|

시장보고서

상품코드

2063608

PET 방사성 트레이서 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)PET Radiotracer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

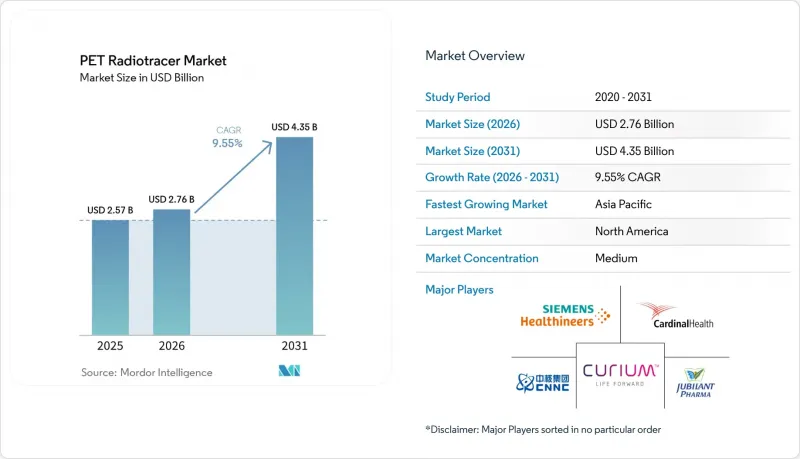

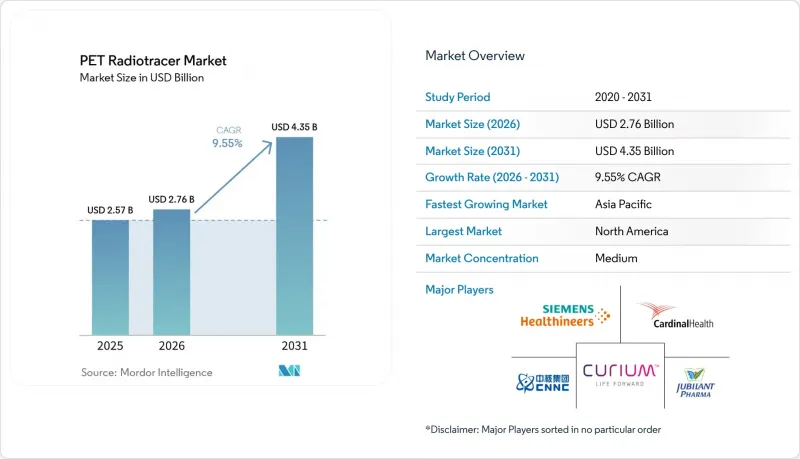

Mordor Intelligence에 의하면, PET 방사성 트레이서 시장 규모는 2025년 25억 7,000만 달러에서 2026년에는 27억 6,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 9.55%로 성장을 지속하여, 2031년까지 43억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 방사성 트레이서의 유형(18F-FDG, PSMA 표적 치료제(F-18, Ga-68), 아밀로이드 치료제, 18F-NaF(골), 기타), 동위원소(플루오르-18, 갈륨-68, 탄소-11, 지르코늄-89, 구리-64, 기타), 용도(종양학, 신경학, 심장학, 기타), 최종 사용자(병원, 영상진단센터, 기타) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 PET 방사성 트레이서 시장 동향 및 인사이트

종양학의 부담과 PET 검사 증가

2026년에는 미국에서 전립선암 신규 환자가 33만 4,000명, 사망자 수가 3만 6,000명을 넘어설 것으로 예측되는 등 암 발병률이 증가하고 있어, 다른 검사법으로는 한계가 있는 병기 판정, 치료 효과 평가, 재발 감지 분야에서 PET에 대한 의존도가 높아지고 있습니다. 테라노스틱스(치료 진단) 케어 모델의 통합이 진행됨에 따라, 진단용 PSMA-PET 및 소마토스타틴 수용체 PET가 방사성 리간드 요법과 연계되면서 치료 과정에서 확인 스캔이 필요해짐에 따라, 환자 1인당 영상 진단 빈도가 증가하고 있습니다. PSMAfore 연구에서 도출된 증거는 PSMA 기반 치료의 조기 도입과 더 우수한 영상학적 무재발 생존 기간을 뒷받침하고 있으며, 질병 경과에 있어 더 이른 시점에 PET를 활용하려는 움직임을 뒷받침하고 있습니다.

아시아태평양에서는 사이클로트론 및 PET 시설의 구축이 빠르게 진행되고 있으며, 중국의 원자로 기반 루테튬-177 생산 능력과 더불어 테라노스틱스 프로토콜의 활용 가능성이 높아지고 있습니다. PSMA 방사성 리간드 요법에 대한 PSA 반응률이 62.5%임을 보여주는 동아시아의 임상 경험은 다양한 환자군으로의 적용 확대를 뒷받침하고 있습니다.

미국 CMS의 별도 지급 제도가 트레이서 이용을 촉진

2025년 1월부터 시행되는 고액 기준액을 초과하는 진단용 방사성 의약품에 대한 지불을 분리하는 미국의 정책은 병원 외래 진료의 경제 구조를 재편하고, 비용 전가 이후 제품의 생존 가능성을 확보했습니다. 이로 인해 혁신을 저해하던 기존의 ‘볼륨 클리프(급격한 수요 감소)’가 완화되었습니다. 2026년에는 지수 연동형 기준치가 655달러로 상향 조정되어 인플레이션 대책이 강화됨과 동시에, 고가의 PET 트레이서에 대한 상환 설계의 안정성이 입증되었습니다.

CMS는 평균 판매 가격이 아닌, 병원의 청구 데이터를 기반으로 한 평균 단가를 기준으로 지급하지만, 이러한 분리 지급 방식은 이익률 하락을 억제하고 병원 및 외래 진료 센터 모두에서 제품 공급을 유지합니다. 패스스루 방식에서 일반 지불 방식으로의 전환은 이용 빈도가 낮은 제품의 경우 가격 변동을 초래할 가능성이 있지만, 이 체계는 기존의 포괄 지불(번들 페이먼트) 방식에 비해 여전히 접근성을 개선하고 있습니다. 중기적으로는 민간 보험사나 해외 지급 기관이 미국의 정책을 참고할 가능성이 높으며, 이는 PET 방사성 트레이서 시장의 보다 광범위한 보상 기준에 영향을 미칠 수 있습니다.

PET/CT의 막대한 설비 투자와 설치 장소의 제약

PET/CT 도입 및 설치 예산은 여전히 고액이며, 표준 기기의 수명 주기 내에서 처리 능력이 투자 회수 기준을 충족하지 못하는 환경에서는 도입이 제한됩니다. 해당 시설은 핫셀, 클린룸, 그리고 GMP 기준에 따른 제조 및 취급 기준을 준수하는 데 드는 추가 비용에 직면해 있으며, 이러한 비용에 더해 각국 규제 당국의 허가 절차가 복잡하다는 점도 부담으로 작용하고 있습니다. 승인까지 걸리는 기간, 용도지역 규제, 지역 사회의 반대 등으로 인해 지연이 발생하여 PET 설비의 지리적 분포에 불균형을 초래할 가능성이 있습니다. 2025년에 발표된 분석에 따르면, 단축 방향 시야 스캐너의 가동 시간을 연장하는 것은 기술 업그레이드보다 효율적이지는 않지만, 많은 의료 기관은 재정적 제약으로 인해 여전히 가동 시간 연장에 의존하고 있습니다. 국내 생산 부족과 일부 국가의 불균형한 상환 환경이 접근성 격차를 악화시켜, PET 서비스가 소수의 대도시권에 집중되는 요인이 되고 있습니다.

부문별 분석

2025년 기준으로, 플루오르-18 FDG는 PET 방사성 트레이서 시장 규모의 45.22%를 차지하고 있으며, 이는 종양학, 신경학, 심장학 분야에서 확고히 자리 잡은 사용 현황과 사이클로트론 및 PET/CT 시스템의 막대한 도입 대수를 반영한 것입니다. FDG의 폭넓은 임상적 적용성으로 인해 기준선 수요량은 안정적이지만, 포도당 대사 정보가 불충분한 사례에서 질환 특이적 약물의 사용이 확대됨에 따라 성장률은 둔화되고 있습니다. PSMA 표적 약물은 전립선암 치료 과정에서 진단과 치료 선택 모두에 중요한 역할을 하기 때문에 2031년까지 연평균 성장률(CAGR) 13.27%를 기록하며 가장 빠르게 성장하고 있는 방사성 트레이서 부문입니다.

피플포라스타트의 향후 계획에는 2026년 3월 FDA 승인을 받은 제조 최적화 제형이 포함되어 있으며, 이를 통해 배치 규모가 약 50% 증가하고, 핵심 생산 거점의 지리적 커버리지 확대가 기대됩니다. 발전기 기반의 갈륨-68 키트는 보관 기간을 연장함과 동시에 당일 조제가 가능하도록 하여, 사이클로트론을 보유하지 않은 소규모 병원에서도 PSMA-PET 영상 진단을 제공할 수 있도록 지원합니다. 동아시아에서는 서유럽인들과는 다른 유전체 프로파일에도 불구하고, PSMA 방사성 리간드 요법에 대한 PSA 수치의 현저한 반응이 확인되었으며, 이는 PSMA 기반 진단 건수에서 대상 환자층이 확대되고 있음을 뒷받침하고 있습니다.

임상 워크플로우의 변화는 PET 방사성 트레이서 시장에서 PSMA 약제가 다른 검사를 대체하는 것이 아니라, 오히려 수요를 확대시키는 이유를 여실히 보여주고 있습니다. PSMA 표적 치료의 각 대상 환자에 대해서는 표적 발현을 PET를 통해 확인해야 하므로, 이에 따라 진단 절차가 이미 확립된 경우에도 추가적인 검사가 실시됩니다. FDA 승인을 받은 4가지 PSMA 치료제 간의 경쟁적 역학은 차별화된 형식과 물류 시스템을 통해 전반적으로 처리 능력과 서비스 범위를 확대함으로써, 의료 제공업체들에게 더 폭넓은 접근성과 유연한 일정 수립을 가능하게 하고 있습니다. 이와 동시에, 소마토스타틴 수용체 트레이서, 아밀로이드 제제 및 골 트레이서는 신경내분비 종양, 알츠하이머병 및 전이 모니터링 분야에서 적용 가능한 용도를 확대되고 있습니다. 섬유아세포 활성화 단백질 및 기타 표적과 관련된 파이프라인의 동향은 고형암 전반에 걸쳐 향후 치료 옵션을 확대할 가능성이 있지만, 단기적인 성장은 여전히 전립선암 및 신경내분비 질환 적응증 분야에서 가장 두드러집니다. 이러한 동향들이 복합적으로 작용하여, PET 방사성 트레이서 시장에서 다양한 진단 기법을 아우르는 성장 요인을 강화하고 있습니다.

플루오르-18은 FDG의 보급과 반감기 110분 이내인 지역 영상진단센터에 서비스를 제공하는 집중형 사이클로트론 네트워크의 규모의 경제 효과 덕분에, 2025년에는 67.51%의 시장 점유율을 차지했습니다. ‘허브 앤 스포크’ 방식의 생산 체제는 중복성을 확보함으로써, 주요 도시권의 처리 능력이 높은 시설에서 의료기관의 일정 관리 위험을 줄이는 데 기여하고 있습니다. 갈륨-68은 2031년까지 연평균 성장률(CAGR)이 13.4%로, 가장 빠르게 성장하고 있는 동위원소군입니다. 이는 유연하고 주문형 조제를 선호하는 시설에서 PSMA 및 소마토스타틴 수용체 영상 촬영을 위한 발생기 기반 접근 방식이 장려되고 있기 때문입니다. 일부 시장에서는 발전기 비용이나 공급 제약이 걸림돌이 되어 왔으나, 기술적 개선과 국내 발전기 도입 노력에 힘입어 내구성과 효율성 문제에 대한 해결책 마련이 시작되고 있습니다.

사이클로트론을 이용한 갈륨-68 생산은 더 높은 수율과 지역적 공급 확대의 가능성을 내포하고 있으며, 규제 및 공정 요건을 충족하는 한 특정 지역에서 발생기를 보완하거나 대체할 가능성이 있습니다. 플루오린-18의 규모의 경제는 성장 지역 내 PET 생산 인프라에 대한 지속적인 투자를 통해 강화되고 있습니다. 그 예로는 여러 시설에 걸친 PET 네트워크의 확장, 수요가 높은 트레이서의 납기 단축 및 공급 탄력성 향상을 목적으로 한 생산 능력 확충 등을 들 수 있습니다.

면역 PET 지르코늄-89나 테라노스틱스 페어용 구리-64와 같은 진행 중인 동위원소 혁신은 임상 도구 세트를 다양화하며, 영상 진단과 치료 결정이 긴밀하게 연계되는 정밀 종양학으로의 전환과 부합합니다. 아시아태평양에서의 동위원소 생산 현지화는 수입 의존도를 더욱 낮추고, PET 검사 건수가 증가하고 있는 대규모 국가들에서 확장 가능한 상업적 공급을 뒷받침하고 있습니다. 이러한 변화들은 중앙 집중화를 통한 효율성과 분산화를 통한 접근성의 균형을 맞추면서 PET 방사성 트레이서 시장을 강화하고 있습니다.

지역별 분석

북미는 2025년에 42.32%를 기록하며 1위를 차지했습니다. 이는 여러 건의 FDA 승인, 명확한 보험 급여 체계, 그리고 CDMO 및 방사성 의약품 약국에서의 최근 생산 능력 투자에 힘입은 것으로, 이 모든 요소가 결합되어 상당한 처리 능력과 회복력을 제공합니다. 또한, 해당 지역에서는 방사성 의약품 분야에서 대규모 M&A도 발생하고 있으며, 이를 통해 통합된 공급망이 강화되고, 증가하는 PSMA 및 아밀로이드 영상 진단 수요에 대응하기 위한 상업 인프라가 확대되고 있습니다. 메디케어 외래 진료 지급 제도에 대한 지속적인 정책 개선은 고부가가치 추적 대상에 대한 경제적 인센티브를 유지하고 있으며, 이러한 환경은 민간 보험사의 의사 결정 및 시설 계획에 계속해서 영향을 미치고 있습니다. 임상시험 활동의 집중과 PET/CT 스캐너 도입 대수 증가 역시 북미 PET 방사성 트레이서 시장의 지속적인 선도적 지위를 뒷받침하고 있습니다.

아시아태평양은 동위원소 생산의 현지화, PET 제조 네트워크의 확대, 그리고 일본과 한국 등 국가들의 고밀도 의료 인프라에 힘입어 2031년까지 연평균 성장률(CAGR) 13.95%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 일본의 성숙한 핵의학 생태계는 최근 체결된 라이선싱 및 제조 계약과 맞물려, 규제 체계가 정비됨에 따라 PSMA 및 신경학 분야 전용 트레이서의 급속한 보급을 뒷받침하고 있습니다. 한국에서는 갈륨-68 발생기 기술의 발전을 비롯한 여러 동위원소에 대한 국내 생산 노력을 통해 수입 의존도를 낮추고, 중규모 병원에서의 이용 기회를 확대하는 것을 목표로 하고 있습니다. 중국 내 원자로 기반 루테튬-177의 일괄 생산은 해당 지역에 테라노스틱스의 도입을 전략적으로 지원할 뿐만 아니라, 해외 공급 제약에 대한 노출을 줄여줍니다. 이러한 동향들이 맞물려 다자간 확대가 촉진됨에 따라, 아시아태평양의 PET 방사성 트레이서 시장 규모는 예측 기간 동안 가속화될 전망입니다.

유럽에서는 노후화된 원자로, 운송 물류, 농축 물질에 대한 의존과 같은 구조적 취약성에 지속적으로 대응하는 한편, 국내 생산 확대 및 방사성 의약품 규제 체계의 조화를 위한 투자도 진행하고 있습니다. EU 차원의 제안에서는 원자재 공급원의 다각화, 인증 절차의 개선, 그리고 보다 탄력적인 공급망을 구축하기 위한 전략적 노력의 지속이 요구되고 있습니다. 서유럽 내 PET 네트워크 확장을 포함하여, 업계 각사가 추진하는 신규 생산 능력 확충은 종양학, 신경학 및 심장학 프로그램을 위한 트레이서 공급의 신뢰성을 높이는 것을 목표로 하고 있습니다.

남미에서는 역량 강화, 품질 시스템 및 교육을 중시하는 지역 협력 프로그램이 테라노스틱스의 활용 가능성을 높이고 그 보급을 촉진하도록 설계되어 있습니다. 한편, 대상 범위를 좁힌 각국의 승인을 통해 특정 방사성 의약품 시장 진입이 효율화되고 있습니다. 이러한 지역적 동향은 규제 당국의 지침 및 업계의 투자와 맞물려 PET 방사성 트레이서 시장의 성장세를 유지하는 데 기여하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the pET radiotracer market size is expected to grow from USD 2.57 billion in 2025 to USD 2.76 billion in 2026 and is forecast to reach USD 4.35 billion by 2031 at 9.55% CAGR over 2026-2031.

This report is Segmented by Radiotracer Type (18F-FDG, PSMA-Targeted Agents [F-18, Ga-68], Amyloid Agents, 18F-NaF [bone], and Others), Isotope (Fluorine-18, Gallium-68, Carbon-11, Zirconium-89, Copper-64, and Others), Application (Oncology, Neurology, Cardiology and Others), End User (Hospitals, Diagnostic Imaging Centers, and Others), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global PET Radiotracer Market Trends and Insights

Oncology Burden and PET Procedure Growth

Rising cancer incidence, including a projected 334,000 new U.S. prostate cancer cases and more than 36,000 deaths in 2026, intensifies reliance on PET for staging, response assessment, and recurrence detection where other modalities have limitations. The ongoing integration of theranostic care models links diagnostic PSMA-PET and somatostatin receptor PET with radioligand therapies, which increases imaging frequency per patient as treatment pathways require confirmation scans. Evidence from the PSMAfore study supporting earlier PSMA-based therapy adoption and better radiographic progression-free survival has encouraged use of PET earlier in the disease trajectory.

In Asia-Pacific, the rapid buildout of cyclotrons and PET facilities, complemented by reactor-based lutetium-177 capacity in China, enhances availability for theranostic protocols. East Asian clinical experience showing 62.5% PSA response rates to PSMA radioligand therapy supports expanding adoption across diverse patient profiles.

US CMS Separate Payment Boosts Tracer Access

The U.S. policy to separate payment for diagnostic radiopharmaceuticals above the high-cost threshold, effective January 2025, restructured hospital outpatient economics and preserved product viability after pass-through, which reduces the historical volume cliff that discouraged innovation. The indexed threshold increased to USD 655 for 2026, reinforcing inflation protection and signaling stability in reimbursement design for premium PET tracers.

While CMS pays based on mean unit cost from hospital claims rather than average sales price, the decoupled payment approach curbs margin compression and sustains product availability in both hospitals and outpatient centers. Transitions from pass-through to regular payment can create rate volatility for lower-utilization products, yet the framework still improves access relative to prior bundled-payment dynamics. Over the medium term, private insurers and international payers are likely to study U.S. policy for reference, which may influence broader reimbursement benchmarks for the PET radiotracer market.

High PET/CT Capex and Siting Constraints

PET/CT acquisition and installation budgets remain significant, which limits adoption in settings where throughput cannot meet return thresholds within standard equipment lifecycles. Facilities face additional costs for hot cells, cleanrooms, and compliance with GMP-grade manufacturing and handling standards, and these costs are coupled with licensing complexity across national regulatory bodies. Approval timelines, zoning restrictions, and community opposition can add to delays and create uneven geographic distribution of PET capacity. Analysis published in 2025 indicated that extending hours on short-axial-field-of-view scanners is less efficient than upgrading technology, but many providers still rely on extended hours due to capital constraints. Limited domestic production and uneven reimbursement environments in some countries exacerbate disparities in access, concentrating PET services in a few metropolitan corridors.

Other drivers and restraints analyzed in the detailed report include:

- PSMA-PET Adoption and Product Proliferation

- Alzheimer's Care Pathways Expand Amyloid/tau PET

- Short Half-lives and Isotope/Parent Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fluorine-18 FDG accounted for 45.22% share of the PET radiotracer market size in 2025, reflecting entrenched use across oncology, neurology, and cardiology and a large installed base of cyclotrons and PET/CT systems. FDG's broad clinical applicability keeps baseline volumes steady, although growth rates are moderating as disease-specific agents expand in scenarios where glucose metabolism is less informative. PSMA-targeted agents are the fastest-growing radiotracer class at a 13.27% CAGR through 2031, as they serve both diagnostic and therapy-selection roles in prostate cancer pathways.

Piflufolastat's trajectory, including an FDA-cleared manufacturing-optimized formulation in March 2026 that increases batch sizes by about 50%, supports broader geographic coverage from central production hubs. Generator-based gallium-68 kits enable same-day preparation with improved shelf life, which helps smaller hospitals without cyclotrons offer PSMA-PET imaging. East Asian evidence of strong PSA response to PSMA radioligand therapy, despite different genomic profiles compared with Western populations, supports a broadening addressable base for PSMA-driven diagnostic volumes.

Clinical workflow changes underscore why PSMA agents amplify demand rather than substitute for other tests in the PET radiotracer market. Each candidate for PSMA-directed therapy requires PET confirmation of target expression, which adds scans even when the diagnostic pathway is already in place. Competitive dynamics across four FDA-cleared PSMA agents collectively expand capacity and reach through differentiated formats and logistics, resulting in wider access and more flexible scheduling for providers. In parallel, somatostatin receptor tracers, amyloid agents, and bone tracers extend addressable uses in neuroendocrine tumors, Alzheimer's disease, and metastatic surveillance. Pipeline activity in fibroblast activation protein and other targets may add future options across solid tumors, though near-term growth remains most intense in prostate cancer and neuroendocrine indications. Together, these trends reinforce diversified growth drivers across modalities for the PET radiotracer market.

Fluorine-18 held 67.51% share in 2025 on the strength of FDG ubiquity and scale advantages in centralized cyclotron networks that serve regional imaging centers within the 110-minute half-life window. Hub-and-spoke production architectures enable redundancy and help providers manage scheduling risks for high-throughput sites in major metropolitan areas. Gallium-68 is the fastest-growing isotope class at a 13.4% CAGR through 2031, driven by generator-based access for PSMA and somatostatin receptor imaging where sites prefer flexible, on-demand preparation. Generator costs and supply constraints have been hurdles in some markets, though technological improvements and domestic generator initiatives are beginning to address longevity and efficiency.

Cyclotron-based gallium-68 production offers higher yields and regional distribution potential that can complement or replace generators in select geographies, subject to regulatory and process requirements. Fluorine-18's scale economics are reinforced by continuous investment in PET manufacturing infrastructure across growth corridors. Examples include multi-site PET network expansions and capacity additions that aim to reduce delivery lead times and increase supply resilience for high-demand tracers.

Ongoing isotope innovation, such as zirconium-89 for immuno-PET and copper-64 for theranostic pairs, diversifies the clinical toolkit and aligns with the shift toward precision oncology where imaging and therapy decisions are closely coupled. Localization of isotope production in Asia-Pacific further reduces import dependence and supports scalable commercial supply in large countries with rising PET volumes. These changes strengthen the PET radiotracer market by balancing centralized efficiency with decentralized access.

Geography Analysis

North America led with 42.32% in 2025, supported by multiple FDA approvals, clear reimbursement frameworks, and recent capacity investments across CDMOs and radiopharmacies that together add meaningful throughput and resilience. The region has also seen substantial M&A in radiopharmaceuticals, which strengthens integrated supply chains and scales commercial infrastructure to handle growing volumes of PSMA and amyloid imaging. Ongoing policy refinements in Medicare outpatient payment systems sustain economic incentives for high-value tracers, and that environment continues to influence private payer decisions and facility planning. The concentration of clinical trial activity and a large installed base of PET/CT scanners also support continued leadership of the PET radiotracer market in North America.

Asia-Pacific is the fastest-growing region with a 13.95% CAGR through 2031, driven by the localization of isotope production, the expansion of PET manufacturing networks, and high-density healthcare infrastructure in countries like Japan and South Korea. Japan's mature ecosystem for nuclear medicine, combined with recent licensing and manufacturing agreements, positions rapid adoption for PSMA and neurology-focused tracers as regulatory pathways mature. In South Korea, domestic production initiatives for multiple isotopes, including advances in gallium-68 generator technology, aim to reduce import reliance and broaden access for mid-tier hospitals. China's reactor-based lutetium-177 batch production provides strategic support for regional theranostic adoption and reduces exposure to overseas supply constraints. Together, these developments reinforce a multi-country expansion where the PET radiotracer market size for Asia-Pacific is set to accelerate over the forecast horizon.

Europe continues to address structural vulnerabilities linked to aging reactors, transport logistics, and enriched material dependencies, while also investing to expand domestic production and harmonize regulatory frameworks for radiopharmaceuticals. EU-level recommendations seek to diversify raw material supply, improve certification processes, and continue strategic initiatives to build a more resilient supply chain. New capacity additions from industry players, including expanded PET networks in Western Europe, aim to enhance reliability of tracer supply for oncology, neurology, and cardiology programs.

In South America, regional collaboration programs that emphasize capacity building, quality systems, and training are designed to improve availability and foster adoption of theranostics, while targeted national approvals streamline market entry for select radiopharmaceuticals. These regional moves, along with agency guidance and industry investment, help sustain momentum for the PET radiotracer market.

- Advanced Accelerator Applications SA

- Alliance Medical Limited

- Blue Earth Diagnostics

- Cardinal Health

- China lsotope & Radiation Corporation

- Curium Pharma

- Cyclotek

- Eckert & Ziegler

- GE Healthcare

- IBA Radiopharma

- Isologic Innovative Radiopharmaceuticals

- Jubilant Pharma Limited

- Lantheus

- Nihon Medi-Physics Co.,Ltd.

- NTP Radioisotopes

- Siemens Healthineers

- SOFIE

- Telix Pharmaceuticals Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Oncology Burden and PET Procedure Growth

- 4.2.2 US CMS Separate Payment Boosts Tracer Access

- 4.2.3 PSMA-PET Adoption and Product Proliferation

- 4.2.4 Alzheimers Care Pathways Expand Amyloid/tau PET

- 4.2.5 Consolidation and CDMO Capacity Expand Supply

- 4.2.6 Ga-68 Generator Access Enables Decentralized PET

- 4.3 Market Restraints

- 4.3.1 High PET/CT Capex and Siting Constraints

- 4.3.2 Short Half-lives and Isotope/Parent Shortages

- 4.3.3 Staffing and GMP Compliance Bottlenecks

- 4.3.4 Tariff/trade Uncertainties Raise Generator Input Costs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Radiotracer Type

- 5.1.1 18F-FDG

- 5.1.2 PSMA-targeted Agents (F-18, Ga-68)

- 5.1.3 Somatostatin Receptor Agents (Ga-68 DOTATATE/DOTATOC/DOTANOC)

- 5.1.4 Amyloid Agents (F-18 florbetapir, flutemetamol, florbetaben)

- 5.1.5 18F-NaF

- 5.1.6 Others (Neurology Amino-Acid Tracers, Inflammation & Infection Tracers)

- 5.2 By Isotope

- 5.2.1 Fluorine-18

- 5.2.2 Gallium-68

- 5.2.3 Carbon-11

- 5.2.4 Zirconium-89

- 5.2.5 Copper-64

- 5.2.6 Others (Oxygen-15, Nitrogen-13, Rubidium-82, etc)

- 5.3 By Application

- 5.3.1 Oncology

- 5.3.2 Neurology

- 5.3.3 Cardiology

- 5.3.4 Others (Inflammation & Infection, Drug Development & Theranostic Selection)

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Diagnostic Imaging Centers

- 5.4.3 Others (Academic & Research Institutes, Nuclear Medicine Clinics)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Advanced Accelerator Applications SA

- 6.3.2 Alliance Medical Limited

- 6.3.3 Blue Earth Diagnostics

- 6.3.4 Cardinal Health

- 6.3.5 China lsotope & Radiation Corporation

- 6.3.6 Curium

- 6.3.7 Cyclotek

- 6.3.8 Eckert & Ziegler

- 6.3.9 GE HealthCare

- 6.3.10 IBA Radiopharma

- 6.3.11 Isologic Innovative Radiopharmaceuticals

- 6.3.12 Jubilant Pharma Limited

- 6.3.13 Lantheus

- 6.3.14 Nihon Medi-Physics Co.,Ltd.

- 6.3.15 NTP Radioisotopes SOC Ltd

- 6.3.16 Siemens Healthineers AG

- 6.3.17 SOFIE

- 6.3.18 Telix Pharmaceuticals Limited

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment