역 가소성을 활용한 것으로, 이를 통해 적격 유아를 대상으로 한 감독 하의 용량 점진적 증량 과정에서 더 높은 내약성 임계값과 개선된 안전성 신호가 입증되었습니다. POSEIDON 임상시험에서 치료를 받은 유아의 61.2%가 종료 시 부하 시험에서 2,000mg의 땅콩 단백질에 대한 내성을 보인 반면, 위약군에서는 2.1%에 그쳤습니다. 또한, 조기에 치료를 시작할 경우 감작의 진행이 둔화되는 것과 일치하는 면역학적 징후가 관찰되었으며, 이는 새로 진단받은 가족을 대상으로 한 조기 집중 치료 접근법을 뒷받침하는 것입니다. REMS 제도 하에서는 각 용량 증량 단계마다 인증된 의료기관에서 관찰 하에 투여해야 했기 때문에 치료 접근 절차는 여전히 복잡했으며, 소아 알레르기 전문의가 부족하고 예약 대기 기간이 길어지는 지역에서는 일정 조정에 어려움이 발생했습니다.

접근성은 주마다 다르며, 많은 지역에서 후임자를 양성하기 위한 펠로우십 연수 프로그램이 부족하여, 이로 인해 적응증 도입 초기 단계에서의 확대가 제한되었습니다. 2026년 1월 판매 중단 결정(최종 공급 기한은 2026년 7월 31일)에 따라, 기존 환자의 지속적인 치료가 중단되었으며, 신규 치료 시작도 일시적으로 중단되었습니다. 이로 인해 REMS의 적용 범위를 벗어나도 사용이 가능하면서도 소아 환자에서 내약성이라는 장점을 유지할 수 있는 비경구 요법에 대한 관심이 높아졌습니다. 이러한 일련의 과정은 조기 개입의 임상적 근거를 유지하면서, 진료 체계가 감당할 수 있는 범위 내에서 치료법을 운영해 나가는 방향으로 전환하는 것입니다.

박스 경고, 아나필락시스 위험 및 EoE에 대한 우려가 OIT 도입을 제약하고 있습니다.

경구 면역요법은 반복적인 노출을 통해 역치를 높이지만, 그로 인해 용량 증량기 및 유지기 동안 치료 관련 반응의 위험도 높아집니다. 이러한 상충 관계에서는 철저한 상담과 신중한 모니터링이 필요합니다. 임상 경험과 학회 지침에서는 호산구 식도염의 발병 가능성 및 증상이 나타날 경우 치료 중단 필요성이 강조되고 있으며, 이에 따라 절차가 추가되고 전문의의 개입이 필요하지만, 많은 지역 의료기관에게 있어 이를 대규모로 유지하는 것은 어렵습니다. 투여에 따른 생활상의 제약, 즉 투여 후 활동 제한이나 컨디션이 좋지 않을 때의 프로토콜을 엄격히 준수해야 하는 점 등은 가족의 일상생활에서 유연성을 저해하는 요인입니다. 또한, 중대한 반응이 발생했을 경우 진료 기록 작성이나 의료법상 대응과 같은 부담이 발생하기 때문에 소규모 의료기관은 제공 범위를 제한하거나, 체계적인 상급 기관 연계 체계를 갖추고 있는 대학병원 등의 거점으로 환자를 의뢰하는 경향이 있습니다. 표준화된 경구용 땅콩 제품에 대한 REMS(위험 평가 및 완화 전략) 체계는 위험 감소를 목적으로 했으나, 동시에 의료기관 인증, 모니터링, 재고 관리와 같은 절차를 도입함으로써 운영상의 마찰을 가중시켰습니다. 시간이 지남에 따라 이러한 일련의 임상적·운영적 고려 사항들로 인해 일부 가족과 임상의들은 전신 반응의 위험이 낮은 치료법으로 눈을 돌리게 되었으며, 이는 땅콩 알레르기 시장의 환자 흐름에 영향을 미치고 있습니다.

부문별 분석

면역 요법의 연평균 성장률(CAGR) 15.63%는 아나필락시스 응급 처치에서 에피네프린이 차지하는 역할을 고려하더라도, 2025년에 에피네프린이 43.16%의 시장 점유율을 유지하고 있음에도 불구하고, 예방 의학으로의 지속적인 전환을 시사하고 있습니다. 경피 면역요법은 소아를 대상으로 한 3상 임상시험에서 양호한 결과를 보였으며, 46.6%의 반응률과 치료 관련 중대한 이상반응이 적었기 때문에 전신 반응의 위험을 줄이면서 역치 개선을 원하는 가족들에게 매력적인 선택지가 되고 있습니다. 오마리주맙이 IgE 매개성 식품 알레르기에 대한 승인을 받음에 따라, 정기적인 간격으로 교차 알레르겐을 예방할 수 있는 선택지가 추가되었습니다. 이는 유지 요법 기간 중 안전성과 내원 횟수 감소를 우선시하는 가족을 지원하기 위한 것입니다. 경구 면역요법은 일부 환자에서 더 높은 탈감작 효과를 보이지만, 매일 약을 꾸준히 복용해야 하고 더 빈번한 반응에 대한 내성이 요구되기 때문에 치료를 시작하거나 지속할 의사가 있는 가족의 범위는 제한적일 수밖에 없습니다.

표준 경구용 땅콩 면역요법이 2026년 중반에 시장에서 철수함에 따라, 의료기관에서는 적격 환자를 대상으로 패치 요법이나 생물학적 제제를 중점적으로 활용한 전환 경로를 계획하고 있으며, 이를 통해 보호자의 위험 수용도와 일치도를 높이고 치료 대상 환자 수를 확대할 수 있을 것으로 보입니다. 응급 치료제와 지지 요법은 여전히 기본적인 역할을 수행하고 있지만, 질환 자체를 개선하는 것은 아니기 때문에 장기적인 역치 변화에 기여하는 데에는 한계가 있습니다. 그 결과, 땅콩 알레르기 시장에서는 일상적인 노출 위험을 줄이는 치료법으로 성장의 초점이 이동하고 있으며, 연령대에 따른 다양한 선택지가 마련되어 있습니다. EPIT(경구 땅콩 면역요법) 및 생물학적 제제의 근거 기반은 앞으로도 계속해서 성숙해 나갈 것입니다. 또한, 이 두 가지 치료법 모두 많은 가정에서 매일 경구 투여하는 것보다 받아들이기 쉬운, 가족 중심의 절충안을 수반합니다. 면역요법의 보급 추세는 소아 코호트에서 여전히 가장 두드러지며, 패치형 제품에 대한 규제 당국과의 지속적인 협의와 생물학적 제제에 관한 실세계 등록 연구 결과를 바탕으로, 안전성, 실용성, 임상적 임계값 간의 균형을 고려하는 의료기관에서의 도입 양상이 더욱 확대될 것으로 기대됩니다. 이러한 과도기 동안, 임상의의 업무 흐름과 보험사의 정책이 여전히 진전의 주요 결정 요인이 될 것입니다. 의료기관이 효율적인 치료 프로토콜을 수립하고, 예측 가능한 보험 적용 기간을 확보할 수 있는 경우, 치료 시작률은 높아지는 경향을 보입니다. 승인 및 시행 시설의 수용 능력이 여전히 부족한 경우, 의료기관은 예방적 치료의 적절성을 평가하는 한편, 가족을 대상으로 확실한 응급 대응 계획을 유지합니다. 이러한 역학 관계로 인해 두 가지 접근 방식 모두 그 중요성을 유지하고 있지만, 땅콩 알레르기 시장의 성장 추세는 예방 의학에 유리하게 작용하고 있습니다.

지역별 분석

북미는 2025년 시장 가치의 36.53%를 차지했습니다. 고비용 예방 치료에 대응할 수 있는 긴밀한 전문 의료 네트워크와 보험 급여 체계가 조기 도입을 뒷받침하고 있지만, 사전 승인 절차가 복잡한 경우 보험사의 절차로 인해 도입이 지연될 가능성이 있습니다. 의료 인력공급 능력은 여전히 과제로 남아 있으며, 각국의 학회는 의료 서비스가 부족한 주에서 발생하는 접근성 격차를 해소하기 위해 졸업 후 의학 교육 정원 확대를 지속적으로 주장하고 있습니다. 캐나다의 공적 보험 제도는 형평성 목표를 지지하고 있지만, 각 주의 처방약 목록에서는 신제품을 신중하게 평가하고 있어, 치료 성과나 예산에 미치는 영향에 관한 데이터가 더 많이 수집될 때까지 보험 적용을 통한 접근이 지연될 가능성이 있습니다. 이러한 상황에서 의료기관이 일정 관리, 모니터링, 승인 절차를 신뢰할 수 있는 프로세스로 통합하고 있는 지역에서는 생물학적 제제나 신흥 패치 제제 시장 점유율이 확대될 것입니다. 진료 모델의 표준화와 보험사의 승인 절차가 안정화됨에 따라, 땅콩 알레르기 시장은 계속해서 확대될 전망입니다.

아시아태평양은 도시화에 따른 노출 양상의 변화, 진단 건수 증가, 전문의 양성 확대에 힘입어 2031년까지 연평균 성장률(CAGR) 16.57%를 기록하며 가장 빠르게 성장하는 지역이 될 것으로 전망됩니다. 중국에서는 발표된 연구 결과를 통해 대도시권 어린이들의 땅콩 과민반응 실태가 뚜렷이 드러난 반면, 전문 의료 서비스의 수용 능력 한계가 보고되고 있으며, 이로 인해 ‘골드 스탠다드’로 여겨지는 경구 식품 부하 검사에 대한 접근이 어려워져 실제 임상 현장에서의 치료 경로가 좁아지고 있습니다. 응급 대응 체계는 지역에 따라 다르며, 발표된 분석에 따르면 특정 지역에서는 병원에 도착하기 전 에피네프린 투여율이 낮은 것으로 나타났는데, 이는 치료 성과에 있어 간병인의 훈련과 의료기기의 접근성이 미치는 역할을 여실히 보여주고 있습니다. 일본에서는 매우 어린 아동에게서 감작이 확인되었음에도 불구하고, 위험을 회피하려는 처방 문화와 매일 투여에 대한 거부감으로 인해 경구 면역요법의 보급이 저해되고 있는 독특한 경향이 나타납니다. 그러나 경구 투여 이외의 치료법에 대한 근거가 축적됨에 따라, 이러한 상황은 점차 변화할 가능성이 있습니다. 동남아시아의 의료 시스템에서는 아나필락시스 교육이 활발히 이루어지고 있으며, 간병인이 신뢰할 수 있는 응급처치 계획을 갖춘 임상 현장은 예방적 치료 경로의 기반을 마련하고 있습니다. 승인된 예방적 선택지가 확대됨에 따라, 소아 의료에 중점을 두고 중산층 수요가 증가하고 있는 도시 지역에서는 땅콩 알레르기 관련 시장이 가속화될 것입니다.

유럽에서는 독일, 영국, 프랑스의 성숙한 알레르기 의료 인프라와 표준화된 경구용 제품의 도입 현황에 따른 편차, 그리고 추적 관찰 및 단계적 용량 증량을 위한 진료 체계의 지역적 차이가 공존하고 있습니다. 2026년 1월, 표준화된 경구 땅콩 면역요법의 중단이 결정됨에 따라 치료 중인 가족들에게 영향이 미쳤고, 소수의 환자를 치료하던 시설에서는 치료의 기세가 꺾였습니다. 이에 따라 비경구적 예방법이나 생물학적 보호에 대한 관심이 높아지고 있습니다. 남유럽에서는 보험 적용 절차와 진료소의 업무 흐름이 발전함에 따라 예방 요법이 점차 도입되고 있지만, 여전히 보수적인 치료 패턴이 유지되고 있습니다. 중동유럽에서는 체계적인 단계별 진료 및 모니터링을 지원할 수 있는 전문 의료 체계와 보험 급여 체계의 확충이 현재도 진행되고 있습니다. 중동 및 아프리카에서는 첨단 치료제를 수입하고 외국인 거주자가 주도하는 전문 의료 서비스에 의존하는 걸프 국가들에 수요가 집중되고 있는 반면, 많은 사하라 이남 시장에서는 다른 의료 과제와 우선순위가 상충하고 있어 도입 준비 단계에 있습니다. 남미에서는 민간 전문 의료 네트워크가 잘 갖춰진 주요 도시 지역에서 성장이 가장 두드러지며, 중산층 가정에서의 인지도도 높아지고 있습니다. 전반적으로, 이러한 동향은 치료법이 현지 보험 적용 범위, 의료 체계 및 보호자의 선호도에 부합함에 따라 땅콩 알레르기 시장의 꾸준한 지역적 확장을 뒷받침하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the peanut allergy market size is expected to increase from USD 0.56 billion in 2025 to USD 0.63 billion in 2026 and reach USD 1.14 billion by 2031, growing at a CAGR of 12.49% over 2026-2031.

This report is Segmented by Therapy Class / Modality (Immunotherapy, Epinephrine, Antihistamines, and Others), Route of Administration (Oral, Injectable, and Others), Patient Age Group (Toddlers, Children & Adolescents, and Adults), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market and Forecasted in Terms of Value (USD).

Global Peanut Allergy Market Trends and Insights

Anti-IgE Biologic Approval Expands Eligible Treated Population

The approval of omalizumab for IgE-mediated food allergy in February 2024 shifted care from single-allergen desensitization toward protection against accidental exposures across multiple foods, which aligns with day-to-day risk management for families who juggle several co-allergies. Pivotal OUtMATCH data showed that 68% of treated participants tolerated at least 600 mg of peanut protein without moderate-to-severe symptoms compared with 5% on placebo, while demonstrating concurrent gains for milk, egg, and cashew at thresholds relevant to real-world exposures, which reframed discussions about comprehensive protection versus single-allergen desensitization. Stage 2 results released in March 2025 reported no serious adverse events in patients receiving omalizumab monotherapy, compared with higher event rates in oral immunotherapy, and lower epinephrine use among omalizumab-treated patients, which reinforced the appeal of a safety-first strategy for families wary of frequent reactions during dose escalation.

The ability to protect across allergens at dosing intervals every 2 to 4 weeks can attract patients who previously avoided therapy due to daily dosing demands and lifestyle disruptions, broadening practical eligibility. The clinical profile sets a new baseline for shared decision-making by allowing families to pursue meaningful protection without navigating daily reaction risk inherent in oral protocols. As more centers integrate biologics into pathways, the peanut allergy market is expected to capture patients who value steady-state safety over maximal desensitization.

Toddler Expansion in OIT Indications Accelerates Earlier Initiation and Uptake

The July 2024 extension of Palforzia's indication to ages 1 to 3 leveraged immune plasticity in very young children, which supports higher tolerance thresholds and improved safety signals during supervised escalation in eligible toddlers. The POSEIDON trial reported that 61.2% of treated toddlers tolerated 2,000 mg of peanut protein at exit challenge compared with 2.1% on placebo, and noted immunologic signals consistent with blunting of sensitization trajectories when started early, which supports a front-loaded approach to care for newly diagnosed families. Access workflows remained complex under REMS, since each escalation step required supervised dosing at certified centers with observation, which created scheduling friction in regions with limited pediatric allergists and long appointment backlogs.

Accessibility varied by state, and multiple regions lacked fellowship training programs to replenish the pipeline, which constrained scaling during the indication's early window. The January 2026 discontinuation decision, with final availability through July 31, 2026, disrupted continuity for existing patients and paused new starts, which shifted focus to non-oral modalities that can operate outside REMS while maintaining pediatric tolerability advantages. This sequence preserves the clinical rationale for early intervention while redirecting operational momentum toward modalities that fit within practice capacity.

Boxed Warnings, Anaphylaxis Risk, and EoE Concerns Constrain OIT Adoption

Oral immunotherapy raises thresholds through repeated exposure, which also raises the risk of treatment-related reactions during escalation and maintenance, and this tradeoff requires extensive counseling and careful monitoring. Clinical experience and society guidance emphasize the possibility of eosinophilic esophagitis and the need to interrupt therapy if symptoms emerge, which adds procedural steps and specialist involvement that many community practices find hard to sustain at scale. Lifestyle constraints attached to dosing, including activity modifications after administration and strict adherence to protocols during illness, reduce day-to-day flexibility for families. Practices also face documentation and medicolegal overhead whenever severe reactions occur, which nudges smaller centers to limit offerings or refer to academic hubs that maintain robust escalation infrastructure. The REMS framework around standardized oral peanut products aimed to reduce risk, but it also introduced center certification, monitoring, and inventory management steps that increased operational friction. Over time, this set of clinical and operational considerations has directed some families and clinicians toward modalities with lower systemic reaction risk, which influences patient flow within the peanut allergy market.

Other drivers and restraints analyzed in the detailed report include:

- Non-Oral Modalities (EPIT, SLIT) Progress Toward Approval With Favorable Tolerability

- At-home/Self-Injection Pathways Reduce Visit Burden and Improve Persistence

- Coverage Variability and Delistings Hinder Access and Continuity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Immunotherapy's 15.63% CAGR signals a durable shift toward preventive care, even as epinephrine retained 43.16% share in 2025, given its role in anaphylaxis rescue. Epicutaneous immunotherapy posted favorable Phase 3 results in children, with a 46.6% responder rate and few treatment-related severe events, which makes it attractive for families that want threshold gains with lower systemic reaction risk. Omalizumab's approval for IgE-mediated food allergy added an option for cross-allergen protection at regular intervals, which supports families that prioritize safety and fewer clinic events during maintenance. Oral immunotherapy achieves higher desensitization for some patients but requires daily adherence and tolerance for more frequent reactions, which narrows the pool of families willing to initiate or persist.

As standardized oral peanut immunotherapy exits the market in mid-2026, practices are planning transition pathways that emphasize patches or biologics for eligible patients, which could expand treated volume through better alignment with caregiver risk tolerance. Rescue and supportive medications remain foundational but do not modify disease, which caps their contribution to long-run threshold changes. As a result, the peanut allergy market is reallocating growth toward modalities that reduce day-to-day exposure risk, with multiple age-tailored options. The evidence base for EPIT and biologics will continue to mature, and both modalities pair with family-centered tradeoffs that are easier to accept than daily oral dosing for many households. Immunotherapy's trajectory remains strongest in pediatric cohorts, and ongoing regulatory interactions for patch-based products and real-world registry experience for biologics are expected to deepen adoption patterns in centers that balance safety, practicality, and clinical thresholds. During this transition, clinician workflow and payer policy will remain the main governors of pace. Where practices can stand up efficient protocols and achieve predictable coverage windows, initiation rates tend to improve. Where authorization and site capacity remain tight, practices keep families on robust rescue plans while evaluating preventive fit. This dynamic keeps both tracks relevant, but the direction of growth within the peanut allergy market favors preventive care.

Geography Analysis

North America held 36.53% of the 2025 market value. Dense specialty networks and reimbursement pathways that can accommodate high-cost preventive therapies support early adoption, while payer steps can still slow starts when prior authorization is complex. Workforce capacity remains a flashpoint, and national societies continue to advocate for more graduate medical education slots to close access gaps in underserved states. Canada's public coverage model supports equitable goals, yet provincial formularies evaluate new products cautiously and can delay funded access until more outcome and budget impact data is assembled. In this context, biologics and emerging patches should gain share where centers harmonize scheduling, monitoring, and authorization steps into reliable flows. The peanut allergy market will continue to expand as practice models standardize and payer pathways stabilize.

Asia Pacific is projected to be the fastest-growing region at a 16.57% CAGR through 2031, driven by urbanization-linked exposure patterns, rising diagnoses, and expanding specialist training. In China, published work highlights meaningful peanut sensitization among children in metropolitan areas but also documents capacity limits in specialty care, which complicates access to gold-standard oral food challenges and narrows real-world treatment pathways. Emergency readiness varies across the region, and published analyses show low rates of pre-hospital epinephrine in specific locales, which underscores the role of caregiver training and device availability in outcomes. Japan presents a distinct pattern where risk-averse prescribing culture and daily dosing aversion have tempered oral immunotherapy uptake despite documented sensitization in very young children, which may shift gradually as non-oral modalities grow their evidence base. Southeast Asian health systems have been active in anaphylaxis education, and clinical settings that equip caregivers with reliable rescue plans are laying groundwork for preventive pathways. As authorized preventive options expand, the peanut allergy market should accelerate in urban hubs with strong pediatric focus and growing middle-class demand.

Europe combines mature allergy infrastructure in Germany, the UK, and France with uneven commissioning for standardized oral products and variable capacity for follow-up escalation visits. The January 2026 decision to discontinue standardized oral peanut immunotherapy affected families mid-treatment and reversed momentum in centers that had built small pipelines, which pushed attention toward non-oral preventive alternatives and biologic protection. Southern Europe retains more conservative treatment patterns, with gradual adoption of preventive modalities as coverage pathways and clinic workflows evolve. Central and Eastern Europe are still scaling specialty capacity and reimbursement frameworks that could support structured escalation visits and monitoring. The Middle East and Africa display concentrated demand in Gulf economies that import advanced therapeutics and lean on expatriate-driven specialty services, while many sub-Saharan markets are earlier in the readiness curve due to competing health priorities. South American growth is strongest in major urban centers with private specialty networks, where awareness is rising among middle-income families. Collectively, these dynamics support steady regional expansion of the peanut allergy market as modalities map onto local coverage, capacity, and caregiver preferences.

- Aimmune Therapeutics, Inc.

- ALK-Abello

- Alladapt Immunotherapeutics, Inc.

- Camallergy Ltd

- COUR Pharmaceuticals Development Company, Inc.

- DBV Technologies S.A.

- F. Hoffmann-La Roche Ltd

- Greer Laboratories, Inc.

- IgGenix, Inc.

- Intrommune Therapeutics, Inc.

- Novartis

- Prota Therapeutics Pty Ltd

- Regeneron Pharmaceuticals

- Sanofi

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Anti-IgE Biologic Approval Expands Eligible Treated Population

- 4.2.2 Toddler Expansion in OIT Indications Accelerates Earlier Initiation and Uptake

- 4.2.3 Non-Oral Modalities (EPIT, SLIT) Progress Toward Approval With Favorable Tolerability

- 4.2.4 At-home/Self-Injection Pathways Reduce Visit Burden and Improve Persistence

- 4.2.5 Adjunct Biologic + OIT Regimens Improve OIT Tolerability and Pass Rates

- 4.2.6 Multi-stakeholder Infrastructure (REMS-certified centers) Streamlines Implementation

- 4.3 Market Restraints

- 4.3.1 Boxed Warnings, Anaphylaxis Risk, and EoE Concerns Constrain OIT Adoption

- 4.3.2 Coverage Variability and Delistings Hinder Access and Continuity

- 4.3.3 Allergy/Immunology Workforce and Certified-Site Capacity Bottlenecks

- 4.3.4 Regional Product Withdrawals/Supply Transitions Disrupt Availability

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

5 Market Size & Growth Forecasts

- 5.1 By Therapy Class / Modality

- 5.1.1 Immunotherapy

- 5.1.2 Epinephrine

- 5.1.3 Antihistamines

- 5.1.4 Others

- 5.2 By Route of Administration

- 5.2.1 Oral

- 5.2.2 Injectable

- 5.2.3 Others

- 5.3 By Patient Age Group

- 5.3.1 Toddlers

- 5.3.2 Children & Adolescents

- 5.3.3 Adults

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 Aimmune Therapeutics, Inc.

- 6.3.2 ALK-Abello

- 6.3.3 Alladapt Immunotherapeutics, Inc.

- 6.3.4 Camallergy Ltd

- 6.3.5 COUR Pharmaceuticals Development Company, Inc.

- 6.3.6 DBV Technologies S.A.

- 6.3.7 F. Hoffmann-La Roche Ltd

- 6.3.8 Greer Laboratories, Inc.

- 6.3.9 IgGenix, Inc.

- 6.3.10 Intrommune Therapeutics, Inc.

- 6.3.11 Novartis Pharmaceuticals

- 6.3.12 Prota Therapeutics Pty Ltd

- 6.3.13 Regeneron Pharmaceuticals, Inc.

- 6.3.14 Sanofi S.A.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment